THC - Tenet Healthcare: More M&A And Recruitment Efforts Could Imply Undervaluation

2023-05-19 14:40:15 ET

Summary

- Tenet Healthcare is a diversified healthcare provider.

- In the last quarter, the company reported one more hospital as compared to that in 2022. As a result, the KPIs improved.

- Further expansion of the Ambulatory Care segment through acquisitions, organic growth, and construction of new centers and strategic partnerships will likely bring FCF growth.

- Successful growth of the Conifer business segment by providing revenue cycle management services and expanding value-based offerings as well as enhancing customer experience will likely enhance net sales growth.

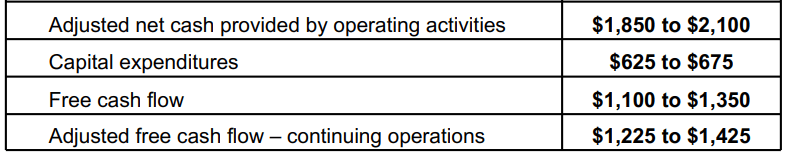

- I believe that the growing aging population could bring significantly more clients. Management expects 2023 FCF of close to $1.1-$1.3 billion.

Tenet Healthcare Corporation ( THC ) owns a diversified portfolio with an extensive network of facilities in the healthcare industry. I also believe that the recent guidance and the free cash flow expectations for the year 2023 will most likely bring the attention of new investors. Besides, further recruitment and retention efforts to make lower labor costs and new acquisitions will most likely bring both revenue growth and free cash flow margin enhancement. Even considering changes in healthcare regulations, new regulatory standards, or debt covenants, in my opinion, the stock stays at an undervalued price mark.

Tenet Healthcare Continues To Acquire Hospitals, Which Increases The KPIs

Tenet Healthcare is a diversified healthcare provider with headquarters in Dallas, Texas, and a global business center in Manila, Philippines.

It operates through direct and indirect subsidiaries, including USPI Holding Company as well as partnerships and joint ventures. It currently has 61 acute care and specialty hospitals with more than 575 healthcare facilities, including hospitals, doctors' offices, employers, and clients.

{kind=link}

Tenet's business model consists of 3 separate operating segments: Hospital Operations, Ambulatory Care, and Conifer. On the part of the hospital operation, it offers general services such as acute services, operating rooms, and recovery rooms. For the Outpatient section, it offers a variety of procedures and lines of services, such as orthopedics, otorhinolaryngology, and gastroenterology. In the Conifer segment, operations are provided by its joint venture Conifer offering value-based solutions, including clinical integration, financial risk management, and population health management.

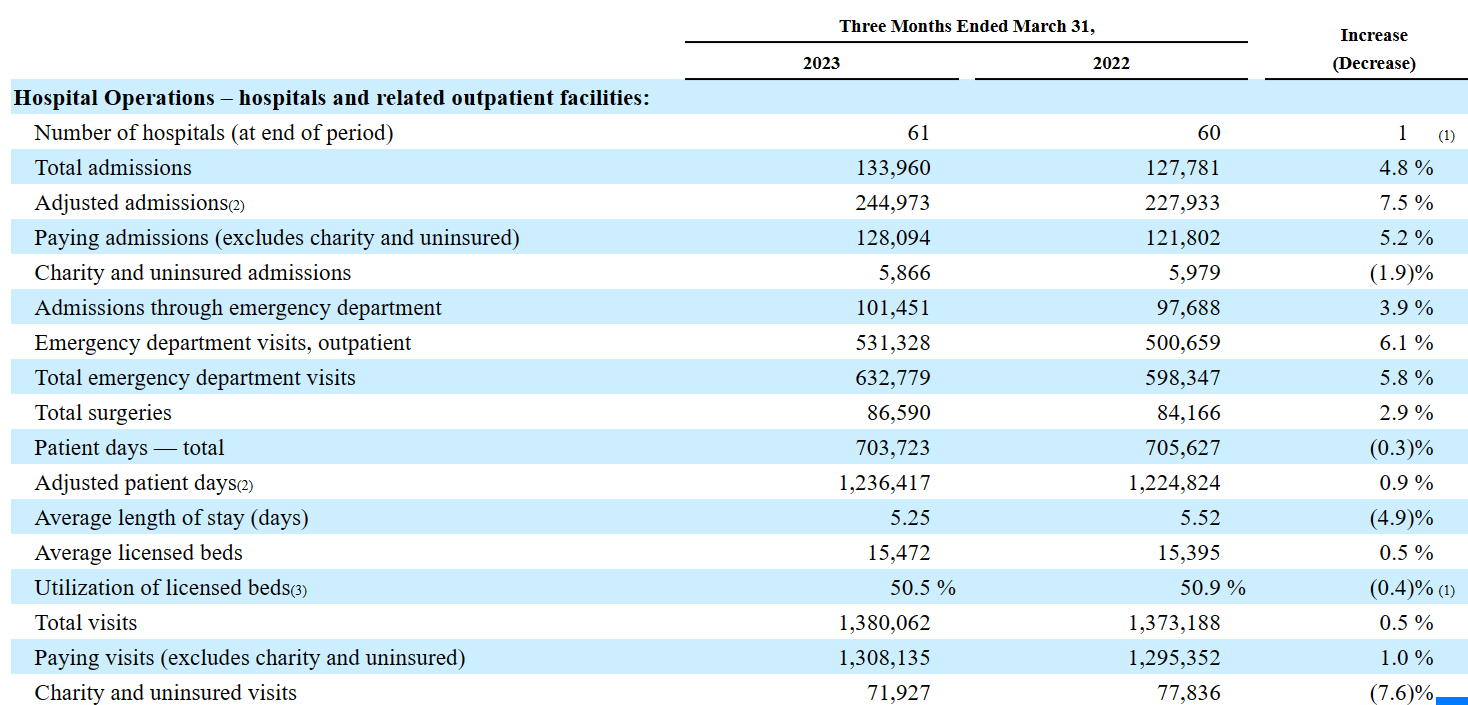

In the last quarter, the company reported one more hospital as compared to that in 2022. As a result, the KPIs improved. I believe that some of the figures reported by management right after the new acquisition are worth noting. Total admissions in the first quarter stood at 133960 with paying admissions of 128094. The company also reported 101451 emergency department visits, with 632779 total surgeries and utilization of licensed beds of close to 50.5%.

{kind=link}

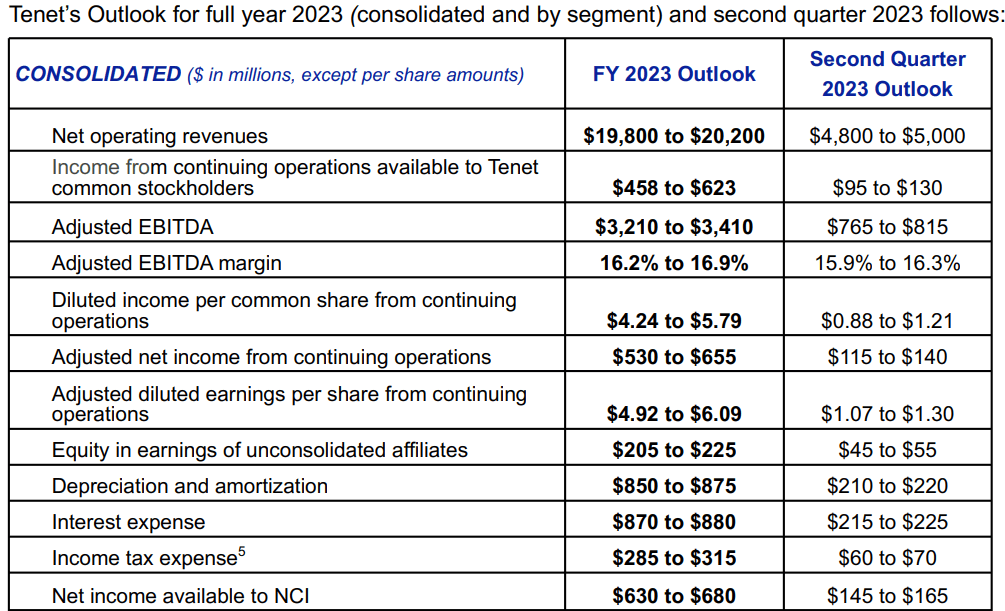

I believe that having a look at Tenet today is a pretty good idea considering the outlook given for the year 2023. It includes 2023 net operating revenue of $19.8-$20 billion, adjusted EBITDA of $3.2-$3.4 billion, and net income close to $630-$680 million .

{kind=link}

It is also worth noting that management expected FCF of close to $1.1-$1.3 billion with capex close to $625-$675 million. Taking into account these figures, I believe that designing a discounted cash flow model is interesting.

{kind=link}

Balance Sheet

Tenet reports a balance sheet with a substantial amount of property and equipment as well as an outstanding goodwill obtained from the acquisitions of hospitals. More than one-third of the total amount of assets is represented by goodwill, so I believe that goodwill impairments are likely. The acquisitions were financed by long-term debt, which does not seem small, but appears to be under control.

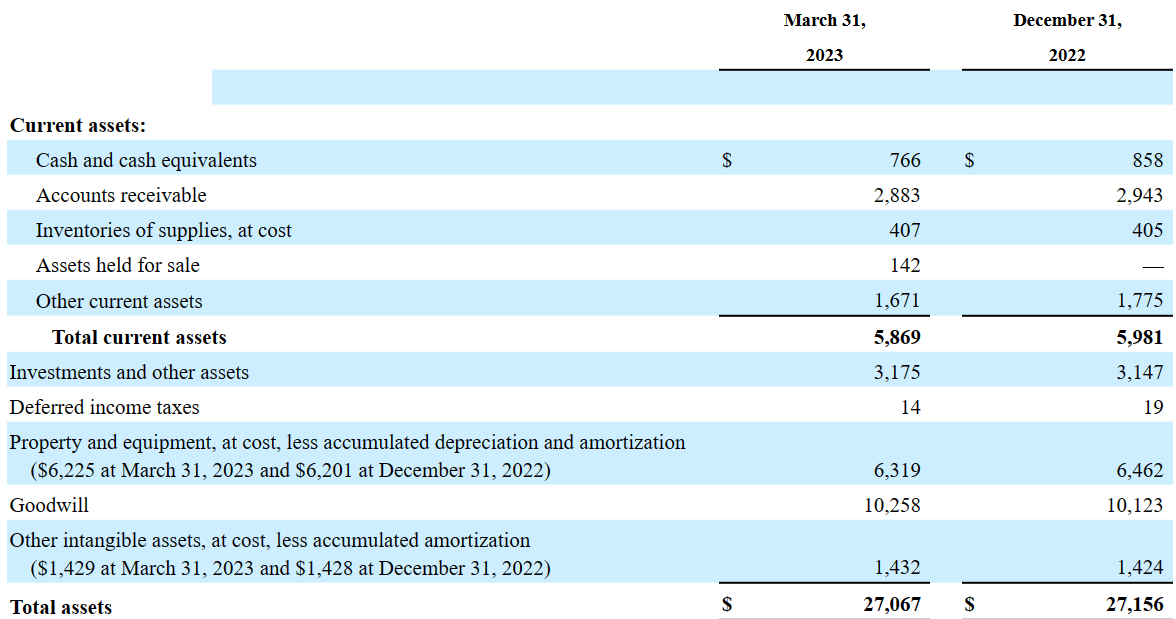

As of March 31, 2023, Tenet reported cash and cash equivalents close to $766 million, accounts receivable of $2.883 billion, inventories of supplies worth $407 million, and total current assets of $5.869 billion.

Besides, investments and other assets stood at $3.175 billion, with deferred income taxes of $14 million and property and equipment, at cost, less accumulated depreciation and amortization of $6.319 billion. Finally, with goodwill worth $10.258 billion and other intangible assets of $1.432 billion, total assets were equal to $27.067 billion. The asset/liability ratio stands at more than 1x, however, I believe that investors need to pay attention to the total amount of debt outstanding.

{kind=link}

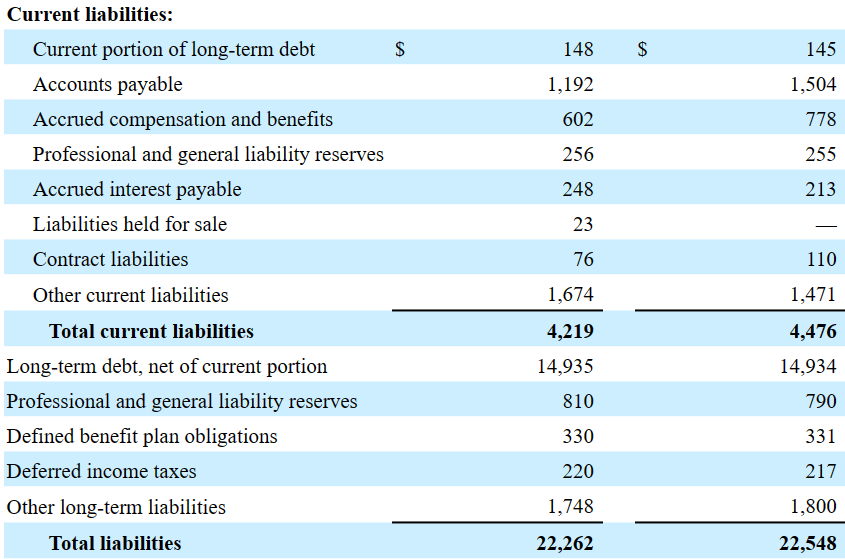

With the current portion of long-term debt close to $148 million and accounts payable worth $1.192 billion, accrued compensation and benefits are equal to $602 million. The company also reported accrued interest payable worth $248 million, with contract liabilities close to $76 million and other current liabilities worth $1.674 billion.

Also, with long-term debt of $14.935 billion and professional and general liability reserves close to $810 million, defined benefit plan obligations are equal to $330 million, and total liabilities were equal to $22.262 billion.

{kind=link}

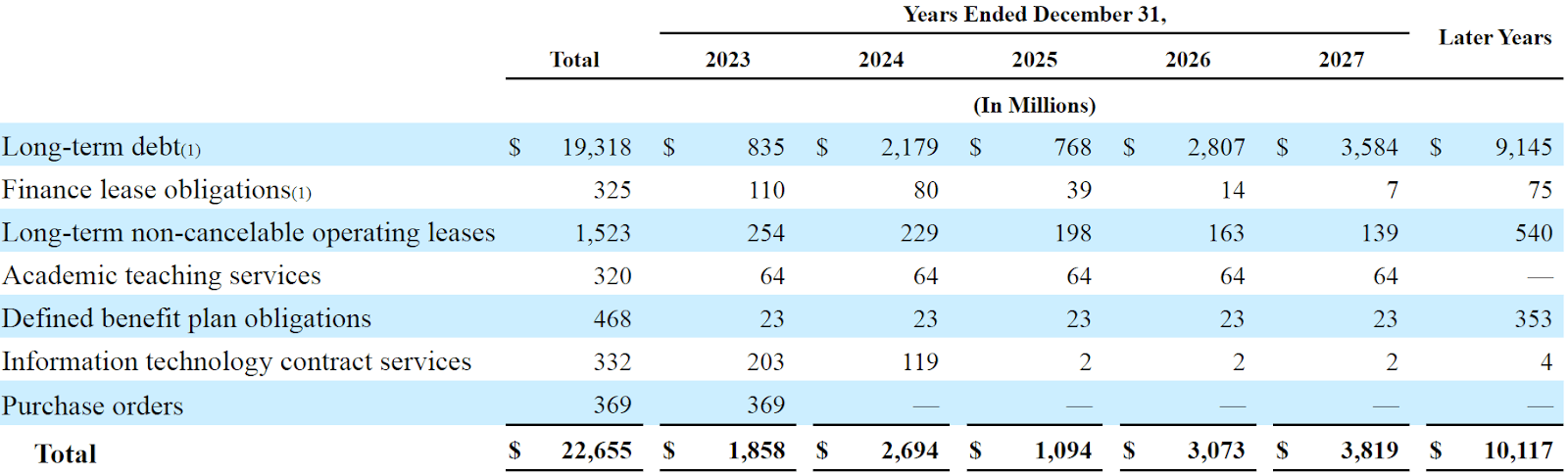

Considering the total amount of debt, I decided to include the table of contractual obligations. Long-term debt stands at $19.318 billion with finance lease obligations worth $325 million, long-term non-cancelable operating leases of $1.523 billion, academic teaching services worth $320 million, and defined benefit plan obligations of $468 million. In my view, the largest contractual obligations are around 2026, 2027, and thereafter. I believe that Tenet will be able to negotiate its obligations or find new financing.

{kind=link}

Competitors

Hospitals and health centers compete based on the quality of care, location, services offered, reputation, and facilities. Tenet competes with public hospitals, financially privileged nonprofit organizations, large university hospitals, and specialized centers. Competition is also influenced by national laws and the rise of independent institutions. Relationships with managed care plans are critical because contracts affect your income. They compete on price, reputation, location, quality of services, and medical personnel. Exclusivity and vertical integration of third-party payers and service providers also present competitive challenges.

My DCF Valuation

I believe that further expansion of the Ambulatory Care segment through acquisitions, organic growth, and the construction of new centers and strategic partnerships will likely bring FCF growth.

I also think that we may see growth of the hospital systems through operational efficiencies, investments in physicians, improvement in patient care and physician satisfaction, and asset optimization. Finally, successful growth of the Conifer business segment by providing revenue cycle management services and expanding value-based offerings as well as enhancing customer experience will likely enhance net sales growth.

I would also expect that management will successfully implement strategies to lower labor costs through recruitment and retention efforts. Fortunately, in the last quarterly report, management noted a reduction in the labor expenses during the three months ended March 31, 2023. I would expect a further reduction in labor expenses in the coming years.

In some of our communities, employers across various industries have increased their minimum wage, which has created more competition and, in some cases, higher labor costs for this sector of employees. Although we continue to incur a higher level of contract labor expense than we have historically, our recruitment and retention efforts drove a reduction in this expense during the three months ended March 31, 2023. Source: 10-Q

In the last quarterly report, the company noted significant price increases in medical supplies and some supply chain disruptions. I would expect this price increase to be too low over the coming years. I would also expect lower supply chain disruptions. As a result, I believe that costs would lower, which would have a positive impact on free cash flow growth.

We have also experienced significant price increases in medical supplies, and we have encountered supply-chain disruptions, including shortages and delays, caused by current economic conditions. In addition, our Ambulatory Care segment has been impacted by shipment delays in construction materials and capital equipment with respect to its de novo facility development efforts, which are a key part of our portfolio expansion strategy. Source: 10-Q

Finally, I expect patient volume from inpatient to outpatient settings which would most likely benefit the company. Besides, I believe that the growing aging population could also bring significantly more clients. In this regard, management offered certain commentary.

Patient volumes are shifting from inpatient to outpatient settings due to technological advancements and demand for care that is more convenient, affordable and accessible. The growing aging population requires greater chronic disease management and higher?acuity treatment. Source: 10-Q

In order to design my FCF model, I took a look at the expectations of other financial advisors , which include 2023 FCF close to $1.433 billion, 2024 FCF of $1.315 billion, and 2025 FCF of $1.127 billion. Market estimates also include EBITDA growth and EBIT growth.

S&P

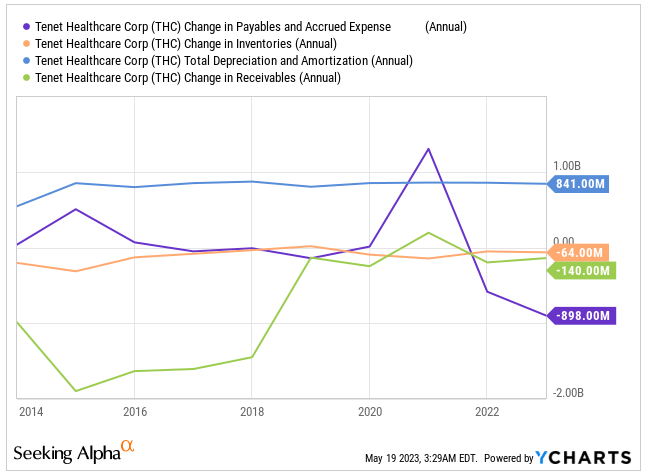

For the calculation of the changes in account payables, changes in inventories, D&A, and changes in receivables, I took a look at the figures reported in the past . In my view, my numbers are conservative.

{kind=link}

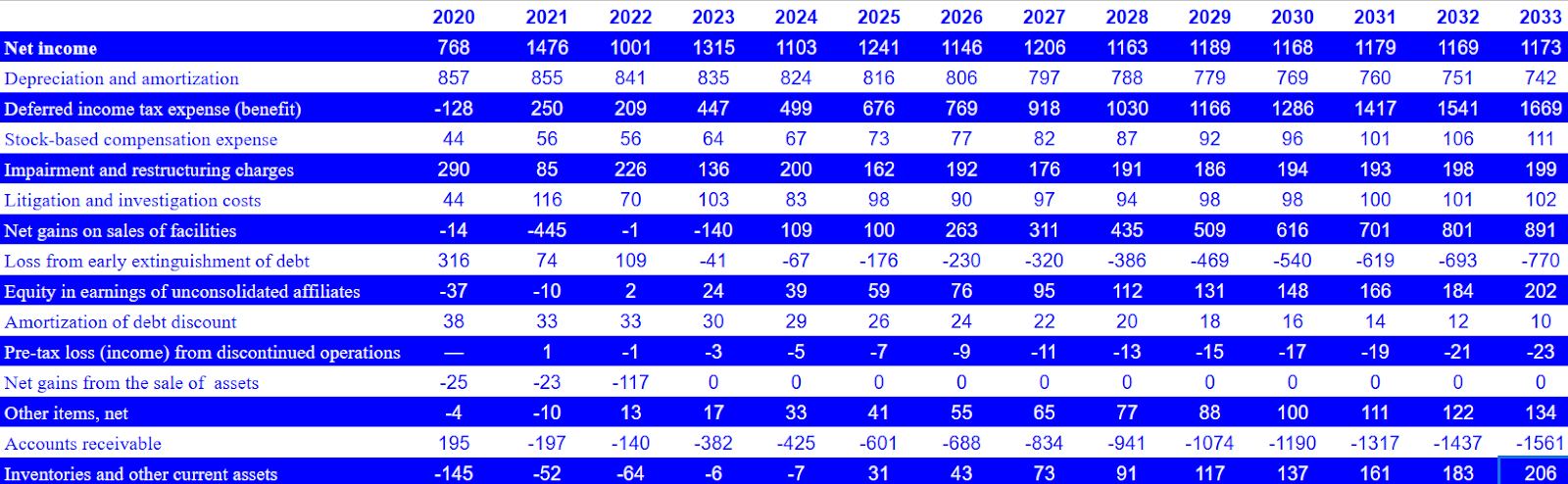

My expectations for 2033 include net income of $1.172 billion, depreciation and amortization close to $741 million, and deferred income tax expense close to $1.669 billion. Also, with stock-based compensation expenses worth $110 million and impairment and restructuring charges of $198 million, I included litigation and investigation costs of $102 million.

With equity in earnings of unconsolidated affiliates of close to $202 million, I also included changes due to accounts receivable of -$1.562 billion and changes of inventories and other current assets of $206 million.

{kind=link}

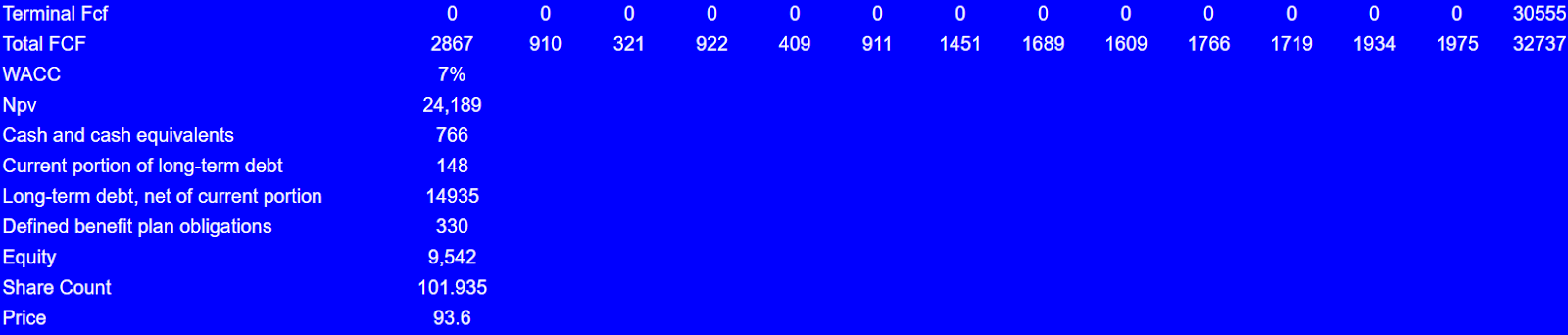

If we also include income taxes of -$408 million, changes due to accounts payable, and changes in accrued expenses, contract liabilities, and other current liabilities of -$500 million, 2033 net cash provided by operating activities would be $1.001 billion. Finally, with 2033 purchases of property and equipment of close to $1.181 billion, 2033 FCF would be $2.182 billion.

{kind=link}

Assuming an EV/FCF ratio of 14x, 2033 terminal FCF would be close to $30.554 billion. With a WACC of 7%, the enterprise value would be close to $24.189 billion. If we add cash and cash equivalents of $766 million, and subtract the current portion of long-term debt of $148 million, long-term debt of $14.935 billion, and defined benefit plan obligations of close to $330 million, the implied equity would be $9.542 billion. The implied price would be $93 per share.

{kind=link}

Risks

Among the risks for Tenet, there are healthcare program changes. In particular, changes in the Patient Protection and Affordable Care Act may push patients down in the near future. In this regard, Tenet made several comments in the last annual report.

Of the nine states in which we operate hospitals, four have taken action in accordance with the Affordable Care Act to expand their Medicaid programs; however, over half of our licensed beds at December 31, 2022 were located in five states, namely Alabama, Florida, South Carolina, Tennessee and Texas, that have not expanded Medicaid under the law. Source: 10-K

There is ongoing uncertainty with respect to the ultimate net effect of the Affordable Care Act due to the potential for continued changes in the law's implementation and how government agencies and courts interpret it. Moreover, we cannot predict what future action, if any, Congress might take to amend the Affordable Care Act. Source: 10-K

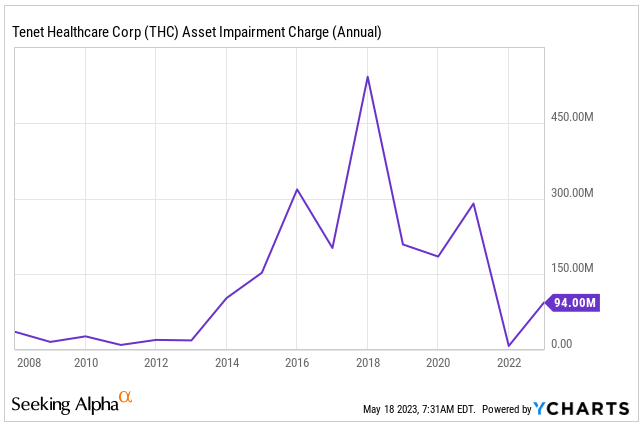

Considering the number of acquisitions made by Tenet in the past, I believe that shareholders might suffer goodwill impairments and impairments of intangible assets. As a result, I would expect declines in book value per share and perhaps declines in share price. As shown in the chart below, the company has a history of asset impairment charges. In sum, it might happen again.

{kind=link}

Besides, debt and restrictive covenants, among others, could negatively affect the company. If debt holders do not allow certain acquisitions, I believe that inorganic growth may lower, which would most likely lower the implied stock fair price.

My Opinion

Tenet Healthcare's diversified portfolio, extensive network of facilities, and focus on outpatient services provide opportunities for growth. I also believe that the recent guidance given for 2023, which includes beneficial FCF, and EBITDA will most likely bring some investors' interest. Like we saw in Q1 2023, I believe that Tenet Healthcare will most likely acquire new assets, which may enhance key performance indicators, and bring free cash flow growth in the coming years. Besides, I would be expecting higher free cash flow margin as the company continues to make recruitment and retention efforts to lower labor costs. Even taking into account changes in healthcare regulations or new regulatory standards, I believe that the stock remains undervalued.

For further details see:

Tenet Healthcare: More M&A And Recruitment Efforts Could Imply Undervaluation