TSCDY - Tesco: Beat And Raise Still Doesn't Warrant A Buy

2023-10-06 14:55:26 ET

Summary

- Tesco reported strong H1 results with growth in food sales and raised its guidance for operating profits for the year.

- The raising of guidance still implies a flattish H2 and we remain skeptical given the consistently moderating inflation.

- UK PM Rishi Sunak has consistently vowed to reduce inflation in half ahead of the 2024 elections.

- We believe the valuation multiples still do not warrant a Buy as a result of a strong run up in the stock through the year. Reiterate Neutral.

Investment Thesis

In continuing with our coverage of Tesco (TSCDY), we had rated Tesco as a Hold given limited catalyst for margin expansion and moderating food inflation. The company has done substantially well in H1 reporting strong LFL growth along with higher than anticipated operating profits and has further raised its operating profit guidance for the year. However, it still implied a flat growth in EBIT for the second half of the year and while we really like the market share gain with strong NPS scores, other food retailers have also been catching up with Sainsbury also reporting a 14 bps market share expansion. In addition, we believe the moderating food inflation, which can go down to single digits by the end of the year in our view, could lead to significant cost pressures which the company may not be able to substitute with higher volumes - which would continue to be a dampener. We reiterate at Hold as we believe post the 40%+ jump in share price over the year, there are significant downside risks amidst the current inflationary trajectory and its ability to consistently eke out margin expansion.

H1 Trading Update

Tesco reported strong H1 results with retail LFL sales growth of 7.8% driven by strong growth in UK/Ireland LFL sales which came in at 8.4% partially offset by a tepid 0.9% LFL sales growth at 0.9% in Continental Europe. Food sales drove the increase with a 10.6% growth whilst a 4.8% LFL decline in clothing and home sales reflected the exit of low margin categories such as large consumer electronics. UK/ Ireland Q2 LFL sales growth came in at 8.0% compared to Q1 of 8.8% as a result of moderating inflation through the second quarter while CE LFL was impacted by inflation and tougher comparables primarily within Hungary which reported negative volumes as inflation shot up to 31%. ALDI price match distributions currently at ~650 products (from 700 products in 1Q), with price-lock on 1,000+ products until January. Prices were cut on approx. 2,500 products by H1 that are on average ~12% cheaper than the start of the year. In addition, UK online outperformed grabbing market share (~70 bps) and stable penetration (at 13%).

Group level Adj. EBIT jumped 14% YoY at £1,482 mn delivering a beat to the consensus. The strong growth was driven by a 14% jump in retail Adj. EBIT as a result of stable volumes and benefits from its Save to Invest program (~£290m of savings) partially offset by cost pressures while Tesco bank EBIT jumped 25% YoY driven by higher net interest income and lower bad debts (5.7% compared to 6.4%). Within Retail, UK and Ireland reported a strong margin expansion by 50 bps at 4.4% driven by continued market share gains leveraging its brand positioning while CE margins declined by 160 bps as a result of significant cost pressures amidst declining volumes.

Management raised the guidance for the year and now expects full year FY24 Adj. EBIT to be £2.6 - £2.7 bn driven by strong first half results. However, that still leads to a flattish Adj. EBIT in H2 2023 and a modest improvement in operating margins.

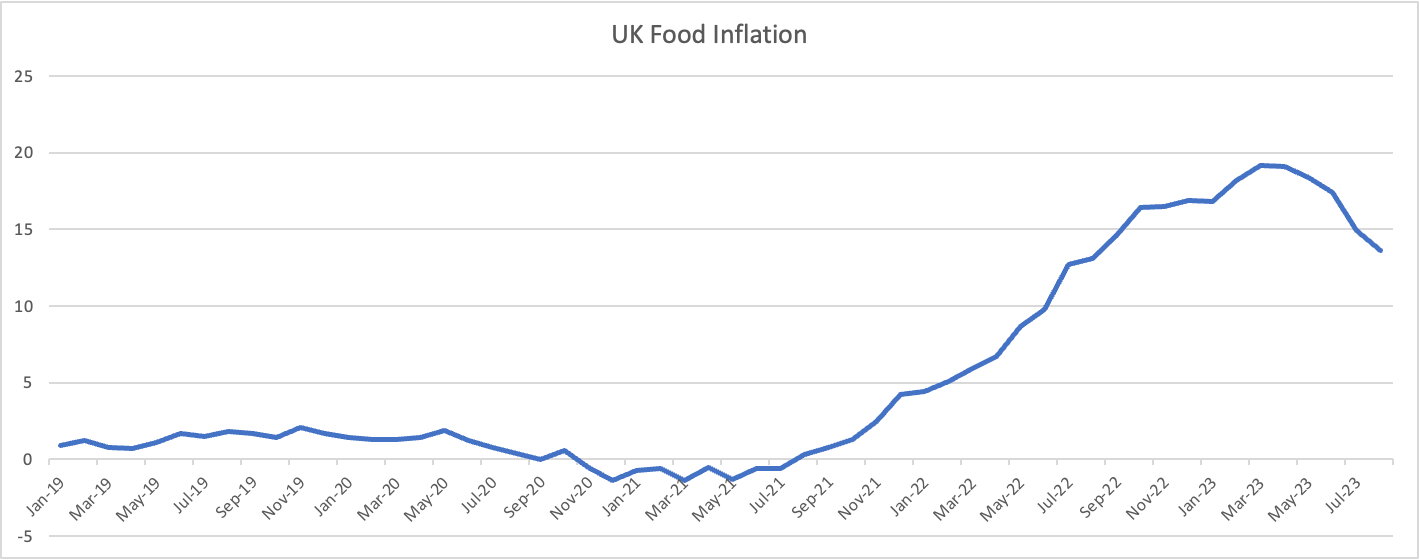

UK Food inflation has continued to moderate since peaking in March and BOE Chief Economist, Huw Pill is expecting it to be at 10% by the end of this year with IGD forecasting an 8-10% food inflation by the end of the year and the possibility of turning negative in 2024. We believe the strong H1 growth was primarily as a result of record inflation with relatively expensive essentials inflating the SSS growth of the food retailers. However, as the price hikes unwind, it would become a serious headwind as the volumes may not be able to compensate for the decline as a result of pricing actions.

Office for National Statistics, UK

{kind=link}

In addition, the UK Prime Minister Rishi Sunak has consistently vowed to halve the inflation ahead of the 2024 elections, which may seem a tall task as a result of rampant inflation, but nonetheless, the government pressure and public outcry can also lead to policy changes such as price freezes, price matching and discounts as was recently announced in Canada .

Valuation

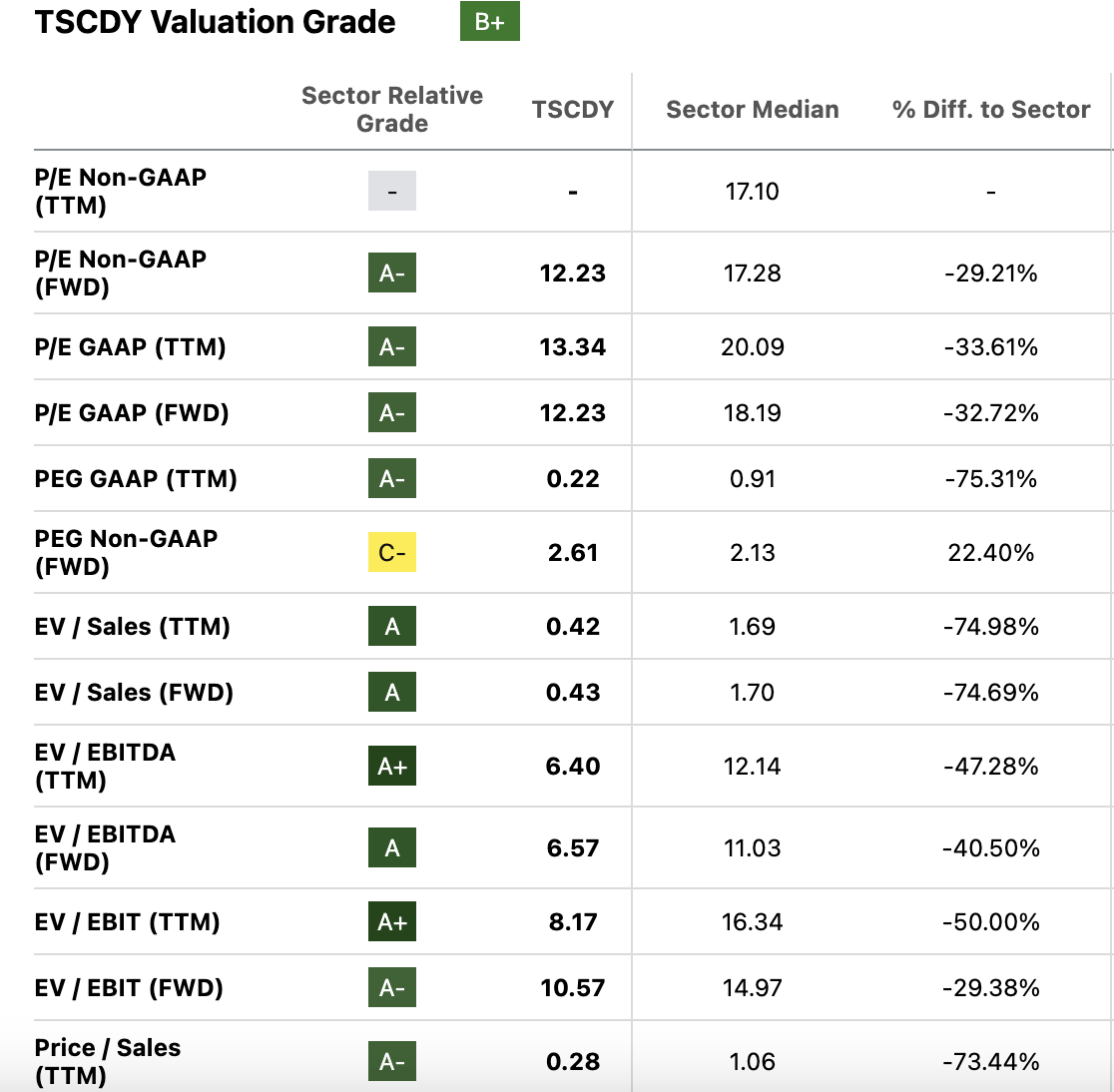

Tesco trades at about 12.2x Fwd P/E compared to the sector median of 17.3x, a ~30% discount compared to its peers. The relative discount is primarily as a result of the lower growth and return ratios compared to its peers. In addition, looking on a PEG basis, the stock still appears to be expensive compared to peers as it trades at 2.6x PEG compared to industry PEG of 2.1x.

{kind=link}

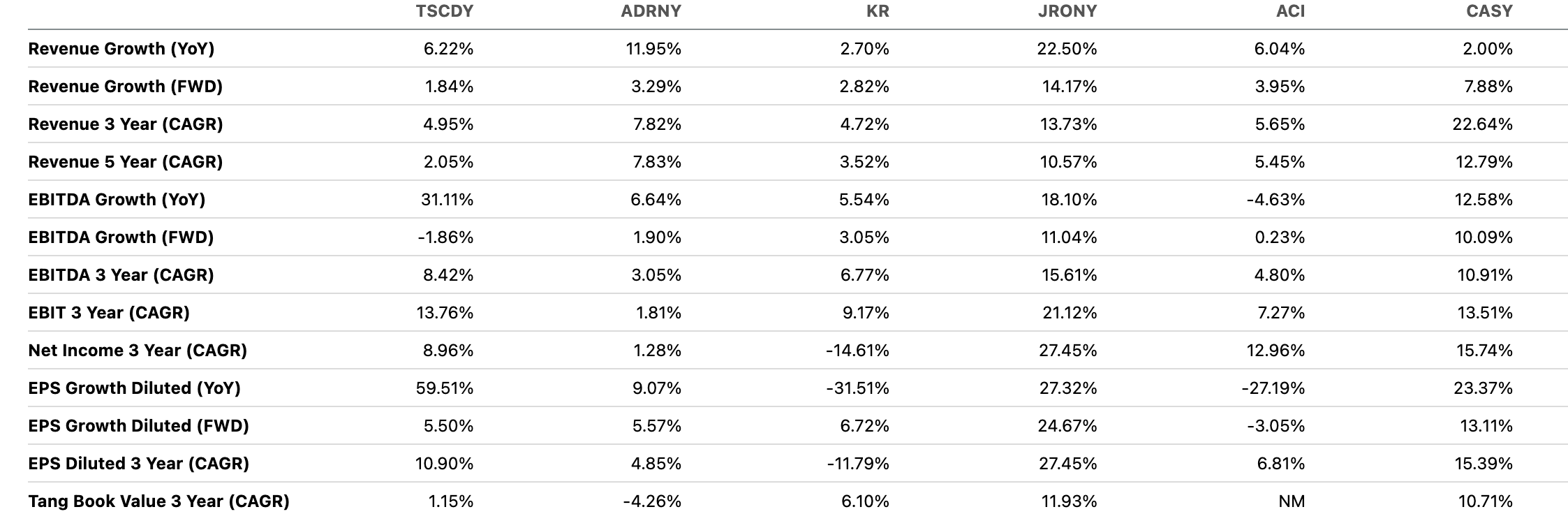

Tesco had the slowest revenue growth compared to its peers in last 5 years while its EBITDA growth is towards the higher end compared to 3 of its peers. In addition, the forward revenue, EBITDA and EPS growth is amongst the lowest compared to its peers which justifies the implied discount.

{kind=link}

We believe while the company has done substantially well in H1 2023 and has a healthy dividend yield, the company is still essentially guiding to a flat growth in operating profits for H2 2023. We believe the current multiple still leaves limited margin of safety and we reiterate our Hold rating.

Risks to Rating

Risks to rating include:

1) Macroeconomic uncertainty can lead to declining consumer spends which can lead to consumers trading down, impacting operating margins

2) Competitive pressure may intensify from discount retailers and other broadline retailers which can lead to price wars and higher promotional activities which can lead to declining operating margins

3) Government policies which aim to cap prices or bring some regulatory framework to curb inflation could be a negative for the retailers

4) Upside risks include management focus on shareholder value creation driven by dividends and share repurchases which can provide support to the stock

Final Takeaways

Tesco has reported a strong set of numbers, beating the consensus which sent the shares soaring higher. In addition, it also boasts a higher yield among the high dividend stocks with an attractive dividend yield of 5%+. However, we believe there are near term downside risks as a result of moderating food inflation and growing political pressure in the UK for reducing inflation ahead of the elections next year. We believe the current valuation multiple, which appears to be at a discount, still does not provide a margin of safety given the already strong run up in the stock for the year. Reiterate Hold.

For further details see:

Tesco: Beat And Raise Still Doesn't Warrant A Buy