TPL - Texas Pacific Land: Almost Like A Permian Basin ETF

2023-07-13 13:34:40 ET

Summary

- Texas Pacific Land generates revenue through land management and water services in the Permian Basin, with clients including Occidental Petroleum, Exxon Mobil, and ConocoPhillips.

- TPL faces long-term risks such as a lack of control over royalty revenue, a decline in the oil market, and the eventual depletion of hydrocarbon resources.

- The company is exploring alternative revenue sources, such as renewable energy installations and bitcoin mining facilities, to mitigate risks and ensure future cash flow.

Description

Texas Pacific Land ( TPL ) is a royalty-based company that owns land in the Permian Basin. The company generates income from royalties that it collects for the use and production of gas/oil on the land it owns. Buying Texas Pacific stock is a way to gain exposure to the oil and gas market without incurring exploration risk, one of the main problems in the production/extraction sector. The company has generated extraordinary returns for shareholders in recent years due to the explosion of production that has occurred in the Permian Basin since the introduction of fracking on site.

The company is free of debt and is not very capital intensive, which is reflected in its high gross margins and the minuscule capital expenditure it uses, mainly focused on the water segment. This article will describe the company and try to determine if it can be a good long-term investment.

Business segments

TPL's bulk of revenue is made via two segments: Land Management and Water Services and Operations. In the subsequent lines we briefly explain what each part consists of.

Land management: currently constitutes most of TPL's revenue and consists of two main pillars: oil and gas royalties over production and utilization of their land as well as sales of terrains to oil and gas producers while conserving the rights to generate future royalties if oil and gas is extracted.

Water services: the company provides pressurized water injection so as to fracture the rock and extract the underground oil and gas. This segment produces income via two ways: water royalties and water sales to the operators of the wells.

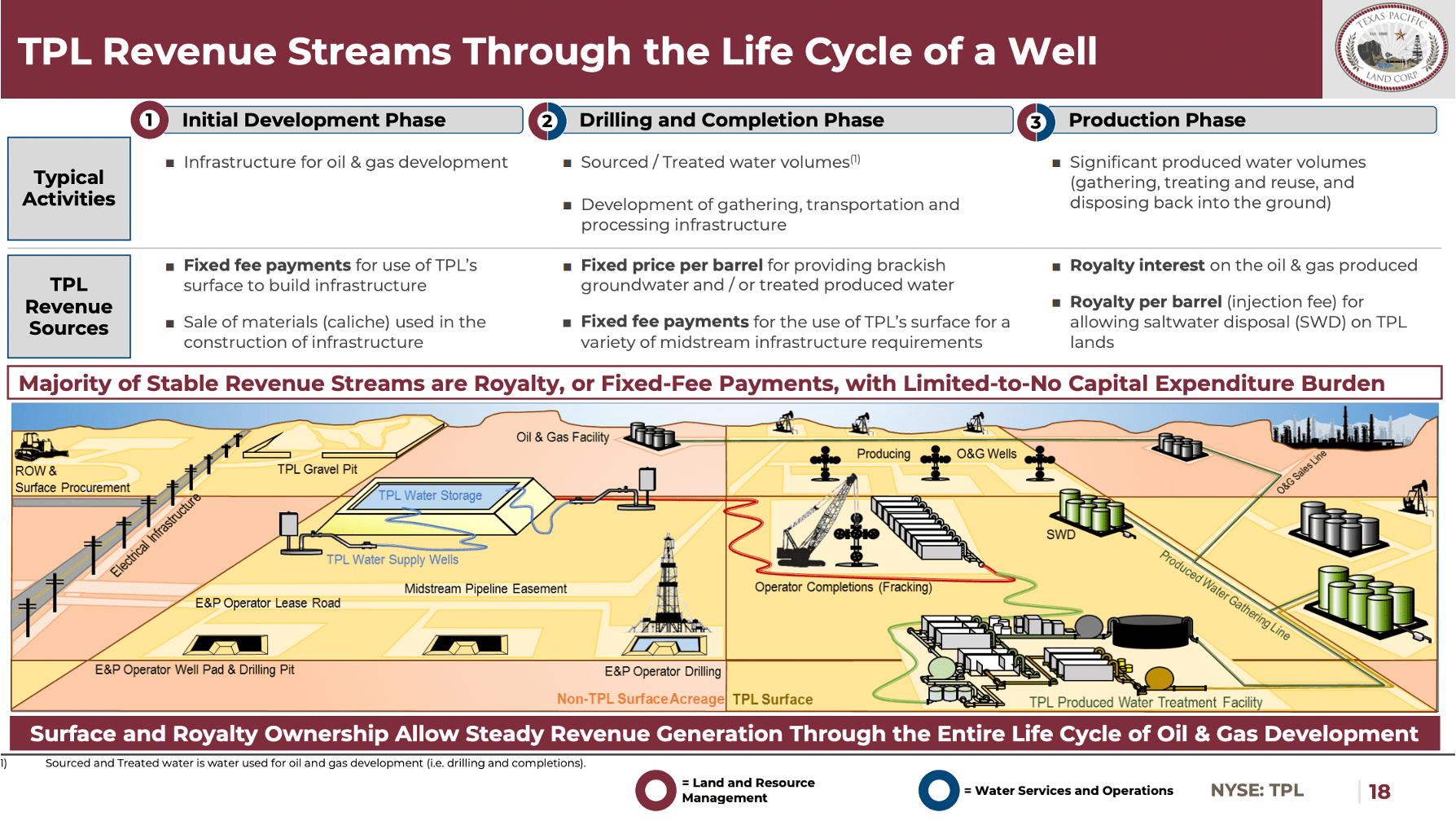

One of the main concerns that investors can have is the lifetime of the wells, as these producing assets are not everlasting and that can have a negative impact on the profitability of the company over the long term. Even though this concern is legitimate, the company mitigates this risk by generating revenues over all the stages of the life of a well. The following picture extracted from their IR page shows how they profit from all the life cycles of a well.

Revenues over the life of a well (TPL IR)

{kind=link}

Firstly, they charge fixed fees for the use of their surface to build the infrastructure. Secondly, they charge fees for managing the water underground and for using their surface for building midstream infrastructure. Finally, during the production phase, TPL generates revenue from royalties of oil and gas and royalties from injection of water in the wells.

Once we have seen how the company generates its stream of income, it is also sensible to analyze which O&G operators make up the bulk of their clients. The Permian basin is a very large producing area, so it is expected that big operators will be present extracting the hydrocarbon resources present in the area. Some of the clients of TPL are Occidental Petroleum (OXY), Exxon Mobil (XOM) and ConocoPhillips (COP). 50% of the revenue of TPL comes from 4 O&G producers and that may seem a bit risky at first glance. However, these operators are big companies, and it is highly unlikely that they will stop production in the Permian basin due to the low extraction costs per barrel of oil compared to the price at which the barrel is sold in the international markets.

Risks

It is worth mentioning that no investment is risk free. TPL faces, from my point of view, several long-term risks that may have an impact on the terminal value, from where most present value of a company comes from.

In the first place, TPL does not have full control over the royalty revenue they generate. The equation of revenues is royalty per unit x number of units. And the number of units produced depends on the operator's will of producing more, or less barrels based on market conditions. Hence, this is an important risk, but it is somewhat mitigated by the fact that production has enjoyed an increasing trend in the Permian basin and will most likely continue to do so in the coming years.

I believe the oil market will decline in the long term due to political restrictions and the necessity to reduce carbon emissions in the economy. However, natural gas will be needed in the energy transition and demand will increase in the coming years in Europe and Asia in my view. The US has the opportunity to increase the production in the Permian basin and convert itself into one of the biggest suppliers of LNG in the world.

Another major concern is what will happen when wells run out and become dry of hydrocarbons. The company is highly dependent on those assets and one could have serious doubts about the visibility of hydrocarbon-related cash flows. This is why the company is exploring 'next generation' alternatives that may produce royalty-based cash flows that in the long term will replace the high dependence on hydrocarbon-related revenue. Some projects include renewable energy installation and bitcoin mining facilities, among other ideas.

{kind=link}

Financial performance

The next key point to assess is the financial statements. How has TPL been performing in terms of fundamental values over the last years? Revenues have multiplied by 300x since 2002, this is equivalent to an CAGR of 33%, mainly due to the huge increase in oil and gas production in the Permian Basin. Operating income, on the other hand, has grown at smaller rates of 24% annually, still a remarkable achievement for a company whose main exposure is the hydrocarbon market. One could question whether the company has made optimal investment strategies (due to the fact that profits have grown at a more slow pace than revenue), but this is due to the fact that over the last years the company has increased its investments in the water management segment. This is more capital intensive than land management and the main reason why expenditures have increased for the corporation.

The development of the Water Services Segment has slightly changed the distribution of revenue in the company, but currently the Land Management segment is the most important in terms of percentage. 76% of the revenue comes from oil and gas royalties and 24% is related to Water Management (Water Royalties and Water Sales). It is expected that in the coming years the company will gradually reduce its exposure to oil and begin to look for other types of uses for the land in order to maintain stable sources of income from the use of its land.

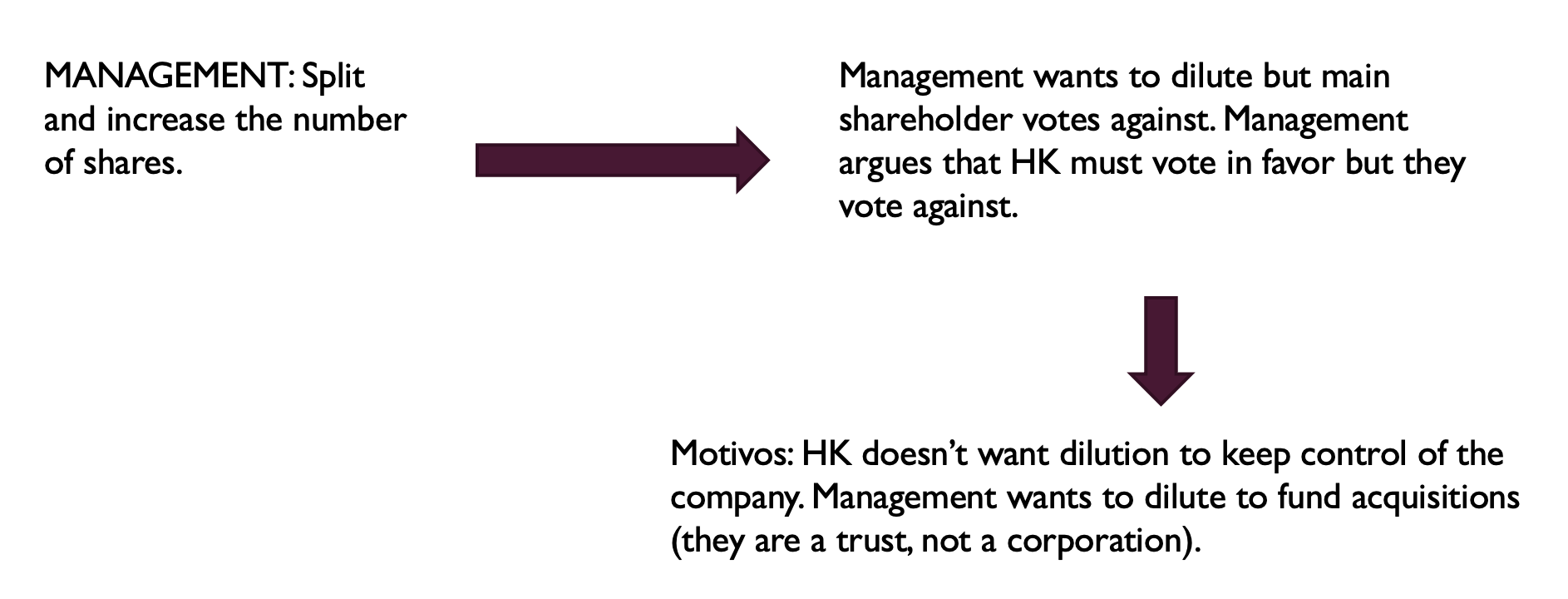

Issues with the board

Over the last months the company's board has been on the spotlight due to a series of conflicts and litigations with Horizon Kinetics, TPL's major shareholder. The source of conflict has been related with the board's will of issuing shares to get cash in order to fund new acquisitions, something which the main shareholder of the company (Horizon Kinetics, HK) currently rejects.

Source of conflict in Texas Pacific Land (Own Models)

{kind=link}

The above panel shows the conflict that exists within the trust between the major shareholders and the board.

Currently, HK owns around 18% of the shares outstanding and the company has a total weight of 35% in their portfolio. Based on the letters of Horizon Kinetics, I highly doubt that they will reduce their investment in the company as the investment purpose is double: not only is the company highly related to the Permian Basin performance, but they probably see all the optionality that come with investing in land, which can be a hedge against inflation.

Valuation

Royalty-based companies are hard to value because their NPV depends on the future cash flows they can produce based on the interest on minerals they control. One of my arguments against multiple valuation is that it is really static and only looks at the present and not at the future. Imagine that we went back to the end of June 2007 where the company traded at around $60 per share and its EPS was $0.78. Using multiples (on net profit), one would have immediately said that the company was expensive and hence the average investor would have not considered even buying it. Today the company generates a diluted EPS of $57 (almost the price of the stock back then) and its price is higher than $1000. I want the reader to understand that I am not making a case against multiples. Under certain conditions they are useful. But when a company has lots of optionality and is positioned over huge reserves of oil and gas that can be exploited for long periods of time a more in-depth analysis is needed.

My argumentation before clearly indicates that I will not give price targets or anything of the sort regarding this company. I think that what investors should weight in the valuation of this corporation are the following points.

- Will the Permian basin continue to be a major oil and gas producer in the world or will its production capacity decline?

- Will the company be able to substitute hydrocarbon-related revenue with complementary sources of revenue that will guarantee the visibility of cash flows in the future?

The potential investor in Texas Pacific should consider how the above questions may affect the company's terminal value risk and determine accordingly whether or not the stock price is low relative to such risk.

Conclusion

Texas Pacific Land is a useful vehicle to get exposure to increasing O&G production in the Permian Basin as well as the appreciation of land in the area. Even though production will increase in the coming years, there are several risk factors that need to be taken in consideration such as exposure to the oil market and how will hydrocarbon-related revenues be substituted in the future.

For further details see:

Texas Pacific Land: Almost Like A Permian Basin ETF