OCDDY - Tesco: Recipe For Success Dominating The U.K. Groceries Market

2023-07-17 00:08:47 ET

Summary

- Tesco is the leading supermarket retailer in the UK. It has navigated increased competition and is set for growth in line with economic development.

- The company's scale/geographical reach, multi-format approach, robust online presence, and innovation contribute to its strong market share.

- Relative to peers, Tesco looks quite attractive, with higher margins. UK inflation continues to pose a risk to this.

- Relative to peers and its historical average, we believe Tesco is attractively priced.

Investment thesis

Our current investment thesis is:

- Tesco is the leading supermarket retailer in the UK, with a highly defensible position due to its extensive supply chain and geographical reach.

- The company has faced increased competition in the last decade but has seemingly navigated this well. This current offering to consumers is highly attractive, allowing for continued growth in line with the industry.

- Relative to peers, the company performs well on a profitability basis but lacks growth. Based on this, we see upside.

Company description

Tesco PLC ( OTCPK:TSCDF ) is a leading multinational retailer based in the United Kingdom. With a presence in several countries, it operates a wide range of grocery and general merchandise stores, including supermarkets, hypermarkets, convenience stores, and online platforms.

Share price

Tesco's share price has significantly underperformed, losing over 45% of its value in the last decade. This is a reflection of its unsuccessful expansion into the US, alongside the increased competition in its core markets, such as the UK.

Financial analysis

{kind=link}

Presented above is Tesco's financial performance for the last decade.

Revenue & Commercial Factors

Tesco's revenue has traded flat during the last 10 years, as various periods of decline have offset any growth achieved. Post-pandemic, growth looks to have returned, with successive years of growth.

Business Model

Tesco employs a multi-format approach, operating different store formats to cater to various customer needs and the geographical landscape, from large hypermarkets to small convenience stores. This hybrid approach allows the business to expand its reach in its key geographies by adapting to its environment. Further, Tesco will price its products in response to its location, with smaller convenience stores charging a premium.

Further, to drive increased footfall, Tesco has developed the services provided within and around its stores, especially the larger ones. Such services include Pharmacies, Eat-ins, Travel Money, Electric charging points, Petrol stations, Car washes, etc.

The company offers a diverse range of private-label products across various categories, providing value and differentiation. This has been a key focus for the business, seeking to grow across the price spectrum, while still offering consumers an attractive value proposition. This is a change in the industry, as the private-label approach historically was to undercut the premium option.

Tesco has a robust online presence, offering grocery delivery and click-and-collect services to meet changing consumer preferences. Tesco has invested heavily in its online presence, as well as its national reach, likely having the strongest offering in the UK.

Tesco's loyalty program, the Clubcard, was an incredible innovation in the industry, seeking to collect data before the concept of data analysis became mainstream outside of tech. This continues to drive customer retention and engagement, while allowing the business to understand consumer spending habits and personalize its engagement.

In conjunction with its primary groceries operations, Tesco also operates a clothing line, Bank, Mobile services, and other small functions.

Competitive Positioning

Tesco's competitive position revolves around its strong brand, which consumers know for its high-quality products, a large array of options, and convenience. Secondly, the company benefits from its well-established supply chain globally, enabling efficient distribution, cost-effective acquisitions, and product availability.

Groceries Industry

Groceries businesses differentiate themselves through pricing strategies, promotions, and quality offerings. Tesco faces competition in the UK from other supermarket chains like Sainsbury ( OTCQX:JSNSF ), Asda, Morrisons, Waitrose, Marks and Spencer/Ocado ( OTCQX:MAKSF )/( OTCPK:OCDGF ), Co-Operative, Iceland, as well as discounters like Aldi and Lidl.

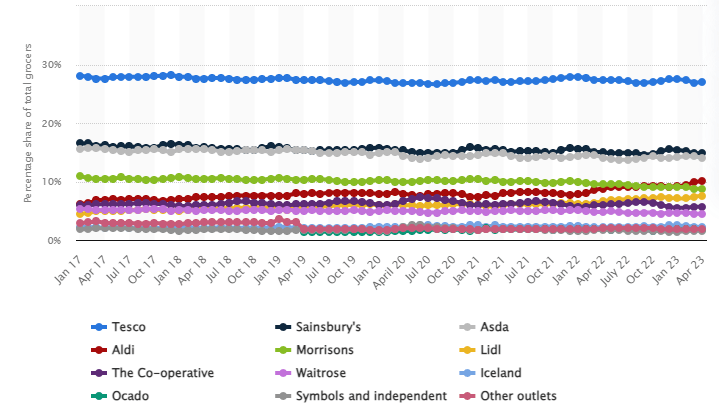

Tesco is currently the largest player in the UK, with a substantially higher market share than its next nearest competitor, Sainsbury.

UK Supermarket Market Share (Statista)

{kind=link}

This market share advantage is a reflection of its reach in the UK alongside brand superiority, providing the business with a highly defensible position, as to overtake the business would require a significant financial investment. There are many territories where the majority of the largest players operate, such as large towns and cities, and so the superiority of its brand (and services offered) should not be downplayed.

In the last decade, the traditional big 4 (Tesco, Sainsbury, Asda, and Morrisons) have faced significant pressure from Aldi and Lidl, as both businesses aggressively expanded in the UK through undercutting. Both businesses cut costs wherever possible in order to achieve this, to much success. The growth trajectory of both was accelerated by the GFC, as many consumers began to struggle financially, and most of the West went into an extended period of Austerity.

This competition continues to be a concern, although less so for Tesco in recent years. This is because, as the graph above illustrates, most of the market share has been taken from its peers. Secondly, Tesco, and others, have begun price-matching Aldi, closing the value delta.

Economic & External Consideration

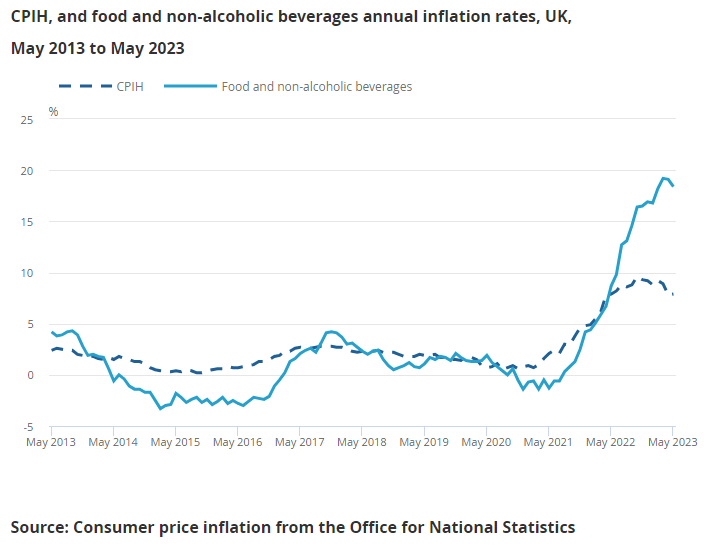

Current economic conditions have been highly disruptive for consumers, with inflation and interest rates contributing to a significant squeeze on finances. As a groceries operator, Tesco's supply chain has been significantly impacted by this, with food costs rapidly rising and forcing the business to pass these on to consumers. Thus far, margins have crept up but not materially so, implying impact parity.

Consumers have been highly critical of businesses increasing their prices, even if they are not necessarily profiting in excess. We believe Tesco has transitioned this well, having publicly locked prices for many goods for an extended period of time.

{kind=link}

Looking ahead, UK food inflation is currently at its peak level, with most essentials significantly rising in price. This creates risk for Tesco as it navigates the current conditions. Sainsbury, for example, was slow to increase prices as a means of winning customers (a slight gap to Asda is observed several months prior) but is now forced to rapidly increase due to margin pressures.

{kind=link}

Margins

Tesco's margins have marginally improved during the majority of the decade, although remain below the FY13/14 levels. This initial erosion is due to competition but the current upward trajectory implies an improvement in its current position.

We suspect as inflationary pressures subside, likely in the next 6-8 months, Tesco could gain further, reaching c.7%.

Balance sheet & Cash Flows

Tesco is conservatively financed, with a ND/EBITDA ratio of 2.6x. The majority of this is leases and so we are not overly concerned about solvency.

Tesco's capital allocation has been conservative, with Management maintaining a healthy cash balance, while distributing the remaining to shareholders. The current yield is high but sustainable, with Management able to reduce buybacks to support this.

Outlook

{kind=link}

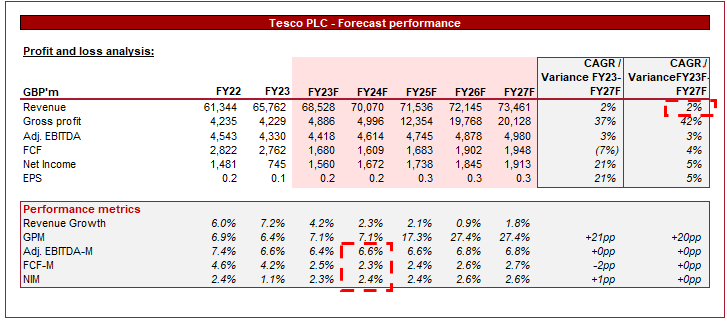

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a 2% growth rate in the coming years, essentially in line with the long-term growth rate. This is a reasonable estimate given the lack of outperformance levers.

Margins are also forecast to improve although slowly, a positive development. This will likely occur as inflation is declining, allowing Tesco to price smartly as costs decline.

Industry analysis

Food retail industry (Seeking Alpha)

{kind=link}

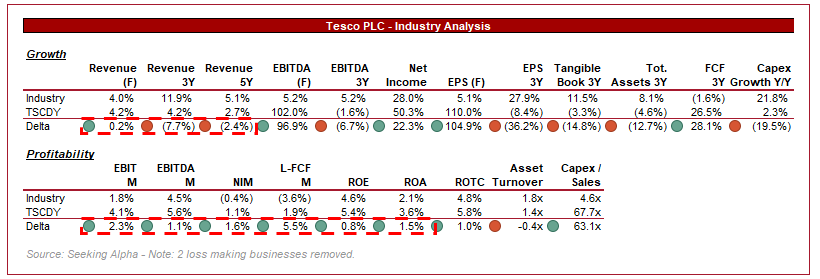

Presented above is a comparison of Tesco's growth and profitability to the average of its industry, as defined by Seeking Alpha (14 companies).

Tesco's growth is underwhelming relative to the group, although is a reflection of smaller growth businesses inflating the average.

When profitability is compared, Tesco performs far better, leading comfortably on every key metric.

Our view is that the profitability metric is far more important, as the industry is highly mature, reducing the scope for high growth once scale is reached. Based on this, Tesco is positioned well for an attractive relative valuation.

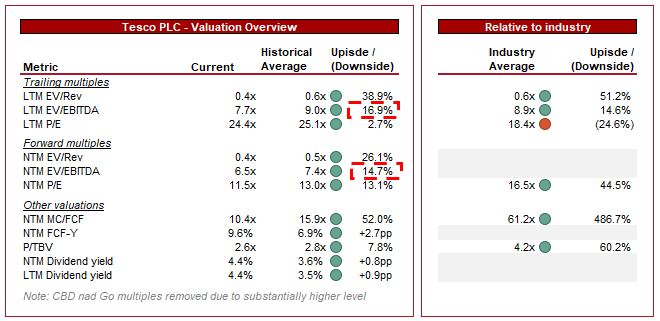

Valuation

{kind=link}

Tesco is currently trading at 8x LTM EBITDA and 7x NTM EBITDA. This is a discount to its historical average.

Tesco's discount to its historical average does not look appropriate. The company looks to be on a better trajectory, although the growth is more a reflection of price action rather than volume, while its competitive position is shown to be defensible. This implies a slight premium to its historical average, but to be conservative at least a 15-17% upside.

In order to assess Tesco's relative valuation, we have also excluded Grocery Outlet ( GO ) and Companhia Brasileira De Distribuicao ( CBD ), both of which are trading at a noticeable premium to the rest of the businesses, distorting the average. Based on this, it implies upside for Tesco. We believe the business is positioned well compared to these businesses and so to trade at a discount implies at least a 15% upside.

Based on this, we believe Tesco is attractively priced, with upside of 15-20%. This remains below analysts, whose consensus price estimate is 23%, with 8/11 buy/outperform ratings.

Key risk to our thesis

The key risk to our thesis is the development of inflation in the UK. British consumers can only bare so much and so if prices continue to increase, we could see consumers reducing their spending or turning to discount retailers.

Final thoughts

Tesco looks to be a well-positioned business. It has substantial scale and brand value in the UK, allowing the business to achieve consistent growth in line with the industry. Although Aldi and Lidl continue to present a threat, the normalization of Tesco's market share position implies this pressure is subsiding.

Relative to peers, we believe Tesco is attractively positioned, with its valuation implying upside.

For further details see:

Tesco: Recipe For Success, Dominating The U.K. Groceries Market