TSCDF - Tesco: Limited Near Term Catalyst Neutral

2023-08-03 22:39:02 ET

Summary

- Tesco's performance has been lacklustre, with its stock price declining 13% over three years compared to its peers.

- The company had a strong start to FY23-24, with LFL sales growing 8.2% YoY and reiterating its FY24 guidance.

- Bulls believe Tesco has a strong operational track record and 4%+ dividend yield, while bears are concerned about easing food inflation and margin pressure.

- We initiate at Neutral for lack of catalysts in the near term.

Investment Thesis

Tesco ( TSCDF ) is the largest food and non-food retailer in the UK with presence across several countries in Europe. Its performance has been lacklustre significantly underperforming its peers with its stock price declining 13% over the three year period as it grappled with declining margins.

It reported a strong Q1 and start to the FY23-24 with LFL sales growing 8.2% YoY, in line with the estimates, driven by UK and ROI increasing 9.0% YoY and growth across formats led by Large and Convenience store formats in the UK. It reiterated its FY24 guidance with flat level of retail operating profit and its continued commitment with £750 mn worth of stock repurchases for the year should enthuse investors. We believe Tesco will be able to grapple with the tightening of consumer wallets given its lesser exposure to discretionary items. However, post the 30%+ jump since October last year and amidst margin pressure due to easing inflation, we believe there is limited upside potential. Initiate at Neutral.

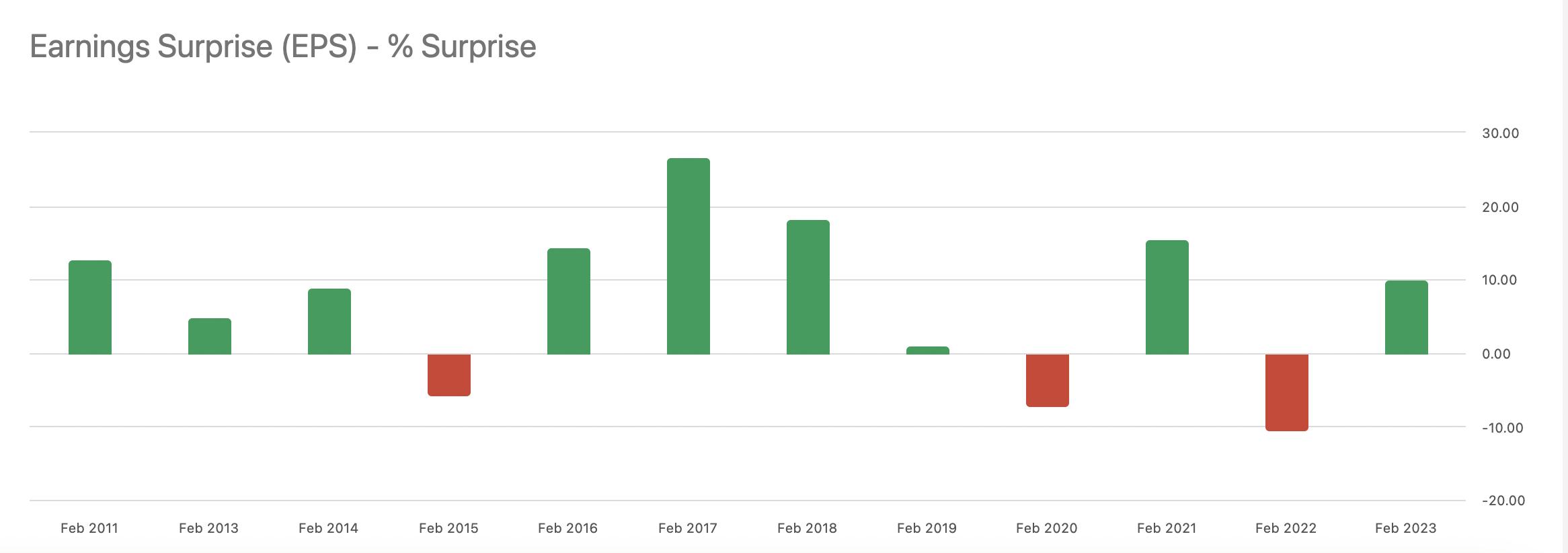

What do Bulls Say?

Tesco has a strong operational track record over the years beating earnings 9 out of 12 times over the past decade as well as 6 out of 8 quarters over the past 2 years.

{kind=link}

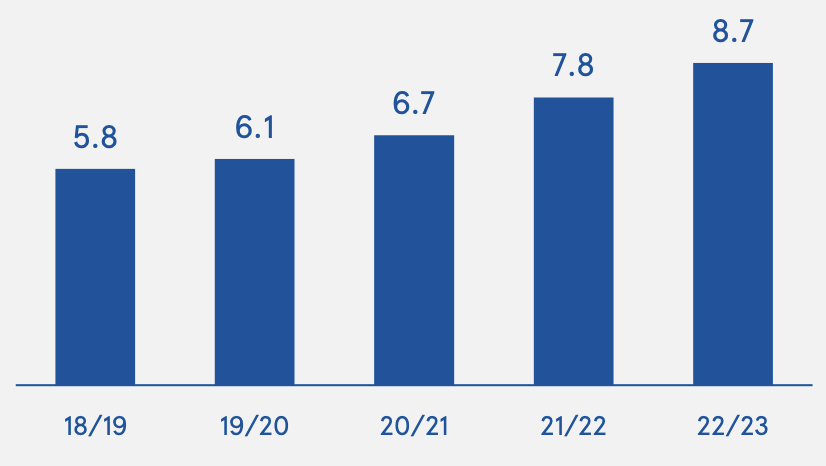

A strong start to FY24 underpins the retailers visibility of defending its market share as well as maintaining its margins. Booker had been performing exceptionally well reporting its highest ever sales figures in FY23 and further continuing the momentum into FY24 with double digit sales growth across Retail (ex-Tobacco) and Catering.

Booker Sales (in £bn)

{kind=link}

Apart from that, it returned £1.6 bn in shareholder value through dividends and buybacks and has further committed to 50% net payout ratio and an additional £750 mn in share repurchases in the coming year. At 12x Fwd P/E and a dividend yield of 4.2%, the stock is a defensive play amidst a looming recession and has a favorable risk reward.

What do Bears Say?

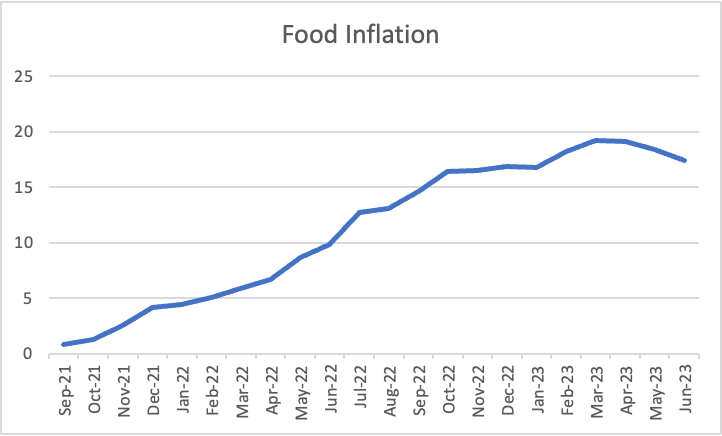

Food inflation has been easing and is expected to decline further to under 9% by the end of 2023.

Office for National Statistics, UK

{kind=link}

Despite higher inflation, the company has not been able to lift margins as a result of sticky wages and other fixed costs as well as promotional environment.

We believe given the moderating inflation and price cuts which is being passed on to the consumers (prices of bread was cut by 12% and of broccoli and pasta by 16% compared to last couple of weeks) along with its focus on maintaining market share and sticky wages and fixed costs, there is no upside to margin performance.

Its performance in the past 2008 recession has been somewhat lacklustre as it continued to focus on defending market share and yet it reported a 2% LFL growth in Q3 FY2009, it's worst growth in 16 years despite, and led to a squeeze on the margins.

Inflation, excluding petrol, reduced substantially in the quarter, and is declining more rapidly in Tesco than in the wider market as we seek to help customers to spend less by reducing prices and making more affordable products available, including through the recent launch of our new ‘Discounter’ products and related range and price changes.

- As per FY 2009 Q3 Results

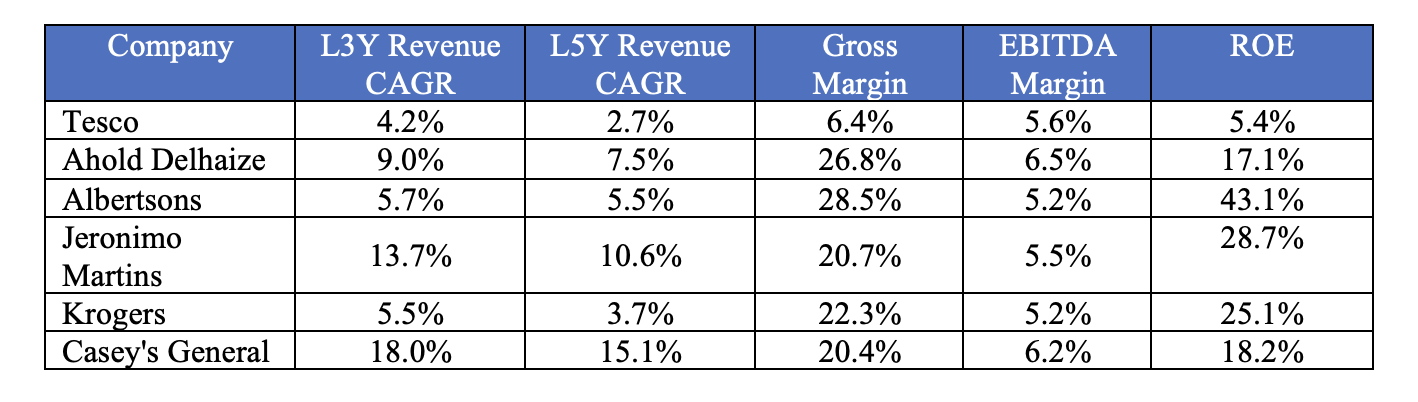

The company trades at 12x 1Y Fwd P/E and it appears at a discount to its peers which trades at average 1Y Fwd P/E of 14.5x. However, this discount is warranted given the relative underperformance of Tesco in terms of growth metrics and margins and that is being reflected in the stock price.

{kind=link}

Conclusion

We believe the company has posted a strong start to FY2024 with stellar LFL growth across the counters. It has also achieved £550 mn in cost savings last year providing a better visibility to achieve its stated goal £1 bn target by next year. However, with moderating inflation and sticky wage costs, we believe there are lack of catalysts to warrant a further upside in margins. While we do believe the customers may marginally trade up with easing inflation, it may not be material to see any margin upside. While the share buyback and dividends will keep investors enthused, we have a neutral stance and would await for any catalysts to drive the margins higher. Initiate at Hold.

Risks to Rating

Risks to rating include

1) any change in the macroeconomic backdrop would significantly affect the consumer preferences and spending patterns which would in turn impact sales of the retailer

2) Intense competitive pressure and higher promotional environment by other retailers and discounters in order to defend market share would further squeeze margins

3) Further initiatives for shareholder value creation will likely be looked as key positive for the share price.

For further details see:

Tesco: Limited Near Term Catalyst, Neutral