TX - Ternium: A Long-Term Buy Despite Growth Concerns

2023-05-17 19:31:31 ET

Summary

- Ternium has been hit hard by sliding steel prices, but the company says headwinds could be easing.

- Ternium's decision to build a $2.2 billion electric arc furnace slab mill in northern Mexico has rattled some investors with respect to the stock's mid-term outlook.

- However, despite these concerns over potential growth and cash flow constraints, the stock looks significantly undervalued with the potential to deliver strong excess returns in the long run.

Ternium S.A. ( TX ), an integrated steel giant, is well positioned in the market to exploit expected growth in the Americas in the long term. Although Ternium has been pummeled recently by the nosedive in market prices, it continues to deliver solid profits and cash flows, and expects conditions to improve next quarter. Some are skeptical about Ternium's plans to invest some $2.2 billion to build an electric arc furnace, or EAF, slab mill in northern Mexico to meet trade pact requirements. Yet, even when accounting for this substantial investment in growth capex, and its impact on cash flows, the stock still appears intrinsically undervalued by almost 15%.

Headwinds Could Be Easing

Ternium, which is actually headquartered in Luxembourg, describes itself as Latin America's leading flat steel producer, with facilities in Mexico, Brazil, Argentina, Colombia, the U.S. and Central America. The company serves businesses in the construction, automotive, home appliances, packaging, transport, and energy industries. Ternium's top market is Mexico, representing 67% of shipments, followed by Argentina (18%), and the US (7%).

Ternium Shipments by Country/Region (Ternium Q123 Earnings Presentation)

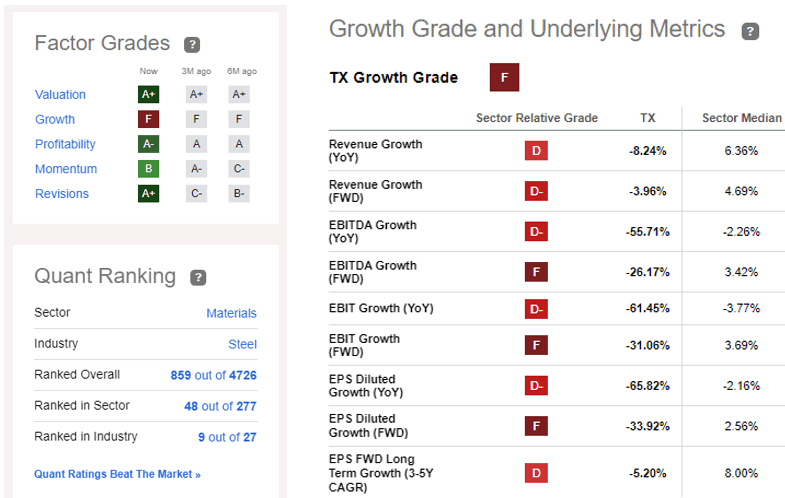

Ternium is ranked 9th among steel industry stocks on Seeking Alpha, with A's in valuation and profitability and a B in momentum. However, the stock would be ranked even higher but for an F grade in the growth category. The company is significantly down in key underlying historical and forward growth metrics, including sales, EBITDA, EBIT, and EPS.

Ternium Growth Grades (Seeking Alpha)

{kind=link}

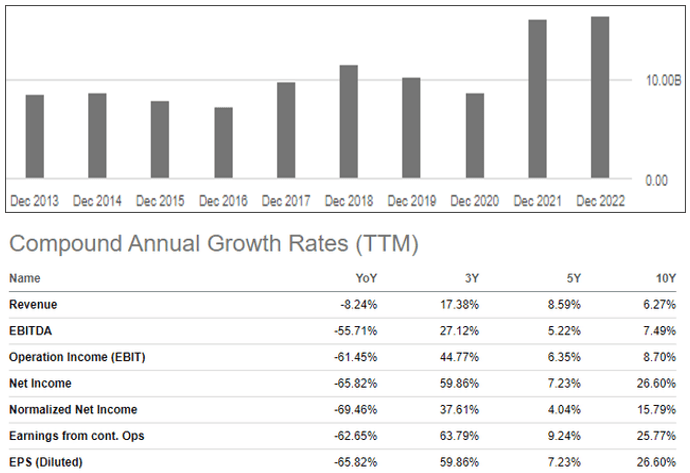

However, it is also important to point out the company has seen strong growth over the past 3, 5 and ten years in all of the same metrics. Annual sales rose over 90% between 2013 and 2022, from $8.5 billion to $16.4 billion, a CAGR of over 6 percent.

Ternium Historical Growth (Seeking Alpha)

{kind=link}

Ternium saw mixed results in terms of meeting analyst expectations in Q1, crushing the EPS target by over 90% but falling about 1 percent short of the revenue target. Based on Ternium's Q1 filings and earnings call , it appears the steel slump could be ending, with sales per ton rising slightly versus the previous quarter. Total shipments were up 4% compared to Q122 and are expected to continue rising in the next quarter. The company also expects EBITDA to increase in the second quarter, driven by higher steel shipments and anticipated sequential increases in realized prices.

Ternium Realized Prices in Q123 (Q123 Earnings Presentation)

Shipments in Mexico, the company's largest market, increased 10% to 2.1 million tons, marking a new record high for the company. Ternium said during the process they were able to boost market share in Mexico as well.

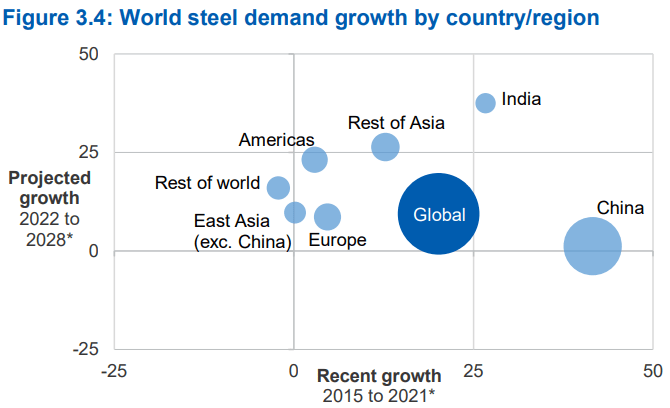

In terms of big picture future growth, Mexican steel production is forecasted to bounce back overall in 2023 and 2024 by over 2% each year, according to World Steel Association projections . Steel demand from the Americas overall is projected to grow by almost 25% by 2028 from where it was in 2022, exceeding the global average.

World Steel Production Forecast (Australian Department of Industry, Science and Resources (DISR), Resources and Energy Quarterly March 2023)

{kind=link}

Valuation

From a relative point-in-time snapshot in the now, Ternium is significantly undervalued according to every one of Seeking Alpha's underlying metrics for the category. The stock is trading at only 5.5 x earnings and 2.7 x cash flow. Some are concerned, however, that the investment in the new slab mill could hurt the longer-term valuation. In March, Itau BBA downgraded Ternium over the move, arguing that - although the EAF should help improve company profits by reducing slab costs - the intensive capex requirements will limit free cash flows from now until the middle of 2026 when the facility is due to ramp up. The objective of the project is to meet "melted-and-poured" requirements under the USMCA.

Ternium's growth capex projects overall will total $2.9 billion, including the EAF project, the company said in its 2022 annual report , to be allocated over the next four years (2023-2026) on top of the regular maintenance capital expenditures, which averaged about $600k annually in the past five years. The company, however, has not even disclosed the planned EAF's location, let alone any details on expected returns, although in the past they've said it has a minimum internal rate of return of around 10% for such projects.

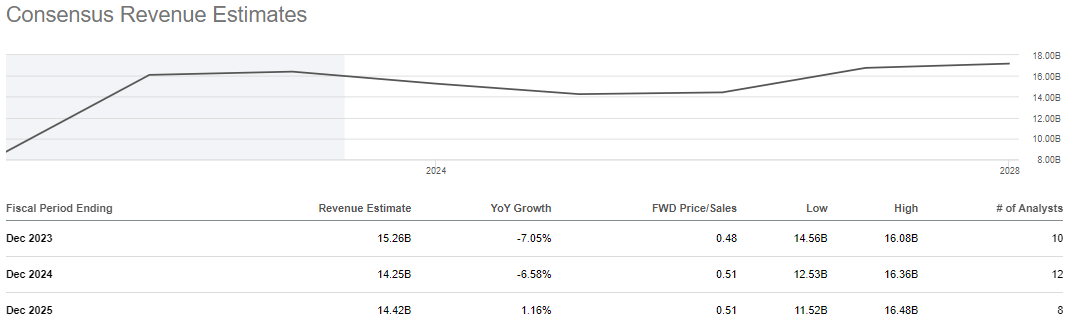

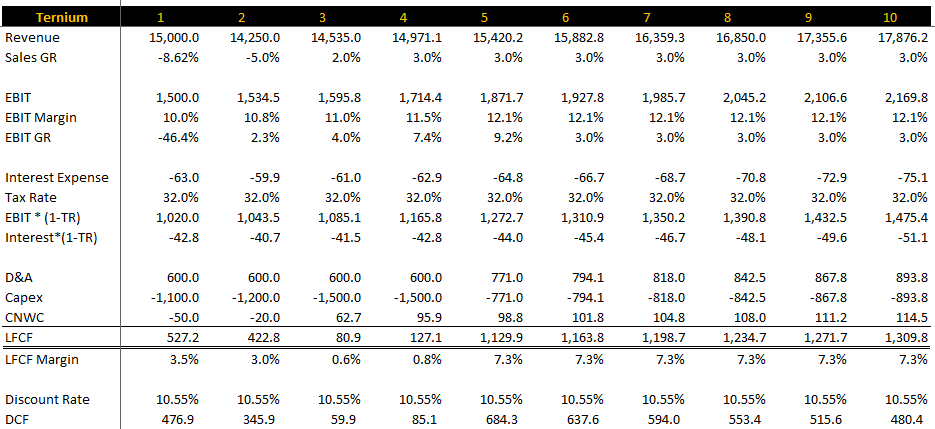

And, finally, the DCF analysis. I used consensus estimates to develop the top line for the first three years of my model. Annual sales are expected to fall by over 7% in 2023 to $15.2 billion, by another 7% in 2024, before bouncing back for slight growth in 2025. However, I adjusted these slightly for my model, taking into account my "year 1" will overlap with 2024.

Ternium Sales Forecasts (Seeking Alpha)

{kind=link}

For years 4-10, I used an annual growth rate of 3%, which seemed within reasonable bounds of the long-term projections discussed above. To "sanity" check my DCF inputs for margins and annual growth rates, I looked at averages for the past ten years, seven pre-covid years, and TTM. For year 1 of the model, however, I started with 10% for EBIT margin in line with Q123, then gradually pushed it to 12%+ by year ten. I ended with a ten-year average of 11.6% which happens to be the sector median.

The key was determining how to reasonably boost EBIT margins gradually based on the growth capex. I calculated a reinvestment rate by taking net capex + change in net working capital / NOPAT. I then multiplied the reinvestment rate by ROIC to get to an expected growth in operating margin for the subsequent year. You can see the significant rise in capex in years 3 and 4 in dollars overall and relative to revenue and depreciation.

{kind=link}

I used 10.55% as the discount rate based on equity risk premium (ERP) of 6.37% * a beta of 1.116 derived from an adjusted and levered industry average. In the end, I found the stock to be undervalued by 14% based when compared to Wednesday's mid-day share price of $39.50.

Tx DCF Analysis (MH Analytics)

The sensitivity was high around the EBIT margin, especially to the downside. For skeptics who think Ternium's EBIT will drop to 9% annually, for example, the stock is overvalued by about 30%. On the other hand, if you think the EBIT average should be 13%, the stock is undervalued by 25%.

Risks

In addition to the risk associated with the "growth" capex spending amounting to no more than regulatory expenses or any benefits being materially delayed, investors should consider that because Ternium's profit potential is highly correlated with steel prices, any protracted decline of which will have a substantial negative impact on business operations. Tied to this is the risk of any significant drops in consumption from the automotive, construction and/or home appliance sectors, in addition to excess supply both regionally (which will drop revenues) or globally (which impacts steel prices).

In addition, Ternium's vertical integration is a double-edged sword: should they fail to adequately invest in mine upkeep and exploration and exploitation, for example, they will be forced to rely more on third-parties, which will push up direct costs.

For at least the past decade, Ternium has effectively mitigated these external and internal risks in terms of protecting operating profit and net income margins - but they remain legitimate concerns and investors should be wide-eyed about them.

Conclusions

Ternium has maintained a dominant position in Latin America's steel market and is well-positioned financially and operationally to continue to do so. Although the company has been hit hard by falling steel prices, they continue to deliver robust returns, and it appears the market could be turning in its favor based on anticipated contractual and spot steel prices. Despite these strengths, the stock is trading well below its value, from a relative and intrinsic perspective, which is why I recommend it as a buy.

For further details see:

Ternium: A Long-Term Buy Despite Growth Concerns