TNRSF - Tenaris: Supportive Fundamentals And High Capital Returns

2023-11-09 08:27:18 ET

Summary

- Tenaris is a leading manufacturer of pipes and related services with a strong market share and a global presence.

- The company is set to benefit from supportive market fundamentals in the US and internationally, with strong demand and reduced supply.

- Tenaris has a future beyond oil and gas, particularly in carbon capture and hydrogen technologies, which will drive its growth in the green transition.

- We expect significant cash generation and higher capital returns over the next years and estimate a higher than 20% IRR.

We present our note on Tenaris ( TS ), a leading manufacturer of pipes and related services. We find the supportive fundamentals, strong balance sheet, and massive cash generation combined with a cheap valuation appealing. We will provide a brief overview of the firm and its activities, analyze market fundamentals and other key value drivers, and value Tenaris’ equity. We have a Buy rating on Tenaris.

A brief overview of Tenaris

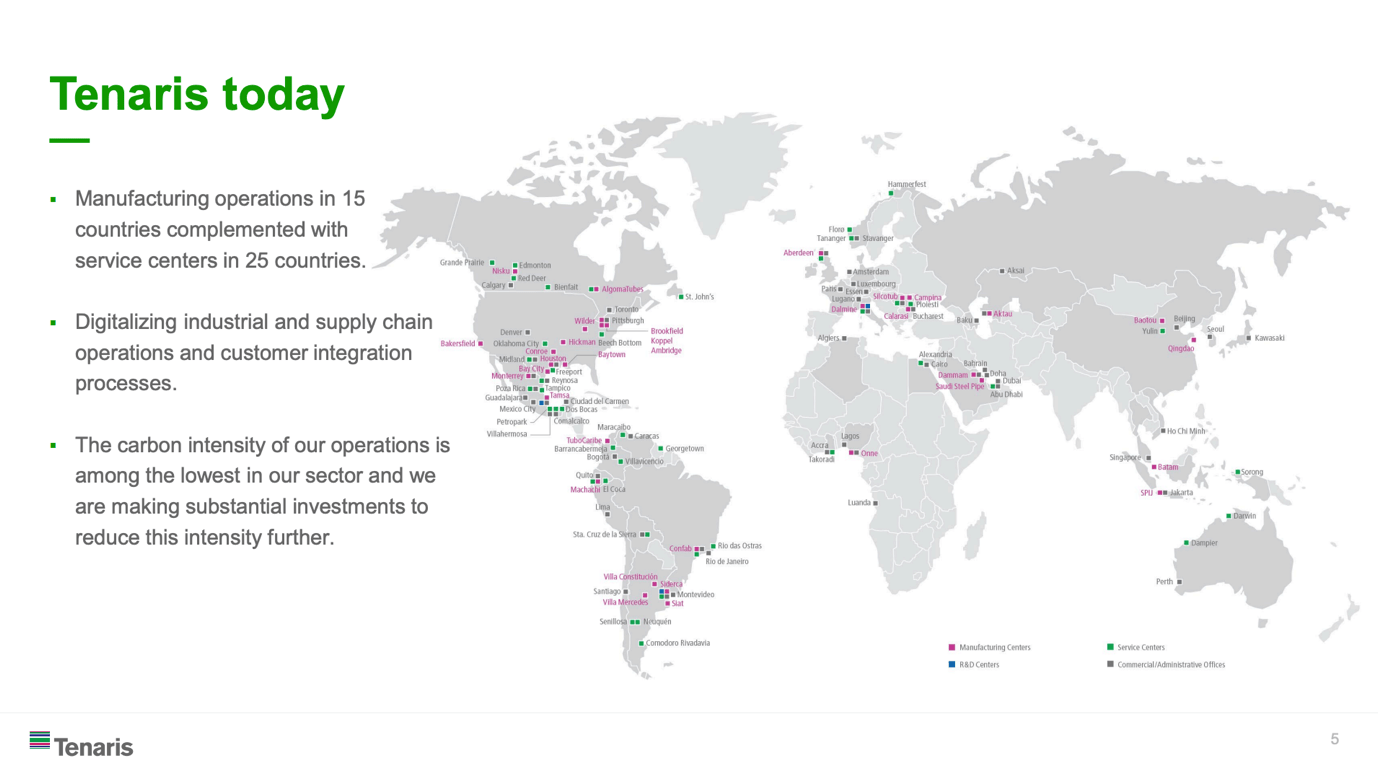

Tenaris is a global supplier of tubes and related services for the energy industry and certain other industrial applications. It engineers and designs casings, tubing line pipes and mechanical pipes. Tenaris’ manufacturing system integrates steelmaking, pipe rolling and forming, heat treatment, threading, and finishing. The company has a research and development network focused on enhancing the portfolio and improving processes. The company has a strong market share, especially in pipelines, offshore, and South America. Tenaris employs more than 25k people and is present in all continents. The founding Rocca family owns ca. 60% of the shares, and Mr. Paolo Rocca serves as Chairman of the Board and CEO. Tenaris has a current market capitalization of ca. $20 billion.

{kind=link}

Supportive fundamentals

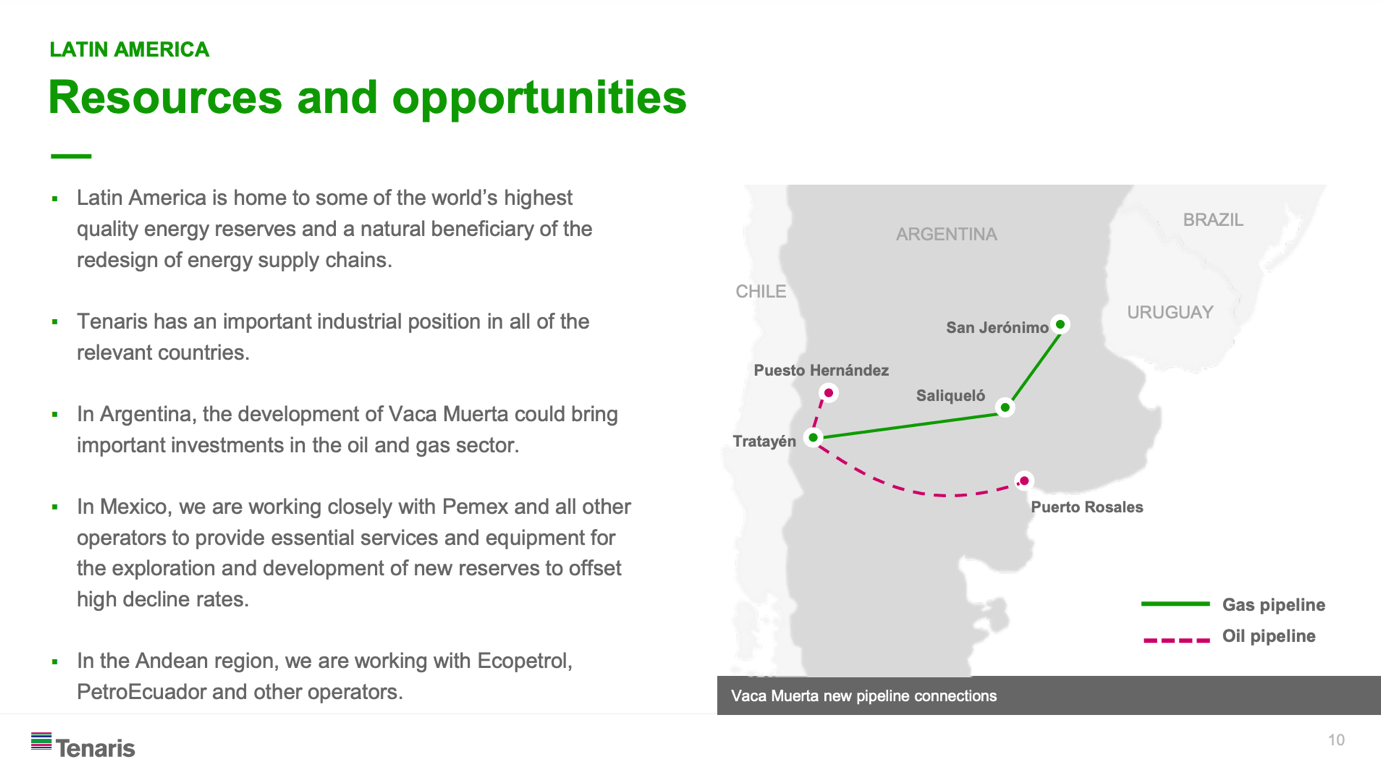

Tenaris is set to benefit from highly supportive market fundamentals in the US and internationally. Earlier in the year the US market was under pressure due to increased capital discipline from US oil and gas operators (and a lower rig count as a result) and increasing OCTG imports. Despite temporary pricing pressure, fundamentals remain robust as demand remains stable and supply has been significantly reduced over the last decade. Major plants are structurally closed and effectively impossible to reopen, hence the local supply is insufficient, and the US OCTG market relies on imports. The international market has been strong year-to-date, surpassing expectations, and Tenaris’ key markets such as Latin America have been very active. We are constructive on E&P capex outlook (also supported by IEA 2030 projections) on the back of strong oil and gas prices, and we expect Tenaris to benefit significantly.

{kind=link}

Navigating the green transition

Despite some market participants’ perceptions, Tenaris has a future beyond oil and gas, namely in carbon capture and hydrogen technologies. Carbon capture needs to be significantly scaled up to meet energy transition targets and tubes and pipelines are needed for transportation. The high pressure of corrosiveness of CO2 requires high-performance alloys. Select current technologies within the existing product portfolios that are usable for these purposes, benefiting OCTG companies.

Q3 Results

Tenaris reported robust Q3 results beating analyst consensus expectations and company guidance. EBITDA came in at $1 billion (31% margin) and FCF came in at $1.1 billion, also positively impacted by a working capital release. Year-to-date FCF stands at $3.1 billion and the company has a $3.3 billion net cash position. More than $1.4 billion of capital returns were approved, out of which $1.2 billion of share buybacks or around 6% of outstanding shares. $300 million has been already implemented. The company has a constructive outlook on the market, expecting a recovery in US activity and increased offshore drilling. We believe this set of results confirms our view on Tenaris.

Valuation and investment recommendation

We value OCTG companies using EV/EBITDA multiples and FCF yields. Our assumptions are conservative, and our estimates are largely in line with sell-side consensus. We forecast $13.3 billion of sales in FY2024e and an EBITDA of $3.6 billion (at a 27% EBITDA margin) reflecting the conservative end of our constructive fundamental outlook. EBITDA could come in well above $4 billion if the US market recovers steeply – which is not baked into the consensus and would be a significant positive surprise. We forecast a Free Cash Flow of $2.5 billion and we expect FCF generation to remain strong over the mid-term i.e., above $2 billion per annum, driving capital returns higher while maintaining a robust balance sheet. We expect an increase in the stable normal dividend (likely higher than 55c per share) and significant special dividends until FY2025e. We expect a total of between $5.5 - 6 billion of shareholder distributions between the current fiscal year and FY2025, amounting to nearly 30% of the market capitalization. We believe the dividend increase is a major catalyst for the stock.

We value Tenaris at 7x forward EV/EBITDA, lower than the 9x 5-year EV/EBITDA ratio average. We obtain an enterprise value of $25.2 billion and after making EV adjustments we arrive at an equity value of $28.5 billion implying a share price of $48 per share or 43% upside. Alternatively, we value Tenaris using FCF yields. Using a normalized FCF of $2.1 billion, we apply a 9% target FCF yield (derived from a 10% discount rate and 1% growth rate), and we arrive at a target EV of $23.3 billion or an equity value of $26.6 billion implying 33% upside. We can apply various valuation methodologies and perform a range of sensitivity analyses, but we believe it is evident that even with unoptimistic underlying assumptions Tenaris shares are undervalued by more than 30%. Combined with shareholder distributions at more than 30% of the current market capitalization, we estimate Tenaris offers 20%+ IRR over the mid-term and is one of the most attractive names in the energy services space.

Risks

Downside risks include but are not limited to deteriorating macroeconomic conditions, lower than expected oil and gas prices, lower than expected oil and gas capex, increased competition from reopening plants i.e., a return of capacity, increased international capacity especially in Asia, more stringent fracking regulation, antitrust regulation in the US, technological risk, energy transition risk, governance risk, legal risk (e.g., corruption cases), etc.

Conclusion

Given the supportive backdrop, valuation upside, and high capital returns to shareholders, we recommend buying Tenaris shares.

For further details see:

Tenaris: Supportive Fundamentals And High Capital Returns