TSCDY - Tesco: Valuation Is Not Reflective Of Better Market Position

2023-04-19 15:36:45 ET

Summary

- Tesco had a solid FY23 with strong retail segment FCF and operating profit, despite inflationary pressures.

- The cost savings program is on track to exceed expectations, and the retail media opportunity presents significant growth potential.

- The current valuation of Tesco does not reflect the company's improved competitive position and growth opportunities, such as the convenience network and prospects of major growth in media income.

Overview

I believe improved margins and a more robust growth profile in recent years attest to better management at Tesco ( TSCDY ). TSCDY, in my opinion, has recovered some of its market share because of its increased competitiveness on price, enhanced price image, product offerings, and improved execution in matching discounters on certain basic items (hence keeping customers that leave for discounters in the store). It has also shifted its emphasis from costs and cash flow to creating a consistent history of capital returns for shareholders. As a result, I think TSCDY is in a better position now than it has been in the past, and if the current upswing continues, it should lead to a positive re-rating of the stock price. Therefore, I advocate a buy recommendation.

FY23 results were solid

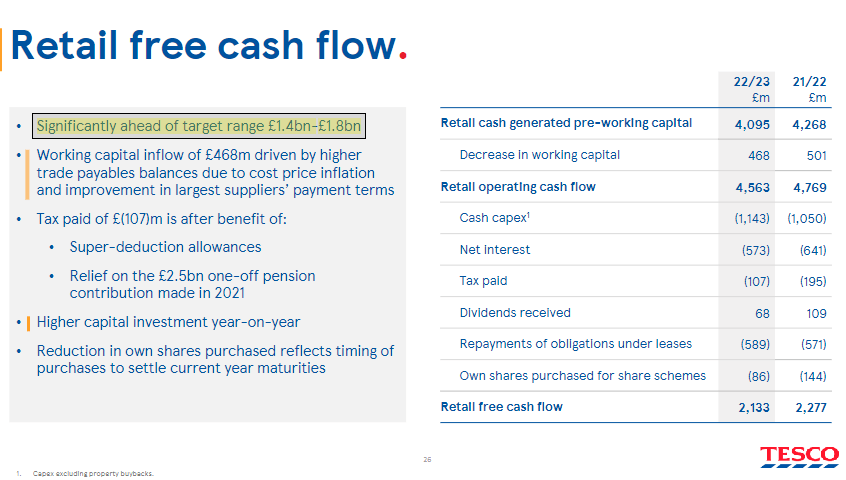

Tesco had a very successful FY23. The retail segment's FCF of £2.13 billion was significantly higher than the guided £1.8 billion, and the retail segment's adj. operating profit of £2.49 billion was within the upper bound of the guidance range. UK & ROI adj. operating profit drove the y/y decline due to falling volumes, significant OPEX inflation, and price investments, but results were good relative to guidance. However, despite significant market inflation affecting volumes, Central Europe fared better with good cost control and reported an adj. operating profit of £180 million. The release of a COVID-19 macroeconomic provision last year likely contributed to the 18.8% drop in adjusted operating profit for Tesco Bank, which came in at £143 million. Retail like-for-like sales increased by 5.1% despite inflationary pressures and post-COVID normalization, contributing to a 5.3% increase in total group sales, which reached £57 billion. Sales in the UK and ROI were up 4.7% year-over-year, and sales in Central Europe were up 10.4% year-over-year. After listening to the earnings call, I was similarly upbeat. The tone was upbeat, with the underlying business fundamentals and the ability to compound cash appearing to be in good shape.

Cost savings program

A major takeaway for me is that significant progress is being made by management to speed up the cost-cutting initiative and bring in at least one billion pounds by February 2024. With £550 million taken out so far, management is already $100 million ahead of its annualized run rate. In addition, management stated that they would prefer to fully offset the OPEX inflation over FY24 like they did last year, which, according to my calculations for energy and wages, could lead to greater cost savings than anticipated (well over £100mn).

Retail media

Clubcard's popularity keeps growing, and there are now 14 million active users across the UK. The way management has been talking about the retail media opportunity has given me hope. While I don't have the precise numbers, we can make educated guesses about the magnitude of the opportunity. Assuming a profit margin of 50%, given how highly incremental this revenue is, would result in approximately £140 million in extra profit for Tesco, assuming a revenue opportunity of £280 million. These profits are likely to be used to expand operations in the short term, but it should be available to investors as a pool of growth capital eventually.

Guidance

Management has projected a range of £1.4-1.8 billion in retail free cash flow, £130-160 million in adjusted operating profit at the bank, and a relatively stable adjusted operating profit at the retail level. The announcement of a £750 million share buyback over the next twelve months is another positive signal that the company's balance sheet strength and FCF generation are on the upswing and inspires my confidence in this forecast. I think the capital return story would bring many investors back into the name, potentially driving a valuation re-rating upwards, if Tesco actually does as it guides.

{kind=link}

Valuation

The current valuation of Tesco, in my opinion, does not reflect the company's improved competitive position over the past. Tesco is trading at 12.5x forward earnings, which is below its long-term average. As I see it, Tesco's growth opportunities, such as the convenience network, and the prospects of major growth in media income over the medium term should help the company emerge stronger from the COVID period. On the latter, I believe this profit stream will further improve the overall margin profile as well. If we combine all these together along with the capital return story, it is not hard to imagine the market attaching a higher multiple to the stock, if it does what I expect.

Conclusion

TSCDY has shown improved management, increased competitiveness, and a focus on capital returns for shareholders, resulting in a better market position than in the past. The FY23 results were solid, with strong retail segment FCF and operating profit, despite inflationary pressures. The cost savings program is on track to exceed expectations, and the retail media opportunity presents significant growth potential. Management's guidance and share buyback program inspire confidence in the company's future. I recommend a buy recommendation, as I believe the market will attach a higher multiple to the stock if it continues on its current trajectory.

For further details see:

Tesco: Valuation Is Not Reflective Of Better Market Position