TRNO - Terreno Realty: A Robust Industrial REIT With Strong Dividend Growth

2023-10-03 13:25:06 ET

Summary

- Terreno Realty Corporation has achieved impressive FFO and dividend growth since 2011.

- TRNO operates in high-demand coastal markets with limited supply, allowing for above-average same-store NOI growth.

- TRNO has a well-diversified tenant base, low debt, and a strong growth trajectory, making it an attractive investment opportunity.

Investment Thesis

At first glance, Terreno Realty Corporation ( TRNO ) may appear expensive, offering only a dividend yield close to 3%. However, since initiating dividends in 2011, it has achieved an impressive CAGR of 13.1% and recently hiked its dividend by an additional 12.5% . Due to its strong FFO growth and consistent dividend increases, TRNO may be an appealing choice, not only for investors focused on dividend growth.

Strategy

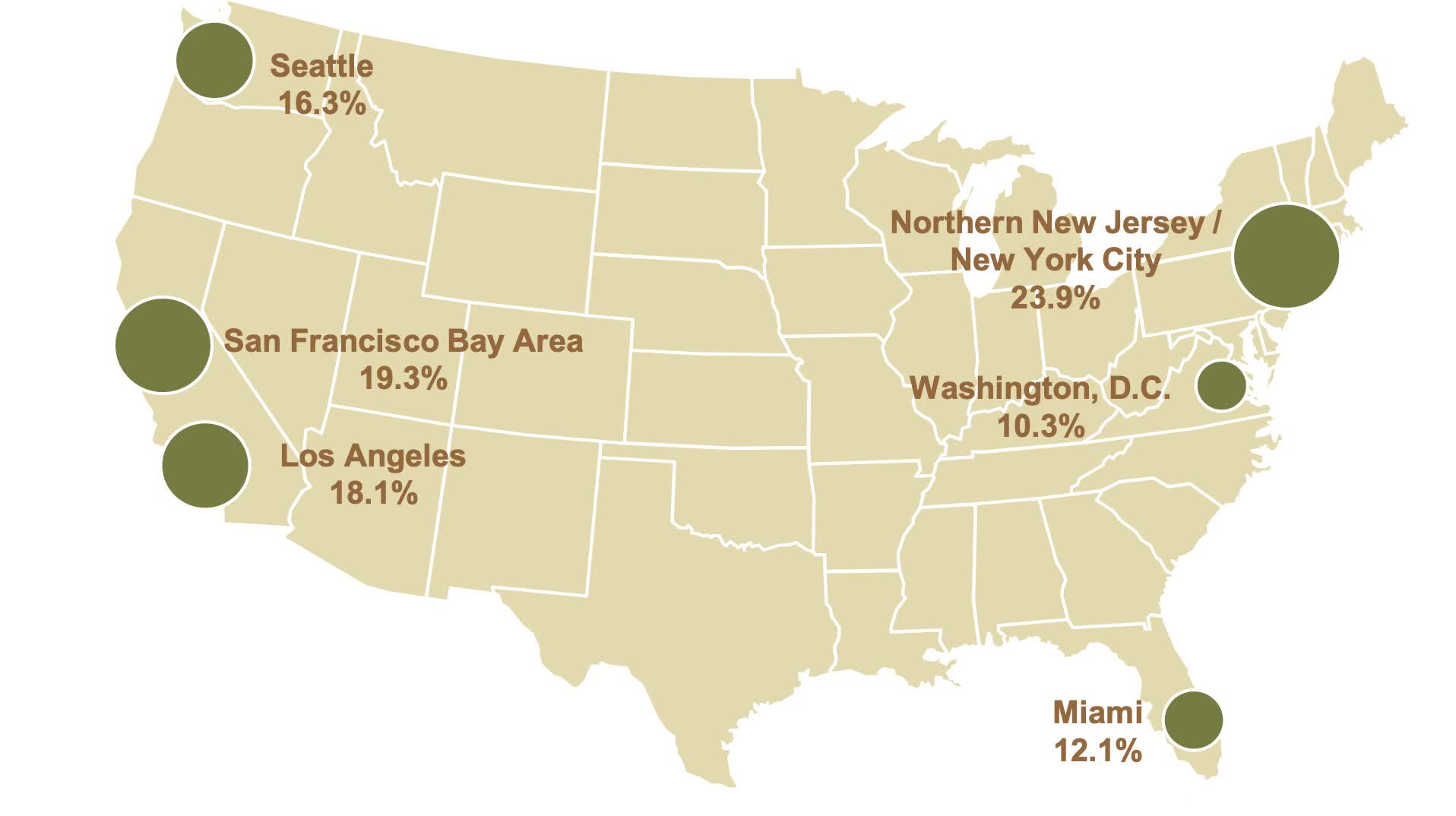

TRNO is an industrial REIT with an interesting market approach. It operates in six coastal U.S. markets, listed here in descending order of annualized base rent ((ABR)): Northern New Jersey/New York City, San Francisco Bay Area, Los Angeles, Seattle, Miami, Washington, D.C.

{kind=link}

It's worth noting that all these markets exhibit a high population density, driving demand for distribution and logistics centers. However, they also face space constraints and regulatory limitations on new industrial facilities .

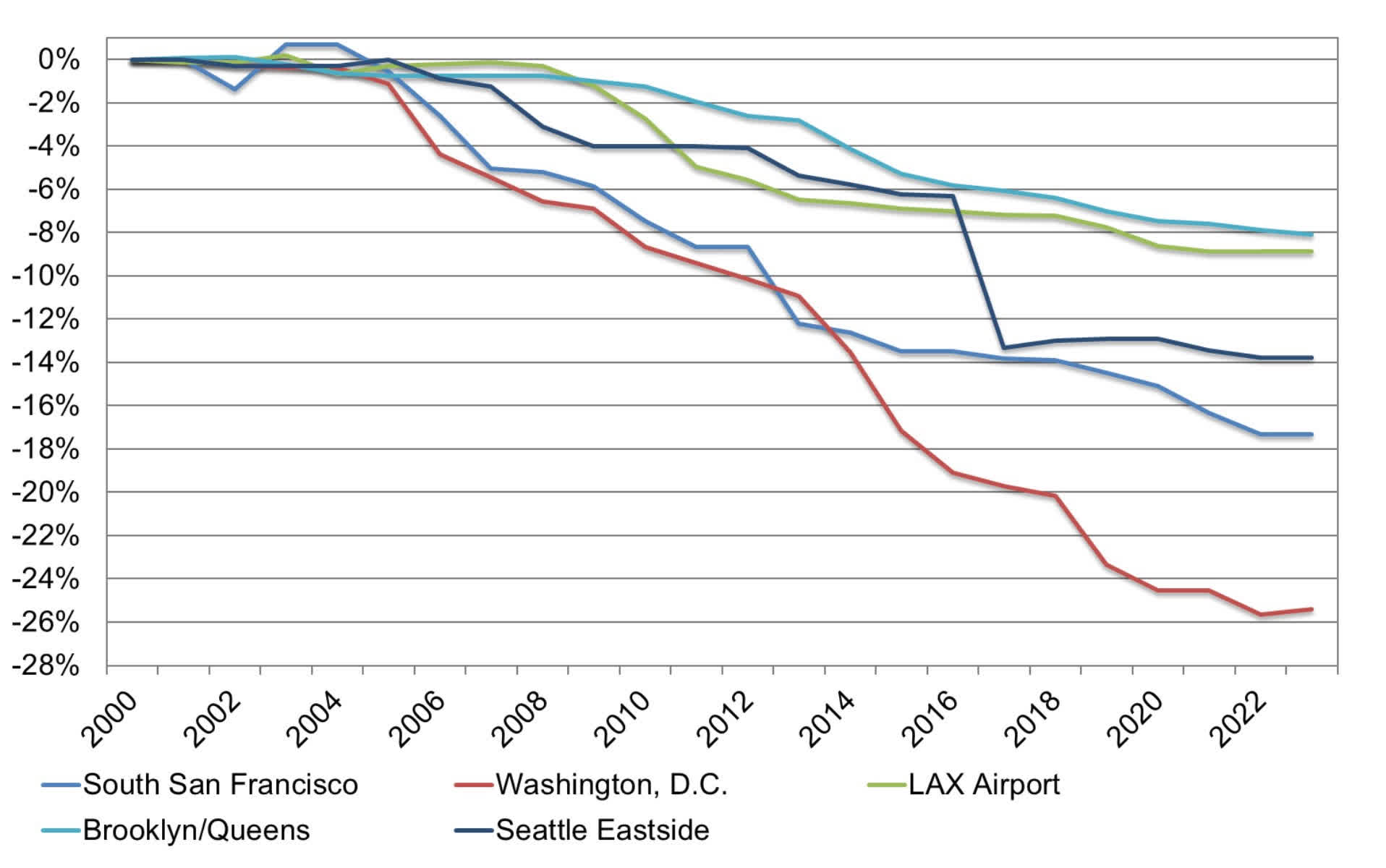

Moreover, in most of these markets, the supply of warehouses and distribution centers is shrinking. The extent of this decline in square footage in some submarkets since 2000, can be observed in the next picture.

{kind=link}

In contrast, nationwide, the industrial supply has increased by approximately 30%.

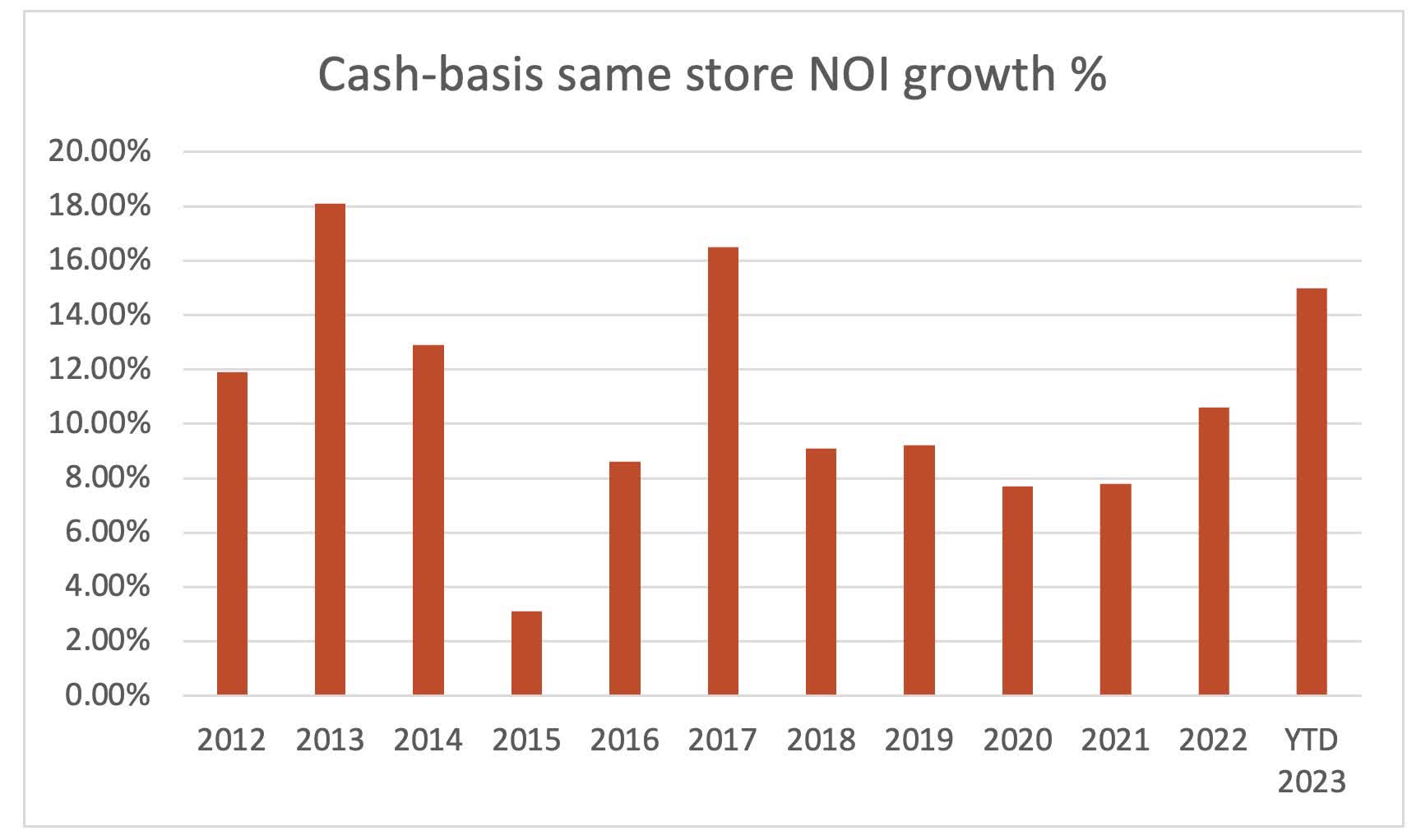

The overall market dynamic is advantageous for TRNO, allowing it to achieve above-average same-store NOI growth, due to this imbalance of supply and demand. For instance, year-to-date, TRNO has achieved an impressive 15.0 % increase in cash same-store NOI growth.

{kind=link}

Overview

TRNO owns 257 buildings in these markets, which represent 76% of its ABR.

The majority of its remaining portfolio consists of 46 improved land parcels, totaling 161.4 acres and comprising 13.5% of its ABR. The land parcels are primarily used for outdoor storage by tenants but hold the potential to be redeveloped for better use in the future. TRNO derives 6.6% of its ABR from transshipment and 4% from Flex (mostly light industrial and R&D).

Currently, TRNO holds 62.7 acres of land available for future development and is in the process of redeveloping six properties, which will have approximately 1.1 million square feet.

The majority of these ( over 90% ) consists of four buildings located in Miami's Countyline Corporate Park, close to where TRNO already operates seven other properties.

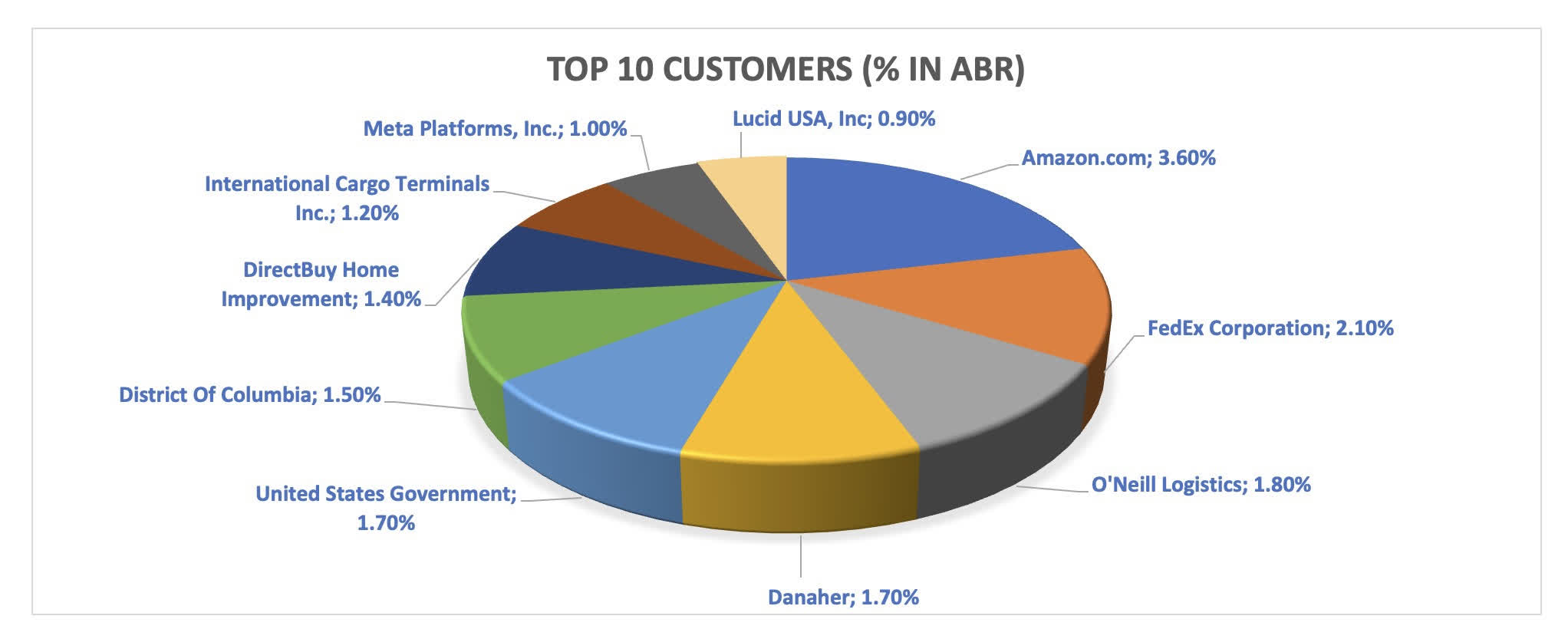

A broad tenant base helps reduce risks associated with potential financial distress among individual tenants. The largest tenant Amazon.com contributes only 3.6% of TRNO's ABR, while the top ten tenants contribute only 16.7%.

{kind=link}

In the case of tenant bankruptcies or difficulties in rent payments, it should be easy to replace them with other tenants, in my opinion.

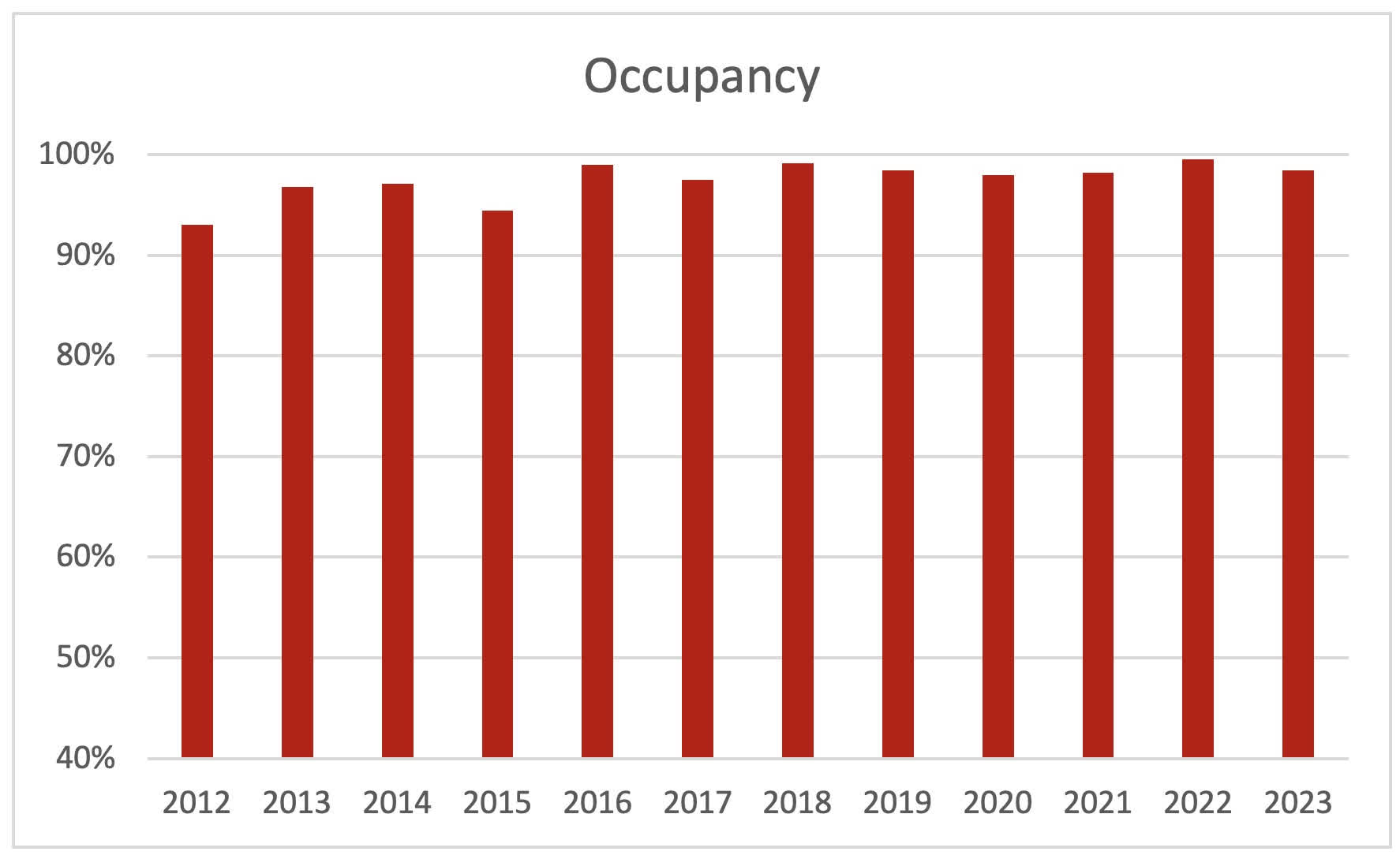

Occupancy

The same store occupancy rate stands at 98.4%, slightly lower than last year (99.5%). But still comfortably above the historical average. The overall occupancy rate is a tick lower at 97.8%.

{kind=link}

Part of TRNO's strategy involves investing in real estate with lower occupancy and redeveloping or leasing it, which explains the discrepancy between same-store occupancy and overall occupancy. The weighted average occupancy at the time of acquisition is 85.6%.

Furthermore, there are no elevated risks with the lease rollover schedule. Only approximately 3% of total ABR expires by the end of the year, with 6.5% due in 2024 and 13.0% expiring in 2025. It's important to note that lease expirations also present higher rent opportunities. I have confidence, that the management will achieve higher rents when releasing properties for the remainder of this year and into the next. In the first half of 2023, new leases and releases resulted in a 64% increase in rental income, even as approximately 8% of the total square footage had to be released.

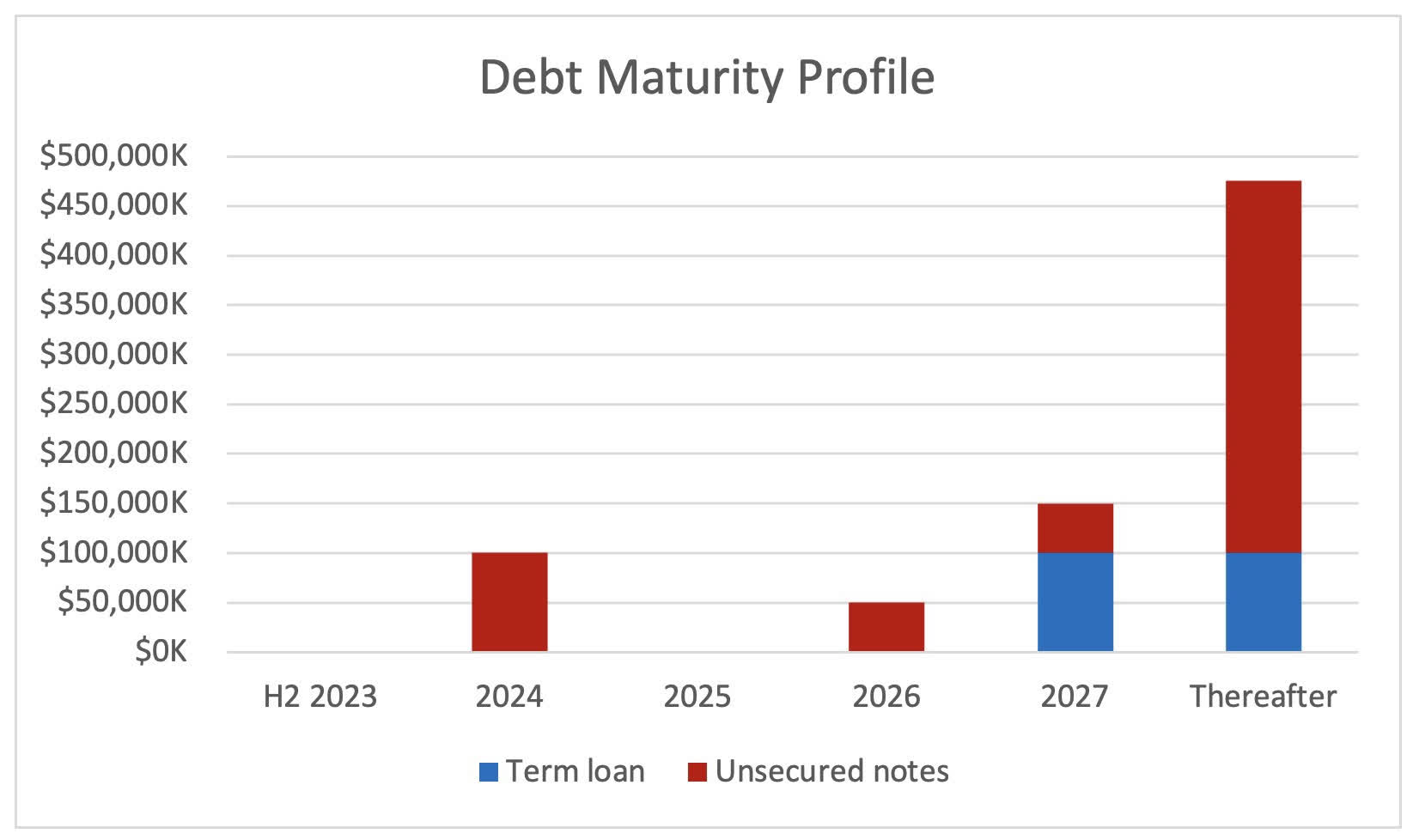

Debt

With a total debt-to-adjusted EBITDA ratio of 3.4x, debt is quite low and, in my view, easily manageable even in the current high-interest rate environment. Moreover, this ratio has shown improvements compared to twelve months ago when it was 4.1x. In terms of absolute numbers, TRNO has $771 million in unsecured debt, but only a small fraction of it is due within the next three years and the weighted average interest rate stands at 4.0% for the total debt.

{kind=link}

Additionally, TNRO has an untapped revolving credit facility, with $400 million available.

Dividend and FFO

When examining the growth in FFO and dividends, TRNO's strategy seems to be performing well. The five-year growth rate of the dividend according to Seeking Alpha is 12.89%. This rate is slightly lower than the growth rate since TRNO paid its first dividend in 2011. Put another way: The dividend per share has more than tripled in the last 10 years.

Naturally, this is only possible with FFO growth as well, and therefore it's no surprise that also FFO per share has more than tripled since 2013, rising from $0.60 to $2.00 in 2022.

Recent Results

Most of the key points from the last earning report have already been discussed throughout this article. However, I'd like to highlight one or two additional facts from the last quarter. FFO came in strong at $0.55 per share, marking a 14.6% increase compared to one year ago. While TRNO's acquisitions in 2023 totaled nearly $400 million, in Q2 TRNO invested only $13.4 million in one acquisition of a fully leased distribution center in Washington D.C. with an estimated cap rate of 5.3%. The higher acquisition sum in Q1 was largely attributed to the purchase of a 121-acre site in Miami's Countyline Corporate Park and four industrial buildings acquired in Newark, CA. So far in Q3, only one minor acquisition, a property in Santa Ana, California, for $14.8 million, has been reported in a press release. On the disposition side, cash recycling through dispositions has been limited as well, totaling $25.5 million up to August 1 this year. With the rising interest rates, I believe this is a general trend with many REIT's, and it appears to be a prudent approach.

The majority of Capex in Q2 amounting to a total of $25.78 million out of $38 million, has been used for (re)development and expansion projects, that will create shareholder value in the future. This portion of Capex has considerably increased from Q2 last year ($7.23 million), explaining the approximately 25% rise in Capex compared to Q2 2022, which stood at $30.4 million. With $400 million still in the ATM program, I believe there is no cause for concern.

Risks

Like all companies, TRNO outlines various risks in its 10-Q report, which I recommend reviewing. These risks include tenants going bankrupt, rising interest rates, and increased operational costs, as well as too high leverage.

However, in my assessment, these risks are not uniquely tied to TRNO's strategy and stand and are common to all REITs. Furthermore, TRNO boasts a well-diversified tenant base, a healthy cost structure, and a low net debt to EBITDA ratio compared to other REITs.

Investor Takeaway

Although P/FFO may look expensive, TRNO warrants a higher ratio than many peers due to its long history of notable dividend growth and similar FFO growth. With the points outlined above, I believe this growth trajectory is likely to continue in the coming years.

As the five-year average price to FFO ratio stands at 34.5x, in my view TRNO is currently undervalued, with the ratio being over 20% lower at 26.8x.

If TRNO returns to its five-year average price-to-FFO ratio and achieves a 10% FFO growth, which is below its long-term average, the share price could reach $80, marking an over 40% increase from its current value. While these assumptions carry a lot of uncertainty, also with a margin of safety the current share price offers an attractive entry point, not exclusively to dividend growth investors.

For further details see:

Terreno Realty: A Robust Industrial REIT With Strong Dividend Growth