TSCDF - Tesco: Better Earnings On Improved Macro Conditions And Good Decisions (Rating Upgrade)

2023-10-06 12:32:15 ET

Summary

- Tesco's stock price saw a sharp rise since releasing its interim results, as it improved sales growth and its profits have started expanding again.

- While softer cost inflation has played a part, the company's own cost savings program and responsiveness to customer demand underpin this improved performance.

- Its market multiples look attractive now too, as does its dividend yield, indicating there are gains to be made by investors.

Since I last wrote about the UK’s biggest supermarket Tesco ( TSCDY ) in late March, its price is up by 6.3%. This is underwhelming. What’s not underwhelming, though, is the healthy 5.5% gain it has seen since it released its interim results recently. It’s now up by almost 10% from the closing price on October 3.

With inflation finally coming off, the Bank of England recently pausing rate hikes and the economy avoiding a recession, the macros are clearly more in favor of the grocer than they have been in the recent past. The question now is, can it sustain its price rise? Let’s look at the latest figures to find out.

A look back

When I last looked at Tesco, its Christmas trading update for 2022 showed improved year-on-year (YoY) performance. However, the company noted that consumers had started trading down for more cost-effective products, reflecting the stretch on consumer’s budgets from high inflation.

High-cost inflation had also impacted the company’s profits for the first half (H1 FY22/23), with its financial year ending on February 25, 2023. But with sales still growing and a cost-saving initiative in place, it was possible that FY 23/24 could look better. And the outlook for the next year was key to determining how the stock could perform going forward.

For the full year FY 22/23, the company’s sales picked up from H1 FY22/23 with a 5.3% sales growth at constant currency (H1 FY22/23: 3.5%). The decline in adjusted operating profit slowed down too, to 7.1% (H1 FY22/23: -9.8%). The company’s adjusted retail operating profit also came in line with expectations at just shy of GBP 2.5 billion, in line with its forecast range of GBP 2.4-2.5 billion.

{kind=link}

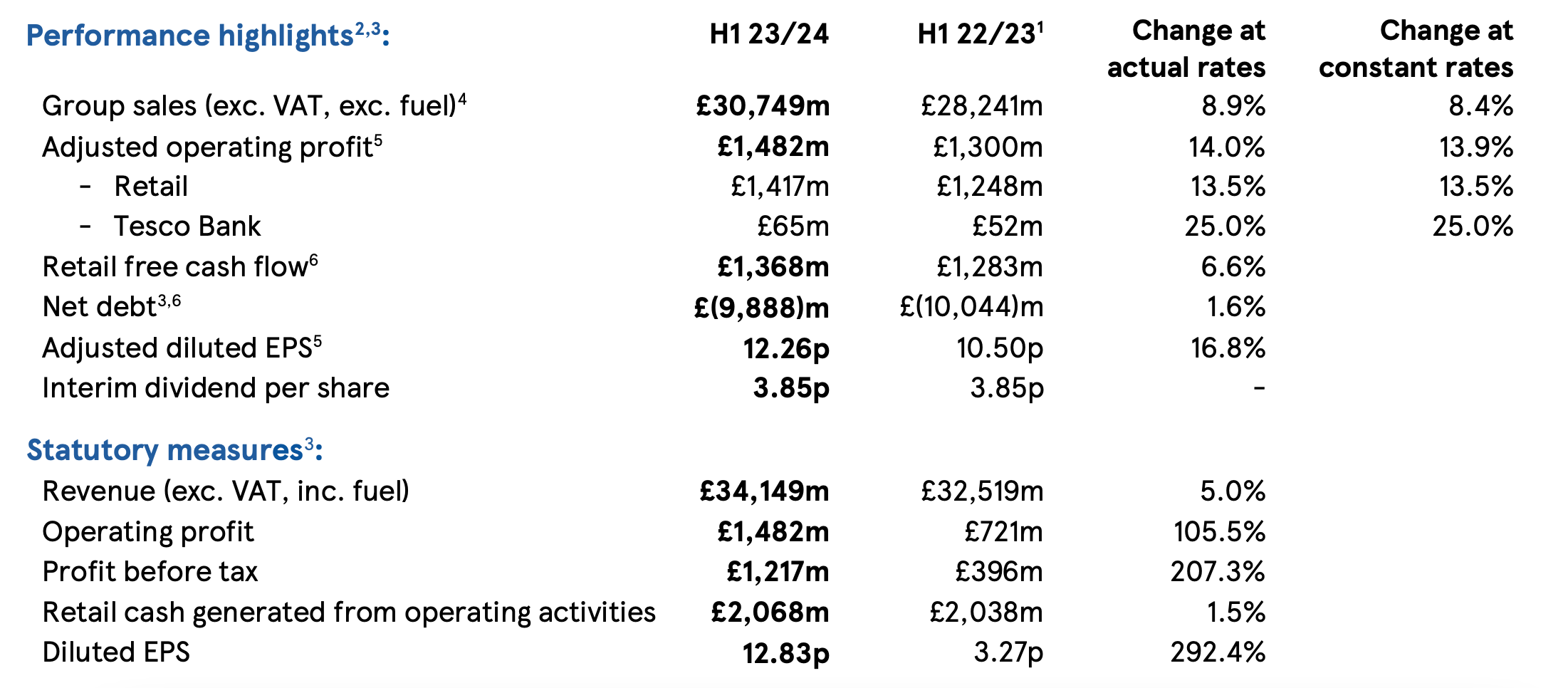

Robust H1 FY 23/24 results

The latest figures show significant improvement in Tesco’s performance in H1 FY 23/24, with sales growth at 8.4% at constant currency, though revenue growth, which also includes fuel sales, was lower at 4.6%. Responding to the earlier noted trend of trading down to the company’s own branded products, it increased its own range to over 1,100 options. With consumers also eating in more, it launched over 150 new products under its premium ‘Finest’ range, which saw a 4.1% rise in volumes in H1 FY 23/24.

{kind=link}

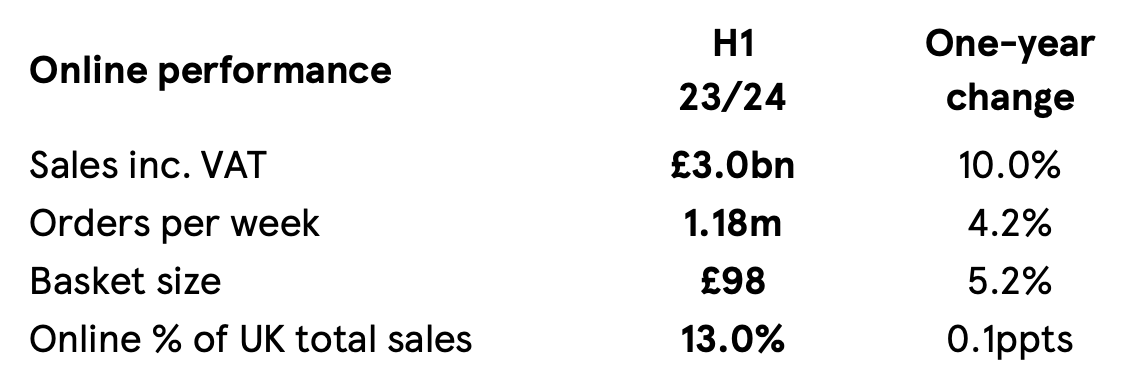

Growing online sales

Interestingly, the post-pandemic shift in online sales has sustained. With the segment’s contribution at 13% of total UK sales now, it’s higher by 4 percentage points from before the pandemic. Online sales also saw a healthy growth rate of 10%, increasing Tesco’s market share in the category.

{kind=link}

Higher income on cost savings

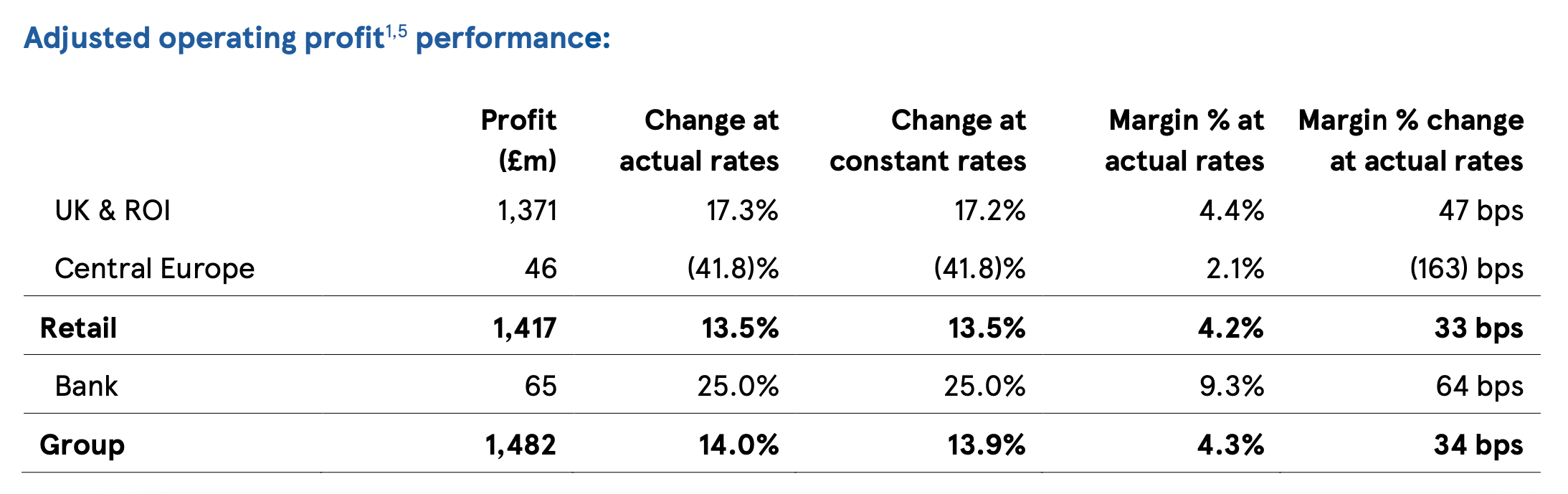

In a break from last year’s trend, the company also reported a 13.9% increase in adjusted operating profit, which was essentially due to the slowing down in the cost of sales growth to 2.4% (H1 FY 22/23: 9.8%). This is partly due to an easing in the cost of inflation but also because of its own cost-reduction efforts.

The company targeted GBP 1 billion in cost savings between February 2022 and 2024. In FY 22/23 it delivered savings of GBP 550 million, and has saved another GBP 290 million in H1 FY 23/24. It now targets total savings of GBP 600 million in FY 23/24 and says that it will result in “at least” GBP 1.1 billion of cumulative savings over the target period.

In line with its improved performance, the company has raised its operating profit outlook a bit from the earlier GBP 2.5 billion to GBP 2.6-2.7 billion now. The gains in H1 FY 23/24 were driven by its retail operations, basically in the UK and Ireland, with a 47bps margin improvement.

{kind=link}

It also reported a 16.8% increase in adjusted diluted earnings per share [EPS], which was helped by its share buyback program. Of the GBP 750 million worth of shares expected to be bought back between April this year and the next, some GBP 503 million have already been purchased in H1 FY 23/24.

What the market multiples say

The company’s trailing twelve-month [TTM] GAAP price-to-earnings (P/E) ratio is now at 12.9x, a marked decline from the elevated 21.1x levels it was at when I last checked. Not only is this way below the 20.9x levels for the consumer staples sector, but it’s also below its own long-term median P/E of 18.6x.

In my estimates of the company’s forward GAAP P/E, I’ve assumed the revenue to be 50.7% of full-year revenues based on past years’ averages. This is slightly higher than the number for H1 because of higher demand during the festive season that falls in H2. With the net profit margin assumed to be at 2.1%, the same as that for the TTM, the forward GAAP P/E ratio comes in at 13.3x. This is also lower than the sector average of 18.2x.

Essentially, all the multiples point in one direction, and that’s a price rise. Even considering that the economy could weaken further going forward, there’s a definite double-digit increase in store for Tesco. Additionally, its dividends are worth considering too, with Tesco’s forward dividend yield at 5.45% right now.

What next?

The Tesco story looks much better than it did the last time I checked. Its sales have continued to grow as the grocer continues to respond actively to changing customer trends, especially at this time when the high cost of living has stretched budgets. Its profits are rising again as well, supported by lower cost inflation and its own cost-saving program. That the company has made consistent efforts to grow through strategic changes of its own, builds confidence in its ability to improve even difficult conditions.

With improved earnings and weak price trends, Tesco’s market multiples also look way more attractive than they did the last time I checked. Its healthy dividend yield is another positive to consider. Even though macroeconomic risks haven’t been entirely overcome yet, on balance the prospects for the stock are significantly improved now. I’m upgrading Tesco to Buy.

For further details see:

Tesco: Better Earnings On Improved Macro Conditions And Good Decisions (Rating Upgrade)