TCBI - Texas Capital Bancshares: Non-Interest Income Overshadows Slow Loan Growth

2023-08-03 04:54:31 ET

Summary

- Investment banking segment performance overshadows rising cost of deposits.

- Non-interest income is growing at a remarkable pace.

- The reduction in deposits may not be such a negative factor according to the CEO.

Intro

In the previous quarterly, my concerns were mainly directed at the rising cost of deposits, and even today this factor continues to be present. However, the outstanding performance achieved by the investment banking segment is the key takeaway from this Q2 2023 and momentarily overshadows the difficulties of the current macroeconomic environment.

Texas Capital Bancshares Q2 2023

{kind=link}

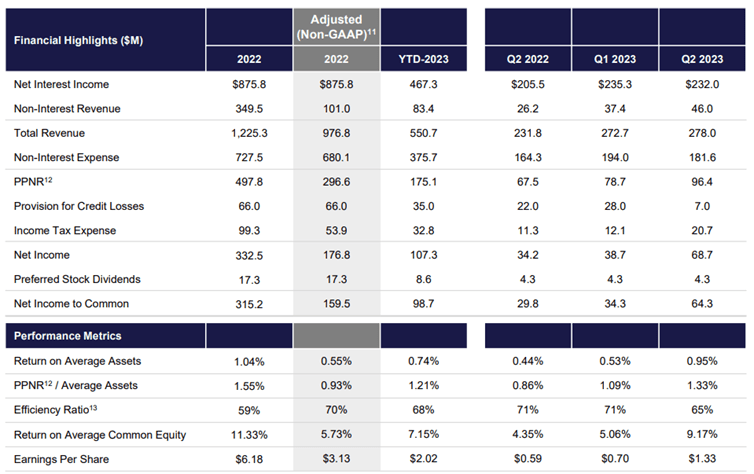

Overall, on a year-on-year basis, Q2 2023 results were definitely improving, however, the same cannot be said by comparing it to last quarter. Q1 2023 had reported a higher net interest income of $3.30 million, a signal that the rising cost of liabilities is not sufficiently offset by the increased yield on assets. However, as we shall see, making the situation less bitter was the growth in non-interest revenue, up 75% YoY and 23% over Q1 2023.

Deposits and loans

Texas Capital Bancshares Q2 2023

{kind=link}

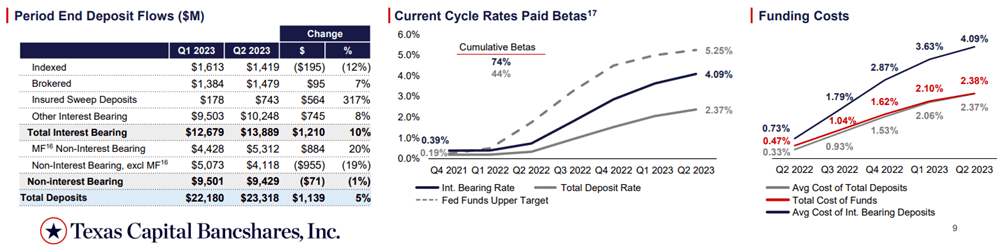

As mentioned, deposits are Texas Capital's ( TCBI ) main difficulties as cumulative betas continue to increase and make banking increasingly complex.

Texas Capital Bancshares Q2 2023

{kind=link}

Compared to the previous quarter, non-interest bearing deposits seem to have stabilized, but the difference of $3.12 billion from Q2 2022 remains large. In any case, their weight relative to total deposits is still high, about 40 percent versus 49 percent last year. Also not to be underestimated is the difference in the cost of interest bearing deposits, 4.09% in Q2 2023 and 3.63% in Q1 2023.

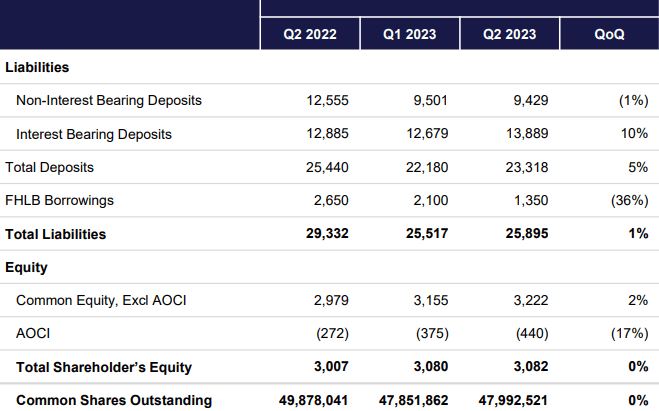

As for unrealized losses, a topic debated in recent times, it is still too early to notice the first improvements. As we can see, accumulated other comprehensive income (AOCI) is weighing more and more on the balance sheet and has reached -$440 million. If the Fed continues to raise interest rates, unless these financial instruments reach maturity, we are unlikely to see improvements in the coming months.

Anyway, the change in interest rates has an impact not only on the balance sheet but also on the income statement.

Texas Capital Bancshares Q2 2023

{kind=link}

The increase in loan volume and respective yields was not enough to offset the rising cost of liabilities, which led to a worsening of both net interest income and net interest margin. This was a fairly predictable outcome that the market probably already discounted months ago and would explain the collapse in price per share during that period. When interest rates are as high as they are now, it is logical to expect a reduction in demand for loans and mortgages, so it is not just a problem for Texas Capital, it is a problem for the entire banking industry.

However, if interest rates continue to rise, net interest income could follow the same trend as long as the cost of deposits does not rise excessively.

Texas Capital Bancshares Q2 2023

Ninety-three percent of LHI excl Mortgage Finance LHI's total portfolio is variable-rate, and 91 percent of these loans are tied to short-term interest rates; which means the yield on assets is largely correlated with interest rate trends.

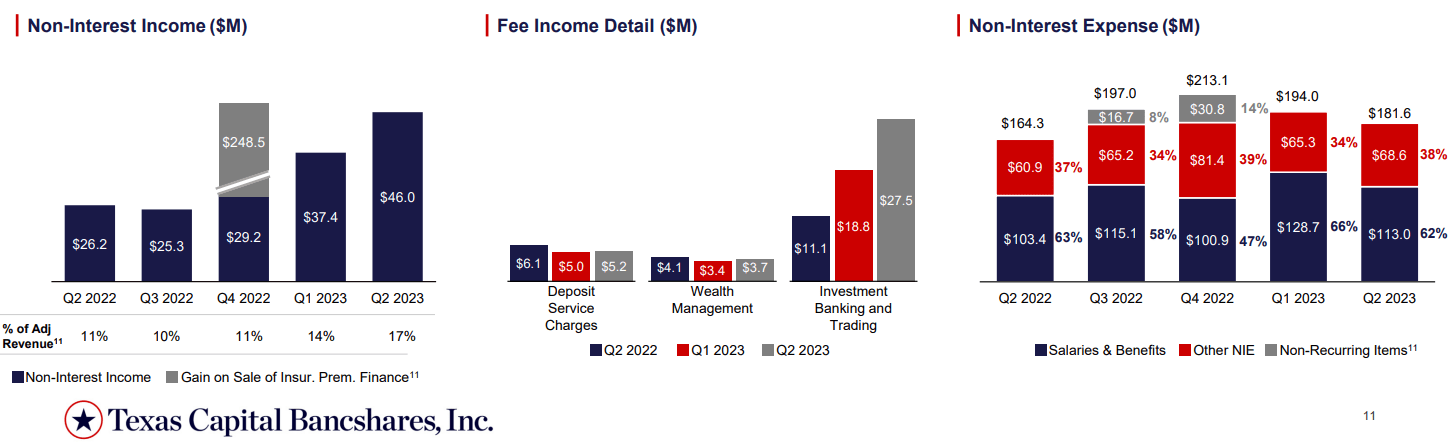

Non-interest income

As anticipated in the intro, non-interest income was the most surprising aspect of Q2 2023 and manages to offset the macroeconomic issues that are plaguing both deposits and loans. To be more precise, the strong growth in non-interest income also manages to explain part of the reduction in deposits.

We are totally agnostic to where the client is on our balance sheet, whether they're in DDA account or they move to AUM to manage liquidity because that they may be rolling out of the DDA, but they're staying on our platform. They're not leaving the firm. And so, we're here to solve client needs and over time will benefit and the client will do. But I think it's really, really important to point out that nobody is leaving the firm. They're just locating to different products and services.

CEO Rob Holmes, conference call Q2 2023.

Basically, Texas Capital's clients have shifted their funds into more profitable financial instruments rather than let them be eroded by inflation. In other words, current money market rates are too inviting not to invest excess cash, and this is probably the cause of the decline in deposits. The point is that depositors to meet this need have been using the services offered by Texas Capital, so the funds have remained within the bank albeit in a different form. The result is a worsening of deposits against an improvement in non-interest income.

For management, the most important thing is to keep its clients within its platform: whether they are borrowers, depositors, or clients looking for someone who can manage their liquidity the important thing is that they always turn to Texas Capital .

A primary focus of ours is recycling capital, and we're solving complex solutions or needs for our clients.

At this stage, management is strongly focused on the non-interest income, and the goal is to increase its relevance.

Texas Capital Bancshares Q2 2023

{kind=link}

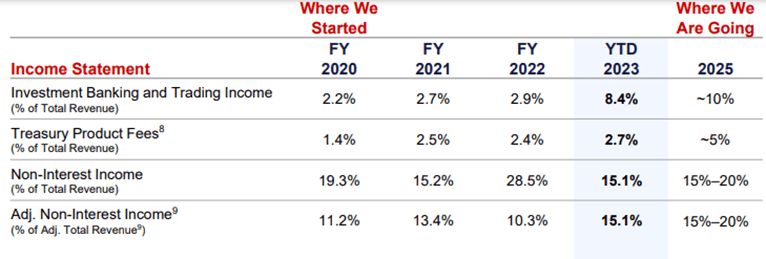

Compared to 2020, investment banking & trading income/total revenue has already improved a lot, about 6.20%, but the target by 2025 is even more ambitious, about 10%. Treasury product fees is also increasingly important, but the goal is to bring it to 5% of total revenues. Overall, by 2025, between 15-20% of total revenues are expected to come from non-interest income.

Texas Capital Bancshares Q2 2023

{kind=link}

Another positive aspect regarding this subject, is that although the improvement over last year was 70%, non-interest expenses remained under control: a 10.50% increase over last year and down 6% from last quarter. All this resulted in a good efficiency ratio of 65 percent.

Conclusion

It is clear that the Fed's restrictive monetary policy is causing quite a few concerns for the banking sector in terms of the cost of deposits, however, not all banks are in a similar situation. Texas Capital has shown that its focus in recent years on investment banking is paying off, and to date non-interest income accounts for 15.10 percent of total revenues. This, combined with a good efficiency ratio, are offsetting a net interest income that is still clearly struggling.

For further details see:

Texas Capital Bancshares: Non-Interest Income Overshadows Slow Loan Growth