TM - Tesla Q3 Earnings Results: 50% CAGR Is Hard To Sustain In The Long Run

2023-10-19 09:15:00 ET

Summary

- Tesla, Inc.'s financials show strong liquidity and profitability, but the company is overvalued compared to competitors.

- The company's outlook for production and revenue growth is optimistic, but there are concerns about the sustainability of this growth.

- Based on a discounted cash flow model, Tesla's intrinsic value is estimated to be around $182 per share, suggesting it is trading well above its fair value.

Investment Thesis

Tesla, Inc. ( TSLA ) just reported Q3 earnings , so I wanted to look at the company's historic financials and cover a little bit about the company's outlook to see if it is a good time to start a position. In short, the company is overvalued unless it can show that it can grow at breakneck speeds for the next decade. Therefore, I assign TSLA a hold rating as my price target ("PT") is not out of the question in the near future.

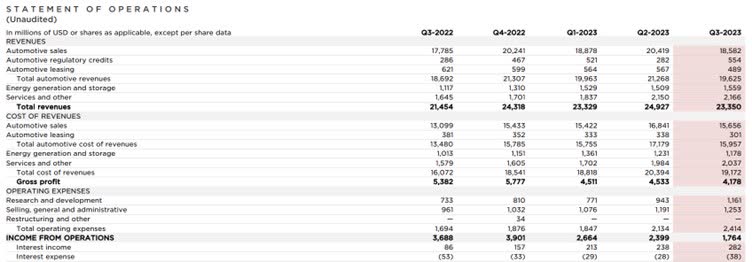

Financials

As of Q3 ’23 , the company had around $26B in liquidity (cash and marketable securities) against less than a 3 billion dollars in long-term debt. This is a great position to be in, as it allows for a lot of flexibility while not being burdened by high annual interest expenses on leverage that reduces the company’s cash flow. The management is free to focus on growth initiatives to gain more market share in the electric vehicle ("EV") space or to innovate further as it has in the past. Interest expense is immaterial, as the company’s investments are making much more in interest than it needs to pay out. It’s safe to say TSLA is at no risk of insolvency.

{kind=link}

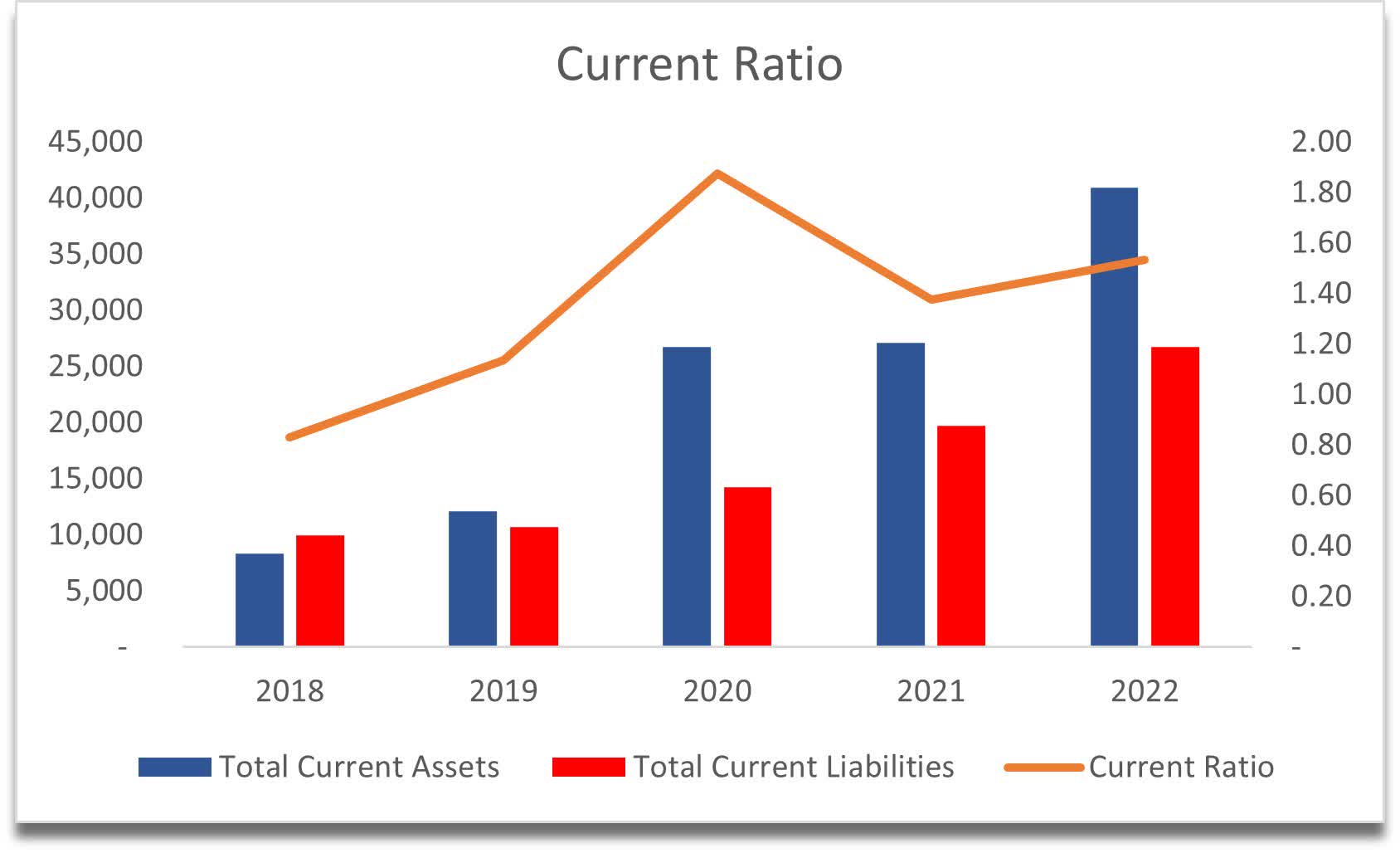

TSLA’s current ratio is decent as of FY22, and the latest quarter showed slight improvement. The company can easily pay its short-term obligations and has enough liquidity for further growth of the company, given its massive cash pile. I believe that a current ratio of well over 2 is inefficient, as it tells me that the company is underutilizing its assets and there might be missed growth opportunities. As of Q3 23, the ratio stood at around 1.7.

{kind=link}

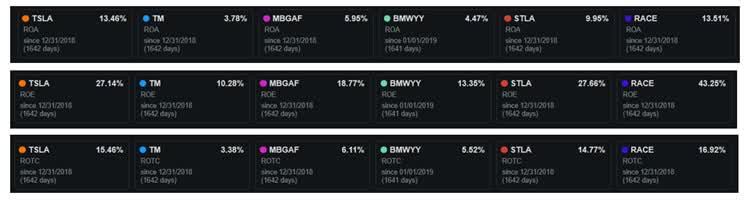

In terms of efficiency and profitability, TSLA's performance has massively improved over the last while and is on par with the top of the competition, according to Seeking Alpha. Ramping up in production of vehicles while keeping operating expenses relatively stable over the years has made the company profitable, and it can compete with the more established car companies.

{kind=link}

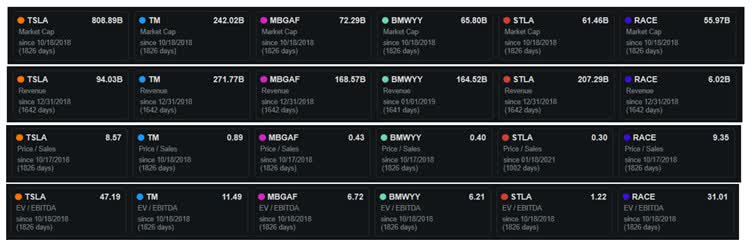

However, if we look at almost every other metric, we can see that TSLA is very expensive. Companies like the ones mentioned have much lower market caps, but much better sales figures and other ratios that make them look very cheap compared to TSLA, except for Ferrari ( RACE ), which is on another level than most of the car companies. TSLA’s market cap is over 3 times larger than Toyota Motor's ( TM ) while making 3 times less in revenue. It is even more baffling when we look at the next 3 companies Mercedes-Benz ( MBGAF ), BMW ( BMWYY ), and Stellantis ( STLA ).

{kind=link}

Granted, none of these companies is expected to grow going forward very much, unlike TSLA. However, it seems that the market is expecting miracles out of Tesla and is pricing it at such valuations because it is projected to grow at a ridiculous pace.

Revenue assumptions from left to right: TSLA, TM, MBGAF, BMWYY, STLA, and RACE (Seeking Alpha)

In terms of margins, these improved quite considerably in FY22, however, ever since the company started to slash vehicle prices, these have come down significantly once again. To be honest, I don’t mind that cars are becoming cheaper, which will lead to competition lowering their prices too, and consumers in the end will win.

{kind=link}

The company can afford to cut prices, as it will come closer to the competition in terms of margins while driving higher sales numbers in the long run.

{kind=link}

Comments on the Outlook

For a company that’s not just a car company, there sure is a lot of revenue coming from the automotive segment.

{kind=link}

I will say there is potential for the other segments to perform well, seeing how quickly they are growing; however, the company’s been building giga and mega factories to support the company’s main revenue generator, which is the Tesla vehicle production.

The company’s outlook for production is sitting at a whopping 50% CAGR as per the management. So far, the company’s revenues matched the multi-year horizon, however, that did not include the company slashing its average sale price of the vehicles, so production of 50% CAGR may not equate to 50% CAGR in sales in the end, so I don't think it is fair to use that growth for revenue figures in the future also, especially now that there have been some slowdowns recently, as you can see from the above financial summary.

With the future gigafactory built in Mexico, the company will add another 2m vehicles per year of capacity. So, it seems the demand for Tesla vehicles is high, and this 6 th gigafactory is slated to start production in Q1 ’25, which is not that far anymore.

The upcoming Cybertruck has around 2m orders outstanding before it is even released. However, that doesn't mean that these orders are going to translate to actual 2m sales, especially since the Cybertruck production capacity is put at around 125,000. On top of that, the orders are reserved for $100, so if it takes too long to get the truck, there will be cancellations. I believe the truck is going to be somewhat of a niche with that design and will not be the most popular vehicle, and the capacity numbers tell me exactly that.

Future contracts with companies like Hertz Global (HTZ) to acquire fleets of TSLA vehicles should bolster the company's revenue. However, more work is needed in that area because 100k vehicles was around $4.2B at that time. I could see these types of contracts getting more popular due to the rising popularity of EVs.

What could work well in the future and what could drive these contracts to become bigger, is the company's efforts to develop a full self-drive ("FSD") vehicle. The company has been working hard in this area of research, and with the booming popularity of AI, I could see many companies like Hertz and taxi-hailing companies like Uber (UBER) hopping on the hype train if it means that the vehicles can safely drive themselves and the companies wouldn't have to pay drivers anymore. Cathie Wood of Ark Invest has a more than ambitious target for robotaxis to deliver $8-$10 trillion by FY30 in revenue, which is a little absurd in my opinion, but the sales will certainly not be hurt by this innovation eventually. However, it first needs to pass a bunch of regulations and prove that it is safe or safer than human driving.

With all that’s out there for Tesla, is it possible that the company will achieve 50%+ CAGR in the long run? It is possible; however, no one can predict the future, and the best we can do is look at a few scenarios to see what the company’s potential in the next decade is.

Valuation

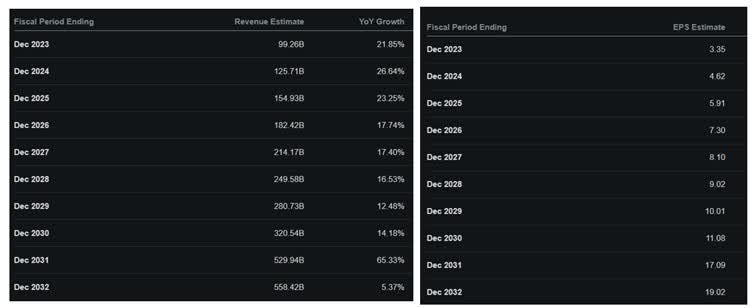

In terms of revenues, the company has had a massive explosion in growth over the decade. At the cut-off of 10 years, the company managed to do 51% CAGR, which is very impressive not just for a car company but for any company. Even a small-cap company would envy TSLA here, and this is on target with what the company wanted to achieve in terms of CAGR vehicle production. The question is, how sustainable is this growth? I am having a hard time believing the company could have another 50% CAGR for the next decade even with the mentioned developments. So, I will go with slightly more realistic, yet still on the optimistic side, projections. Furthermore, 50% CAGR of vehicle production does not equate to 50% CAGR in sales because of the lower average sale price, and if we couple that with the decrease in demand, I could see the sales numbers come below the 50% CAGR in the long run for sure.

Below are my revenue calculations for the three scenarios: base, optimistic, and conservative.

{kind=link}

In terms of EPS and Margins, I also made quite optimistic assumptions, just to go with the rhetoric that the company is going to be very profitable. It seems a little unrealistic (to put it lightly) that the company is going to achieve half a trillion dollars in sales in the next 10 years, but anything can happen.

{kind=link}

As you can see, the numbers are quite a bit more optimistic than the analysts below. However, the outcome is going to be the same in the end, as you will see.

Analysts' Rev Growth and EPS assumptions of TSLA (Seeking Alpha)

{kind=link}

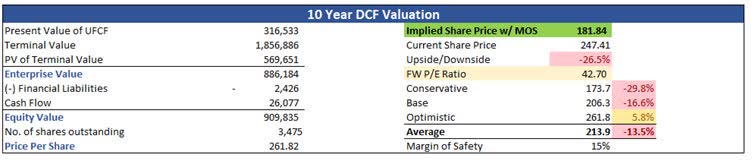

For the discounted cash flow ("DCF") model, I went with a 12% discount rate. I usually go with the company’s weighted average cost of capital, or the WACC, as the discount rate. However, TSLA’s beta is as of right now 2.25, which historically seems to be elevated, so I lowered it to around 1.6, as I don’t think in the long run the company’s beta is going to be so elevated. For the terminal growth rate, I went with 3%, just a little higher than what the U.S. inflation was historically.

On top of these estimates and inputs, I decided to add another 15% margin of safety for that extra cushion. With that said, TSLA’s intrinsic value is around $182 a share, implying that the company is trading well over its fair value.

{kind=link}

Closing Comments

The future for the company sure looks promising. The EV revolution is well on its way and TSLA is likely to be the biggest beneficiary due to how much of a head start it has over its competition in terms of expertise in what makes an EV car great.

I don’t think it is a good time to invest in Tesla, Inc. stock at these prices, as the risk/reward is not very enticing, given how volatile the share price has been over the last while. Just about 5 months ago the company was trading around my PT, so I don’t think it is out of the realm of possibility that we will see this price once again or even lower if the company misses a couple of reports. The stock is very actively traded and technical analysis plays a huge role in the share price fluctuations, so be cautious when starting a position as it might be that the price broke some floor level and is bound to plummet to the next support level which may be 10%-20% lower.

At this price, Tesla, Inc. stock is more of a gamble than anything else, and if it comes down to around $200 a share, that is when I will start to look at it more seriously.

For further details see:

Tesla Q3 Earnings Results: 50% CAGR Is Hard To Sustain In The Long Run