TPL - Texas Pacific Land: 'Buy Land They're Not Making It Anymore'

2023-11-26 07:00:00 ET

Summary

- Texas Pacific Land Corporation owns prime real estate in the Permian Basin, the largest U.S. oil and gas basin.

- TPL generates revenue through fixed fees, material sales, and royalties from major customers like Occidental Petroleum, Chevron, Exxon Mobil, EOG Resources, and ConocoPhillips.

- TPL has impressive financial performance, with a 40% compounding growth rate in free cash flow from 2016 to 2022 and a 10-year average annual total return of 47%.

This article was coproduced with Leo Nelissen.

It’s time to talk about what may be one of the coolest stocks on the market.

A company flying under the radar.

A company that benefits from the oil boom without producing a single drop of oil.

A company that has its roots in the railroad industry that used to be a land trust and now benefits from the shale revolution as a C-Corporation.

That company is the Texas Pacific Land Corporation ( TPL ).

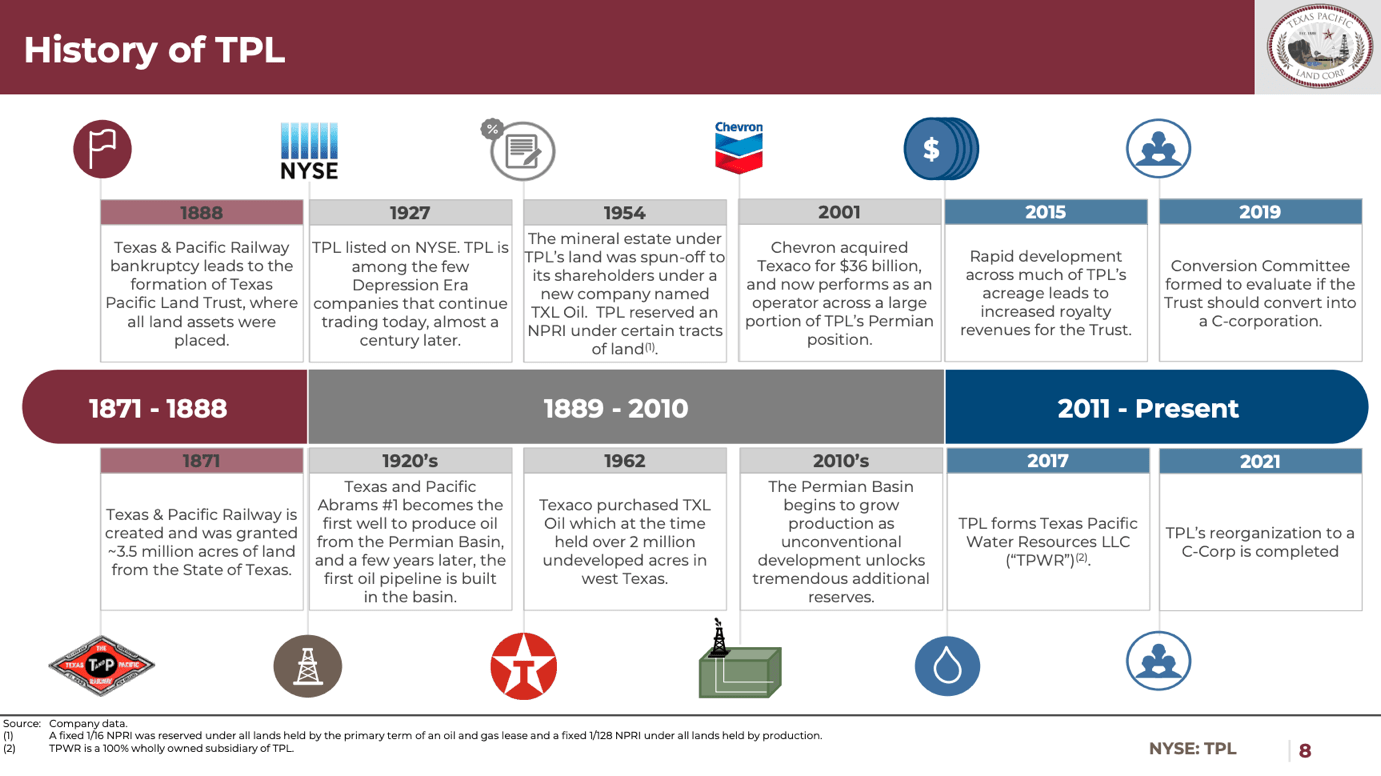

Texas Pacific Land, tracing its roots back to 1888, was initially established as Texas Pacific Land Trust.

Operating under a Declaration of Trust, the entity's primary purpose was to receive and manage extensive land tracts in the State of Texas, previously owned by the Texas and Pacific Railway Company.

This railroad is now a part of the mighty Union Pacific Corporation ( UNP ), the nation’s largest stock-listed railroad.

{kind=link}

A significant chapter in TPL's history unfolded on January 11, 2021, when the trust underwent a strategic reorganization.

This transformative process marked the transition from Texas Pacific Land Trust to Texas Pacific Land Corporation.

It’s not a REIT and has perhaps one of the safest business models in the world:

Buy land, they're not making it anymore. - Mark Twain

However, it doesn’t just own random land.

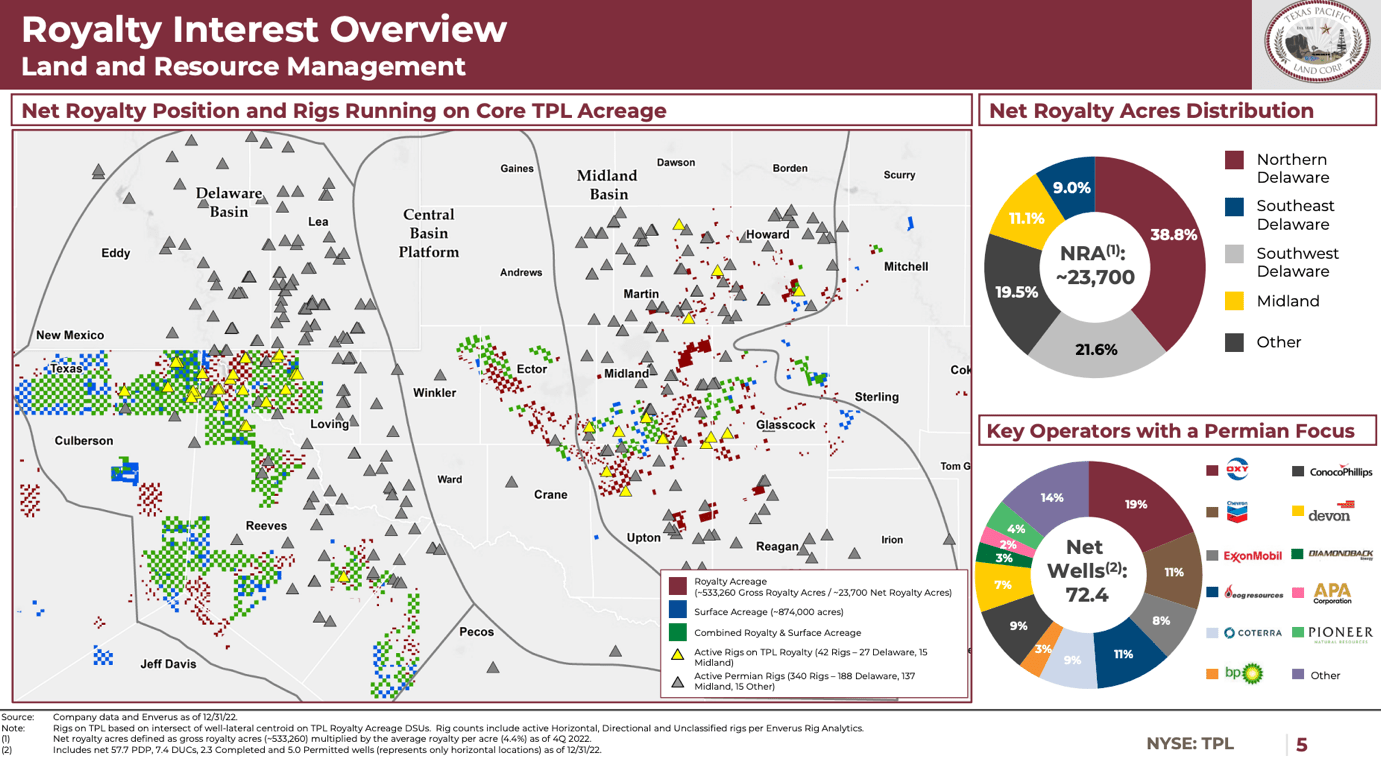

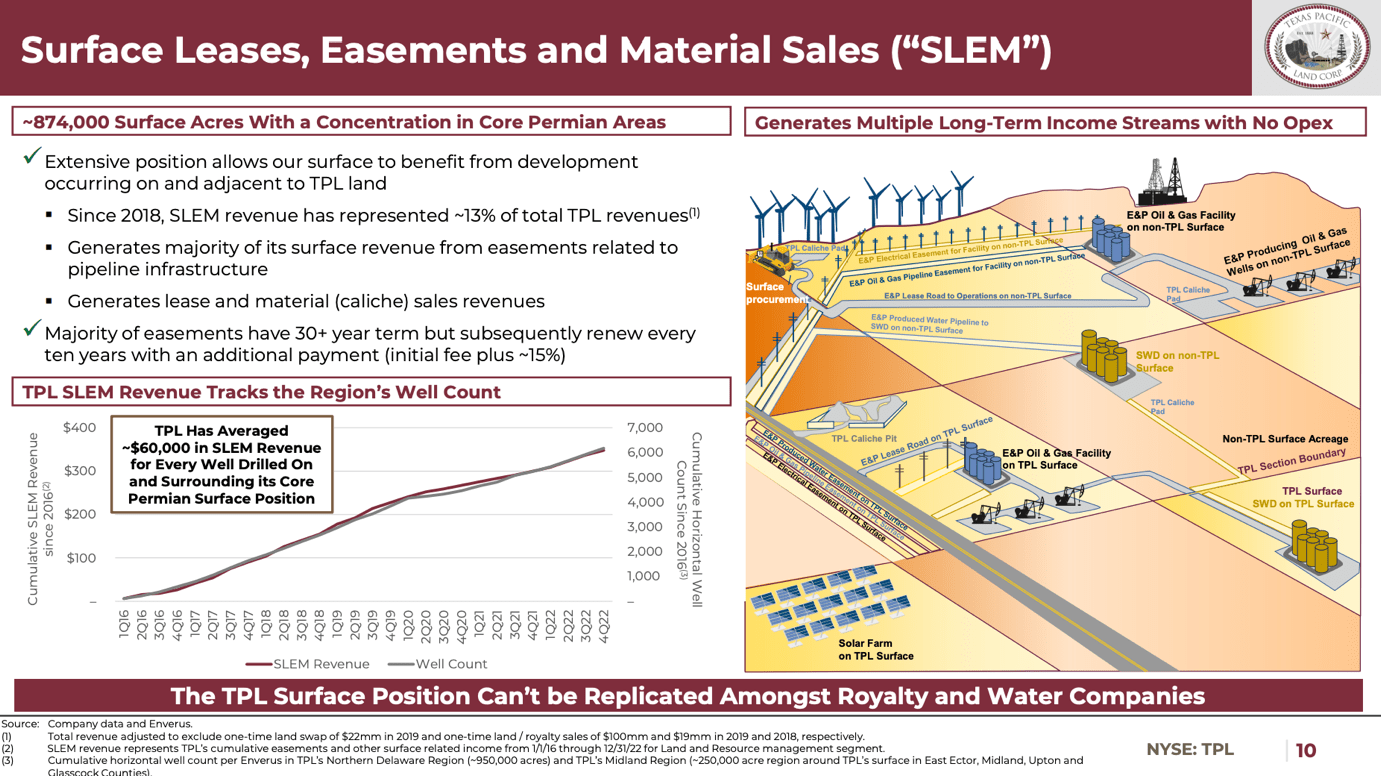

It owns some of the most valuable land anywhere in the world, as TPL stands as one of the largest landowners in Texas, boasting approximately 874,000 acres in West Texas, primarily concentrated in the Permian Basin.

This brings me to a brief history of the biggest oil and gas basin in the United States.

The Place To Be: Permian Real Estate

Oil is one of the most important forces moving macro numbers like inflation. One reason why the United States – and most Western nations – saw subdued inflation between the Great Financial Crisis and the pandemic is the shale revolution.

The chart below shows just how significant the shale revolution was in the United States, as it ended a multi-decade decline in oil production.

(Goehring & Rozencwajg)

The shale revolution was so wild that it caused supply growth to significantly outpace demand growth, which paved the wave for two major oil price declines in both 2015 and 2020.

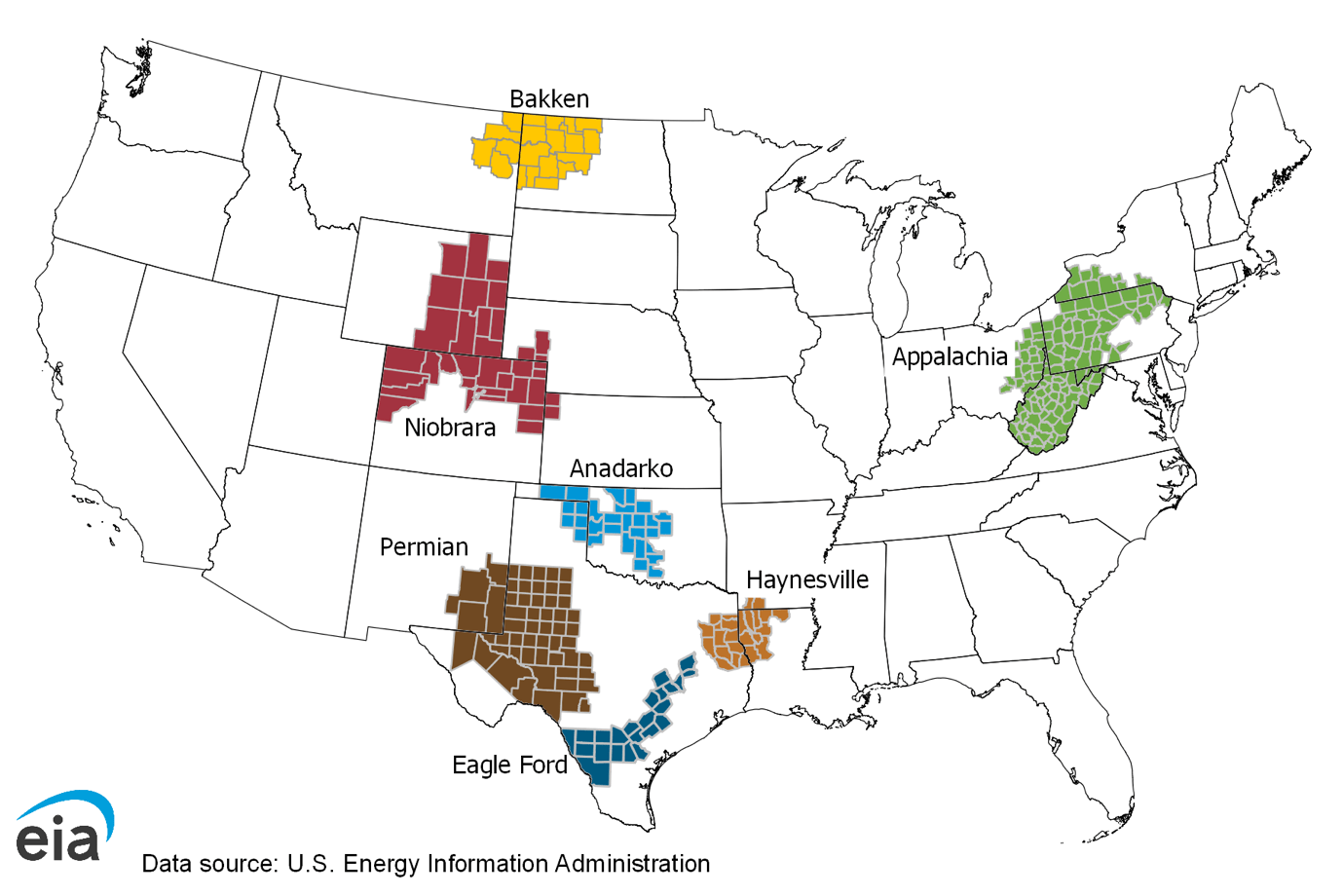

With that in mind, the U.S. is home to seven major oil and gas basins.

{kind=link}

Although all of these basins are important, one of them stands out.

The Permian is the single most important basin in the United States for two reasons:

- It’s the biggest basin.

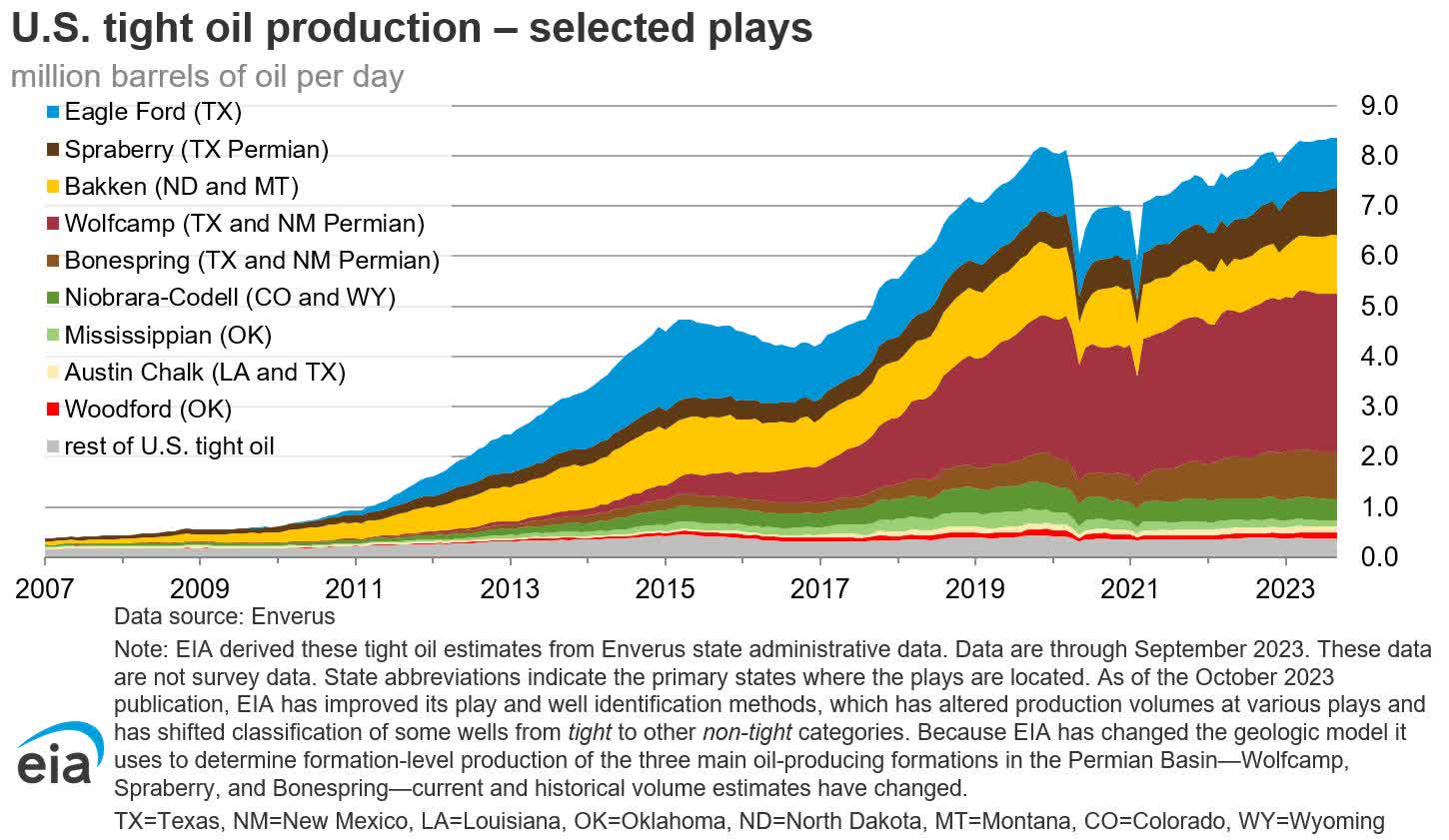

As we can see in the chart below, in 2007, the U.S. barely produced any tight oil (shale/unconventional oil). That number is currently losing momentum at more than 8 million barrels per day.

The Permian produces most of it, as it is home to Spraberry, the Wolfcamp, and Bonespring plays.

{kind=link}

Furthermore, the data shows that shale output is losing steam. Producers are running out of Tier 1 inventories, and most prefer to focus on free cash flow instead of rapid production growth.

This way, they pressure supply growth, making steep oil price declines in the future less likely. It also allows them to spend more cash on dividends and buybacks.

To illustrate Tier 1 inventories, the International Energy Forum estimates that without new production, U.S. unconventional production could see an 81% decline by 2030!

(International Energy Forum)

This is one of the reasons why we are bullish on oil (long-term), as unconventional supply growth is rapidly slowing down, and OPEC is enjoying its regained pricing power to protect higher oil prices.

This brings me to reason two:

- The Permian is the place for supply growth.

As highlighted by Bloomberg’s energy expert Javier Blas , who confirms our prior comments, the shale sector is grappling with the aftermath of capital destruction and changing investor priorities. The industry, once driven by growth at the expense of profits, now prioritizes returns for shareholders.

From Shale 1.0, characterized by rapid growth and heavy spending, to the survival mode of Shale 2.0 during the 2014 price war, the industry has undergone transformations. Now, in Shale 3.0, the focus is on dividends and share buybacks, signaling a shift from growth to profits.

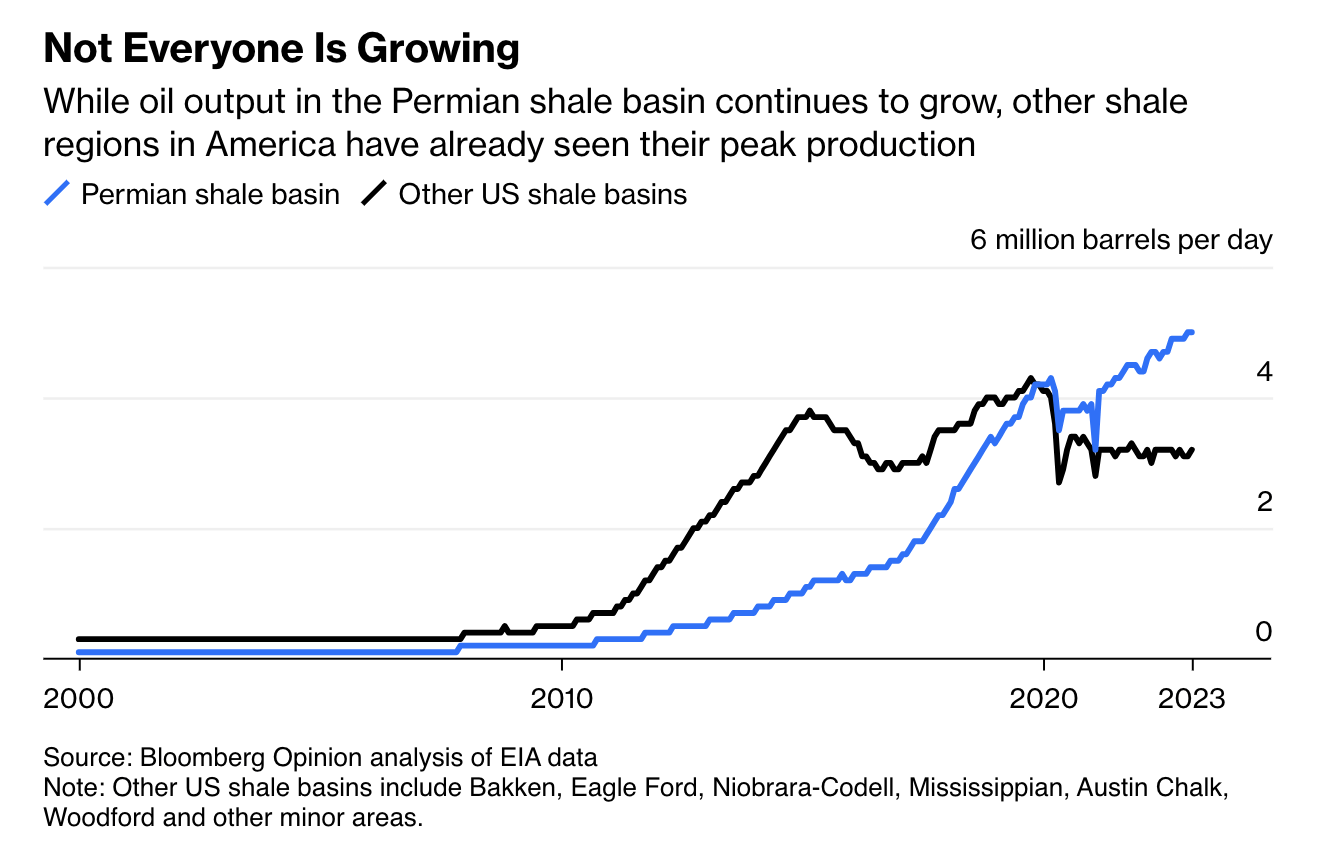

For now, the Permian is the only play capable of growing consistently! Please note that the current supply output is struggling. That’s cyclical, not a sign of peak production.

{kind=link}

However, industry leaders predict "Peak Permian" within the next five to six years, which further adds to the oil bull case.

Now, we’re seeing a wave of major M&A projects to increase Permian production.

This includes Exxon Mobil ( XOM ) buying Pioneer Natural Resources ( PXD ) and Chevron ( CVX ) buying Hess ( HES ).

When it comes to owning real estate, the Permian is the place to be. It still has years of growth ahead of it. It also has very low breakeven prices, allowing companies to keep drilling when other basins are seeing lower output.

On top of that, Texas is one of the best places for renewable energy like solar.

In 2022, Texas was the second-biggest state for solar energy. It gets roughly 5% of its energy from solar. In 2021, the state installed 6 gigawatts of solar energy. In 2022, that number was slightly below 4 gigawatts.

All of this adds to the appeal of owning Permian real estate, where the sun shines bright, oil production is abundant and cheap, and new pipelines are needed to keep up with higher production.

Buying Top-Tier Oil Royalties

As we already briefly mentioned, Texas Pacific Land does not produce oil. It owns the best real estate in the industry.

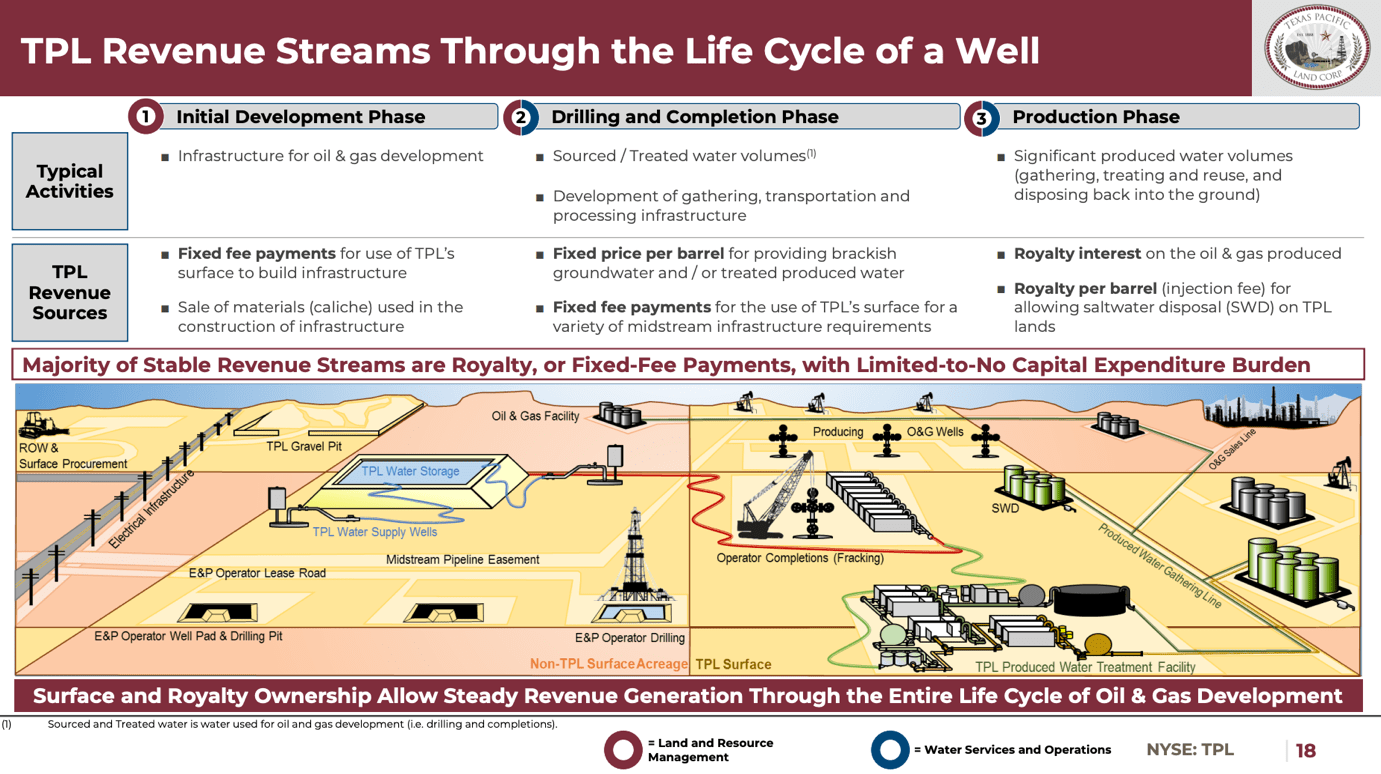

Essentially, TPL's revenue model spans the entire oil and gas development value chain.

{kind=link}

Although not an oil and gas producer, the company benefits from fixed fee payments, material sales, and royalties during different phases of well development. Among its biggest customers are

- Occidental Petroleum ( OXY )

- Chevron ( CVX )

- Exxon Mobil ( XOM )

- EOG Resources ( EOG )

- ConocoPhillips ( COP )

...which are the biggest operators in the Permian.

{kind=link}

Additional revenue sources include pipeline, power line, and utility easements, as well as commercial leases.

In addition to that, TPL is expanding its Water Services and Operations segment.

By providing full-service water offerings in the Permian Basin, the company taps into a crucial aspect of oil and gas operations.

{kind=link}

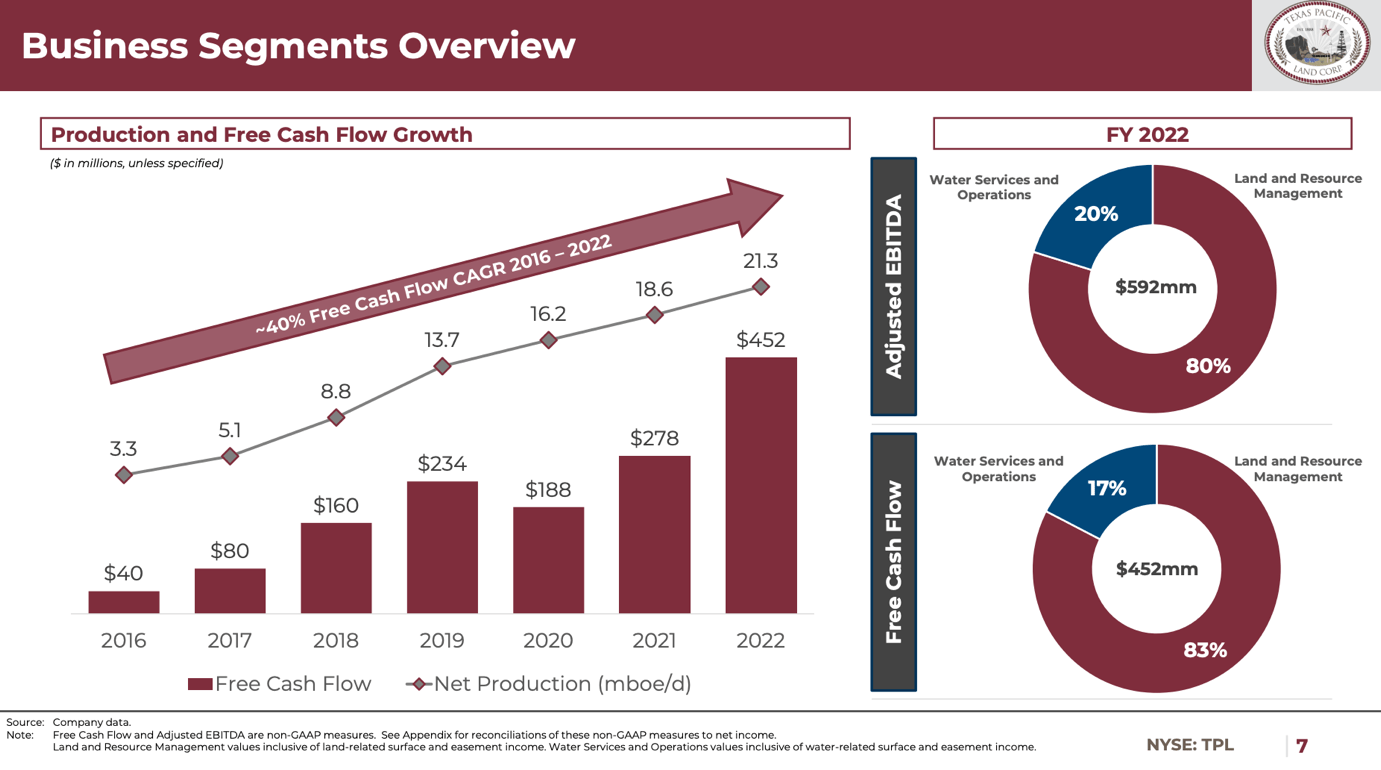

In 2022, the company saw 21.3 thousand barrels of oil equivalent (“BOE”) of daily royalty production. That’s up from less than 2 thousand BOE in 2014. In 2016, the company’s royalties were based on 3,300 BOE per day.

This allowed the company to grow free cash flow from $40 million in 2016 to more than $450 million in 2022. That’s a 40% compounding growth rate!

{kind=link}

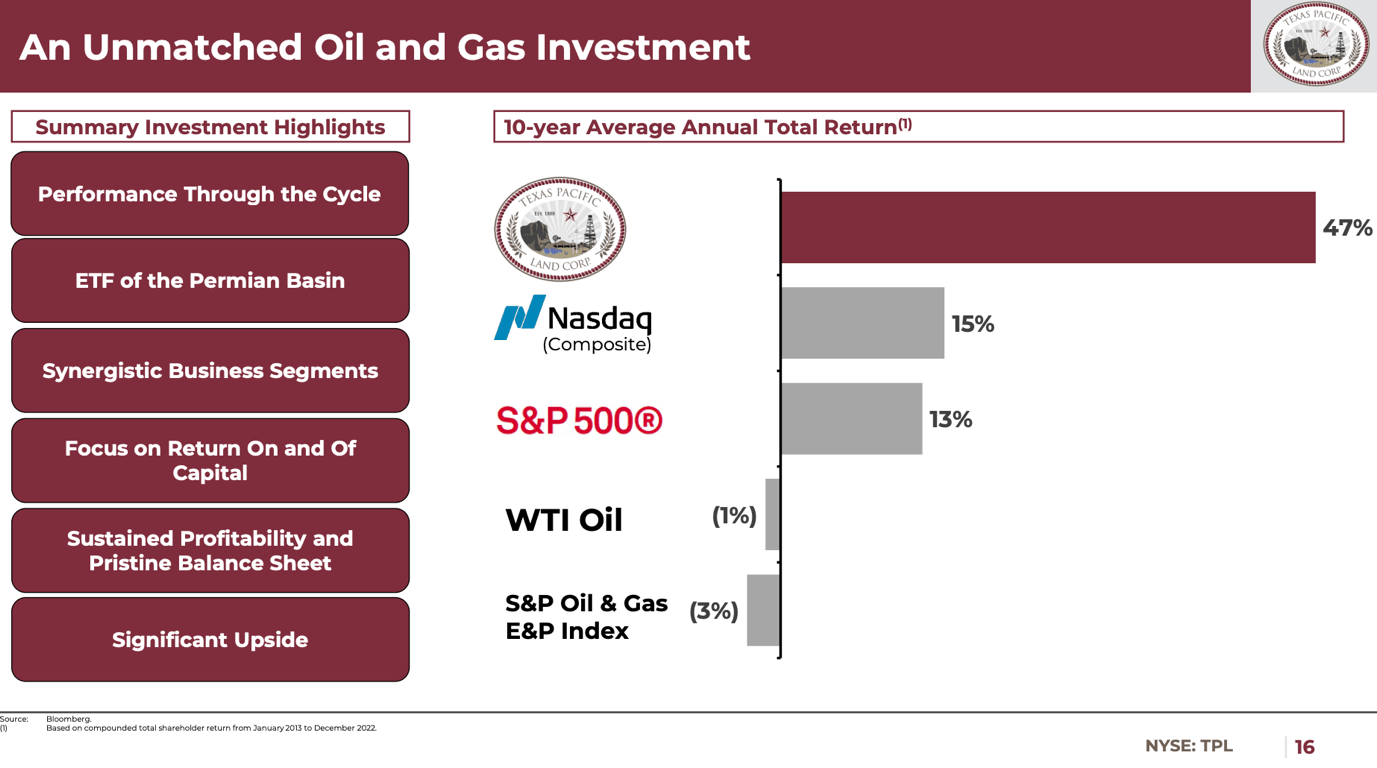

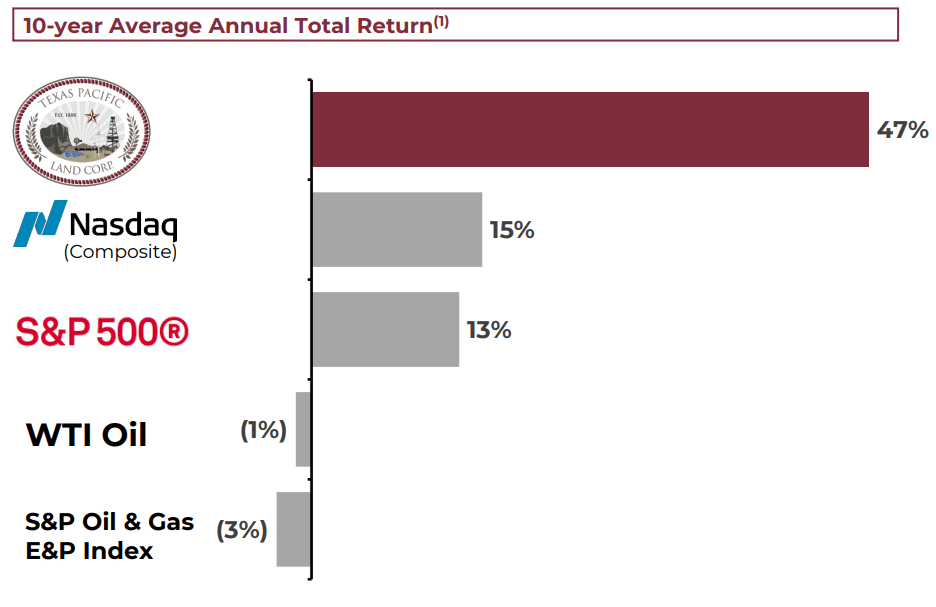

This performance allowed TPL shares to crush everything in their path.

- The 10-year average annual total return of TPL shares between January 2013 and December 2022 was 47%.

- The red-hot Nasdaq returned 15% per year during this period.

- Also, during this period, oil prices fell by 1% per year, causing oil and gas stocks to fall by 3% per year. This shows that TPL is an oil play with much less cyclical risk.

{kind=link}

Nonetheless, as one can imagine, the company remains cyclical, as its production royalties depend on the price of oil and gas.

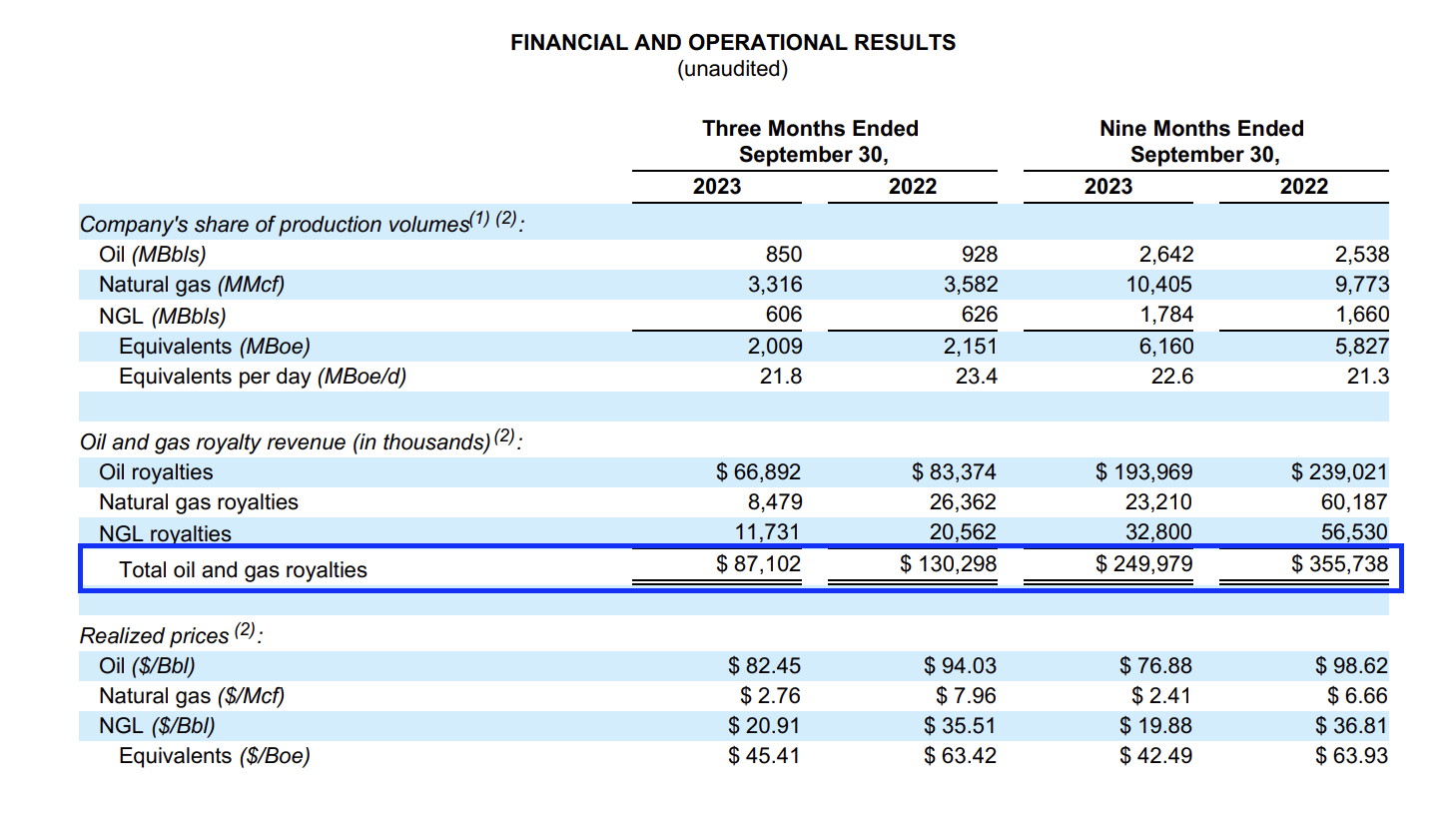

As we can see below, in 3Q23, the company generated $87 million in oil and gas royalties. That’s down from $130 million in 3Q22 and roughly half of total revenues. The other half was relatively stable.

Production volumes were down slightly, with prices taking a bigger hit, as the lower part of the table below shows.

{kind=link}

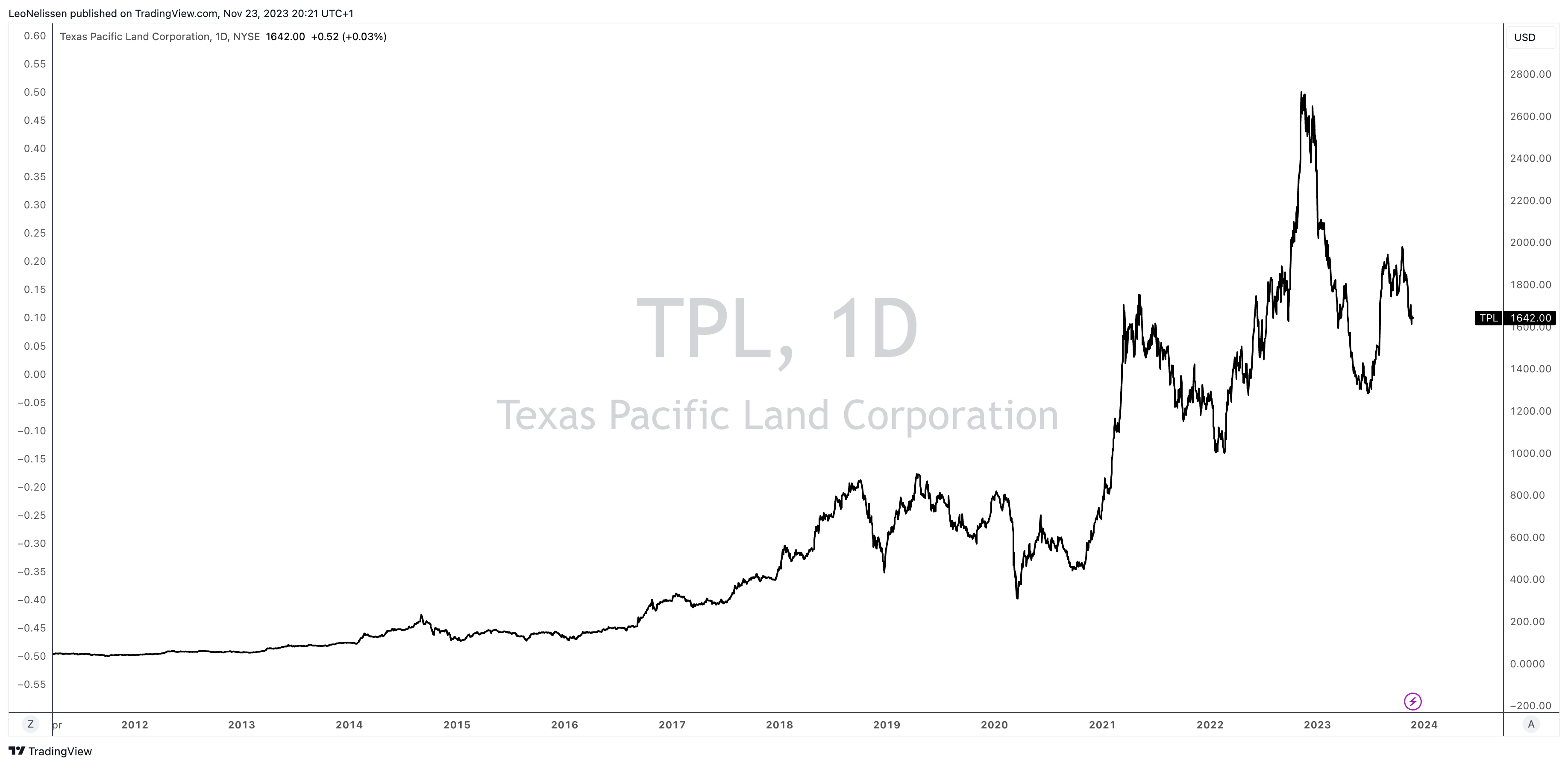

As a result, this year, the $13.2 billion market cap company is down 30% year-to-date. The stock is trading 38% below its 52-week high.

{kind=link}

This brings me to the next part of this article.

TPL Dividends

Let’s start with the disappointing news.

The company has a regular quarterly dividend of $3.25 per share.

This translates to a yield of 0.80%, as the price of a single stock is $1,642.

The good news is that TPL tends to pay juicy special dividends during times of elevated income.

Seeking Alpha

In 2022, the company paid $12 in regular dividends (4 x $3.00) on top of a special dividend of $20 in the second quarter. This brings the total dividend to $32. That’s 1.9% of the current stock price.

Although 1.9% is still nothing compared to high-yield upstream oil plays, this stock needs to be seen as a total return play instead of an income stock.

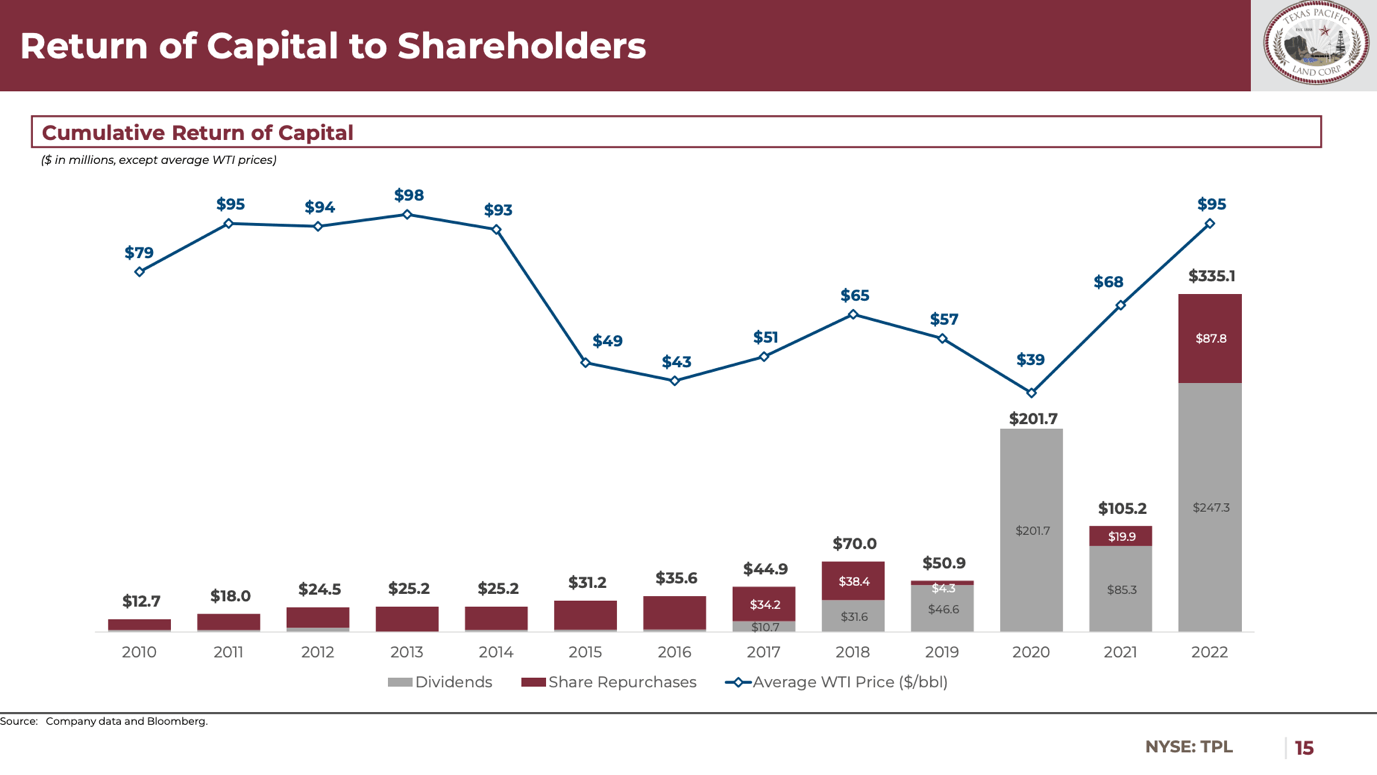

Looking at the chart below, we see that dividend investors benefit from a mix of higher production and strong WTI prices, allowing TPL to buy back stock on top of distributing dividends.

This has added to its strong total return picture.

{kind=link}

It also helps that the company has no positive net debt.

As of September 30, the company has total assets of $1.1 billion and total liabilities of just $115 million.

This is mainly accounts payable and unearned revenue.

It has no financial debt.

Even better, it has $650 million in cash!

That’s 4.8% of its market cap.

This paves the way for juicy dividends down the road, as analysts are very upbeat about its ability to generate free cash flow.

Analysts believe that TPL can generate roughly $580 million in 2024 free cash flow, followed by a surge to $680 million in 2025.

This would translate to a free cash flow yield of 4.3% and 5.0%, respectively.

When adding that the company has a significant cash position, special dividends are very likely to happen in both 2024 and 2025 – unless oil prices implode.

Speaking of oil prices, we believe that TPL will beat free cash flow estimates, as we have little doubt that we’re in a prolonged upswing for oil prices, which should benefit TPL both from a pricing and volumes point-of-view – on top of water royalties and benefits from renewables and pipelines.

“Everything still looks good. I think we still expect overall to see production growth in the coming year. Again, like we said, that really high amount of permits, the quicker turnaround of permits and DUCs, all of those things continue to be positive indicators.

And I think as some of these big pads get brought online, and we get through some of those temperature issues and pipeline constraint issues, we're going to see that production come to market to the benefit of TPL.” – TPL 3Q23 Earnings Call.

So, what about the valuation?

Valuation

The valuation is tricky, as some investors look at TPL as a REIT, which it's not.

Given that TPL does not have a reliable 5-6% yield like some REITs, investors tend to lose interest rather quickly.

After all, it takes a deeper understanding of oil fundamentals to find the value behind this ticker.

TPL is actually attractively valued, as we believe that the stock needs to be valued based on its ability to generate cash.

Hence, we're using the price-to-FCFE ratio.

FCFE is free cash flow to equity, which is the amount of cash available to shareholders after expenses, reinvestments, and debt payments.

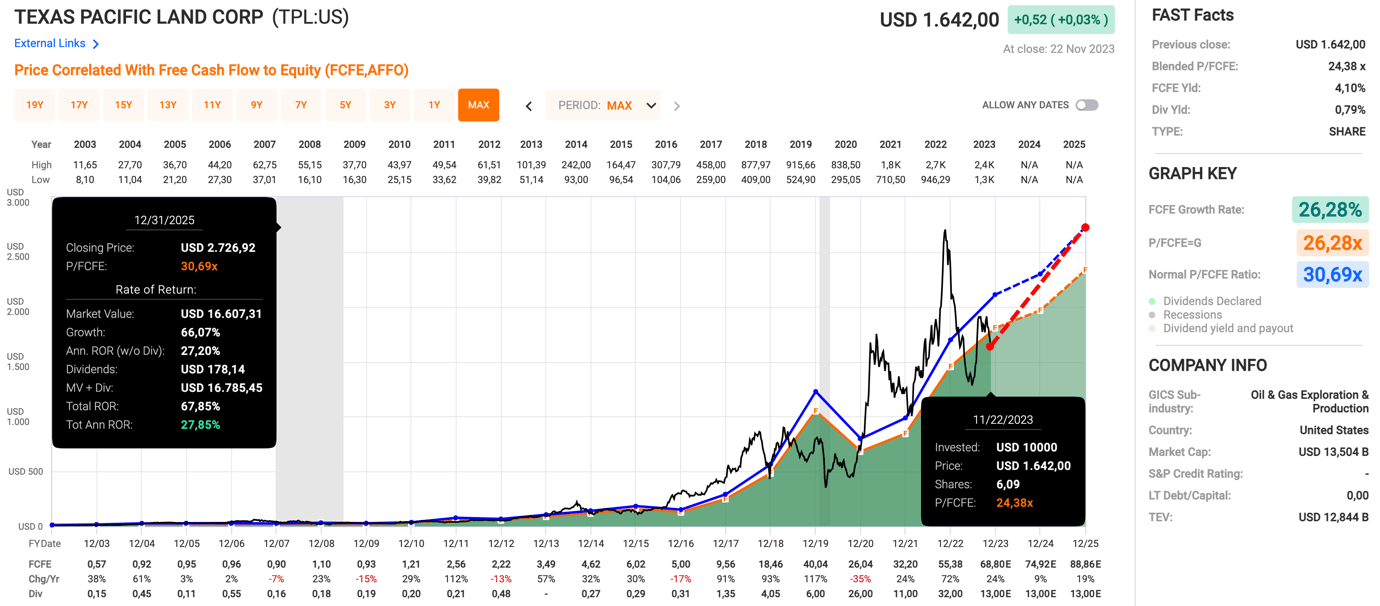

Over the past twenty years, the normalized P/FCFE ratio was 30.7x. That may be elevated. However, bear in mind that the company is showing high growth rates.

- This year, FCFE is expected to grow by 24%.

- Next year, FCFE is expected to grow by 9%, followed by 19% growth in 2025.

Although these numbers are tied to the price of oil and drilled volumes, they show the company’s potential.

Having said that, due to its poor stock price performance, TPL is trading at a blended P/FCFE ratio of 24.4x.

A return to 30.7x FCFE by incorporation of expected growth rates would imply a fair stock price of $2,730, which is 66% above the current price.

It would imply a 28% annual return through 2025.

{kind=link}

This is obviously a theoretical value subject to macroeconomic developments.

Nonetheless, TPL appears to be attractively valued.

The current consensus price target is $2,180.

Takeaway

We believe that TPL would make a great addition to your broader "real property" portfolio that includes infrastructure REITs like American Tower ( AMT ) and Digital Realty ( DLR ), as well as energy plays like Enbridge ( ENB ) and TC Energy (TRP).

Adding TPL exposure would allow you to benefit from rising production in the Permian, pricing benefits from other basins running out of steam, and add uncorrelated energy exposure.

After all, TPL is not a driller.

The only downside is that TPL is not a high-yield stock with a regular dividend.

Nonetheless, it makes up for that by being able to grow rapidly and with occasional special dividends.

Furthermore, its fortress balance sheet means it is well-protected against elevated rates.

Also, TPL has a long-standing policy to repurchase shares with excess cash. As noted in the 2015 annual report,

"As provided in Article Seventh of the Declaration of Trust, dated February 1, 1888, establishing the Trust, it will continue to be the practice of the Trustees to purchase and cancel outstanding certificates and sub-shares. These purchases are generally made in the open market and there is no arrangement, contractual or otherwise, with any person for any such purchase."

In terms of performance, TPL has been an absolute gem, and I must confess that I first heard about this pick from Porter Stansberry who touted this unknown land trust over a decade ago.

{kind=link}

Just going back over a decade, you can see that TPL has grown by 3X Nasdaq and the S&P 500.

Now, I would challenge you to find me another stock that has seen 3X performance in a 10-year period, especially a mid-cap or a larger cap company like Texas Pacific.

That trend continues even this year.

Hence, we rate TPL a Buy . We're on the hunt to buy the stock on weakness and hope to incorporate it into our portfolio over the next few quarters.

Reasons To Be Bullish TPL Stock

- Prime Real Estate Holdings: TPL owns 874,000 acres in the Permian Basin, the largest U.S. oil and gas basin, offering strategic positioning for ongoing and future developments.

- Diverse Revenue Streams: Despite not producing oil, TPL generates revenue through fixed fees, material sales, and royalties, with major customers like Occidental Petroleum, Chevron, Exxon Mobil, EOG Resources, and ConocoPhillips.

- Impressive Financial Performance: TPL's strong financials include a 40% compounding growth rate in free cash flow from 2016 to 2022, leading to a 10-year average annual total return of 47%.

- Dividend Potential: TPL pays regular and special dividends, with a total dividend of $32 in 2022, providing a total return play for investors.

- Robust Balance Sheet: The company has no financial debt, total assets of $1.1 billion, total liabilities of $115 million, and $650 million in cash, positioning it well for dividends and future growth.

- Attractive Valuation: TPL is attractively valued based on its ability to generate cash, with a blended P/FCFE ratio of 24.4x, suggesting the potential for a fair stock price of more than $2,700.

- Growth Potential: Analysts project TPL's free cash flow to reach $580 million in 2024 and $680 million in 2025, with the potential for a 28% annual return through 2025.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Texas Pacific Land: 'Buy Land, They're Not Making It Anymore'