BABAF - Tencent: More Powerful Than You Think

2024-01-08 08:00:00 ET

Summary

- Despite concerns over Chinese government restrictions, Chinese companies like Tencent continue to generate significant cash flow.

- Tencent's dominance extends beyond China, with its products and services being widely used internationally.

- Tencent's business segments include gaming, social networks, advertising, video streaming, music, cloud services, and strategic investments.

It has been three years that many investors have been avoiding Chinese companies regardless of their fundamentals. The continuous restrictions and sanctions imposed by the Chinese government have spread a strong feeling of distrust; perhaps too much.

The underlying thesis is that no Chinese company is truly independent in its operations, which is true; however, these companies continue to generate a huge amount of cash, which is why it is worth investigating further.

After analyzing Alibaba ( BABA ) a few weeks ago, now it is the turn of the other giant: Tencent ( TCEHY ).

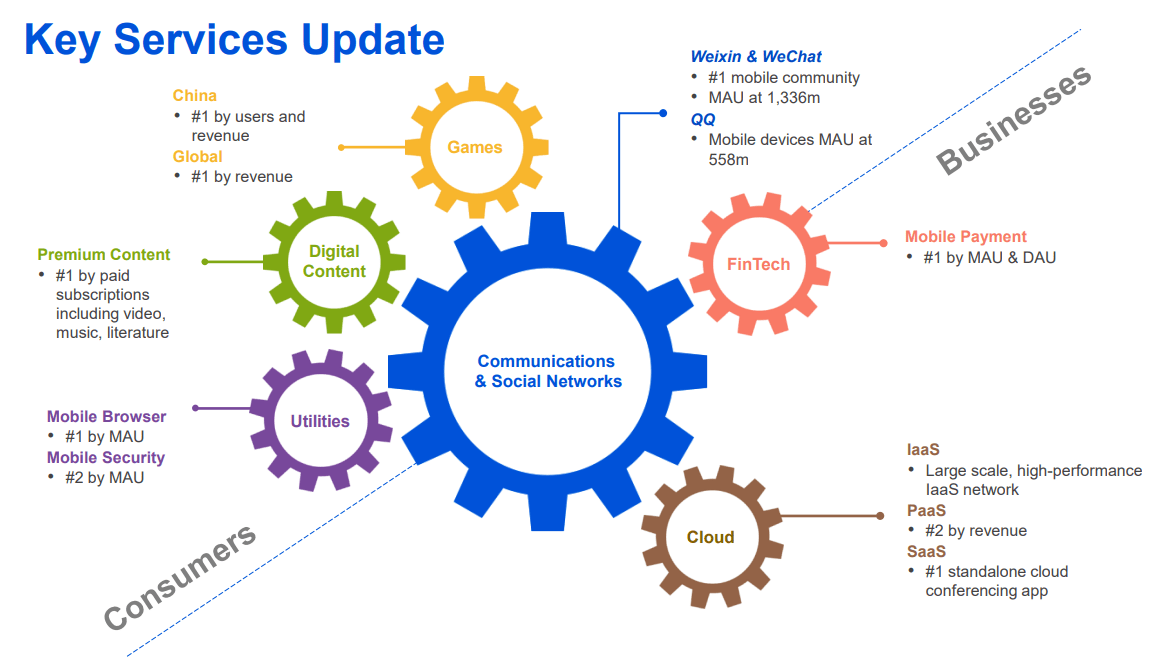

Tencent has its hands everywhere

{kind=link}

Tencent Q3 2023

Explaining Tencent's business model in detail is really challenging given that it is present in many different markets. Suffice it to say that the average Chinese person cannot not use Tencent during the day: doing so would mean not using social media, not buying anything, not listening to music, not playing video games. Certainly, there are other apps that allow them to perform these actions, but Tencent's are the most popular. But there is more.

As we will see later, Tencent has not only put down deep roots in China but also in the West: many people use its products/services on a daily basis without even knowing it.

In this section I will explain in detail the main segments of its operating business and you may be surprised how powerful this company is.

Gaming leader

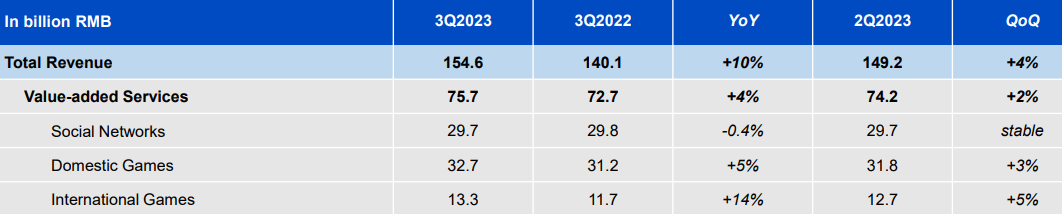

Gaming revenues from China and international ones account for 21.15% and 8.60% of total revenues, respectively. In total, the gaming segment accounts for 29.75% of total revenues, or RMB 46 billion in Q3 2023 .

{kind=link}

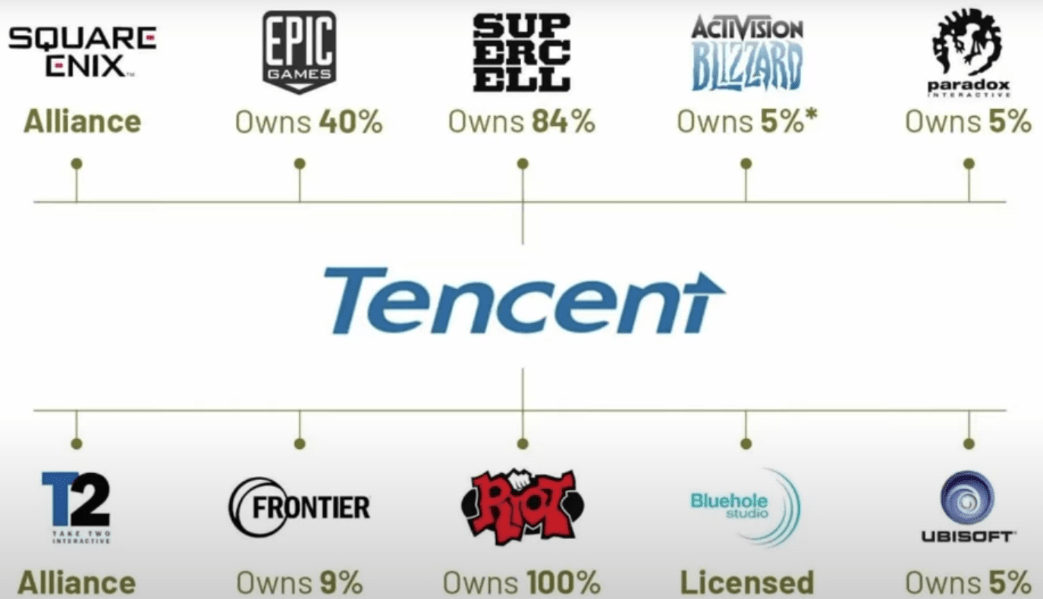

Tencent's acquisitions

In terms of revenue, Tencent is the largest game company in the world and features multiple internationally renowned titles. The secret of its success lies in having made a series of brilliant acquisitions and struck favorable deals with major game providers in the West.

In October 2009, Riot Games released League of Legends as a free-to-play game. Players were growing and Tencent immediately saw potential, in fact in February 2011 it bought 93% of Riot Games for $400 million; in 2015 it will buy the remaining 7%.

To date League of Legends is one of the most popular games in the world (2nd most viewed on Twitch) with 143 million active users in the last 30 days.

mobilemarketingreads.com

In 2022 alone , League of Legends generated revenues of $1.80 billion , 4.5 times the amount to get 93% of Riot Games. Moreover, League of Legends is not the only successful game from this company. Popular names include Valorant ( 25 million active users in the past 30 days), Teamfight Tactics , and Legends of Runeterra . Riot Games was valued at $2.26 billion in November 2023, well above what Tencent paid. All in all it was a bargain.

In 2012 Epic Games realized that the game industry was heading toward a games-as-a-service model (GaaS) and needed to follow this trend to grow its revenue. For the purpose of gaining more experience GaaS, Epic Games entered into a deal with Tencent, already dominant in the industry due to the success of League of Legends . In this deal, Tencent bought 40% of Epic Games for $330 million in June 2012, had the right to appoint directors to the Epic Games board but with limited control over the creative production of the games. In 2018 the free-to-play version of Fortnite was released and the numbers to date are impressive:

- More than 500 million registered players, including 236 million monthly players.

- Revenues are estimated at $26 billion between 2017 and 2022, of which $6 billion was generated in 2022 alone. There is still room for growth; Fortnite is still in vogue among young people.

Epic Games was last valued in April 2022 at $32 billion . When Tencent bought Epic Games the company was worth only $825 million; therefore, the Chinese giant was forward-looking since its 40% is now worth $12.80 billion.

Finally, the last gem concerns the acquisition of 81.40% of Supercell for $8.60 billion through Halti S.A., a Luxembourg-based consortium where Tencent is 51.20% owner. Supercell features some of the world's best-known titles in online gaming, including Hay Day, Clash of Clans, Boom Beach, Clash Royale, and Brawl Stars . These games feature a fast-paced freemium structure: it's free to play them but if you spend something you can upgrade faster. This structure has been highly successful and has allowed Tencent to quickly increase its international and domestic revenues.

In addition to acquisitions, there are also several commercial deals, the most important being those with Activision ( ATVI ) and Ubisoft ( UBSFY ), for Call of Duty and Assassin's Creed , respectively.

At this point you might think that Tencent has created its monopoly simply by acquiring companies that were already in the industry, but this is actually not the case. Tencent has proven repeatedly that it is capable of creating its own games as well.

Its most successful title is Honor of Kings , and it has had peaks of 100 million daily active users . Since its release in 2018, it has generated more than $10 billion, and last year it was the highest-grossing mobile game globally.

Overall, since 2011, under the leadership of co-founder and CEO Ma Huateng, Tencent has become a giant in the gaming world. In addition to the creation of games that have become worldwide successes, management's foresight in making targeted acquisitions at appropriate prices has made the difference. Virtually every successful game (especially mobile) has Tencent's hand in it.

The limitations and prospects of this market

A large portion of gaming revenues (71%) come from China, which exposes Tencent's gaming business to the risk that it may deteriorate after the umpteenth restriction imposed by the government a few weeks ago. Apparently, the fact that teenagers spend hours and hours in front of a screen does not particularly please the government, so I would not be surprised if there are new restrictions in the future. Since Tencent's goal is to keep gamers glued to the screen, it is obvious that this goes against its interests.

Personally, I don't doubt that the situation is getting difficult in China, but at the same time I don't think this is the moment to panic. First of all, people in China will continue to play Tencent's games albeit less than before; secondly, the international segment is the one that is growing the most (+14% over Q3 2022).

{kind=link}

Tencent Q3 2023

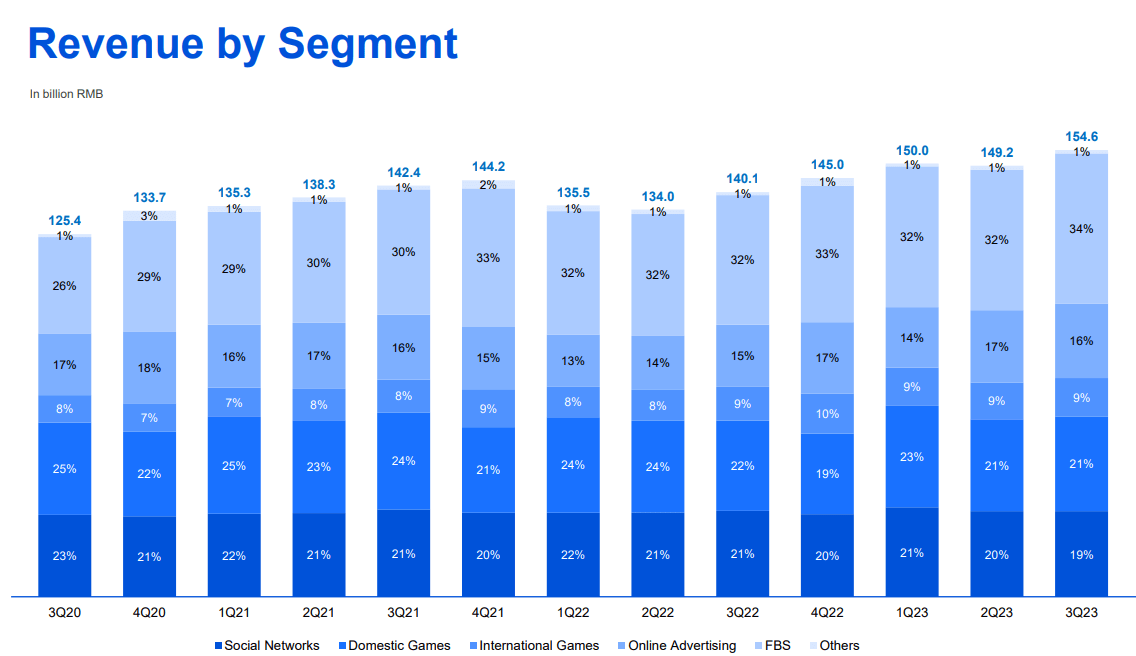

By the way, domestic games revenues have seen a +5% increase despite the fact that a series of regulations against the use of video games were already passed years ago. I don't expect them to grow in double digits, but I also don't expect them to become irrelevant after the latest restrictions. Looking ahead, the international games segment could overtake the domestic segment and this trend is already happening.

{kind=link}

Tencent Q3 2023

Today domestic games has a weight of 21% of total revenues compared to 25% in Q3 2020; in the same period the weight of international games has increased by 1% and reached 9%. Since there is no limitation in the West, I expect that the company will focus a lot on the international segment: the growth potential is still high.

{kind=link}

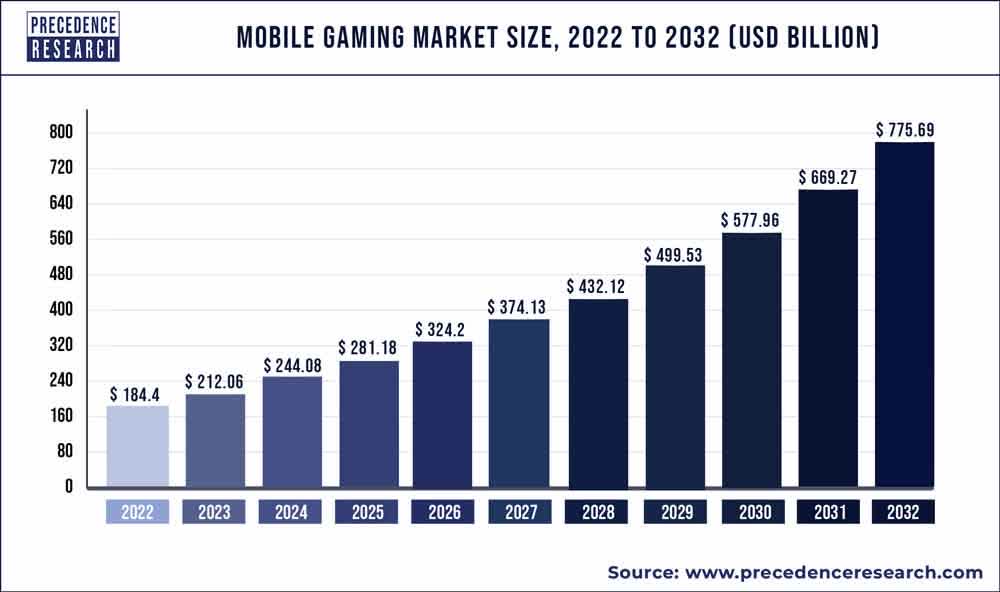

Precedence Research

Overall, the global mobile game market where Tencent has leadership was valued at $184.40 billion in 2022 by Precedence Research . In 2032 it could reach $775.69 billion, experiencing a CAGR of 15.50%. In short, even if the domestic games segment slows down it could be offset by the excellent opportunities internationally.

{kind=link}

Tencent Q3 2023

Finally, the company is working on some games that could attract the attention of many fans, as in the case of One Piece, Assassin's Creed , and Monster Hunter. We will learn more about these in the coming months.

Social Networks and Advertising

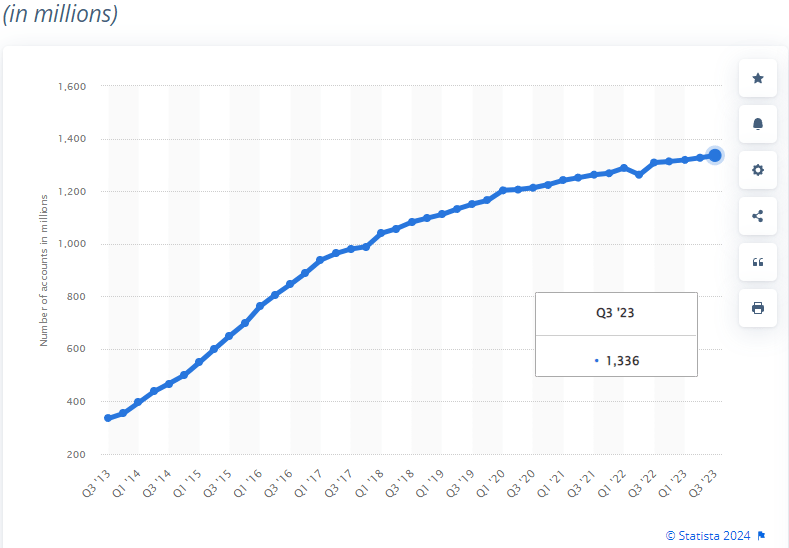

Social Network and Advertising If you are surprised at how dominant Tencent is in the game industry, then it is because you do not know how dominant it is in the world of advertising and social networks in China. WeChat (known as Weixin in China) has 1.33 billion monthly active users, of which 827 million are Chinese. This means that 59% of the population uses it, which is an impressive figure.

{kind=link}

Statista

Having to compare WeChat to a well-known app in the West, I would say it is a mix between Facebook and WhatsApp but with its own payment system. Besides being used by millions of people, WeChat is also dominant because of its wide use from a business perspective:

- 90% of companies use WeChat to communicate in the workplace in China.

- 70% of Chinese companies use WeChat for workplace communications instead of e-mail.

Companies cannot do without it to connect with potential new customers, and advertising on the app is a common way to succeed in increasing revenue. The entire process takes place within the app, even payments with customers. In fact, WeChat Pay is the second most popular digital payment method in the country and is used for virtually anything: grocery shopping, paying bills, online shopping, paying for movies, exchanging money with friends, and to other endless daily uses. In a way, for the Chinese it is as if WeChat is an ‘everything app’ much more so than Facebook and WhatsApp are for us.

The business model designated by Tencent works excellently, and that is why Meta is trying to make WhatsApp very similar to WeChat, especially on the payment aspect. The moment a user connects to WeChat he or she can do virtually anything, so it makes him or her totally dependent.

Tencent has a monopoly in this field and no other app can replace WeChat. Typically, a company with a monopoly does not please the Chinese government as it might accumulate too much influence and abuse its power over competitors, but I doubt that Tencent can be targeted about this. The main reason lies in the fact that WeChat does not use end-to-end encryption, so this ‘everything app’ is a key part of the Chinese Communist Party's ((CCP)) surveillance and censorship apparatus. As absurd as it is, chats and posts on the app are constantly under scrutiny and in case of inappropriate content it is very common to be banned.

So, WeChat is of great help to the Chinese Communist Party, but at the same time it represents a money-making machine for Tencent. Given the situation, I doubt it has growth potential outside of China as in the case of the gaming segment. However, the potential of China alone is huge: we are talking about a country with 1.42 billion people and a booming middle class.

{kind=link}

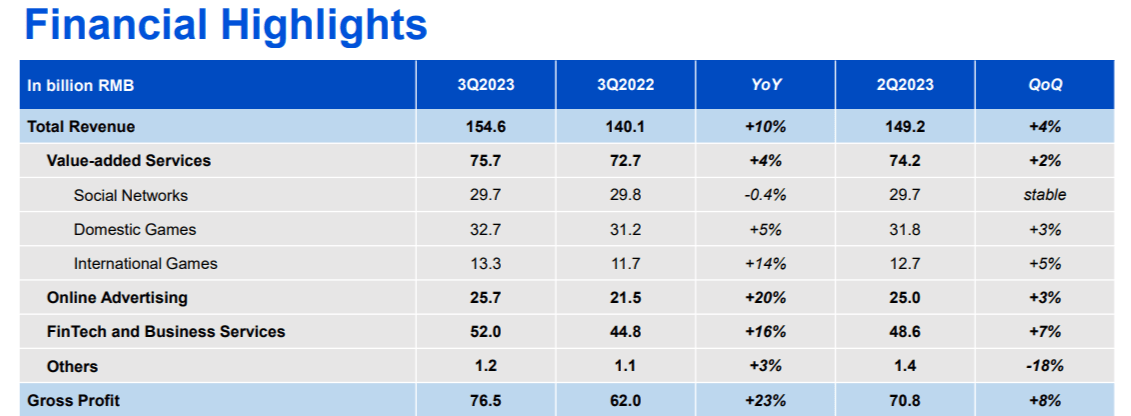

Tencent Q3 2023

Compared to Q3 2022, gross profit increased by 23% and reached RMB 76.50 billion. This growth was mainly supported by revenue growth from online advertising and fintech solutions, both of which are widely used within WeChat.

{kind=link}

Tencent Q3 2023

Since COGS has remained unchanged from last year, gross profit has experienced an increase in all business segments. In particular, FinTech is rapidly exploiting new economies of scale.

Overall, WeChat is more profitable and there are no viable competitors to challenge Tencent. While the government's use of WeChat has oppressive and inappropriate overtones by our standards, I believe it is widening Tencent's moat. Even if there were a company willing to offer a better app than WeChat, it would still be very difficult to implement it in today's Chinese society. First of all, it would need countless government approvals and secondly, the Chinese themselves are now used to using WeChat. Their whole lives are on Tencent's app and probably no incentive will be so great that hundreds of millions of people will migrate to another app with similar functions.

In short, investing in Tencent is in my opinion equivalent to investing in China's economic growth since WeChat Pay is used for any ordinary transaction. Moreover, WeChat is the best way for Chinese companies to sponsor their products and connect with new customers. Probably, only when Meta ( META ) implements these functions on WhatsApp will we really understand how important WeChat is to the Chinese.

Other operating segments

Although it may already seem enough, Tencent is not only the market leader in gaming and social networks, but has many other business segments. There are too many and I will highlight the most well-known ones:

- Tencent Video is a platform very similar to Netflix ( NFLX ) used by as many as 443 million Chinese people each month. It is the most popular in the country; in second and third place are Youku with 421 million users and iQIYI with 413 million users. Statista estimates that the video streaming market in China will be worth $28.49 billion by 2027 and will register a 2024-2027 CAGR of 8.97%.

- Tencent owns the country's largest music company, Tencent Music Entertainment ( TME ). It's almost a monopoly since it has a market share in China's music market of 60%: 660 million people use it every month. The music streaming market in China is expected to generate $3.99 billion in revenue by 2027, registering a 2024-2027 CAGR of 4.87% . This is not a high growth but the market share is remarkable. We can compare Tencent Music to our Spotify ( SPOT ), but bigger.

- Tencent is also the 3rd cloud service provider in China with a market share of 16% . In this respect it is rather behind Alibaba, 1st with a 36% market share. The public cloud market in China is estimated to be worth $137.10 billion in 2027, a CAGR of as much as 18.72% from this year.

- Finally, Tencent often buys significant shares in growing companies, as in the case of Spotify. Sometimes, it makes major business deals to foster the development in China of products that have already been successful in the West: this is the case with Roblox ( RBLX ). In the past Tencent also owned a major stake in Tesla ( TSLA ) and ByteDance (TikTok) but both have been sold.

There would also be dozens of other segments to discuss, but they are of less importance than those mentioned. The point is that Tencent is probably one of the most dominant companies in the world right now, leading in many even different markets. No company has its influence in China, not even Alibaba, and it seems to be slowly expanding to the West as well. Continuous acquisitions are branching out its business more and more, and it is already present in our lives more than we realize.

Valuation

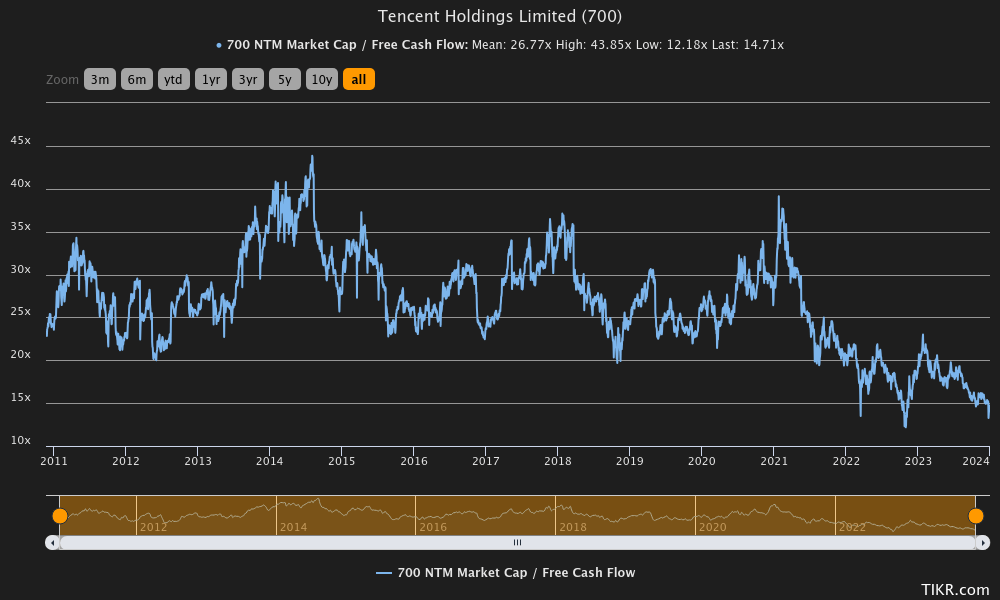

Unlike Alibaba, Tencent's price per share has rebounded quite a bit from the lows reached in late 2022, so it seems that the market is less pessimistic about this stock. Anyway, from the all-time high it has plummeted 63%.

{kind=link}

TIKR

According to the NTM Market cap/ Free cash flow ratio, Tencent has never been cheaper since 2011. Today we are on 14.71x while the historical average is 26.77x. Basically the market is discounting that Tencent's growth will suffer a major setback compared to the past. In my opinion this is too negative a scenario since Tencent remains a leader in multiple high-growth areas as we have seen above. Restrictions on the use of video games in China I do not believe will significantly impact cash flows over the next 10-20 years. Moreover, the growth of FinTech is more than offsetting this problem.

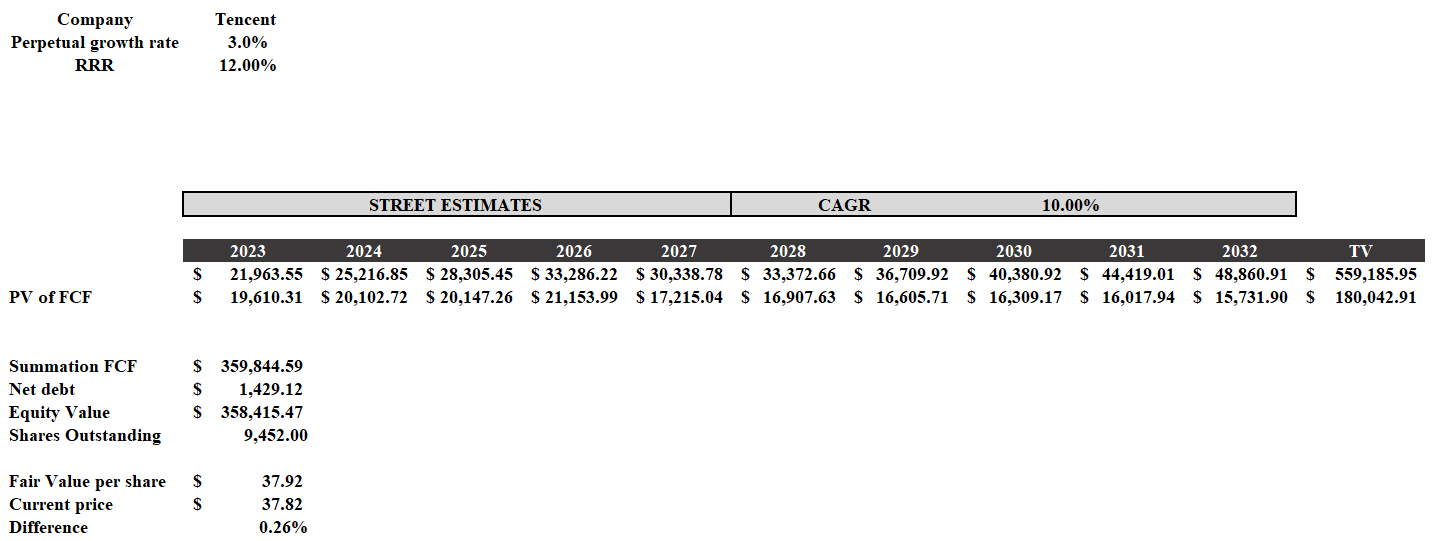

To understand Tencent's fair value, I used a discounted cash flow model by including the following parameters:

- Street Estimates of free cash flow until 2027; CAGR of 10% until 2032. Perpetual growth rate of 3%. This is a conservative estimate given that over the past 10 years the free cash flow CAGR has been 23.80%.

- Required rate of return of 12%. This is a rather high discount rate for a company like Tencent.

{kind=link}

DCF model

Based on these assumptions, Tencent is worth $37.92 per share, so it is fair valued. However, weighing on the valuation is the very conservative discount rate: using the CAPM formula it would be much lower. Entering an RRR of 10%, the fair value would be $50 per share and Tencent would be undervalued. Given the caliber of the company, extremely depressed multiples, and a good fair value with a 10% discount rate, I rate this company more as a buy rather than a hold. In addition, the dividend is low for now (0.80% yield) but the growth is interesting.

{kind=link}

Seeking Alpha

EPS is growing fast and with it also the dividend per share, which today is $0.29; a few years ago it was a few cents. By the way, the withholding tax in Hong Kong turns out to be quite low, only 15%. But there is more.

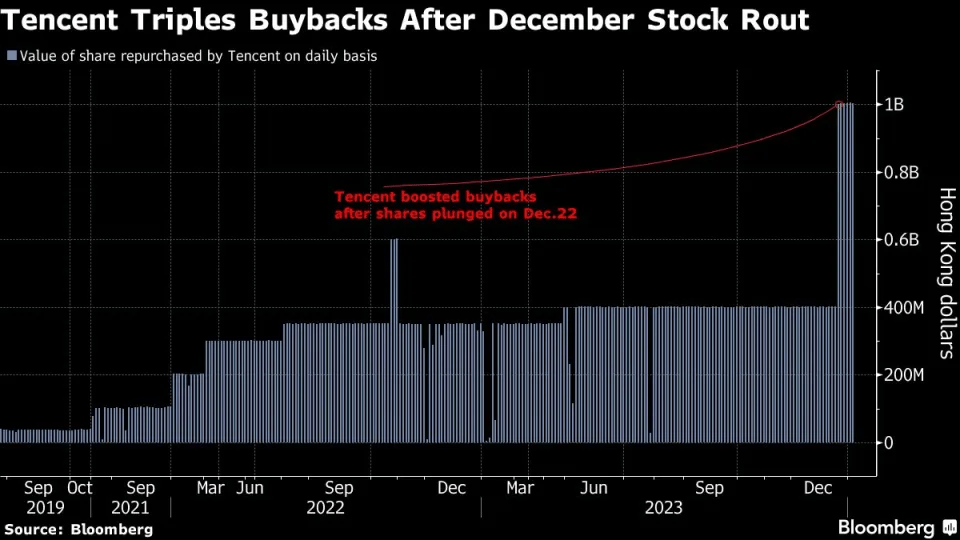

In addition to dividends, we can also expect buybacks. In the last quarter they bought back 48 million shares for RMB 14 billion and they will not stop.

{kind=link}

Bloomberg

Following the collapse a few weeks ago, the buybacks have tripled. Since this company is able to generate an annual free cash flow of $24 billion and has a net debt of only $1.42 billion, I believe it has the potential to aggressively continue its huge buyback plan. With fewer shares outstanding, this will be a major boost to both EPS and dividend per share.

Risks

Like any company, Tencent must also continuously innovate in order to succeed in beating the competition. In any case, as shown above, not only is Tencent the leader in many markets, but it is also the leader by a wide margin. In other words, the competitive advantage is very strong, and competition comes second in terms of the risks associated with investing in Tencent.

Clearly, the main risk concerns the uncertainty that Chinese companies face given the constant sanctions and restrictions imposed by the Chinese government: If Tencent were a Western company, it would never trade at such low multiples. In particular, Tencent is involved in activities that could easily be restricted:

- Social Networks via WeChat. It is well established that prolonged use can create dependency and is not beneficial to psychological health especially in adolescents. At the moment I do not see any restrictions in this area, but in the future there may be new regulations that can limit users' hours within the platform.

- The use of video games has already been restricted several times, and I would not be surprised if there are new regulations to comply with in the future. This is a problem for Tencent, which is why it needs to accelerate international gaming revenues.

In addition to these risks, there are others related to possible sanctions or obligations in investing in common prosperity, something that has already happened to Alibaba as well.

Conclusion

Tencent is a terrific company but political risk is scaring investors. Anyway, the valuation is quite depressed and may have discounted an overly negative scenario. After all, Tencent is one of the best companies in the world and is trading at an NTM Market Cap/Free cash flow of only 14.71x. We are not paying a premium for it. The growth drivers are there, especially in the FinTech, Online Advertising and International Gaming segments.

Finally, I would like to end this article with a personal reflection again on political risk since that is all we talk about when Chinese companies are involved. CCP is the reason why everyone avoids Alibaba and Tencent regardless, but my impression is that not everyone has understood that China risk does not only affect Chinese companies, but all those who are exposed to this country. Taking an example that we all know, Apple (AAPL) seems immune to China risk; yet, there are a number of data points to the contrary:

- Nearly 20% of sales come from China.

- Apple manufactures most of its products in China through partners such as Foxconn.

- It is heavily dependent on chips from TSMC (TSM) to produce its most cutting-edge devices.

If relations between China and the U.S. sour further, Apple could lose a lot. If there is a China-Taiwan war then we could say goodbye to our iPhones.

The point here is not to discourage those who have invested in Apple (this is just one of many examples I could have given), but to bring out an interesting food for thought about how the market is reacting hypocritically about China risk. To put it bluntly, either Chinese companies have been punished excessively or for Western companies this risk has been underestimated.

For further details see:

Tencent: More Powerful Than You Think