FFND - Tesla: Woke Mob Fury - 20 Top Growth Stocks Ranked

Summary

- As the woke mob’s fury grows, Tesla shares are down 70%, despite the fact that revenues and profits keep growing rapidly.

- We rank Tesla (based on fundamental metrics) versus 20 top growth stocks sourced from the top 10 holdings of two popular active growth ETFs (Future Fund (FFND), ARK Innovation (ARKK)).

- Both funds have large positions in Tesla.

- We dive deeper into Tesla, including its tangled business history with the woke mob, future growth potential, profitability, valuation and big risks.

- We conclude with some critical takeaways and our strong opinion about investing in Tesla and growth stocks in general.

Tesla ( TSLA ) shares are down more than 70%, and it’s going to get worse. For starters, the “woke mob” is ticked at CEO Elon Musk. Next, growth stocks in general are getting hammered as interest rates rise and there is no “fed put” in sight. In this report, we rank Tesla (based on fundamental metrics) versus 20 top growth stocks sourced from the top 10 holdings of two popular active growth ETFs, Future Fund ( FFND ) and ARK Innovation ( ARKK ), both have very large positions in Tesla. After digging deeper into the details on Tesla (including its tangled business history with the woke mob, future growth potential, profitability, valuation and risks), we conclude with our strong opinion about investing in Tesla and growth stocks in general.

Tesla Overview:

Tesla

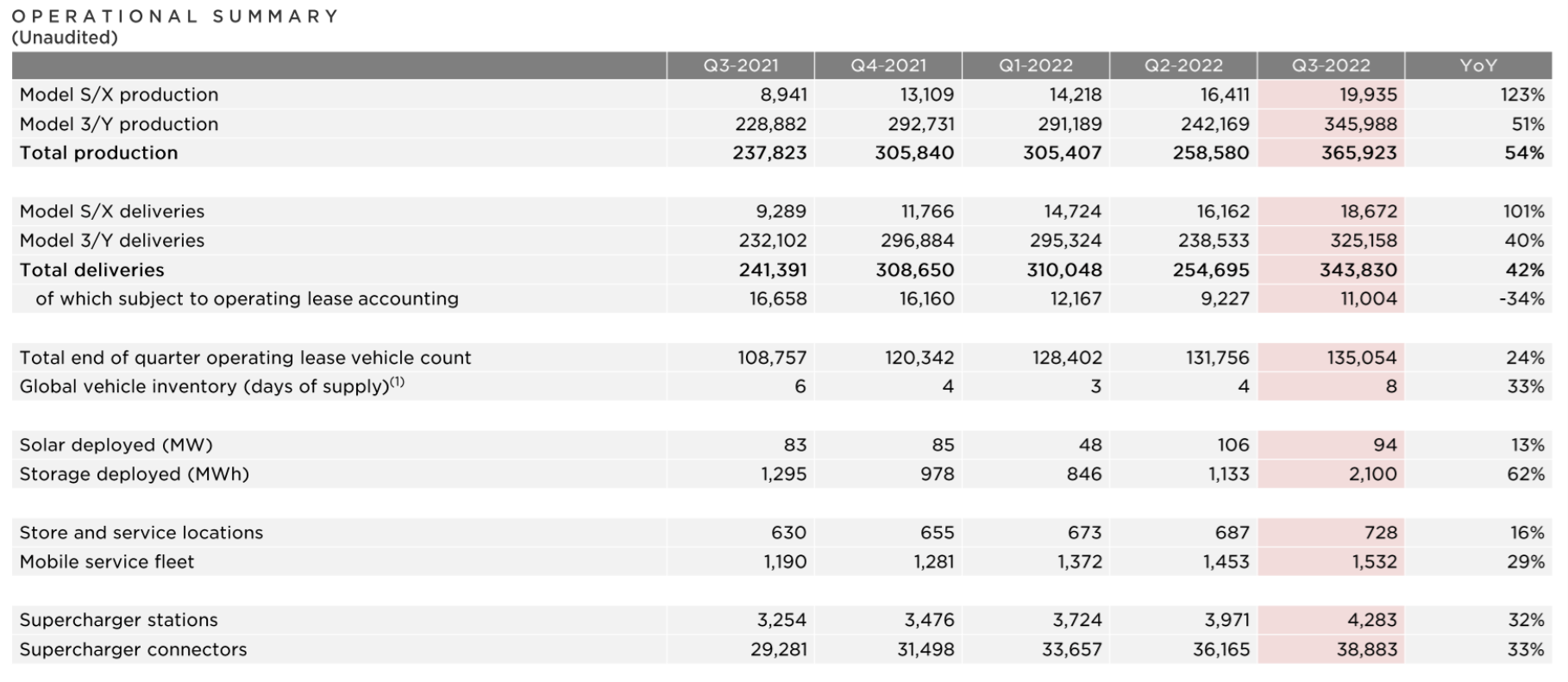

As you know, Tesla designs, develops, manufactures, leases, and sells electric vehicles, and energy generation and storage systems (in the United States, China, and internationally). For reporting purposes, the company is divided into two operating segments (Automotive, and Energy Generation and Storage), but there is a lot more going on. For starters, here is a high level look at Tesla’s recent operations, in terms of vehicle production and deliveries, as well as solar and storage deployment and supercharger stations.

Tesla Q3 Investor Presentation

{kind=link}

Electric Vehicles: The Un-Holy Grail

Tesla’s electric vehicles (“EVs”) and other solutions have captured mounds of positive (and some negative) attention over the years, in large part because it seems to provide a compelling alternative to the dangers of fossil fuel consumption (pollution) and climate change. And while these are noble aspirations, the reality is :

Electricity grids in most of the world are still powered by fossil fuels such as coal or oil, and EVs depend on that energy to get charged. Separately, EV battery production remains an energy-intensive process.

Basically, EV’s are still largely powered by the fossil fuels that many are trying to avoid. Further, electric vehicle batteries are extraordinarily harmful to the environment when their lives are over (plus the mining that goes into obtaining the rare elements for batteries is particularly unfriendly to the environment too). For example :

Not only do these batteries require large amounts of raw materials, including lithium, nickel and cobalt – mining for which has climate, environmental and human rights impacts – they also threaten to leave a mountain of electronic waste as they reach the end of their lives.

Further still, and despite the fact that Tesla has built out an impressive charging network (you can see the numbers in the table above), it’s still a lot easier and faster to simply fill up with gas than it can be to charge an electric vehicle. We’ll have a lot more to say about Tesla vehicles and other Tesla solutions in the section of this report on growth potential.

Tesla’s History: In Bed with the Woke Mob

Tesla was incorporated in 2003, and Elon Must became the largest shareholder in 2004 through a $6.5 million investment (Musk had $100 million from his recent sale of PayPal ( PYPL )—a company he cofounded). However, It wasn’t until 2021 when the company finally become profitable , for the first time, without the help of emissions credits. If you don’t know, emission credits are basically financial incentives created by government entities to help reduce pollution. And these types of government incentives were a huge factor in allowing Tesla to remain in existence over the years. For example, Tesla was only about a month away from going bankrupt during the Model 3 ramp from mid-2017 to mid-2019.

Clearly emission credits and government incentives helped Tesla become the large organization it is today (we’ll have more to say about Tesla’s current financial position later in this report), and those credits and incentives would not have existed were it not for the social and political pressures of the environmentally-focused woke mob.

Why Growth Stocks Are Getting Crushed:

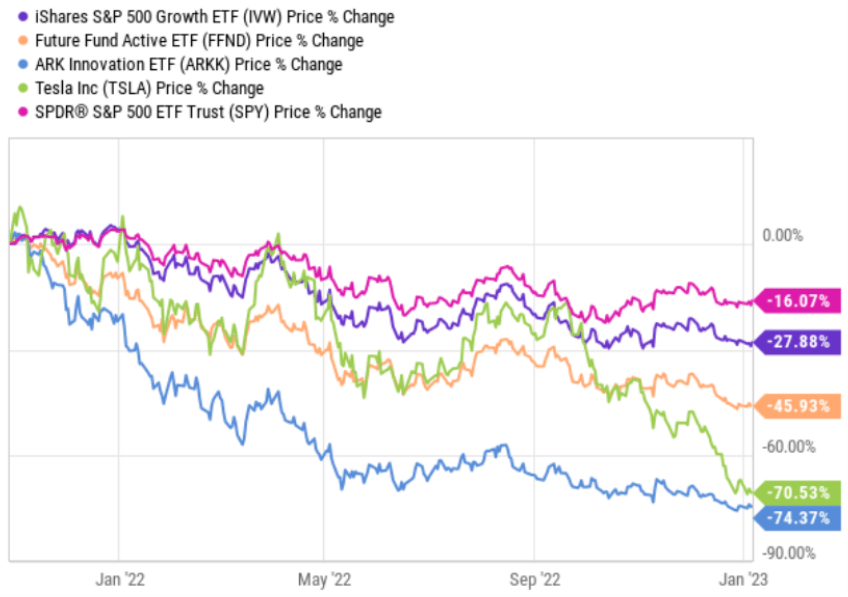

Here is a look at the recent performance of growth stocks (including the S&P 500 Growth Index ( IVW ), the Future Fund and the ARK innovation ETF) versus the S&P 500 ( SPY ). It’s not been pretty for growth stocks, and it’s going to get worse (as we explain below).

{kind=link}

In simple terms, growth stocks are getting hammered because the pandemic bubble is bursting. Specifically, the extraordinarily easy monetary and fiscal policies that were implemented after the onset of the pandemic led growth stocks to soar (because central banks held borrowing costs / interest rates artificially low (near 0%) and governments were throwing free money everywhere). And now that free money is gone, we’re left with the giant sucking sound of high inflation as central banks rapidly raise rates to fight the inflation they helped create.

Making matters worse, there is no “fed put” this time around (i.e. the fed isn’t going to bail out the stock market, as they have done in the past). The fed’s dual mandate is full employment and low inflation, and because unemployment is low but inflation is high, they’re going to keep raising rates (to fight inflation) which is driving the economy closer to an ugly recession. Basically, if you are a stock market investor (particularly a growth stock investor) the fed will likely keep tightening the screws on you until high inflation is gone.

20 Top Growth Stocks, Ranked:

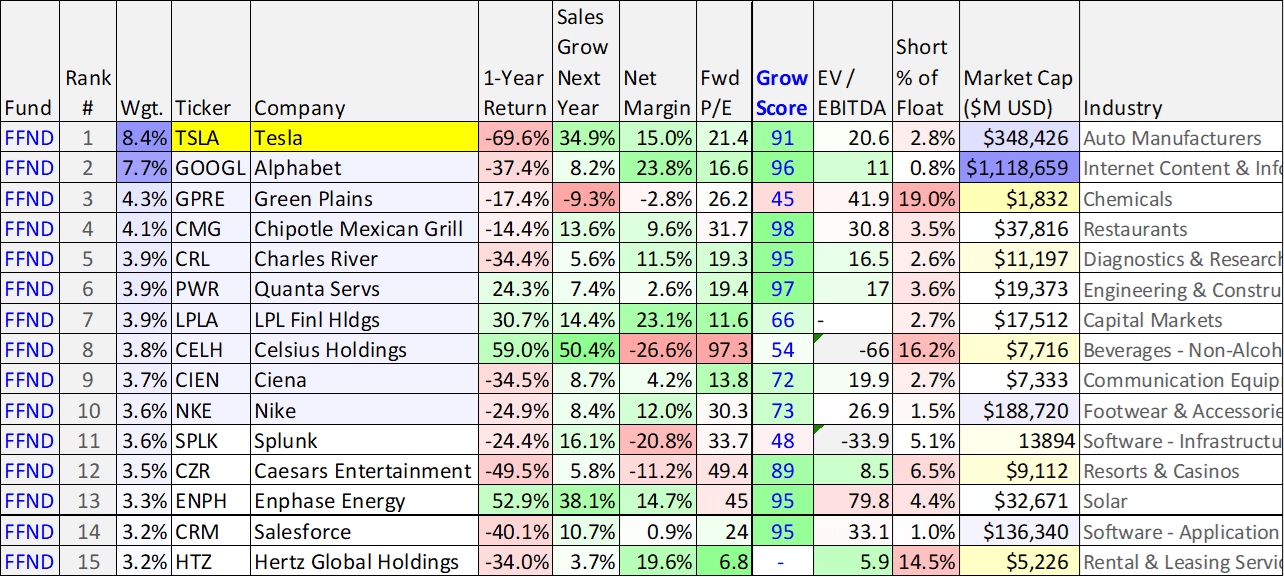

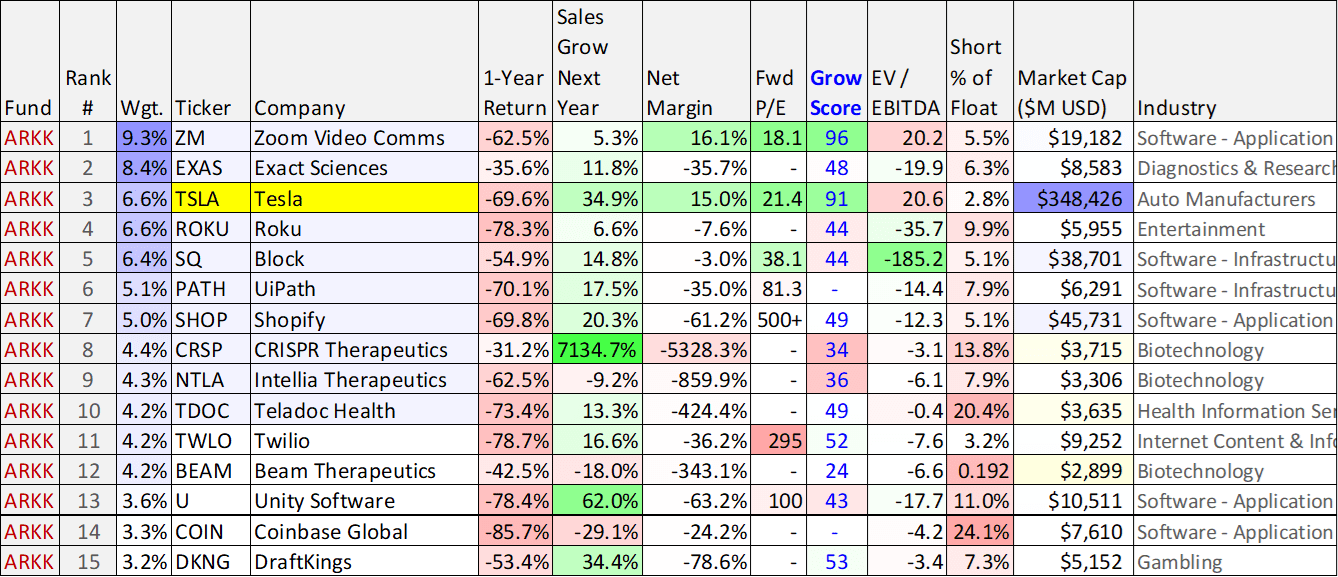

The following tables include the top 10 holdings of two popular growth funds (i.e. Future Fund and ARK Innovation), as well as a variety of additional data points that are important considering the current macroeconomic environment (i.e. recession looming and a hawkish fed). Both funds have large positions in Tesla, as you can see below.

StockRover, Future Fund website

{kind=link}

( GOOGL ) ( PWR ) ( CELH ) ( SPLK ) ( ENPH ) ( CRM ) ( ZM ) ( EXAS ) ( ROKU ) ( SQ ) ( PATH ) ( SHOP ) ( CRSP ) ( NTLA ) ( TDOC ) ( TWLO ) ( U ) ( COIN ) ( DKNG ) ( BEAM )

{kind=link}

The “Growth Score” (blue font) takes into consideration the 5 year history (as well as forward estimates) for EBITDA, Sales, and EPS growth (the best companies score a 100 (green) and the worst score a 0 (red)). If you’d like an expanded list, please reference our new report: Amazon: 100 Top Growth Stocks, Ranked .

Both funds (FFND and ARKK) invest in companies with very high future growth estimates (as you can see in the table above). However, from a fundamentals standpoint, you’ll also notice FFND invests in a lot more companies with positive net income margins, whereas ARKK does not. This has been an absolutely critical metric over the last year as the fed has increased rates. Specifically, companies that are not yet profitable (because they were banking on future profits) have suffered the worst losses (especially considering many of them may never achieve profits now that the fed has raised rates so much. In case you don’t know, when it comes to stock market investing—interest rates matter—a lot!

Also worth mentioning, FFND seems to pay a lot more attention to fundamentals, whereas ARKK appears largely focused on long-term growth ideas and concepts—fundamentals be darned!

Tesla’s Future Growth Potential:

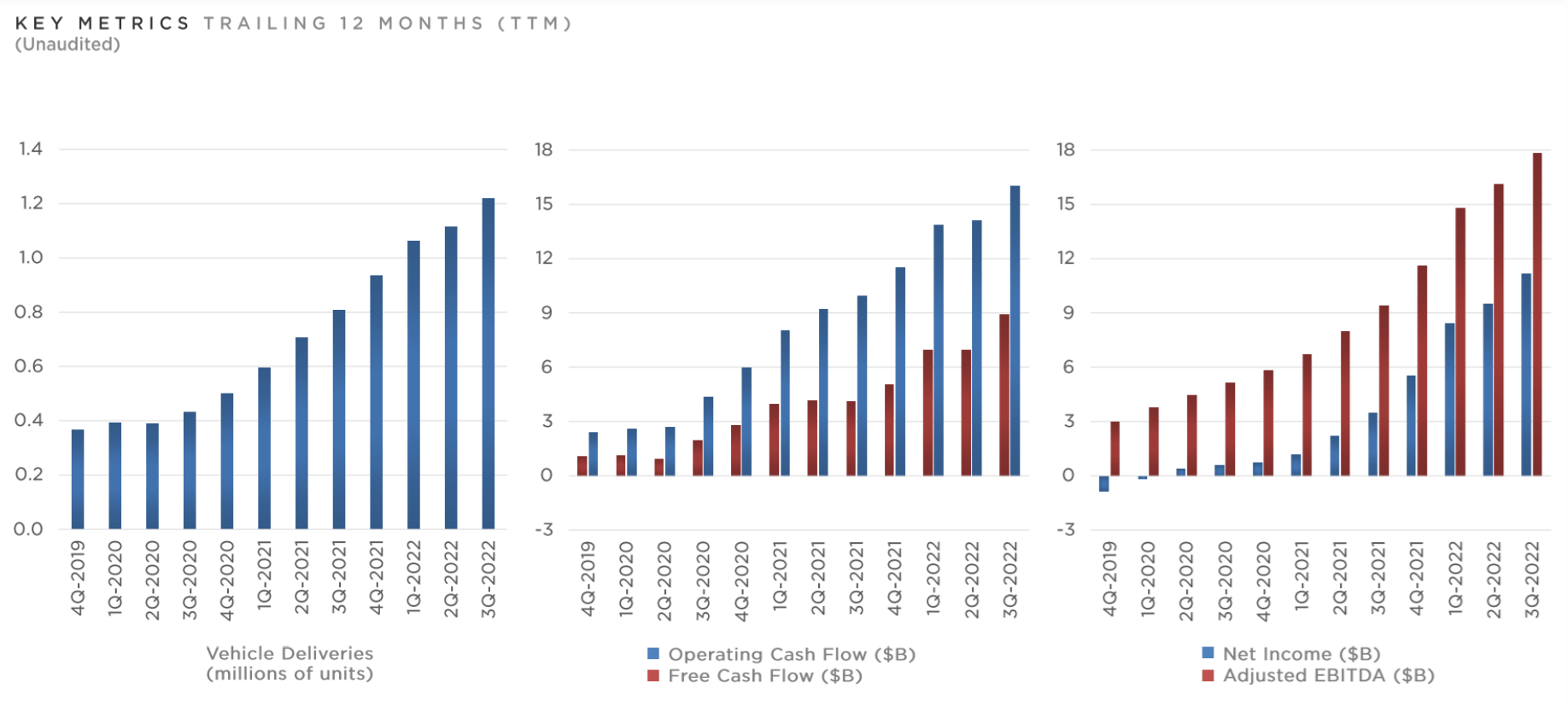

With regards to Tesla, cash flows and profitability are both growing rapidly, a very good thing considering the current challenging capital market environment (e.g. rising interest rates).

Tesla Q3 Investor Presentation

{kind=link}

From a business standpoint, Tesla’s vehicle deliveries continue to grow rapidly (despite the recent delivery miss , which caused the shares to sell off further); deliveries are at an all-time high.

The growing number of deliveries is so important because as production and deliveries keep ramping, so will Tesla’s economies of scale and profit. Further, Tesla could expand its total addressable market (“TAM”) by ten-fold by cutting the cost of an electric vehicle in half, according to this recent note from Sam Korus at ARK Investments.

Last week, during its third-quarter earnings call , Elon Musk noted that Tesla is developing a vehicle that will sell at roughly half the price of the Model 3 and Model Y. While vehicles at price-points above $60,000 address ~5% of the total US car market, the addressable market expands to 50% at ~$30,000, as shown below.

ARK Invest

Further still, Tesla has plans to launch a light truck, a semi truck and a more affordable sedan and SUV platforms. These will all contribute to economies of scale ad reduced manufacturing costs per unit. Further, Tesla’s efforts into autonomous driving software can add subscription revenue and keep the brand awareness and image high. Not to mention, Tesla’s robotaxi business add to the upside. Also notable, Tesla’s Dojo supercomputer could incrementally add value at some point in the future.

Tesla’s Energy Generation and Storage segment also continues to grow. And although not yet contributing meaningfully to profits, it continues to scale and can eventually earn margins similar to Enphase ( ENPH ) (a long-time Blue Harbinger Disciplined Growth Portfolio holding).

Profitability:

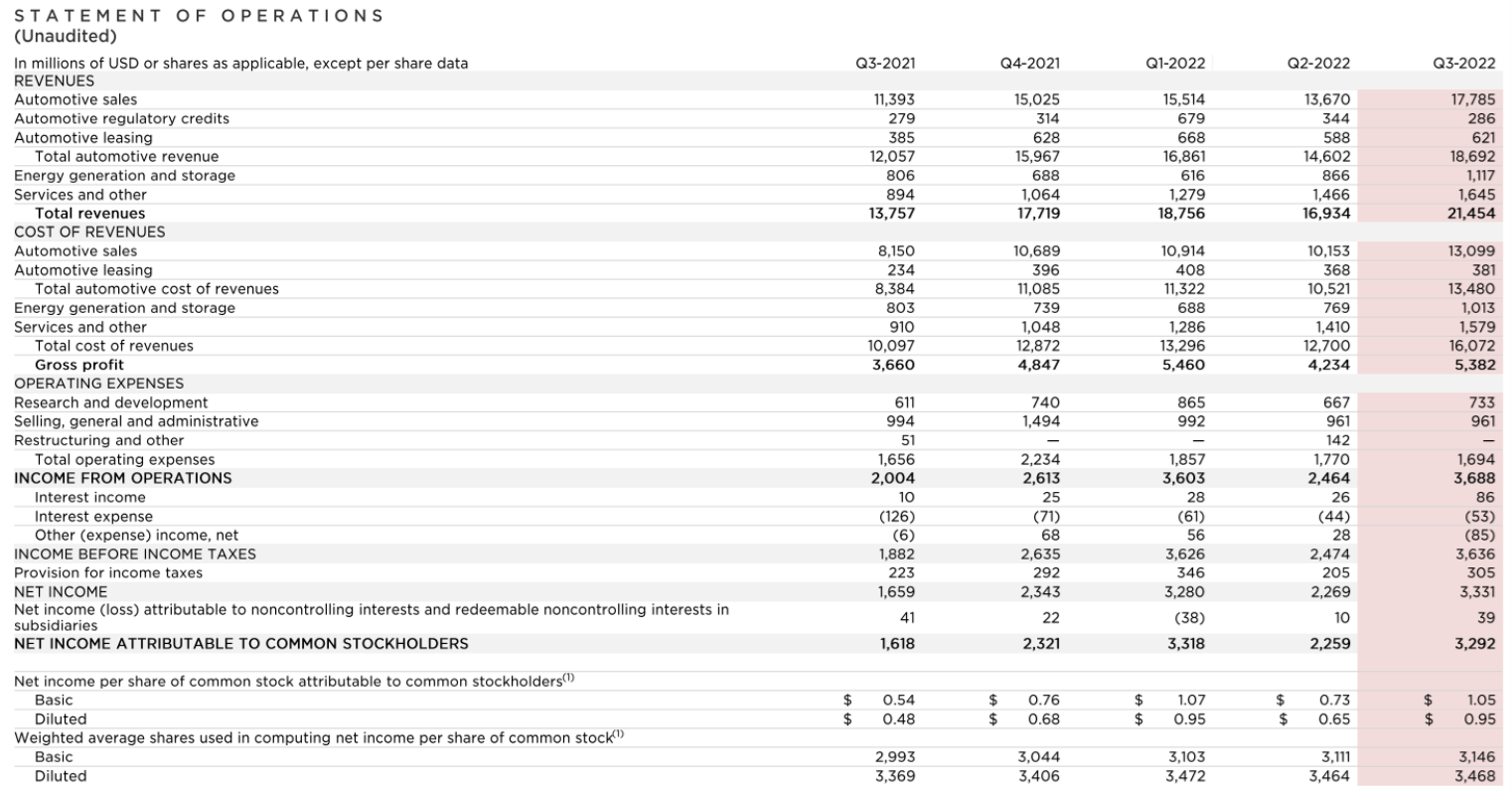

As Tesla continues to ramp, so too will its profitability (margins). It helps tremendously that the company is already profitable—something many other high-growth companies cannot say (see our earlier top growth stock tables), considering rising interest rates make for a more challenging capital markets environment. Here is a look at the company’s most recent quarterly income statement (as you can see costs are not rising as rapidly as revenues, thereby improving margins and profitability).

Tesla Q3 Investor Presentation

{kind=link}

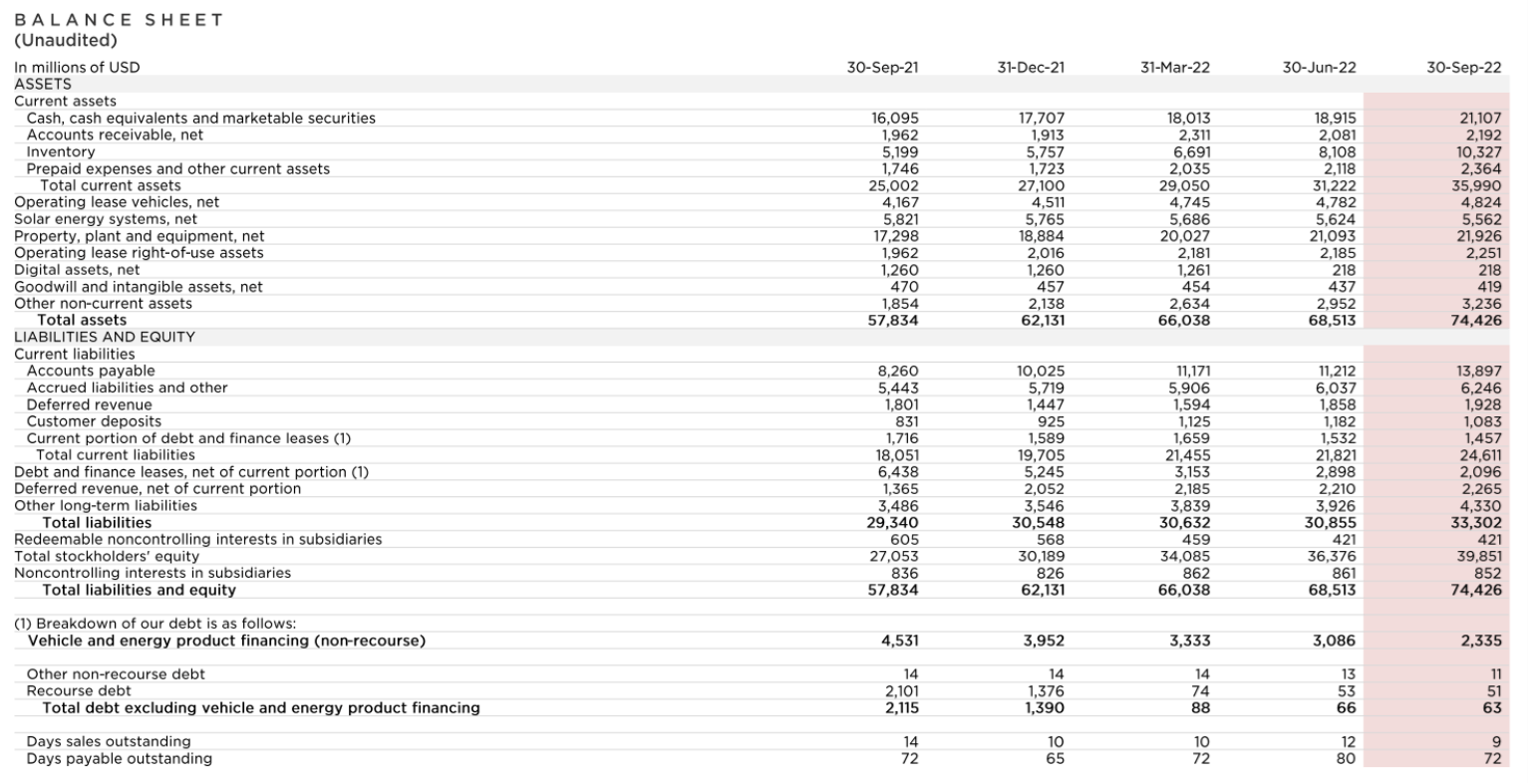

Also very important, Tesla has a healthy balance sheet (see below). In particular, the company has more current assets than total liabilities (a good thing with rates rising and considering a significant portion of debt comes due in the next few years.

Tesla Q3 Investor Presentation

{kind=link}

Tesla does not pay a dividend and has not been repurchasing shares, both good things considering the growth potential is attractive. Specifically, with a return on invested capital above the cost of capital, Tesla has wisely been reinvesting in itself.

Valuation:

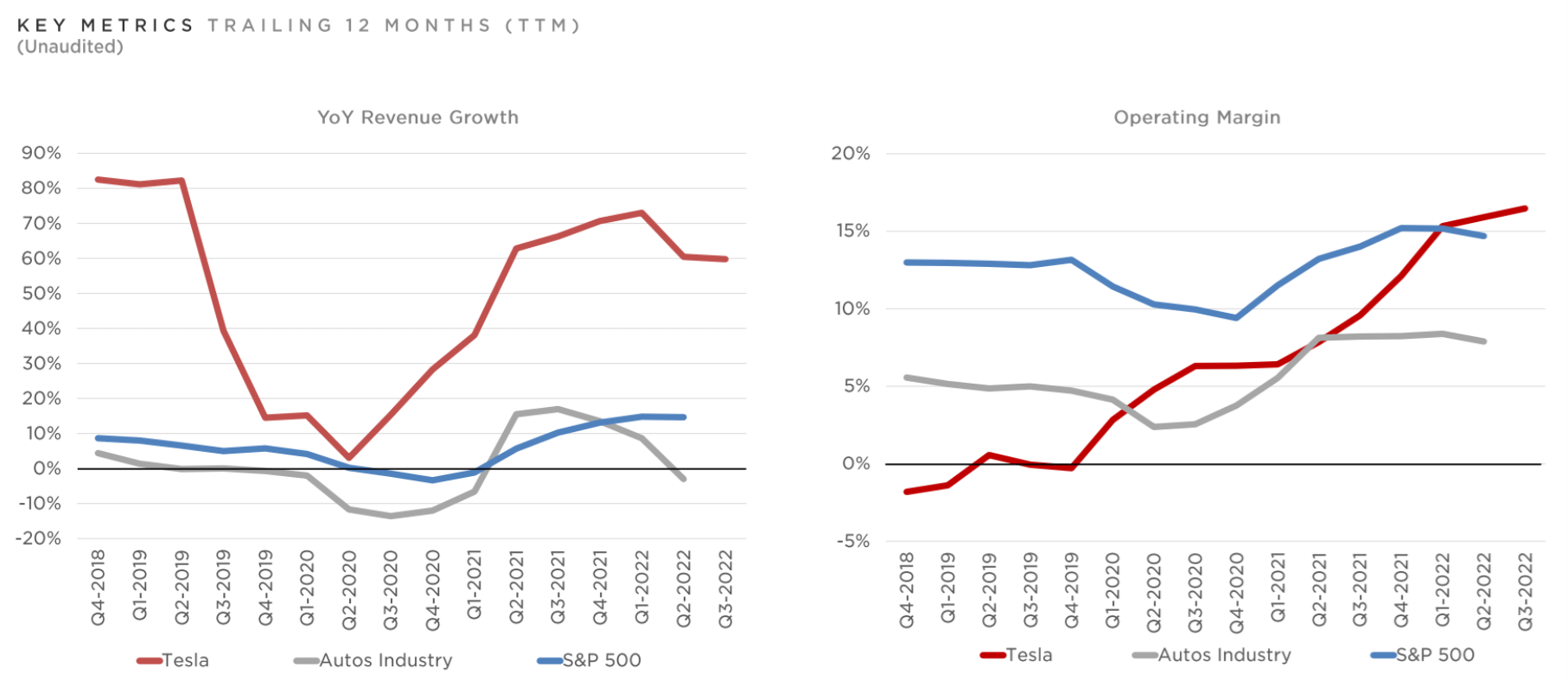

Unlike other growth businesses that have sold off hard over the last year (as the fed has become increasingly hawkish), Tesla is actually profitable and margins are improving. This is a very good thing, but it’s also critically important to acknowledge Tesla’s high uncertainly and volatility (as compared to the auto industry and the overall S&P 500, as you can get some feel for in the graphics below).

Tesla Q3 Investor Presentation

{kind=link}

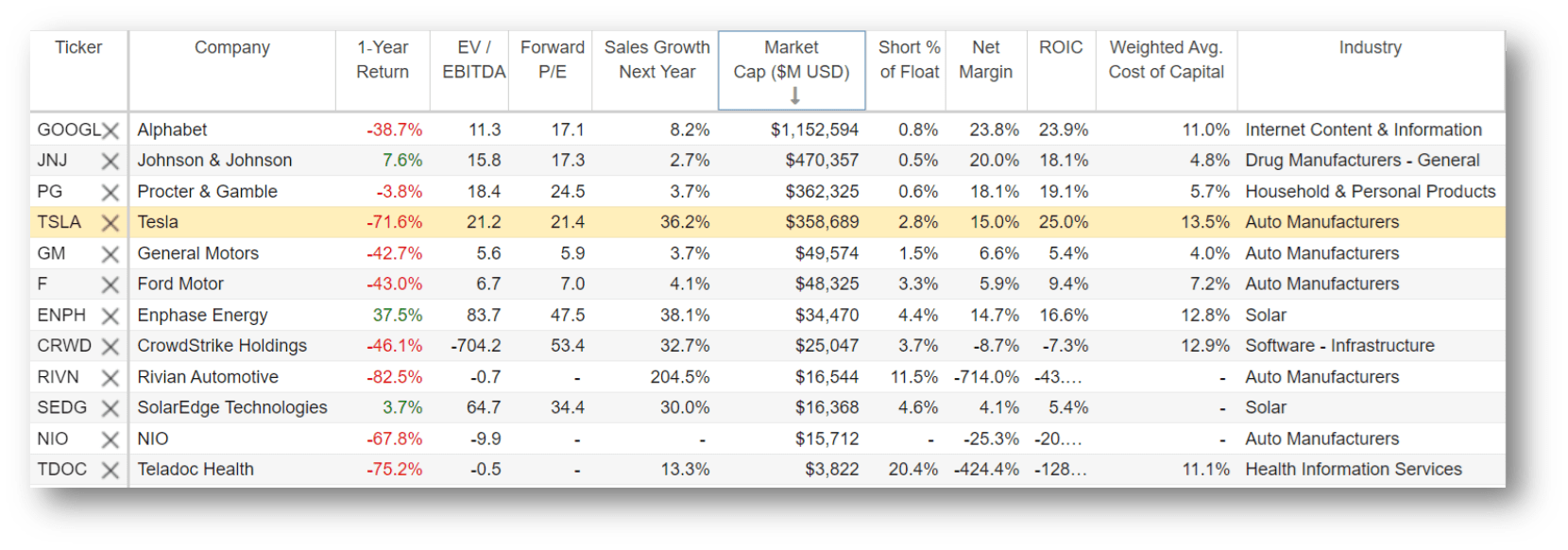

Assigning an exact valuation to Tesla given the high volatility, growth and uncertainty (Tesla is not a boring predictable company like Procter & Gamble ( PG ) and Johnson & Johnson ( JNJ )) is a challenging endeavor with resulting numbers varying widely based on cost of capital, return on capital invested and growth rate assumptions. That said, it can be worthwhile to compare Tesla’s margins, growth rate, profitability and valuation metrics to other large companies, as shown in the table below.

{kind=link}

A few notable things in the table above, Tesla is actually profitable (that’s more than a lot of other high-growth stocks can say) and even though its forward P/E ratio is way above other automakers, so is its expected growth rate much higher. Further, Tesla’s cost of capital is well below its return on invested capital, and its net margins are already very impressive (much better than GM and Ford) and expected to keep improving as economies of scale grow for Tesla.

For a little more perspective, the 33 Wall Street analysts covering the shares have an aggregate “Buy” rating, and many of them have price targets significantly higher than the current share price (which is down over 70% in the last year).

Seeking Alpha

In our view, if Tesla continues on its current growth trajectory (a very big “if”) the shares can easily trade dramatically higher, as earnings are set to grow dramatically. And even if the growth rate comes in lower than expected (but still remains relatively high) the shares are still undervalued. From a high level, the market seems overly pessimistic on Tesla relative to its long-term earnings power and value (perhaps a near-term phenomenon related to the woke mob’s increasing contempt for CEO, Elon Musk).

Risk Factors:

Woke Mob Fury : In case you haven’t noticed, Tesla is a volatile stock that gets a lot of media attention, particularly from the environmentally-focused woke mob. As alluded to earlier, the woke mob created significant political pressure that led to the emissions credits and other government-sponsored incentives that have helped Tesla become the large company it is today. However, the woke mob’s opinion of Tesla is changing rapidly.

For starters, Tesla CEO Elon Musk’s recent purchase of Twitter (a major source for information distribution) has upset many from a political standpoint because they preferred the views of prior Twitter leadership. This has created significant negative media attention for Musk and for Tesla. For example, according to this NBC News article :

“Elon Musk’s uneasy relationship with the left explodes over Twitter takeover… Musk has helped expand America's use of electric vehicles. The left has found a lot of other things to dislike about him.”

Further, Musk's recent sanctioning of the Twitter Files has increased the heat on him and his companies.

Related, Tesla continues to receive low ESG (Environmental, Social and corporate Governance) ratings, while large oil and gas companies are increasingly receiving better ratings. For example, see: How Does Tesla Get A Worse ESG Score Than 2 Oil Companies?

Twitter

However, given the momentum of EV adoption, we expect negative sentiment to create more short-term pressure than long-term pressure. Further still, as constituents work to increase the use of alternative energy sources in the grid, this will decrease the fossil fuel footprint of electric vehicles (although fossil fuels will likely remain the major energy source for decades to come).

Key-Man Risk : CEO Elon Musk splits his time between Tesla , Twitter, SpaceX and The Boring Company . This creates significant demands on his time and could detract from performance (although Musk is reported to be searching for a new Twitter CEO). Further still, Musk owns a significant percentage of Tesla’s shares, which he has recently reduced to fund his Twitter acquisition. Musk sales can negatively impact the share price.

Competition : Traditional automakers are shifting heavily towards EV production which creates increased competition for Tesla. This could cause Tesla’s growth rate to slow. Some pundits argue that Tesla’s valuation multiple should be more in-line with traditional automakers, despite Tesla’s higher growth rate, higher margins and more expansive innovation.

Battery Prices : According to some, battery and solar panel prices will decline faster than Tesla can reduce costs, resulting in little to no profit in this areas.

EV Adoption : The magnitude of EV adoption may not be as great as expected. Some drivers may simply prefer to stick with their gas powered vehicles.

Regulatory Risks : Tesla has historically relied heavily on subsidies and incentives. This may make future growth more challenging. Further, some states are requiring car makes and dealers to be separate, which could create legal challenges for Tesla.

Macro Headwinds : Macroeconomic headwinds, as described earlier, are a significant risk factor for Tesla. Interest rates are higher, economic growth is slowing and the economy is expected to enter an ugly recession. This could dramatically slow growth, although stock prices generally recover faster than the economy.

Key Takeaways and Conclusions:

Tesla is profitable, growing rapidly and significantly undervalued. However, that doesn’t mean the shares won’t keep falling (the woke mob is angry, and this is bad for public perception). Further, the indiscriminate growth stock selloff continues, especially with recession looming and no “fed put” in sight (if you're still not sure what we’re talking about, see our 2023 Outlook: 10 Stocks Worth Considering for more information and ideas).

However, Tesla has the fundamental growth characteristics that Future Fund likes (it’s ranked #1 in that fund). It also ranks above the 90th percentile (a good thing) in our fundamental growth score table above. Further still, Tesla apparently has the long-term rainmaker characteristics that ARK Innovation ETF likes (it’s ranked #3 in that fund).

If you are a low-risk, income-focused investor, stay the heck away from Tesla! (you might instead prefer our report: Top 10 Big Yields: CEFs, REITs, BDCs And MLPs ). But if you are a disciplined long-term growth investor, Tesla is increasingly attractive and worth considering for a spot in your prudently-diversified long-term portfolio. Although volatile, Tesla's long-term upside is very real.

For further details see:

Tesla: Woke Mob Fury - 20 Top Growth Stocks Ranked