TSCDF - Tesco: Waiting For FY2023 Results

2023-03-29 03:43:22 ET

Summary

- The UK's biggest supermarket Tesco hasn't done too badly in the stock markets in 2023 so far, exceeding the performance of both S&P 500 and FTSE 100.

- Sustained sales growth, market dominance, and fruitful cost-cutting measures go in its favour. But the two macroeconomic challenges of high inflation and slow growth can squeeze profits.

- With an elevated P/E, a further hit to profits could mean that its price is due to fall. So much depends on its next set of results and its outlook.

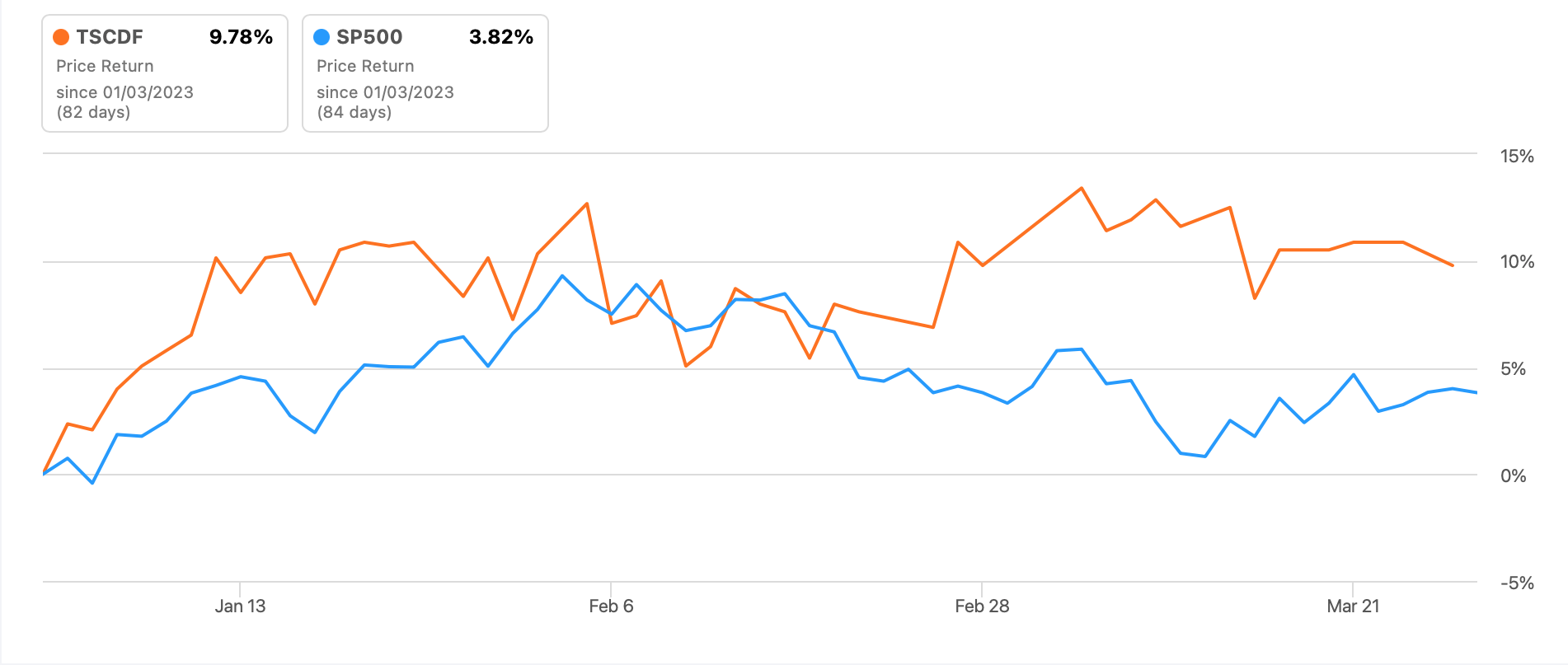

UK's biggest supermarket, Tesco ( TSCDF ) has not done too badly at the stock markets in 2023 so far. Year-to-date [YTD], it is up by 10%. This is striking, compared to the sub-1% rise in the FTSE 100 ( UKX ) index seen over this time, which is an index of the biggest companies by market capitalisation at the London Stock Exchange, which is also the place of Tesco's main listing. It has also performed better than the S&P 500 ( SP500 ) index, which is up by 4% YTD (see chart below).

Price returns (Source: Seeking Alpha)

{kind=link}

However, much of this positive momentum was witnessed at the start of 2023, when the stock markets were relatively more upbeat as inflation showed some initial signs of coming off. Much has changed since. Since I last wrote about Tesco in the second week of January, its price is up by just 2.8%. This too is a shade better than the S&P 500's rise over this time, but that is not saying much. Stock markets have been facing uncertain times and investor hesitation is natural.

Persistent inflation impacts numbers

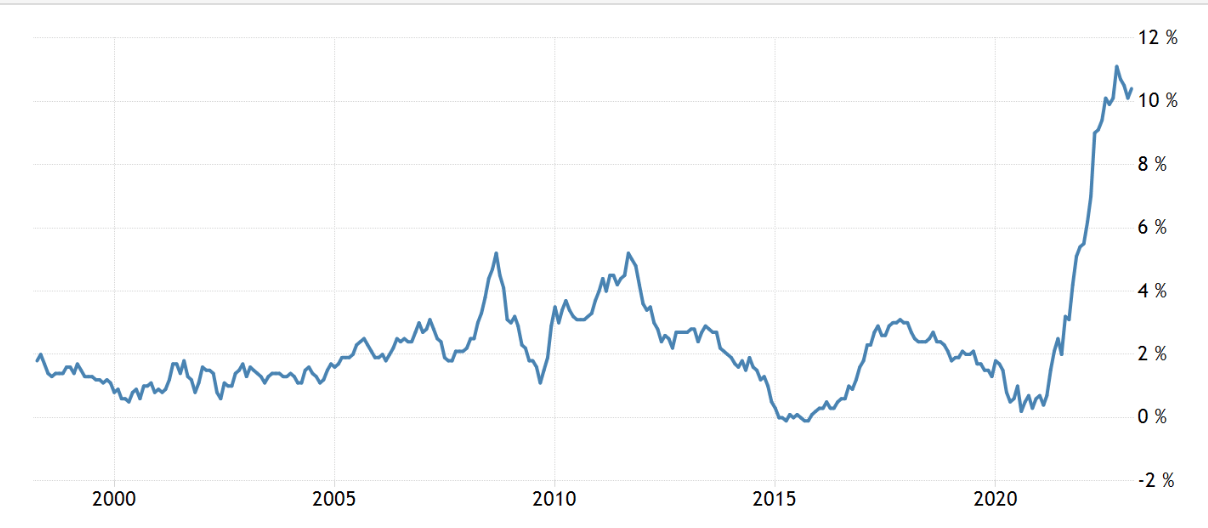

Some of this has probably spilled over to Tesco too, though the macros are challenging for it even otherwise. The company flagged cost inflation as a challenge last year. Despite a rise in sales in the first half of its last financial year (H1 22/23) ending February 25, 2023, its adjusted operating profit declined by 9.8% year-on-year (YoY) and the reported operating profit declined by a huge 43.6%. It also downgraded its adjusted operating profit expectations to the lower end of its forecast range. Fast-paced price increases still remain a challenge, with the UK's inflation coming in at 10.4% in February. It does not help that the UK economy is widely expected to be recessionary in 2023 as well.

UK's inflation over the years (Source: Trading Economics)

{kind=link}

In fact, the company noted the adjustment of consumer behaviour to the difficult economic realities during the festive season. During Christmas, customers are seen to have traded down for Tesco's own branded products from national brands. Also, the company perceived a trend towards dining in instead of eating out. The supermarket's competition with the low-cost German grocers Aldi and Lidl has also risen, because of rising prices.

Sustained market position

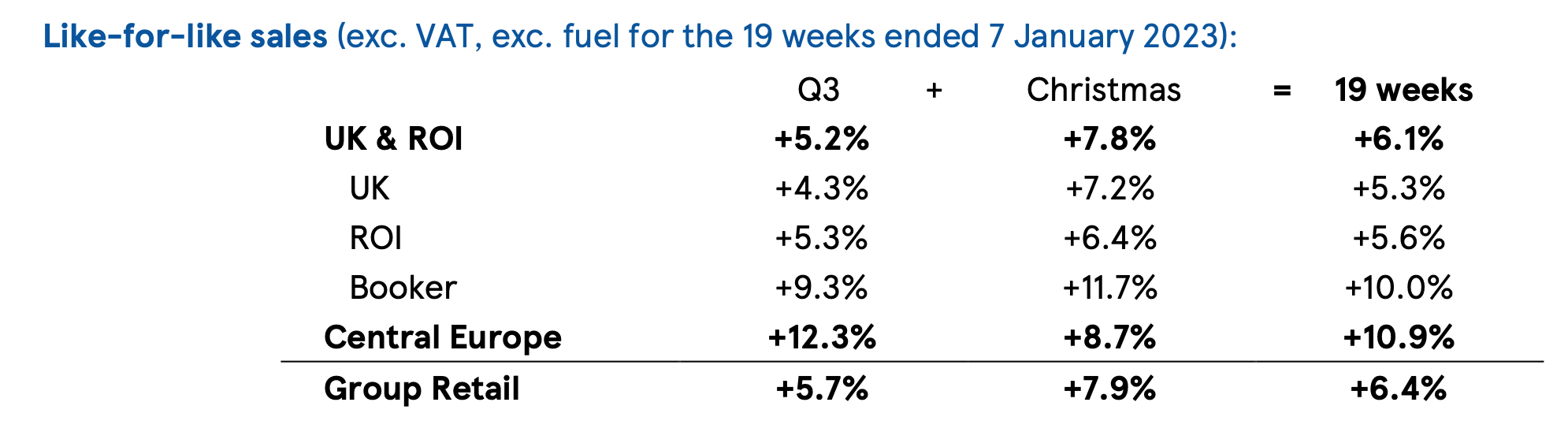

That has not affected its position though, with a 27% market share in the UK. In fact, its festive sales numbers were actually quite healthy. Its Christmas trading update for the 19 weeks after January 7, 2023, showed a 6.4% like-for-like sales increase compared to a 2.6% increase at the same time in 2022 . Notably, its UK sales, where it gets most of its business, grew by 5.3% at this time compared to a minuscule 0.2% last year. But even sales in Ireland and Central Europe were positive, as were those for Booker, its wholesale subsidiary (see table below).

{kind=link}

On its part, Tesco has undertaken a number of initiatives to incentivise customers. It has a price match scheme with Aldi, which makes its products competitive. Its loyalty scheme, which goes by the name of Tesco Clubcard is also rated the best among its peers . It has also put a price lock in place for 1000 everyday products for up to Easter.

Cost reduction

It has also undertaken cost reduction and efficiency improvement, which includes additional self-service checkouts, simplified stock and replenishment routines and store closures. This can ease some pressure off earnings, going by the fast progress it made. It put a three-year plan in place at the start of 22/23, which is expected to result in GBP 1 billion of savings. By the end of H1 22/23, it was already expecting savings of GBP 500 million in the year alone. As a result, it has moved forward the end date by one year.

What the market multiples say

How far this shows up in its profits, however, remains to be seen. The company's profit guidance did weaken despite these savings, so a further decline in earnings per share [EPS] is still possible. With a relatively elevated price-to-earnings (P/E) ratio at 21.1x, compared to 21.8x for the consumer staples sector, there is already little room for a further price increase for now. The company's P/E is also higher than its long-term average ratio . Based on this measure, at this time, it is hard to get behind the Tesco stock or its ADRs. This is even more so since weak profits can impact its dividends.

However, with the increase in sales, its price-to-sales (P/S) is competitive at 0.3x compared to 1.1x for the consumer staples sector. Its forward P/S at 0.2x also looks good, with the sector staying at 1.1x.

Weak long-term price performance

Besides sales growth and an attractive P/S, on the face of it, the company does have a big advantage as a defensive stock during a weak economy. In essence, this means that there can be a floor to how much its price is likely to fall. Except that is not the case right now.

Tesco is down by 11.3% over the past year, and even investors who bought it 5 years ago are seeing just a 9% gain. I can think of just other London-listed stocks that have given much better returns over this time among others . Even considering Tesco's substantial dividend yield of 10.7% over the past four years, investors would have been better off buying alternatives.

What next?

Much of how Tesco will perform in the foreseeable future will depend on its outlook, when it releases its full-year results on April 13. So far, its sales numbers look good and its retention of market position also goes in its favour. Its cost savings initiative has also shown good progress in the first half of the last financial year.

Its profits are however visibly impacted, which is a downer. With cost inflation staying high, it might just continue to face headwinds, though the cost-cutting can help. The outlook for the current financial year will give insight into how it expects its profits to look and also its dividends for the year. Until then I'd hold it.

For further details see:

Tesco: Waiting For FY2023 Results