TCTZF - Tencent: Deep Value For Long-Term Investors

2023-11-26 00:09:29 ET

Summary

- Tencent reported better-than-expected Q3 results, with double-digit Y/Y top-line growth and a decent EPS beat.

- The company's core services, social networks, and gaming continue to generate the bulk of its revenues. Online advertising revenues soared 20% Y/Y.

- Tencent's FinTech business is growing in importance and has significant gross margin momentum, contributing to its overall growth.

- The multi-media conglomerate generates a ton of free cash flow, and shares are a bargain given their potential for EPS growth.

Last week, Chinese internet company Tencent Holdings Limited ( OTCPK:TCEHY ) reported better-than-expected results for the third quarter. Tencent generated double-digit top line growth in Q3’23 and remains a highly promising, large-cap multi-media investment in China, in my opinion, despite fears over government crackdowns, slowing post-pandemic growth, and even when considering other factors such as a potential invasion of Taiwan. Tencent represents deep free cash flow value for investors who want to bet on China’s online economy. With shares trading at a 16X P/E ratio and the FinTech business having momentum, I believe the risk profile remains widely skewed to the upside!

Previous rating

I rated Tencent a strong buy two years ago -- Crazy Undervalued, Don't Be Distracted By Delisting Fears -- while the company was caught up, like Baidu ( BIDU ) and Alibaba ( BABA ), in a major government crackdown and investors feared a potential delisting of Chinese ADRs. Shares of Tencent have revalued approximately 15% lower since, but they have outperformed Baidu and Alibaba. Considering that Tencent continues to grow at healthy rates, is widely free cash flow-profitable, and has growth opportunities in FinTech, I believe the risk profile remains favorable for long-term investors.

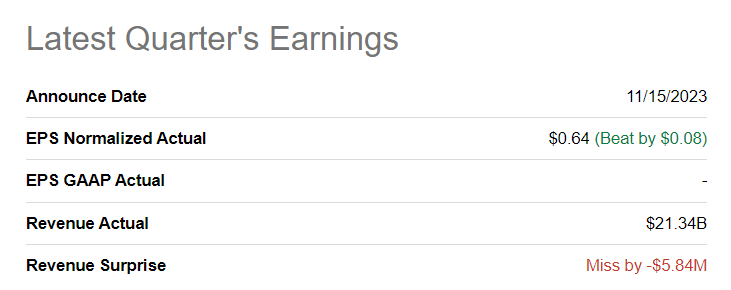

Tencent beat earnings estimates for Q3'23

In the third quarter, the Chinese multi-media conglomerate earned $0.64 per share in adjusted earnings on revenues of $21.34B. The earnings figure beat the consensus estimate by $0.08 per share.

{kind=link}

Strong revenue momentum, growing FinTech importance

Tencent -- known outside of China largely for its ownership of the most popular messaging app WeChat (which includes mobile payment functionality) -- has assembled an impressive empire of online-focused businesses and the company now has a market cap of $400B which is about half the market value of Meta Platforms ( META ), the most comparable U.S. company.

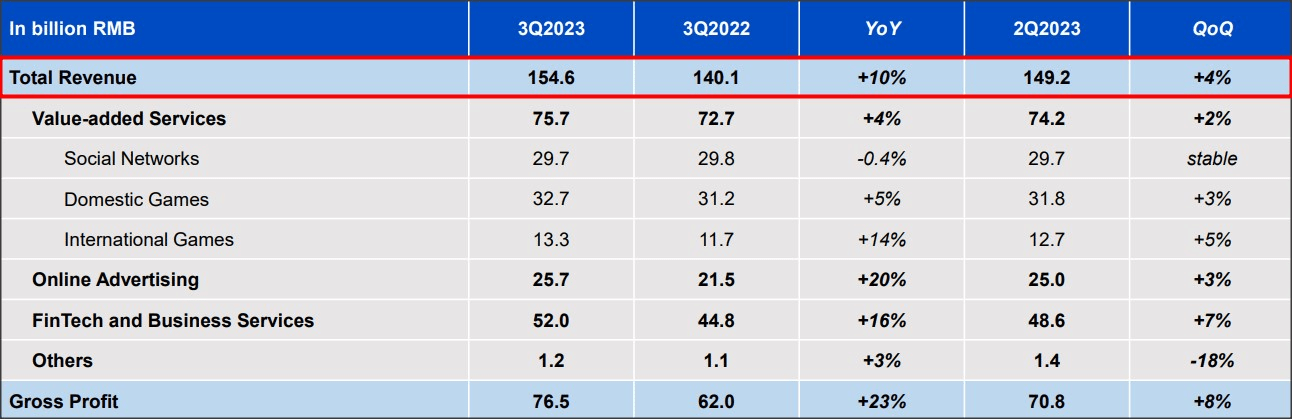

In the third quarter, Tencent generated 154.6B Chinese Yuan ($21.5B) in revenues from its vast portfolio of social media platforms, online gaming businesses, and ventures in the FinTech arena.

{kind=link}

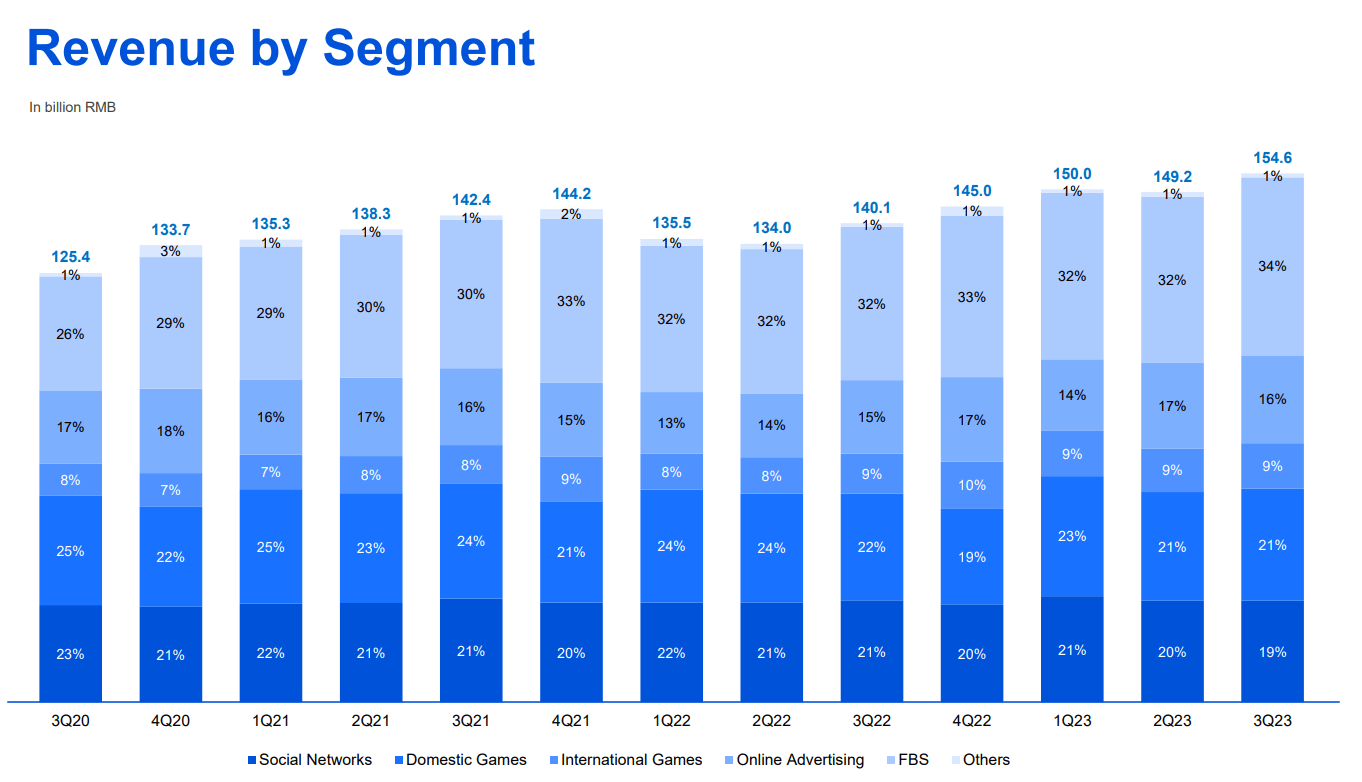

The breakdown of Tencent’s revenues shows that the company continues to rely on its core services -- social networks and gaming -- in order to generate the bulk of its revenues. These services together generated 75.7B Chinese Yuan ($10.5B) in revenues, showing an increase of 4% year over year, and they accounted for approximately 49% of Tencent’s consolidated revenues.

Online advertising revenues soared 20% year over year to 25.7B Chinese Yuan ($3.6B) due to growing ad demand for Tencent’s Video Accounts and mobile ad network.

FinTech and Business Services generated 52.0B Chinese Yuan ($7.2B) in revenues and accounted for a growing 34% top line share (the revenue share in Q3'22 was 32%). Tencent’s FinTech and Business Services have steadily grown in importance for the multi-media conglomerate, in part because the segment is growing faster than its core services and product adoption is rising.

{kind=link}

FinTech opportunity

Tencent is in a unique position to build a significant FinTech business that is integrated with its other businesses and the company can leverage the strength of its social media and online communications platforms to drive its growth. WeChat, for example, had 1.34B monthly active users in the third quarter, making it by far the largest messaging app in China.

Tencent is building a FinTech ecosystem that utilizes the wide adoption of WeChat Pay or QQ wallet which allows users to access e-banking services of major domestic banks. Tencent's Tenpay is now a leading FinTech brand in China whose instant-payment functionality can be used on more than 200,000 shopping websites as well. Tencent's FinTech arm charges fees for its mobile payment and transaction services and may therefore, in the long term, be a digital payments giant in its own right. In the longer term, I expect Tencent to develop its payments arm into a fully integrated FinTech operation facilitating cross border payments, offering wealth management services and insurance products, etc.

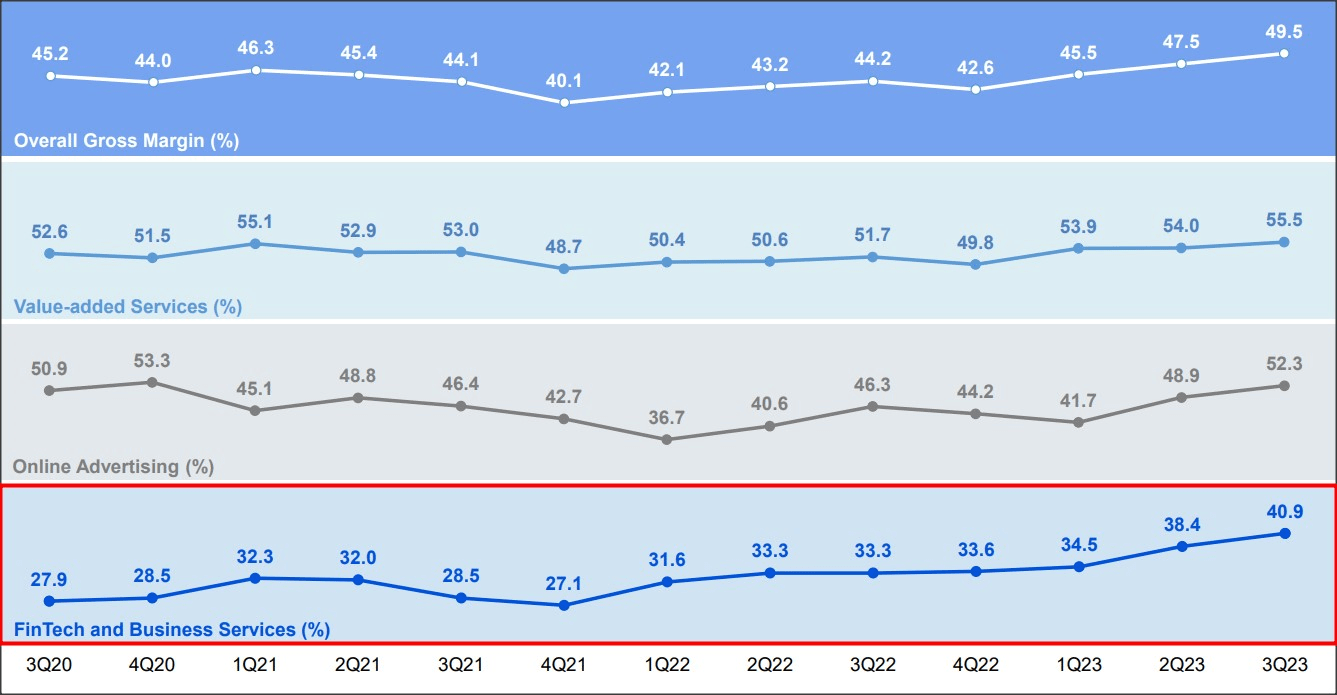

Tencent’s FinTech operations are seeing significant momentum and generated the second-highest top line growth rate in the third quarter (+16% Y/Y). The segment is not only growing quickly (due chiefly due to growing commercial adoption) but also seeing significant gross margin improvements which could make the FinTech business one of the most valuable businesses within Tencent in the future.

In the third quarter, Tencent's FinTech segment generated a gross margin of 40.9% which is below the gross margins of Tencent's core services (social networks & games) and online advertising. However, no other business is seeing its segment gross margins grow as quickly as FinTech/Business Services: in the last three years, both core services and online ads increased their gross margins in the low-to-mid single digits while FinTech-related gross margins soared 47% which has also been a main driver for Tencent's consolidated gross margin growth.

{kind=link}

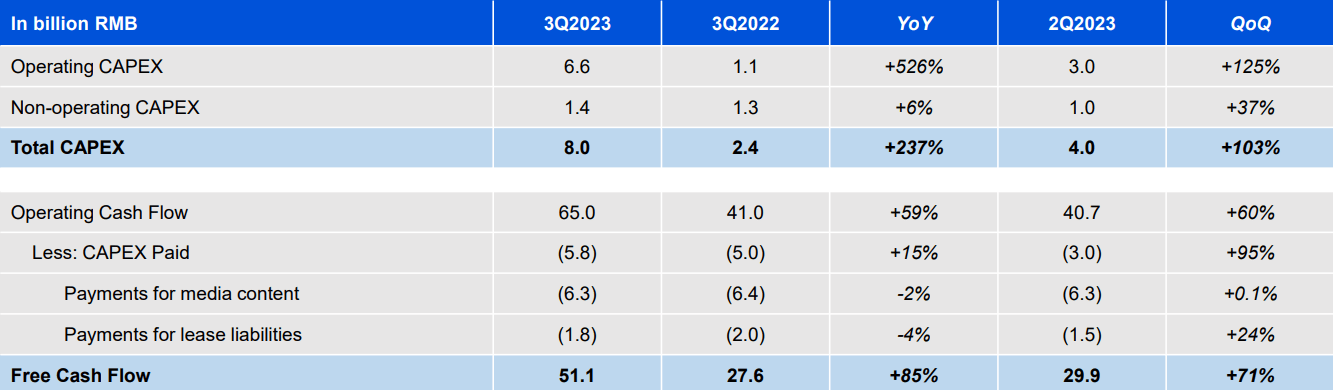

Tencent’s free cash flow

Like Meta Platforms, Tencent is a very free cash flow-profitable enterprise and it generated 51.1B Chinese Yuan ($7.1B) in free cash flow in the third quarter, showing 85% year-over-year growth. This calculates to a free cash flow margin of 33% compared to an FCF margin of 20% in the year-earlier period. These free cash flow margins are impressive and are not that far removed from Meta Platforms' mind-boggling free cash flow margins of 40% .

{kind=link}

Tencent’s valuation

Tencent is an attractively valued large-cap Chinese company: shares of Tencent are valued at 16X FY 2024 earnings which makes the firm more expensive than either Alibaba or Baidu. However, Tencent has by far the highest expected EPS growth at 17% (more than twice Alibaba's projected EPS growth). Tencent could, in my opinion, given its double-digit EPS growth, easily trade at 20X P/E which implies a fair value closer to $53 (28% revaluation potential). Alibaba, due to the introduction of a dividend as well as enormous free cash flow is the reason why I rate the e-commerce company a buy as well: Alibaba Is Now A Capital Return Play .

| Tencent |

| Alibaba |

| Baidu |

| Est. Earnings FY 2024 |

| $2.64 |

| $9.85 |

| $10.84 |

| Earnings Growth 2024 |

| 17% |

| 8% |

| 4% |

| P/E Ratio |

| 15.7X |

| 8.0X |

| 10.5X |

(Source: Author)

Risks with Tencent

Tencent is a large-cap Chinese multi-media company that is subject to significant regulation and exposed to the whims of the Chinese Communist Party. Government crackdowns on Tencent’s multiple businesses are a risk factor for investors as much as slowing growth in the Chinese economy is. A potential invasion of Taiwan may also be considered a short-term risk factor, but I don't see how this would ultimately affect the long-term value of Tencent's online businesses. What would change my mind about Tencent is if the government forced Tencent to divest its FinTech business or if the firm’s free cash flow margins suffered a decline.

Final thoughts

Tencent is seeing double-digit revenue momentum and the importance of the FinTech business within the multi-media company is growing. FinTech is seeing sustained gross margin tailwinds as the company made the growth of this business a priority. Gross margin growth as well as free cash flow strength are two top reasons for investors to buy shares of Tencent for a growth-focused portfolio. Tencent is not as cheap as Alibaba or Baidu, but the company is growing its EPS faster which makes shares attractive at a 16X P/E ratio. Even when considering China-specific risks, I believe the risk profile for Tencent is widely skewed to the upside!

For further details see:

Tencent: Deep Value For Long-Term Investors