TTI - TETRA Technologies: Waiting For A Better Price

2023-07-05 07:36:56 ET

Summary

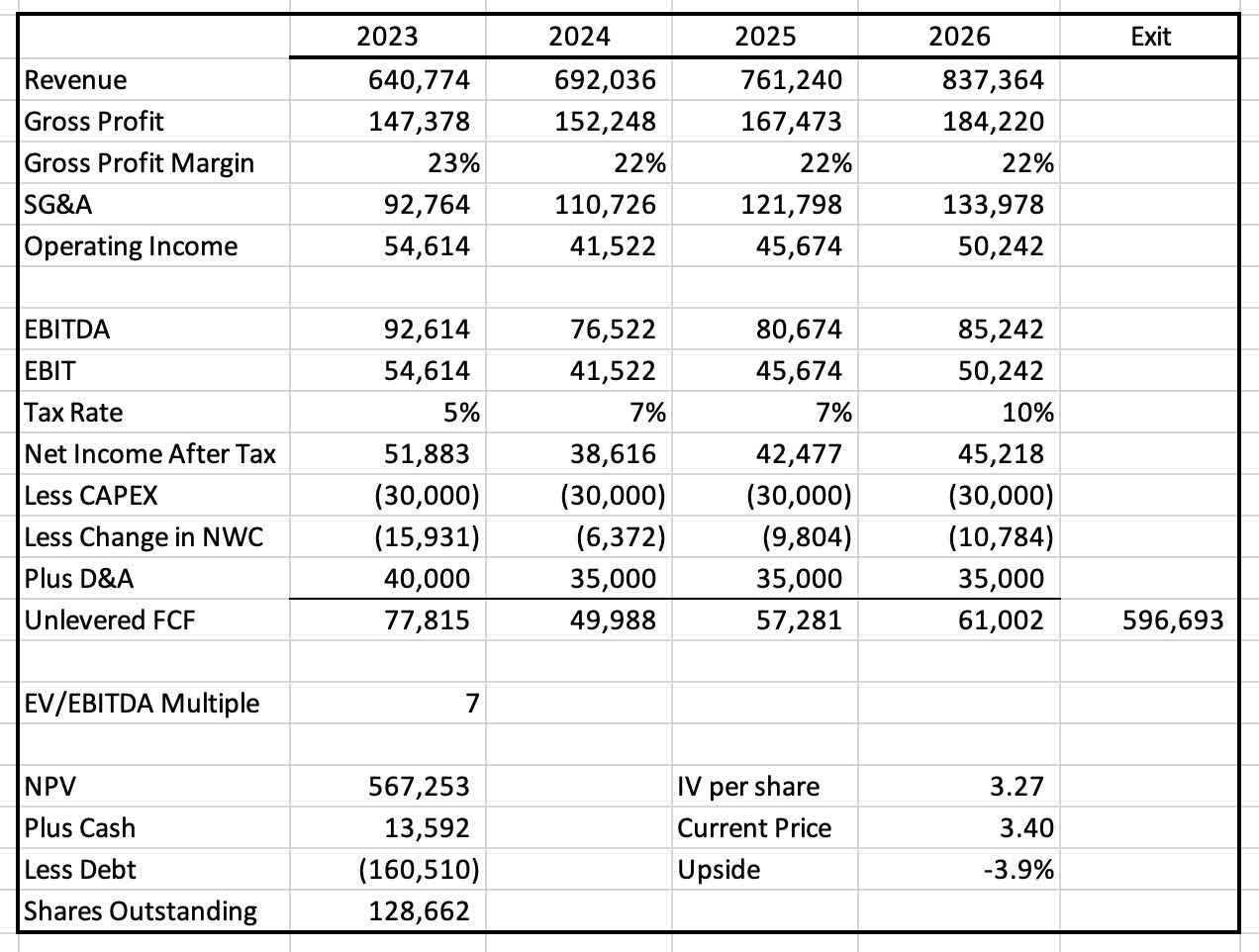

- I estimate TTI's FY2023 revenue to be $640 million and arrive at a fair value price estimate of $3.27.

- In consideration of TETRA Technologies' Bromine-Lithium assets, the current $160 million of long-term debt overhang will be creating funding challenges to future projects.

- I rate the stock a Hold and suggest readers continue following the company's near-term developments.

Editor's note: Seeking Alpha is proud to welcome Nicholas Sherr as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Summary and Thesis

TETRA Technologies ( TTI ) is a small-cap oilfield services provider and producer of salt-based industrial chemicals. I rate TTI as a hold with a target price of $3.19. TTI's $160 million in long term debt and weak Water & Flowback cash flows restrain the firm's ability to maximize its Lithium-Bromine assets.

At best, the global oil market rebounds, a tailwind for TTI's legacy business, and TTI is awarded a long-term supply agreement for zinc-bromide. At worst, cooling O&G prices erase thin margins and disable a pivot into the low-carbon market. I suggest investors to wait for an opportunity with a larger upside.

Company Overview

TETRA Technologies is an oilfield services operator based out of Woodlands, Texas. Prior to the pandemic, the company operated four business segments: Maritech, Compression, Completion Fluids & Products and Water & Flowback Services. In January of 2021, the company sold its stake in the Compression division, reducing its segments to two core operations: Water & Flowback, and Completion Fluids & Products. Additionally, the company holds 27,000 acres of brine leases in Arkansas, containing lithium carbonate equivalents ('LCE') and bromine, both key ingredients for industrial energy storage and other applications.

Revenue Drivers

Grand View Research

The largest driver of revenue for TTI is drilling activity for oil and gas. Given the politics and volatility of the O&G market, estimating prices is not an endeavor for the retail investor. For simplicity's sake, I assume that the global market remains reliant on O&G for the next 5 years, keeping WTI prices higher for longer. The chart above demonstrates the growth of the Drilling Fluids Market in the US with a steady CAGR of 4.5%. The share of Water-based (brines) fluids is increasing, a boon for TTI's core business, as the majority of the firm's Completion Fluid products are brines. Much of the growth in water-based completion fluids stems from concern over the environmental impact of other completion fluids. TETRA's CS Neptune product line sites itself as the one of the top completion products for environmentally sensitive drill sites (North Sea, GoM).

{kind=link}

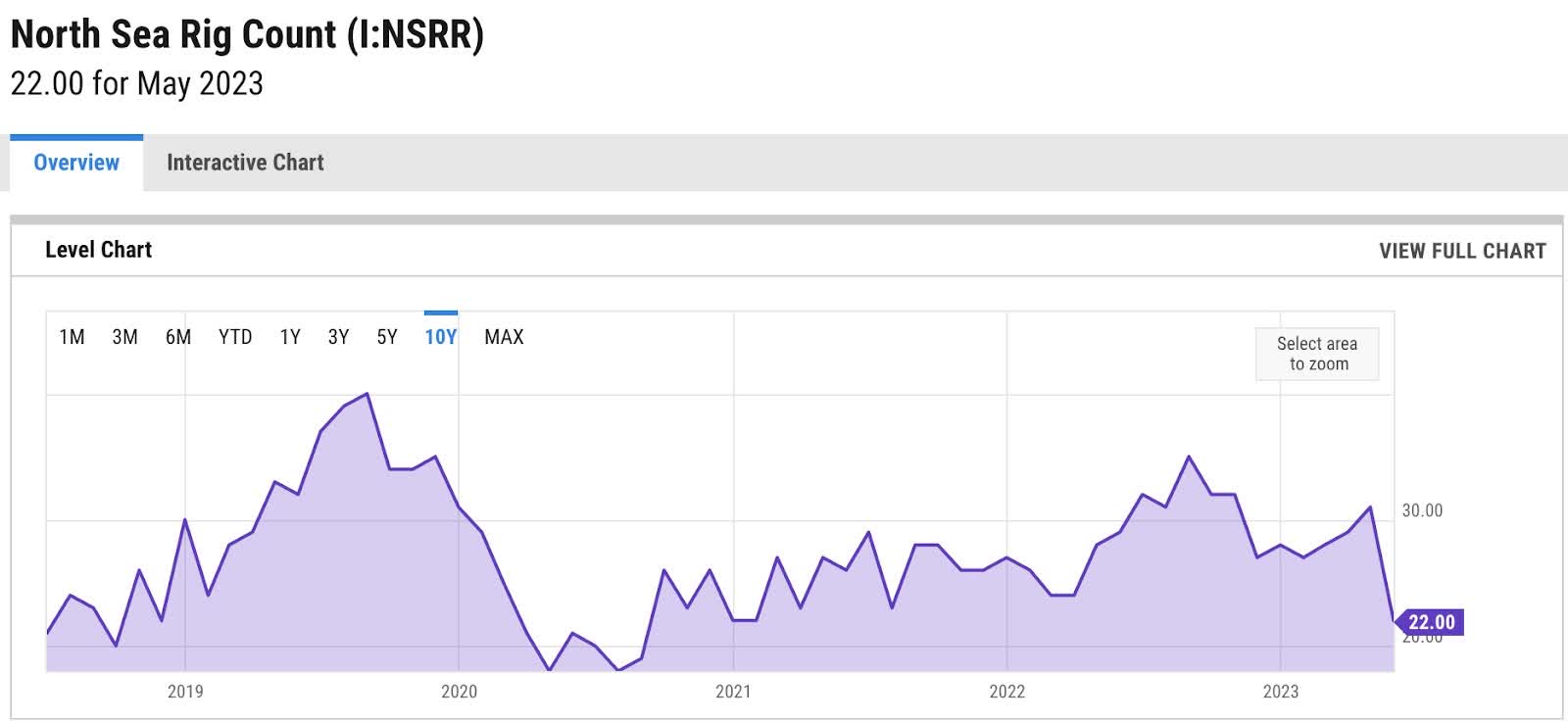

Offshore rig count growth is an important revenue driver for TTI, particularly in the North Sea. I expect activity to cool slightly as a recession approaches and then to return back to a historical average of 30. Management has recently noted that they are working on a new potential fluids contract this year in the North Sea, and foresee moderate growth in the region.

The second component in TTI's revenue mix is the growth in bromine-related products used in completion fluids and battery storage. Historically TETRA has purchased its input bromine on low-cost, long term contracts; however, the multi-year upcycle in offshore rig activity has pushed the firm to purchase excess bromine on the open market to fulfill its fluids obligations. TTI is in the early stages of developing their bromine and lithium leases to manufacture proprietary bromine, which could lower costs and add an additional revenue stream. The firm believes that some of these brine products, like zinc-bromine, are key ingredients for industrial battery fabrication.

Segments

TTI operates through two main business segments: Water and Flowback, and Completion Fluids. The Water and Flowback division is responsible for managing fracking injections and wastewater. This includes monitoring, pit-lining, filtration, and blending. TETRA also provides software to optimize these processes, lowering headcounts for drillers.

The Completion Fluids segment includes the sale of proprietary chemical blends-particularly salts and salt-based brines for O&G applications. TETRA claims that they are, "the only oilfield service provider to manufacture [their] own calcium chloride and heavy brines". Furthermore, TTI sells its industrial grade calcium chloride formulated for non-energy applications: Food & Beverage, Road Salts, Agriculture.

While the bulk of the business is devoted to calcium chloride and oil field services, TTI manages several 'low carbon' projects. TTI's selection of salt-brines, specifically zinc-bromide, is a main ingredient in zinc-bromide batteries. Zinc-ion batteries are being considered as an alternative to lithium-ion, which could potentially be extracted from the 27,000 acres of brine and lithium carbonate equivalent ('LCE') deposits leased by the firm.

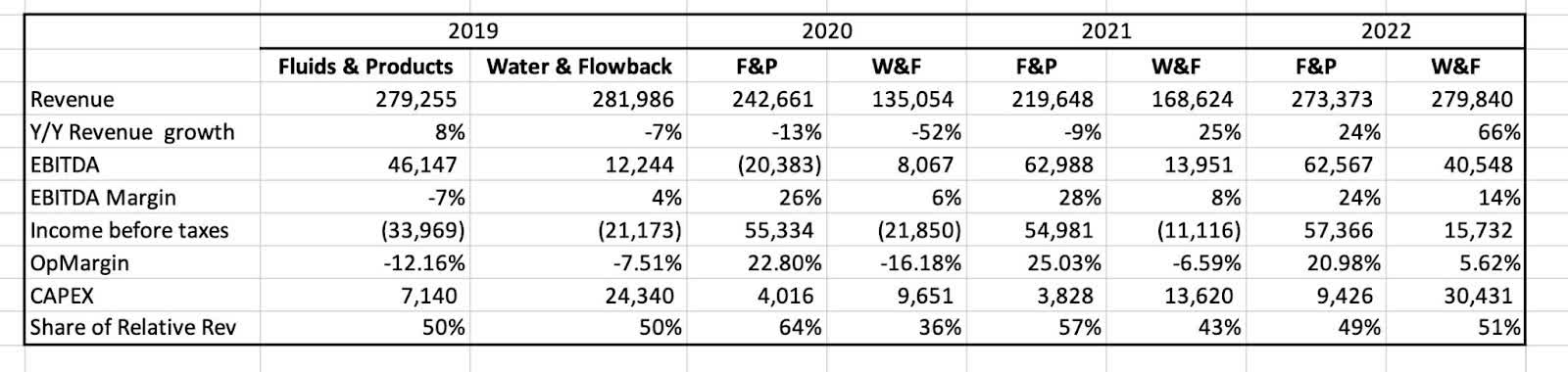

Segment Overview, Values in $000s:

{kind=link}

As of the latest quarterly report , both segments generate roughly equal shares of revenue, however, the Fluids & Products (F&P) division is a significantly stronger unit on almost all metrics. The firm's current strategy is to leverage knowledge and patents from previous O&G applications to high growth, renewable-based initiatives via the F&P unit. The Water and Flowback (W&F) division enables the firm to complement the sale of high value fluids while providing services that (theoretically) add small cash-flows. Unfortunately, the W&F unit has been absolutely and relatively weaker than the F&P division, causing concern looking forward if rig activity takes another pandemic-style knock. On the most recent conference call, management has noted "the strategic priority of margin expansion". To the firm's credit, the W&F division has delivered positive, albeit thin, quarterly operating margins since Q1 of 2022.

Debt

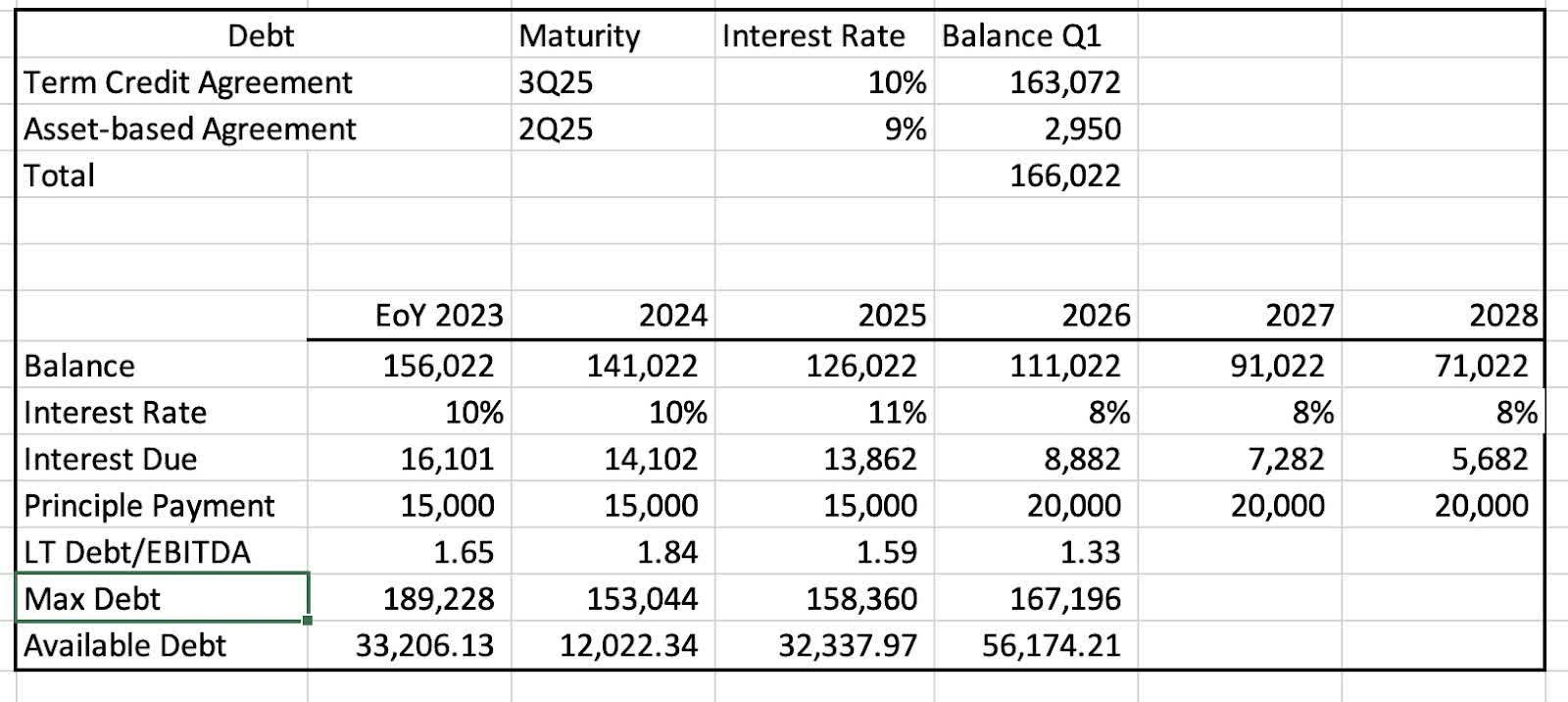

TETRA's debt remains a significant weakness for expanding its low-carbon initiatives. On the most recent conference call , management has noted that the firm does not wish to be levered more than 2x long-term debt to EBITDA.

The table below forecasts TETRA's long-term debt profile. In conjunction with EBITDA projections, I estimate the amount of long term debt TETRA can assume while staying at 2x leverage by multiplying the projected year's EBITDA by 2 and subtracting from the year-end long term debt balance. I assume that TTI makes consistent principal payments of $15MM/year, refinances the remaining debt in 2025, and pays 8% interest thereafter. TETRA's current variable rate on its $160MM 'Term Credit Agreement' is SOFR plus 500bps.

Although TTI is not in existential debt trouble, some credit tightness in 2024 and 2025 suggest significant dilution if the firm undertakes its lithium-bromine project in the next two years. If TETRA's core business remains strong into '24 and '25, there is potential for larger principal payments, but this credit availability will fall short of the 2-year $250+ million capital needed to construct bromine-related assets.

{kind=link}

Base-Case DCF Model

To arrive at a fair-value estimate for TTI, I project and discount future cash flows. I do not account for any potential Bromine initiatives or one-off renewables-related contracts. I estimate FY2023 revenues and income using the firm's guidance and my own quarterly assumptions. For 2024 revenues and beyond, I use annual growth rates based on a mix of historical and forward-looking factors.

My model assumptions include:

-

TTI finishes Q2 at the bottom range of company's guidance for Revenue and Net income (EBITDA guidance range is for Q2 is $27-30MM)

-

Q3 and Q4 Revenues are determined in-line with historical y/y growth rates

-

SG&A remains constant at 16% of revenues

-

Revenue in 2024 assumes a mild recession with a top-line y/y growth of 8%, growing 10% thereafter

-

The terminal value of TTI's business is 7x EV/EBITDA

-

NPV includes a discount rate of 10%

My base-case model suggest TETRA's stock has an intrinsic value of 3.27, roughly on-target with the most recent stock price. However, this model does not assume any cash flows from advancements in the Bromine or Lithium business. If the projects do materialize, cashflows will likely begin on or after 2026.

TTI DCF, Discounted at 10%, all figures in $000s (Company Filings, Author's Calculations)

{kind=link}

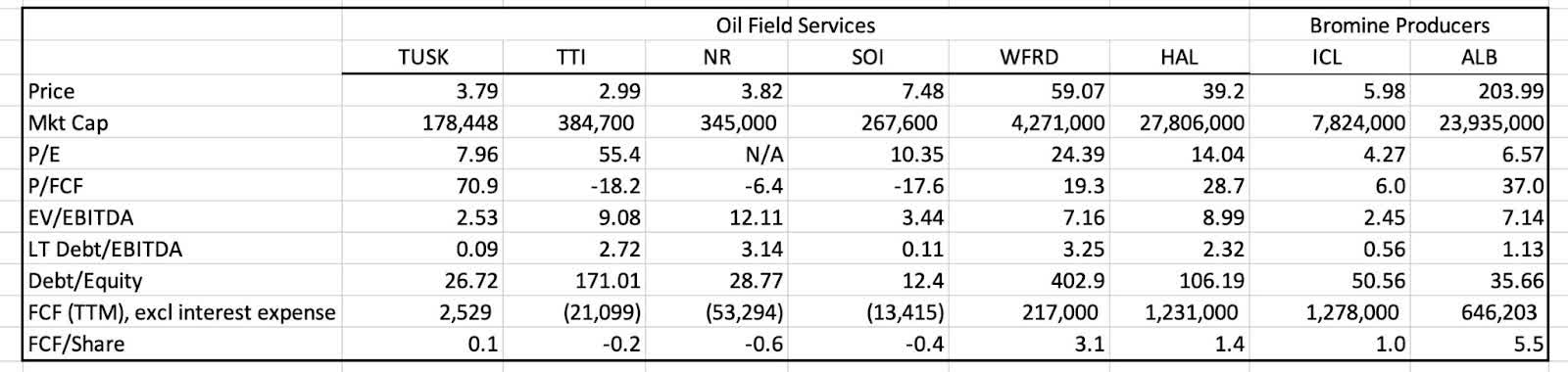

Peer Group

{kind=link}

The above table compares TETRA to five selected OFS companies, and two of the largest producers of bromine products. TETRA does not demonstrate differential performance relative to its peers. From an earnings perspective, TETRA appears to be relatively expensive, given its peers' average P/E of approximately 15. If TTI begins generating substantial earnings from its legacy segments before capitalizing on bromine assets, then such a high multiple is warranted, but until then I'll be waiting for a better deal.

Also of slight concern is TETRA's debt overhang, which stands out relative to its peers. With a Debt/Equity ratio of 171, only giants like Weatherford ( WFRD ) and Halliburton ( HAL ) have similar or higher debt ratios, however, these companies are much larger and occupy a greater part of overall market share. Similarly, with a LT Debt to EBITDA ratio of 2.72, TETRA needs to improve these metrics before increasing borrowing to fund new capital expenditures.

With respect to Free Cash Flow, TETRA has some catching-up to do. With a Price to Free Cash Flow ratio of -18.2, only Solaris (SOI) has a similar cash flow ratio of -17.6. In contrast, though, Solaris boasts lower debt levels and higher earnings power. If TETRA posts positive Free Cash Flow this year, that will be an obvious boon for the stock, but more important will be TTI's ability to generate consistent free cash, a weakness from previous years.

Lithium-Bromine Potential

Recently, TTI announced a partnership with Exxon ( XOM ) to continue developing Lithium and Bromine assets. The details of the deal have not been made public, and until then I suggest that TETRA's acreage of lithium and bromine leases do not provide as much upside as anticipated. The firm holds long term leases over 27,000 acres in Arkansas which form part of the Smackover geological formation. The Smackover is the only source of commercial bromine in the US, containing enough potential lithium for 50 million EV batteries. If TTI can build and produce bromine using its own resources, the firm will no longer be dependent on long-term supply contracts to meet its completion fluid production needs. Additionally, TETRA can sell excess bromine on the market for additional profit.

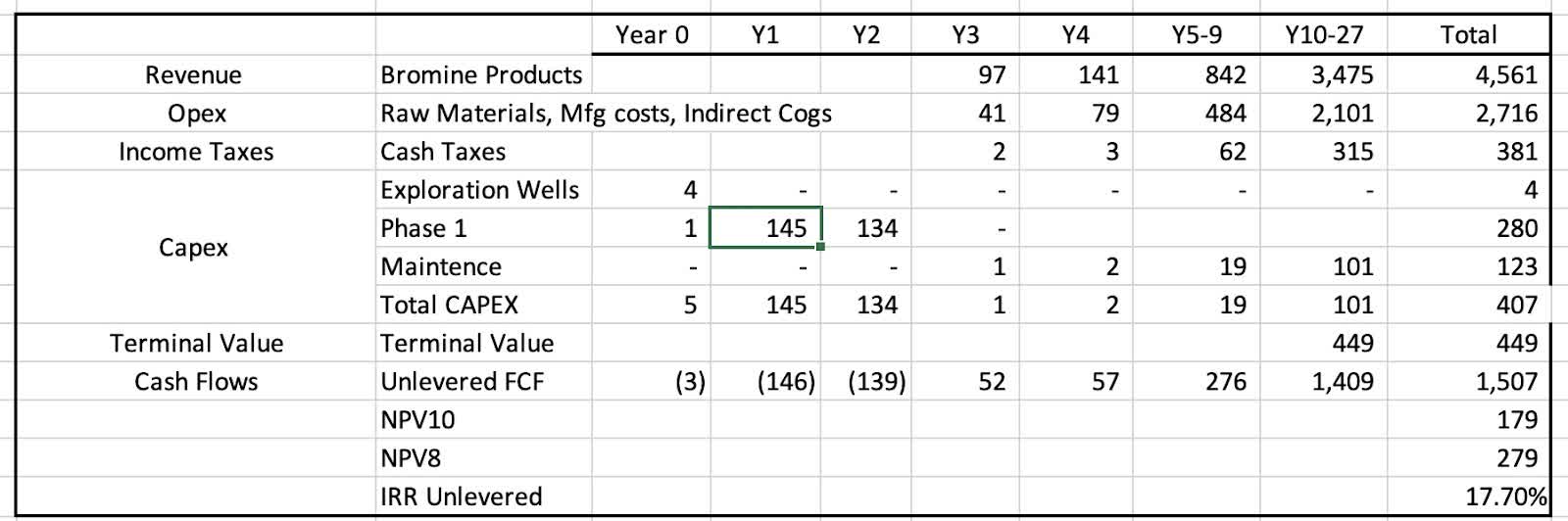

In September of 2022 the firm released a maiden inferred resources report estimating 3.9 million tons of bromine resources. This 129-page document details the geological structure of the property, and recommends next steps to increase the certainty of bromine concentration levels. In February 2023 the company released an SK-1300 Preliminary Economic Assessment , which is partly summarized in the tables below. This assessment estimates needed capital expenditures to obtain potential free-cash flows to the firm. The NPVs provided below reflect the difference in the NPV from TETRA's current bromine business from the NPV if the firm fully develops the bromine project.

{kind=link}

The second table below compares the differences in the NPV of TETRA's bromine business with and without investment in the plant. At this stage of project development, I remain skeptical that TETRA can find capital to finance the project without diluting current shareholders or giving up a significant portion of the project's profits. Furthermore, the development of TETRA's land is still in early stages of exploration, and further drilling and testing is needed to move the assets up the levels of mineral resource classifications. Even though the geological landscape of the Smackover is variable, the neighboring LAXNESS plant gives credibility to initial estimates. Until further resource reports are published and a financing plan is clear, I am hesitant to assume that the bromine project's current NPV is worth anything at all, even in the face of management conference call optimism.

SEC Filings

Risks

My current model includes obvious risks, many of which have been addressed. First, of course, if the chance of a global recession depressing the price of oil, the most important driver of TETRA's legacy business. Second, a recession could similarly impact the growth of TETRA's brines which are needed for industrial and agricultural applications. Finally, TETRA could mishandle the development of its Bromine and Lithium reserves, resulting in shareholder dilution or worse, bankruptcy if the company increases leverage without generating earnings.

What-if...

TETRA Technologies, at its current price of $3.40 has the potential to multiply in the next 5 years with some luck. If WTI peaks again above $85 (without sending the global economy into a nosedive), TETRA secures a long-term zinc-bromide contract and confirms attractive financing, then the stock could easily be worth beyond $6/share. Until then, I'll be walking - but not running - with my shares to the nearest exit.

For further details see:

TETRA Technologies: Waiting For A Better Price