TCTZF - Tencent Music: Turnaround Interrupted

2023-10-26 17:59:39 ET

Summary

- Tencent Music’s live streaming business is under the regulatory spotlight this year.

- While online music subscriptions are outperforming, regulatory headwinds threaten to derail hopes of a turnaround.

- There’s still earnings growth potential here, but at current levels, the risk/reward isn’t great.

Tencent Music Entertainment Group ( TME ), the online music arm of Chinese tech/media conglomerate Tencent ( TCEHY ) (Tencent owns over 50% of TME stock and controls over 90% of the voting rights) and the largest online music entertainment platform in China, has navigated quite a bit of turbulence since its IPO in 2018. The last year has been particularly challenging for TME, but the group is turning the corner on its music subscription business this year, returning to positive growth in H1.

Yet, the social entertainment segment, which houses TME’s live streaming, is still taking hits, most recently disclosing a new round of ‘self-rectification’ efforts in Q2 - the result of a new round of regulatory crackdowns. With more tightening expected on its live streaming platform to meet increasingly stringent regulatory requirements, TME’s social entertainment business is likely headed for some steep P&L declines in H2 2023.

So while the online music outlook is as compelling as ever on the back of strong subscriber growth and per-user revenue upside, social entertainment downside, still a meaningful revenue and profit contributor, is posed to outweigh these positives. TME stock isn’t pricey at ~14x forward PE (vs. a low-teens rate for earnings growth outlook), but it isn’t cheap either when you factor in the regulatory overhang and its potential impact on the earnings base. On balance, I would remain neutral heading into Q3 earnings next month.

Regulatory Crackdowns Return; Livestreaming in the Line of Fire

TME and its parent company, Tencent, have undergone some major regulatory shake-ups through the years. So even with China’s seemingly ‘pro-business’ signaling earlier this year, it was perhaps not surprising that TME has found itself in regulators’ crosshairs, this time on the social entertainment side. Some of the impact was disclosed in Q2 2023 , when management disclosed that tighter ‘risk management’ of its live streaming platform had resulted in a ~25% YoY revenue decline. Since then, TME has broadened its ‘self-rectification’ efforts with WeSing, its social karaoke application, shutting down accounts, and limiting room functions (e.g., virtual lucky draws). This isn’t a one-time effort either – TME management is committed to cleaning up platform activity on an ongoing basis, particularly with regard to activities like fraud, gambling, and violent content, to ensure a 'healthier' environment.

{kind=link}

Tencent Music

The official draft guidelines released in August by the Cyberspace Administration of China (i.e., China’s internet regulator) shed light on TME’s ‘self-rectification’ efforts, emphasizing ‘minor protection’ online. There isn’t too much difference here relative to the many prior crackdowns related to the activity of minors in the past, though this move marks an extension into live streaming as well. Of note, measures include limits on daily time spent, content access, and functions for online live streaming, audio, and video, all of which will directly impact TME’s long-term earnings power.

Given the many issues currently plaguing the Chinese youth, many of whom spend an increasing amount of time on the internet, this may be the first of many new ‘guidelines’ to come as well. So while TME's compliance efforts should keep regulators away, the true impact on traffic and user engagement probably won’t be felt for some time yet - a key negative for the earnings outlook.

Guidance Bar Reset Lower but Don’t Rule Out More Downward Revisions

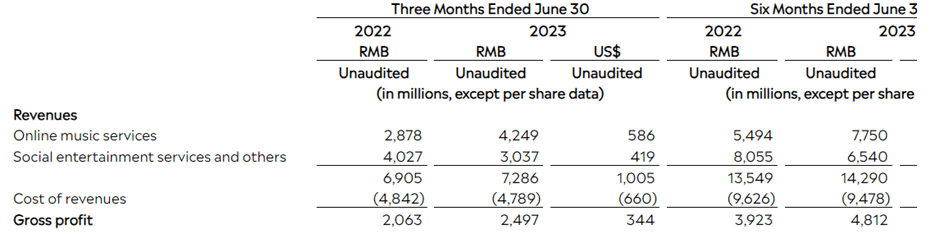

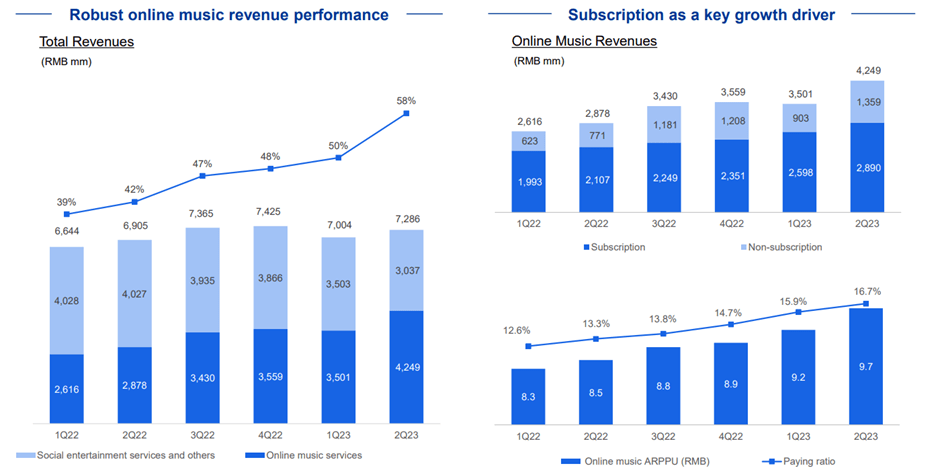

On the bright side, TME still has plenty of upside in its online music subscription business, which management is hoping will support YoY net profit growth for this fiscal year. Growth here is twofold - subscriptions are up to ~99mn in Q2 2023 and have since reached the 100m milestone, while average revenue per user (ARPU) is also up across the user base, helped by a pullback in discounting.

Continued top-line growth is key, given the leverage inherent in online music, allowing for fixed content costs (mainly the minimum guarantee paid in advance) to be spread over a larger revenue base. In tandem, management sees more upside to gross margins following an encouraging ~34% result in Q2. Given TME’s scale, I don’t think this target is out of reach, with plenty of untapped levers still available across content cost cuts (especially on the fixed minimum guarantee) and a mix shift toward higher-margin in-house content (vs pricier licensing deals).

{kind=link}

Tencent Music

Yet, it’s hard to look past the problems at TME’s live streaming business, a view the market seems to share given the vicious post-Q2 selloff. Recall that social entertainment revenue fell to RMB3bn in Q2, a ~25% YoY decline and, most importantly, well below consensus and where management previously guided. It isn’t clear how much more risk control/management and feature censorship will be required post-Q2 either, though the news flow (CAC ‘minor protection’ guidelines and WeSing ‘self-rectification’ efforts occurred in August/September) indicates we’ll see kitchen sinking in Q3/Q4 as well. Also unclear is how much the downgraded user experience will affect retention and engagement - key at a time when live streaming is facing severe competition from short video platforms.

Bulls might argue that management already reset the earnings base in Q2, guiding toward a low to mid-teens rate of YoY decline in total revenue in Q3 2023. For the full year, the revenue guide is down to a low to mid-single digit YoY revenue decline, as well, implying a massive pullback of over 50% YoY in social entertainment revenue. With the margin guidance still somewhat optimistic, on the other hand, at stable YoY adj net profits (higher adj net profit margin), there’s still a fair bit of downside risk to current guidance numbers, in my view.

Turnaround, Interrupted

There’s a lot going right for TME in its online music business, with subscription numbers and ad revenues on the rise in H1 2023. But any tailwinds in the online music segment likely won’t be enough to offset headwinds on the social entertainment side, where more regulatory crackdowns threaten to impair the segmental earnings base.

While management has already begun tightening the screws on live streaming in Q2, expect more risk control implementations through H2 in line with the latest CAC minor protection guidelines and to pre- empt more regulatory pressure going forward. Given TME’s social entertainment business still accounts for a large chunk of profits, this means meeting the current full-year guidance bar for stable net profit and higher net margins will be a tough task.

The current low to mid-teens fwd P/E pales in comparison to Western comparables like Spotify ( SPOT ), but given the regulatory overhang and macro weakness in China, the stock certainly isn’t cheap here.

For further details see:

Tencent Music: Turnaround, Interrupted