ENSG - Tenet Healthcare: A Compelling Opportunity Despite Lofty Debt

2023-10-13 11:49:45 ET

Summary

- Tenet Healthcare operates 61 hospitals and has a growing ambulatory care business, with revenue increasing by 7.7% in the past year.

- The company's net profits and operating cash flow have improved, although EBITDA has decreased.

- Management forecasts increased revenue and profits for this year, but a decrease in EBITDA. The company's debt is a concern, but it has no debt coming due in the near term.

- Shares are also cheap, which indicates some upside potential if nothing terrible arises.

I have always had an appreciation for the medical industry. Even though I have no education or training in that space, perhaps that is why I have found myself interested in companies that operate in this realm. One company that I have been bullish on in this space in the past is Tenet Healthcare ( THC ), an enterprise that operates no fewer than 61 hospitals, while having ownership in others using joint ventures. The company also has a sizable ambulatory care business that it owns and, though quite small, the company also has a small unit dedicated to providing business process services in the medical space.

Back in June of last year, I found myself taking a rather bullish stance on the company. While I do have a solid track record when it comes to the companies I rate a ‘buy’ or better, not every firm turns out to be a winner, especially in relatively short windows of time. This has been one of those firms that has fallen short so far, with shares dropping 13.6% while the S&P 500 has risen 5.9%. Even with this underperformance, the financial strength of the company seems to be improving and shares are cheap, both on an absolute basis and relative to similar firms. Given these circumstances, I've decided to keep the company rated a ‘buy’ for now.

Focus on the fundamentals

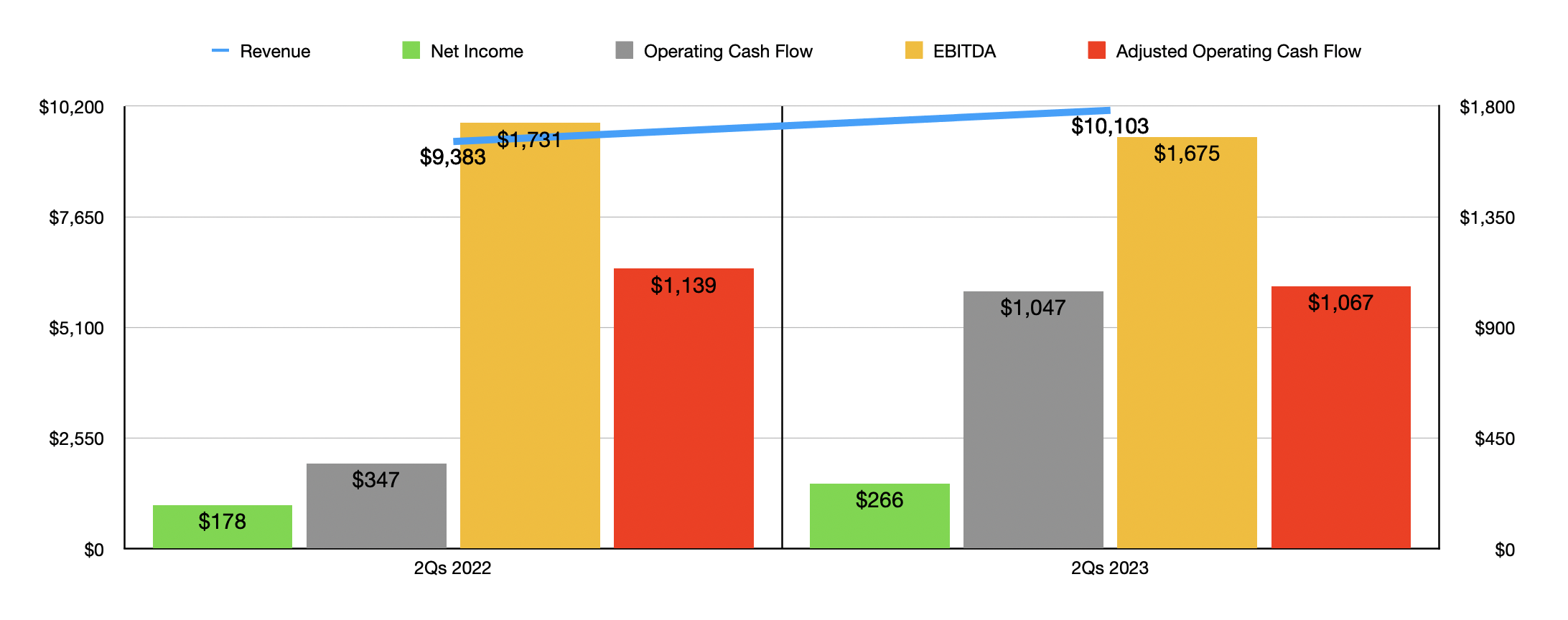

As I mentioned already, Tenet Healthcare has not exactly performed as well as I would have hoped since I last wrote about it in June of 2022. Given this underperformance, you would be forgiven for thinking that the fundamental performance of the company had faltered. In fact, the exact opposite has transpired. By most metrics, Tenet Healthcare continues to do quite well. Take revenue as an example. Sales in the first half of the 2023 fiscal year came in at $10.10 billion. That's 7.7% above the $9.38 billion reported one year earlier.

{kind=link}

There were multiple drivers behind this sales increase. For starters, the Ambulatory Care segment saw an increase in the number of facilities that the company owns from 269 to 320. And the number of hospitals grew from 60 to 61. The increase in the Ambulatory Care business caused revenue under that segment to jump from $1.51 billion to $1.85 billion as the growth in facility count helped to push up the number of cases that unit handled. In the second quarter alone, for instance, the number of cases totaled 346,402. That's 9.1% above what was seen one year earlier. Total admissions under the Hospital Operations segment, meanwhile, jumped 4% on an adjusted basis, climbing from 239,031 to 248,589. Total surgeries increased, as did total emergency department visits. The only weakness for the company from a sales perspective involved its Conifer unit, with sales dropping by about $10 million.

On the bottom line, the picture for the company was mixed but largely positive. Net profits, for instance, grew from $178 million in the first half of 2022 to $266 million the same time this year. Operating cash flow more than tripled from $347 million to $1.05 billion. However, if we adjust for changes in working capital, we would get a decrease from $1.14 billion to $1.07 billion. Meanwhile, EBITDA for the company shrank from $1.73 billion to $1.68 billion.

If everything goes according to plan, management expects revenue this year to come in at between $20.10 billion and $20.50 billion. This would represent a nice increase over the $19.17 billion generated in 2022. Net profits are forecasted to be between $447 million and $582 million, with a midpoint of $515 million. By comparison, in 2022, profits came in at only $411 million. This is not to say that management is forecasting improved results across the board. Because that's not the case. Last year, EBITDA for the enterprise totaled $3.47 billion. This year, it's expected to drop to between $3.31 billion and $3.46 billion. Though this is disappointing, management did say that normalized EBITDA last year was a more modest $3.02 billion. So this would represent an 11% growth, at the midpoint, compared to that adjusted figure for last year. No guidance was given when it came to adjusted operating cash flow. But based on my estimates, it should come in at around $2.17 billion.

{kind=link}

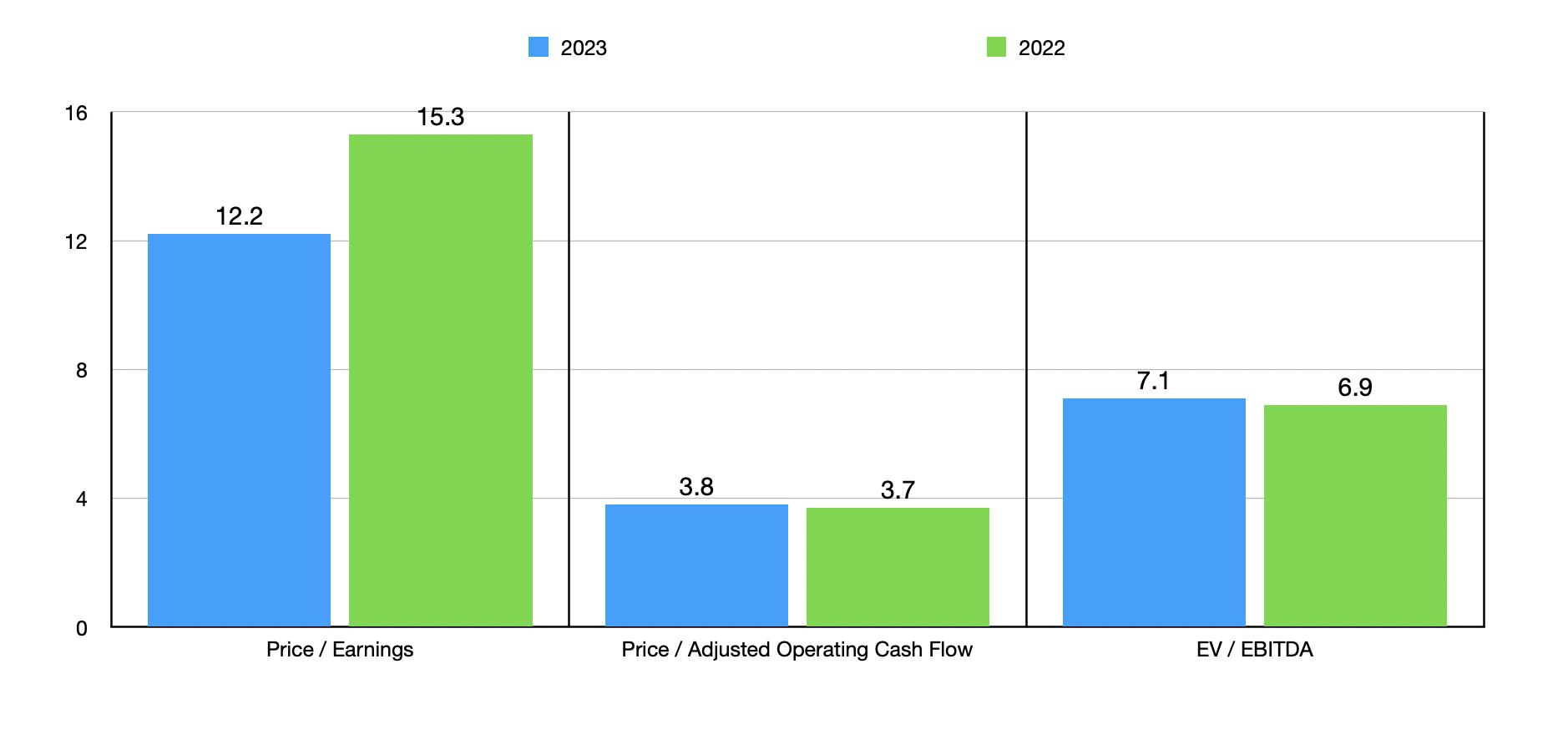

Using these figures, I was able to value the company as shown in the chart above. As you can see, the stock is a bit more expensive on a forward basis when it comes to both the price to operating cash flow multiple and the EV to EBITDA multiple. But when it comes to the price to earnings multiple, it is cheaper. In the table below, I then compared the company to five similar firms. On a price to earnings approach, only one of the five companies was cheaper than our prospect. Meanwhile, using the other two profitability metrics, Tenet Healthcare ended up being the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Tenet Healthcare |

| 12.2 |

| 3.8 |

| 7.1 |

| HCA Healthcare ( HCA ) |

| 12.0 |

| 7.0 |

| 8.1 |

| Universal Health Services ( UHS ) |

| 13.2 |

| 7.8 |

| 8.4 |

| The Ensign Group ( ENSG ) |

| 23.0 |

| 17.8 |

| 13.4 |

| Encompass Health ( EHC ) |

| 20.7 |

| 9.6 |

| 10.1 |

| Acadia Healthcare Company ( ACHC ) |

| 24.4 |

| 18.2 |

| 14.1 |

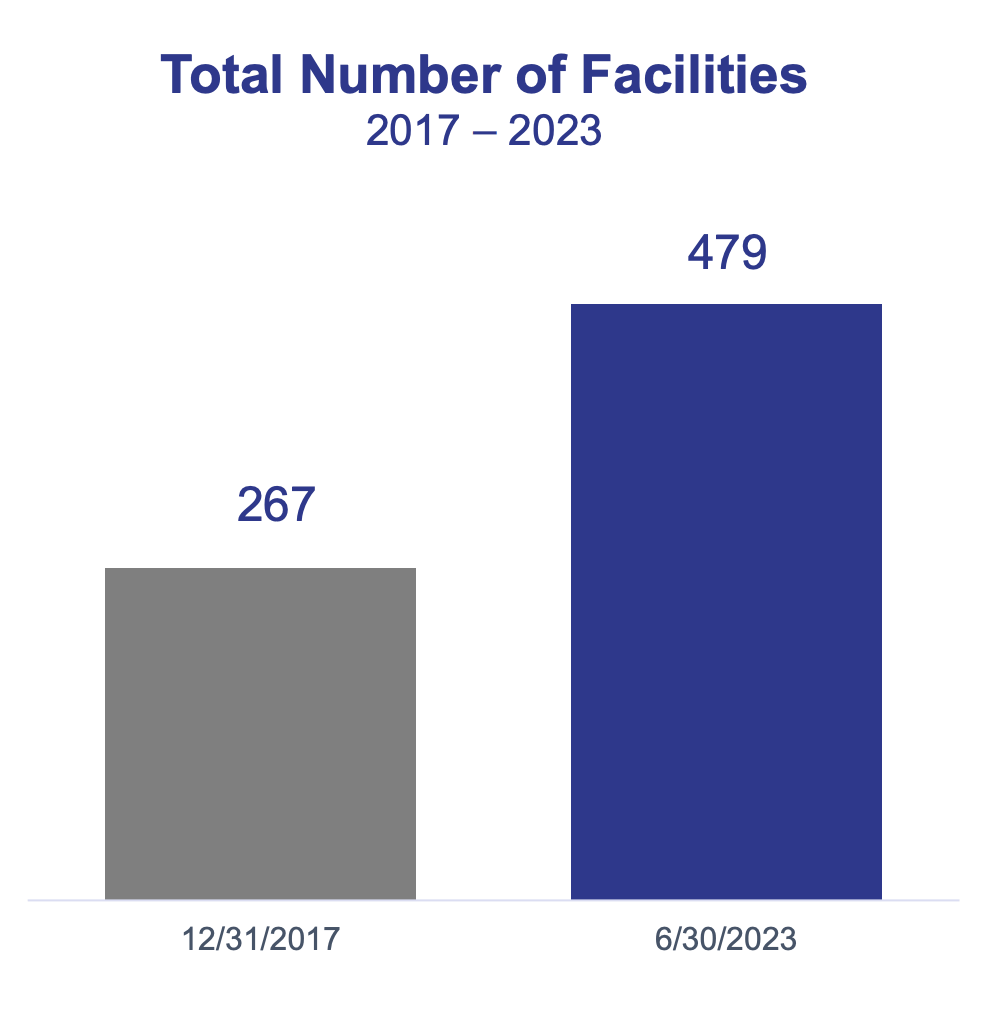

This year is looking good and shares are cheap. But one thing that investors would likely ask is whether or not this trend can continue. In recent years, management has been investing in the growth of a subsidiary known as USPI. This is the unit that the Ambulatory Care segment of the company is comprised of. And while I previously stated in this article that the number of facilities this segment owns is 320, this is the consolidated number.

{kind=link}

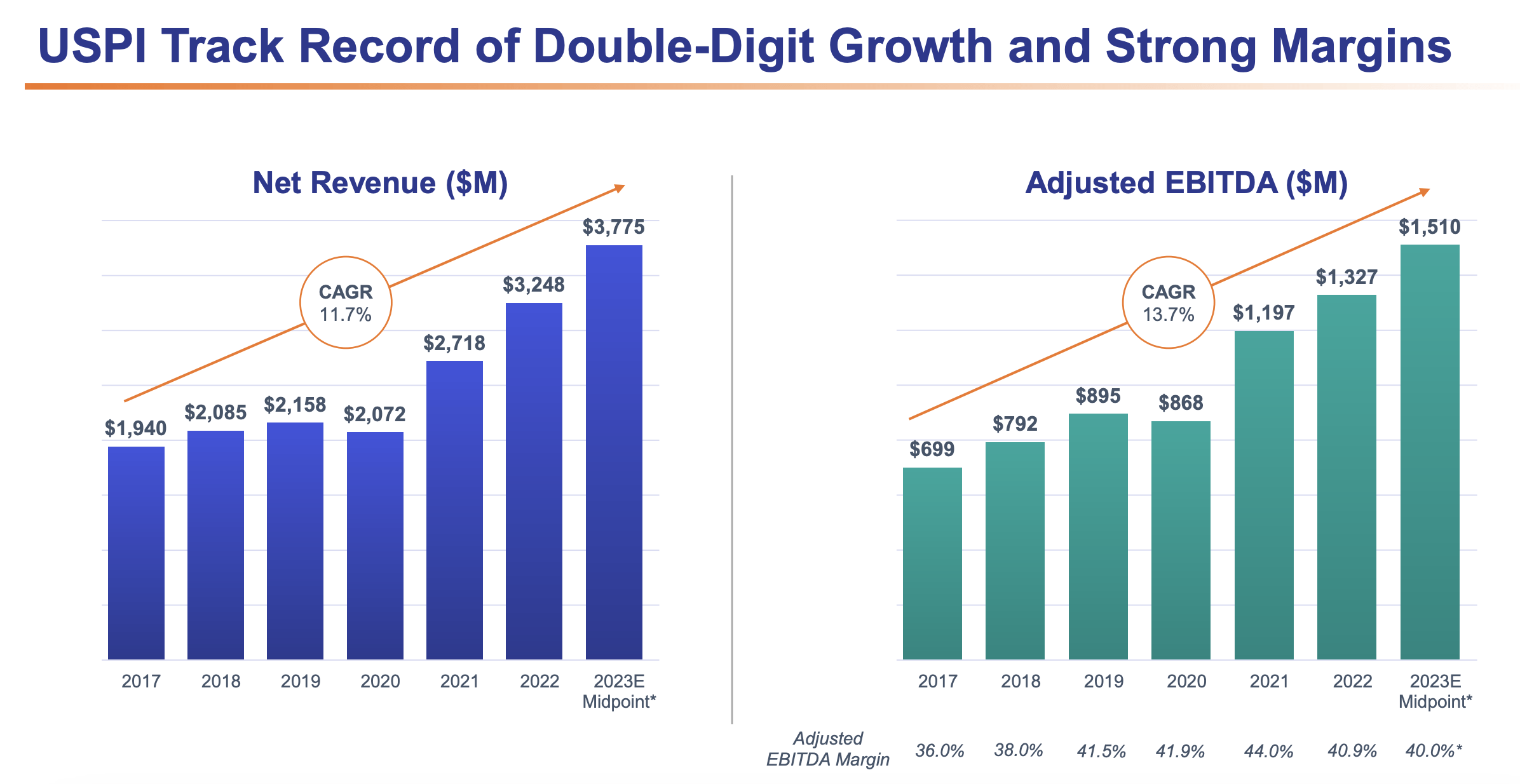

The actual interest that it has in these types of properties reached 479 as of the end of the most recent quarter. This is up from the 267 facilities that the entity had as of the end of 2017. The acquisitions the company has made were instrumental in pushing up revenue associated with this business in recent years. From 2017 through 2023, assuming midpoint guidance is hit this year, that unit will have seen an annualized growth rate of 11.7%. But almost all of that growth has come from 2020 through 2023.

{kind=link}

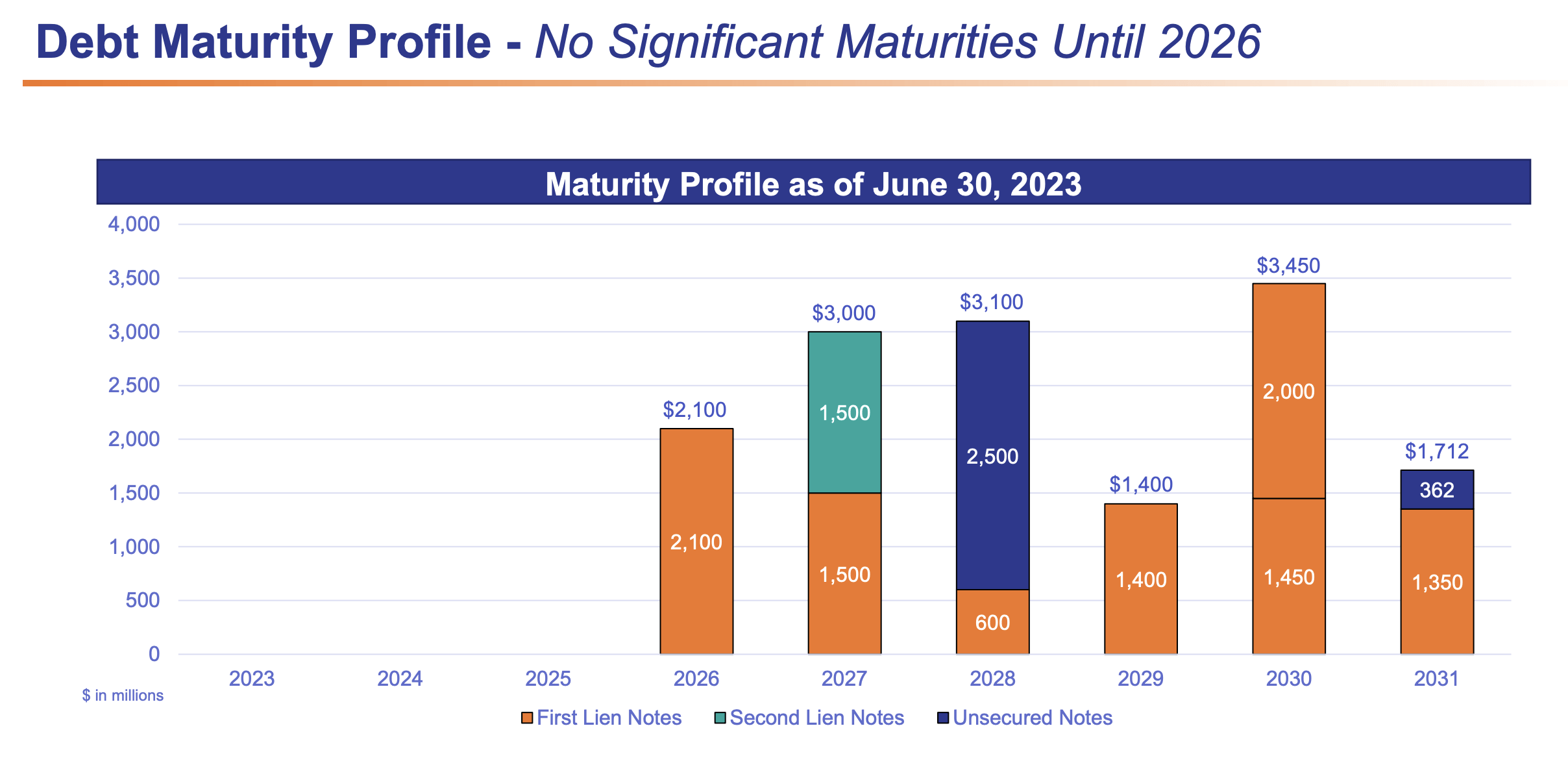

As the company's footprint here has grown, so too has its profit margins. The EBITDA margin of USPI has inched up from 36% in 2017 to 40% this year so far. Though it is worth noting that it did hit as high as 44% in 2021. Of course, growth does not come easy. It can often be expensive. The fact of the matter is that net debt at the company totals $14.11 billion as of this writing. This translates to a net leverage ratio of about 4.14. But there is some good news on this front as well. You see, according to management, none of the company’s debts come due until 2026. And the amount due at that time is $2.10 billion. And since all of the company's long term debt, except periodic amounts it has under its credit agreement, are fixed rate in nature, there is not too much concern about having to refinance in a high interest rate environment. This is a positive thing because even a 1% increase in interest rates applied to the gross debt that the company has outstanding would work out to over $150 million of additional annual cost for the enterprise.

{kind=link}

Takeaway

From all that I can see, Tenet Healthcare seems to be doing fairly well for itself. The company continues to expand and shares look cheap on both an absolute basis and relative to similar firms. We are seeing some mixed bottom line results this year, but nothing terribly concerning. The biggest issue might be the amount of debt that the company has achieved in order to grow like it has. But when you consider how much cash this company generates and the fact that it has no debt coming due in the near term, should be considered a net positive. When you combine all of these factors together, I cannot help but to keep it rated a ‘buy’ for now.

For further details see:

Tenet Healthcare: A Compelling Opportunity Despite Lofty Debt