THC - Tenet Healthcare: Muted Earnings Outlook Doesn't Inspire Confidence For Now

2023-07-28 18:47:38 ET

Summary

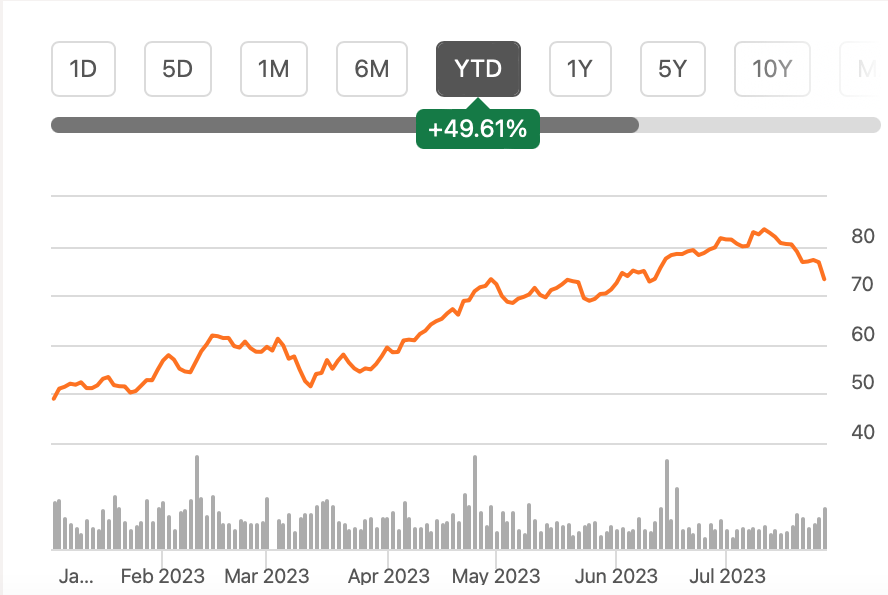

- Tenet Healthcare Corporation has seen a 50% increase in share price YTD, but can it continue to rise after its Q2 2023 results due next week?

- Tenet's Q1 2023 figures were mixed. While revenue grew, the EPS saw a big fall. The company's own outlook projects a continued earnings decline in 2023.

- While Tenet's P/E is attractive compared to the Health Care sector, it's still elevated compared to its own past levels, indicating the need for caution with regards to the stock.

The hospitals and ambulatory care company Tenet Healthcare Corporation ( THC ) has seen an impressive 50% increase in share price year-to-date [YTD]. This is starkly different from the 1% decline in the S&P 500 Healthcare index during this time. With its second quarter (Q2 2023) results out early next week post-market on Monday, July 31, here I assess if they can continue to support the stock's rise.

{kind=link}

The year so far

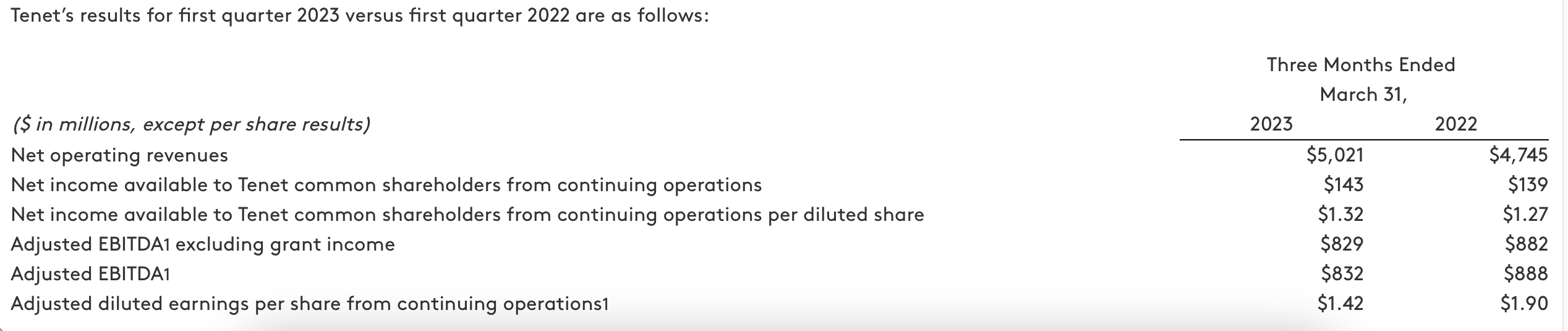

But before that, let me first provide some context, by going over its Q1 2023 results . The numbers were mixed. Net operating revenues grew by 5.8% year-on-year (YoY) on account of growth across its key segments, Hospitals and Ambulatory Care. This is a relief after a weak 2022, which saw a 1.6% revenue decline. There is a low base effect at play here for sure, but even then, there's s something to be said for the fact that even over Q1 2021, revenues showed a 5% growth.

Let me also mention here, that slow growth in 2022 isn't the red flag it looks like at first glance. It slowed because of the company's big Hospital segment, that accounts for over 78% of its total revenues, with much of the remainder coming in from its Ambulatory Care segment. The sale of five of its Miami hospitals and to lower post-COVID-19 demand were the main reasons for this. I do need to mention here, however, that THC's compounded annual growth rate [CAGR] for revenues is sub 1% over the past five years.

{kind=link}

Coming back to Q1 2023, profits did not see a similar recovery as revenues. Quite the opposite. Adjusted EBITDA fell by 6.3% in Q1 2023 and the adjusted EBITDA margin declined to 16.6% from 18.7% in Q1 2022. This is also on account of the Hospital segment, that saw a 21% decline in EBITDA, which the company chalks up to "lower COVID-related volume and acuity."

The segment has a smaller under-50% share in the consolidated adjusted EBITDA, but it still outweighed the 20% growth in the corresponding figure for Ambulatory Care, which brings in 41% of the figure. The remainder comes in from the Conifer segment, which is responsible for patient care-related business processes.

Outlook for Q2 2023 and full year 2023

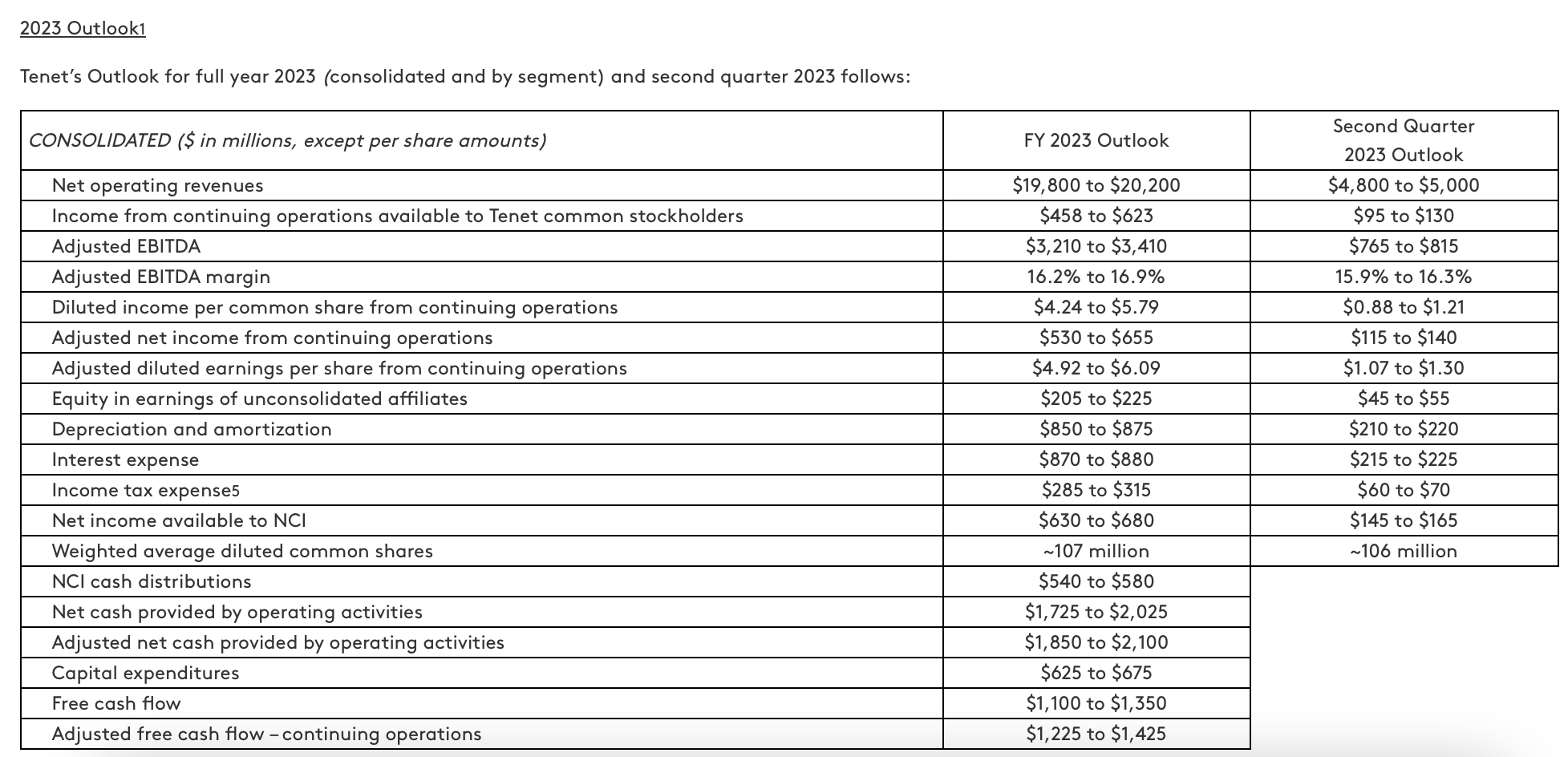

The company provides detailed guidance on both its next quarter and full year outlook. Here, I focus on three key numbers, net operating revenues, adjusted EBITDA and adjusted diluted earnings per share [EPS] from continuing operations.

It sees another quarter of sustained revenue growth in Q2 2023, of 5.6%, which also benefits from a low base effect. However, the difference is, that compared to Q2 2021, the midpoint of the range provided (see table below) is actually a 1.1% fall. So it's both good and bad.

{kind=link}

Next, adjusted EBITDA is expected to continue witnessing a decline too, and by another 6.3%. The adjusted EPS, is expected to see an even deeper decline. After a 25% fall in the previous quarter, adjusted diluted EPS from continuing operations are expected to decline by another 21% in Q2 2023.

The big reason for the dramatic fall in per share earnings last quarter was impairment, restructuring, and acquisition-related costs. The likely context for this is the sale and purchase activity the company undertook in 2021, which involved the hiving off of five hospitals in Miami, as mentioned earlier and the acquisition of ambulatory surgical centers provider SurgCenter Development. It impacted earnings in 2022 as well, and clearly, the impact continues.

A similar trend as Q2 2023 is expected for the full year 2023. Revenues are. Still projected to grow, at a slightly slower pace of 4.3%, compared to what we've seen so far in the year. Adjusted EBITDA is also expected to weaken by 4.6%, while adjusted diluted EPS is seen to continue declining drastically, by 19% for the full year.

The silver linings

The numbers, of course, don't look particularly positive. But there are silver linings. For the purpose of this analysis, as I said earlier, I have assumed the projections to come in at the mid-point of the guidance range. But analysts are, by comparison, less pessimistic. For Q2 2023, on average, they expect the EPS figure to fall by 16.8% and for the full year by 15.4% . They are similarly somewhat more upbeat about revenue figures.

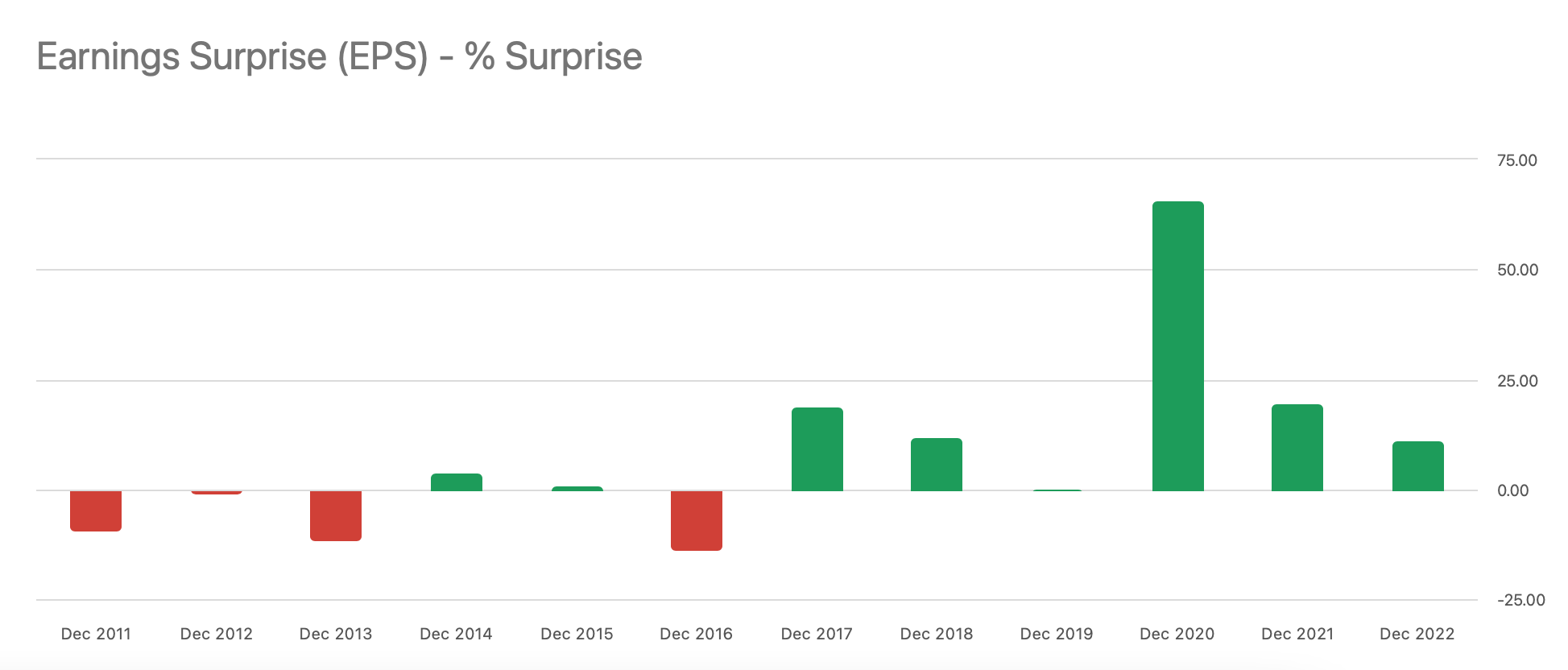

Further, EPS figures have surprised analysts' expectations on the upside consecutively for the last six years (see chart below). And by quite a margin. In 2022, for instance, the surprise was to the tune of 11.5%, and this is the smallest such seen in the last three years. If we assume that the same happens in 2023, the YoY decline in EPS shrinks to a far smaller 5.7%. Also, in 2024, they see a double-digit EPS increase, which isn't that far away now.

{kind=link}

Also, the company also upgraded its own guidance already when it released its Q1 2023 results. Let me give the example of the EPS figure here too, because its decline is most glaring. There has been a bump up of 4.6% in the guidance in this case. Tenet Healthcare doesn't give a reason for the upgrade, but if it continues, we can expect better results than are now forecast.

What the market valuations say

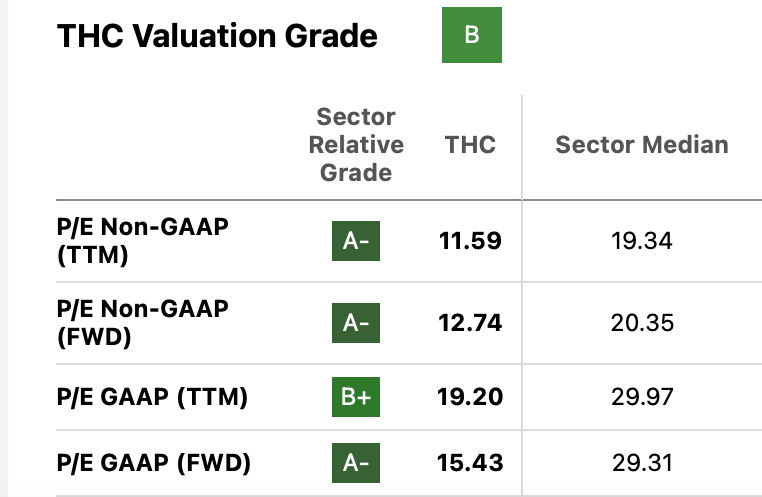

THC's market valuations don't look bad either. At 12.7x, the company's forward non-GAAP price-to-earnings (P/E) ratio is way below the corresponding ratio for the Health Care sector at 20.3x. Its trailing twelve months [TTM] non-GAAP P/E is also similarly lower at 11.6x compared to 19.3x for the sector. A similar trend is visible for its GAAP valuations (see table below).

{kind=link}

This seems to indicate that there's more upside to THC. But here's the rub. The company's trading higher than its five-year average non-GAAP TTM and forward ratios of 9x and 11.3x respectively. Further, based on its own outlook for 2023, the company's non-GAAP forward P/E is even higher at 13.4x than the 12.7x indicated by analysts' estimates. Also, its TTM price-to-sales (P/S) ratio at 0.41x, while also competitive compared to the sector, is also higher than the past five years' average of 0.26x.

So what we have here, is a stock that has a significant upside compared to the sector, but a downside compared to its own past multiples. Given the weakness in earnings displayed recently, I'm more inclined to err on the side of considering the latter. If it had shown an outlier improvement in profits and was expected to do so in the near future, it would be a separate matter. But that's not the case.

What next?

Despite the S&P 500 Healthcare index falling behind in 2023, I like the sector right now because of its defensive qualities, while the economy's uncertain. Ideally that would extend to Tenet Healthcare Corporation as well, but its past performance doesn't inspire confidence.

Even if we discount the fact its performance in 2022 suffered because of hospitals' sales, over the past five years, revenues have still been essentially flat. Added to this is the fact that its earnings look weak right now and are expected to continue doing so over the remainder of 2023.

The restructuring and acquisitions can pay off over time, of course. Tenet is already expected by analysts to perform better next year in terms of earnings. It also has a history of significant EPS surprises, which go in its favor. But when assessing the merits of the stock, we can't depend on that. Not when the company's own outlook is muted.

Tenet could see a further uptick in performance from current expectations, given that the outlook has already been upgraded. But we'll have to wait and watch. In the meantime, its price has risen higher than historical valuations. I'm going with a Hold on Tenet Healthcare Corporation.

For further details see:

Tenet Healthcare: Muted Earnings Outlook Doesn't Inspire Confidence For Now