TPL - Texas Pacific Land Corporation: The Hidden Gem Of The Energy Industry?

Summary

- In this article, we assess a very unusual energy stock, a company with an asset-light royalty-based business model.

- The Texas Pacific Land Corporation owns close to 900 thousand acres of land in the Texas Permian, allowing it to benefit from every stage of the drilling process through royalties.

- I believe that the company is a great long-term energy play. However, the current risk/reward is not attractive.

Introduction

Recently, I wrote an article titled "My Top Plays For The Energy Crisis," which generated an interesting discussion among readers regarding energy stocks and their rationales. One company that has been repeatedly mentioned by readers is the Texas Pacific Land Corporation (TPL) . While I had come across TPL in the past, I never delved into its financials and business model. However, after hearing so much about the company, I decided to take a closer look. This article is dedicated to exploring the fascinating company, which owns hundreds of thousands of acres in the Lone Star State.

I will examine TPL's business model, financials, and lofty valuation to illustrate why the company is rightfully considered an ETF play on the Texas Permian.

Texas: The Place To Be

Can you believe that I've never been to Texas? I really need to change that, as Texas has truly become one of the most important places on earth. Yes, really.

Texas isn't just a tax-friendly state that benefited from the migration from blue to red States after the pandemic, but it is also the state that satisfies the world's energy needs.

According to the EIA , the state of Texas accounted for 43% of the nation's crude oil production and 25% of its natural gas production in 2021. It has 31 petroleum refineries, processing close to six million barrels of crude per day. However, it also produced 26% of all wind power in the United States.

Moreover, the company is home to the largest LNG production and export terminals, the biggest network of pipelines, and a great mix of affordable energy (no surprise there), housing, and innovation that goes well-beyond energy benefiting cities like Houston that quickly turn into the New York of the South.

Now, with that said, the other day, I read a great article on the Texan oil industry.

{kind=link}

Three things got my attention:

- Tax revenues from oil and gas production in Texas exceeded $10 billion for the first time ever.

- The state's Permanent University Fund received $2.1 billion in taxes and royalties last year, supporting the University of Texas and Texas A&M University systems, potentially making the University of Texas the country's wealthiest endowment.

- Local school districts received $1.65 billion in property taxes from oil and gas companies, pipeline operators, and gas utilities.

Texas has never made more money from oil and gas taxes, while the University of Texas is about to overtake Harvard as the wealthiest university.

Why?

Because of land!

Owning Land As A Business Model

The University of Texas oversees 2.1 million acres in the Permian Basin, where it is leasing its land to drillers.

According to Bloomberg (August 2022):

Land operated by the University of Texas System is on track to post its best-ever annual revenue in fiscal 2022 because of soaring oil prices and production on its property in the Permian Basin. Oil reached a high of $120 a barrel earlier this year as a result of a war-induced energy crunch. The revenue is expected to help narrow the gap between the Texas system's $42.9 billion endowment and Harvard's $53.2 billion as of June 2021.

That's where the Texas Pacific Land Corporation comes in.

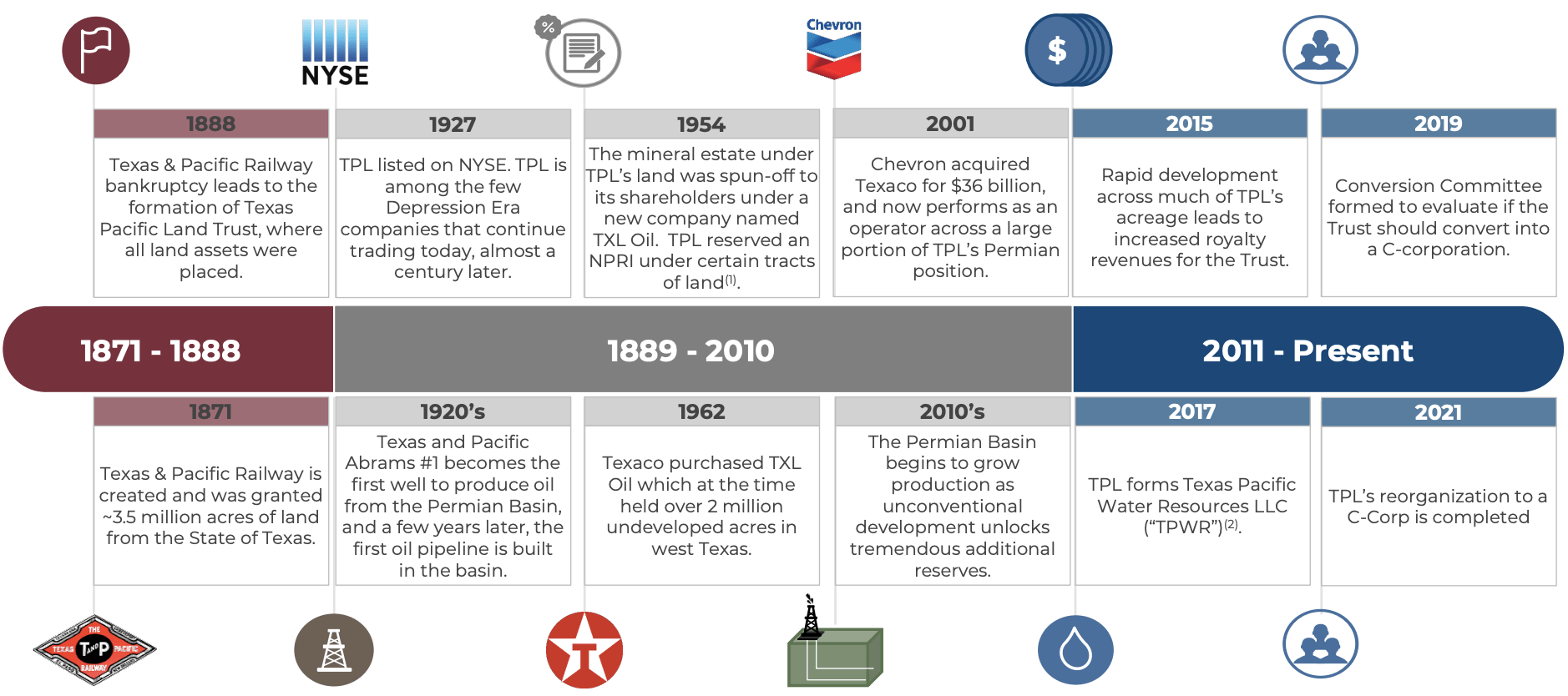

The company behind the TPL ticker is one of the few that was stock listed during the Depression Era of the 1920s. Founded in 1871, the Texas Pacific Corporation started as the Texas & Pacific Railway and was granted 3.5 million acres of land from the State of Texas.

In 1988, the railway went bankrupt, which led to the formation of the Texas Pacific Land Trust, where all assets were placed. Hence, until 2019, the company was a land trust with a different shareholder structure. In 2019, the company decided to work on a transformation into a C-corporation, which was finalized in 2021.

{kind=link}

On January 11, 2021, TPL underwent a reorganization from a trust into a corporation, which involved a series of transactions transferring all of the trust's assets, employees, liabilities, and obligations to TPL Corporation. This reorganization also resulted in the distribution of TPL Corporation's issued and outstanding shares of common stock to holders of sub-share certificates of proprietary interest, based on a one-for-one basis.

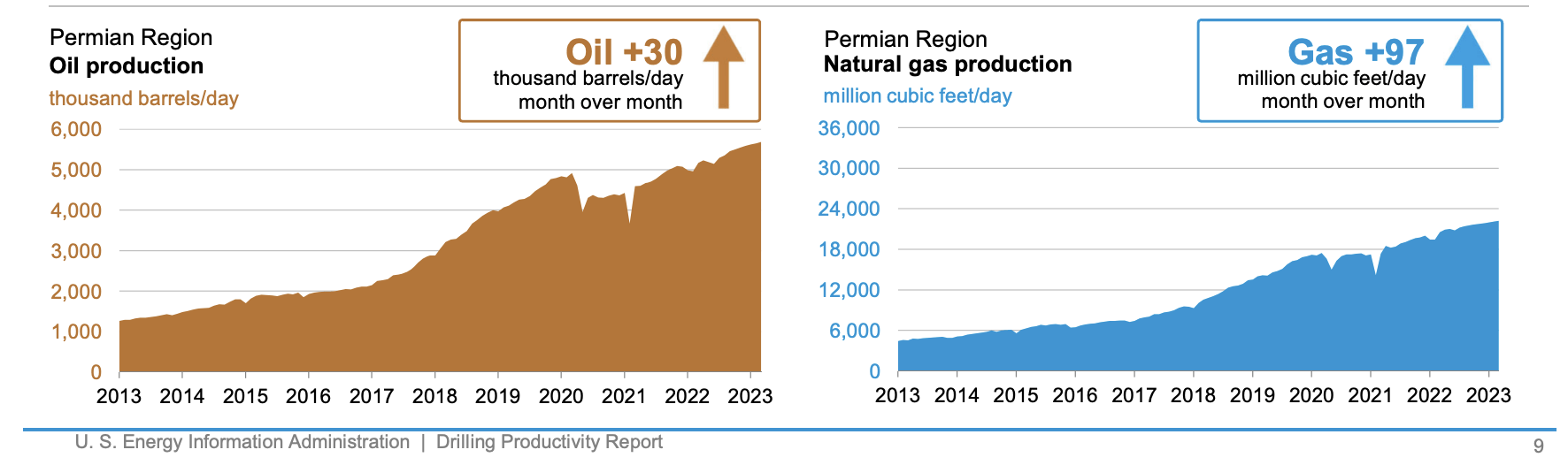

With that said, the company sees itself as "The Permian Basin ETF", as it has 100% exposure in America's fastest-growing oil basin. In 2013, in the early stages of the shale revolution, this region produced slightly more than one million barrels of oil per day. That number has now grown to close to 5.5 million barrels per day.

{kind=link}

The Texas Pacific Land Corporation owns 880 thousand surface acres in this region, with 23,700 net royalty acres.

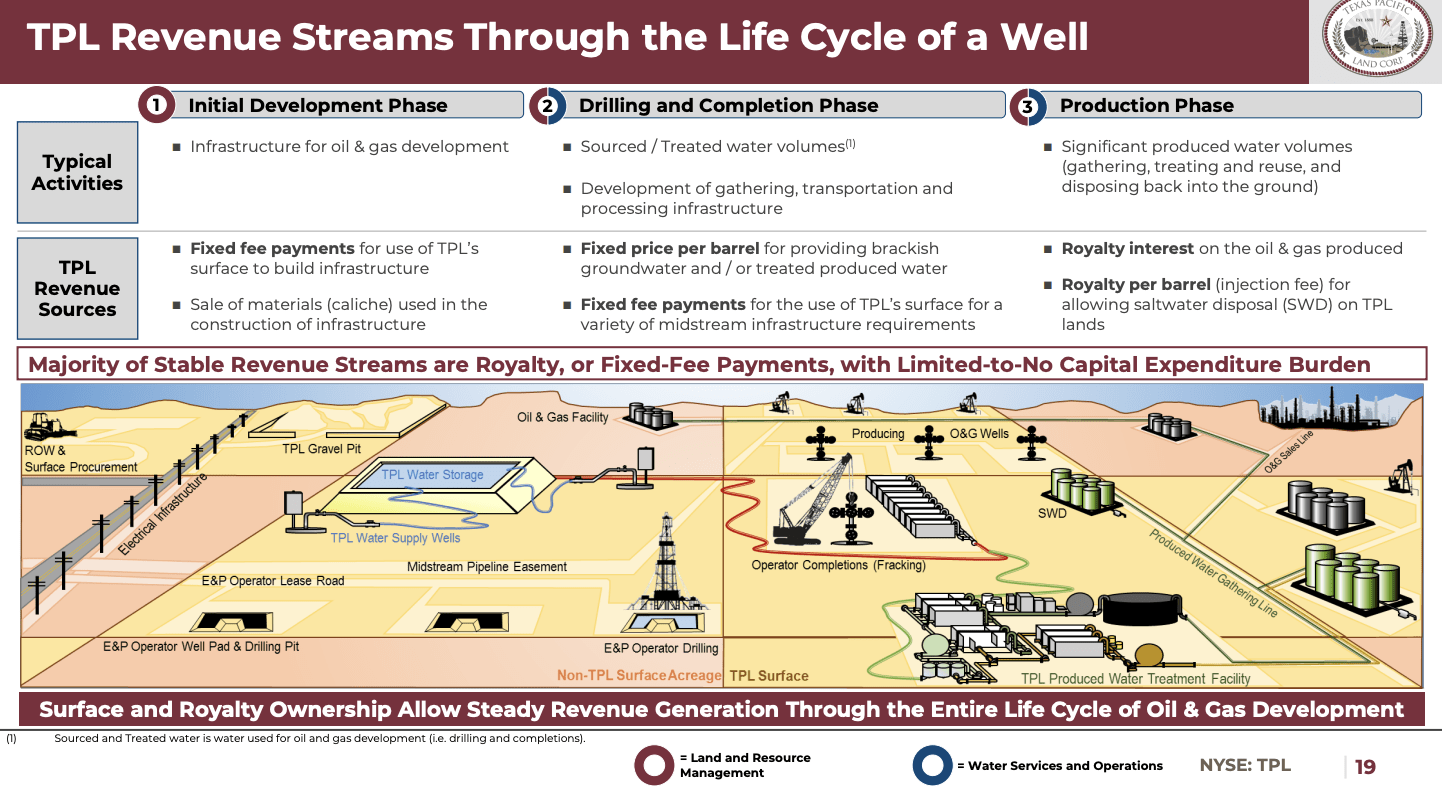

As we already established, the company does not produce oil. It is an asset-light owner of the land, which lets the company benefit from every part of the oil value chain (from planning to shipping it through pipelines):

- Receives fixed fee payments for use of their land during the initial development phase where infrastructure for oil and gas development is constructed

- Generates revenue for sales of materials used in the construction of the infrastructure, such as caliche

- Provides sourced water and/or treated produced water and receives revenue for this during the drilling and completion phase

- Receives fixed fee payments for use of their land during the drilling and completion phase

- Receives revenue from their oil and gas royalty interests during the production phase

- Receives revenues related to saltwater disposal on their land during the production phase

- Generates revenue from pipelines, power lines, utility easements, commercial leases, and seismic and temporary permits related to a variety of land uses, including midstream infrastructure projects and processing facilities as hydrocarbons are processed and transported to market.

{kind=link}

In other words, this is why the company calls itself an ETF, as it makes money in every stage of the oil value chain.

Moreover, its assets are high-quality. The company has at least 14 years' worth of inventory with breakeven prices below $40 WTI. Moreover, leases are expected to benefit from 548 DUCs, which are drilled but uncompleted wells, which do not yet produce oil.

That said, more than 60% of TPL's revenue comes from royalties. The company owns an average 4.4% revenue interest across more than 530 thousand gross royalty acres in the Permian.

The company has a well-diversified customer base with 11 companies accounting for close to 90% of net wells on TPL land. This includes Exxon Mobil ( XOM ), Occidental Petroleum ( OXY ), Devon Energy ( DVN ), and other majors like Pioneer Natural Resources ( PXD ).

Close to 10% of revenues come from SLEM (surface leases, easements, and material sales), which is income from oil and gas activities, renewables, grazing, and hunting licenses. For example, building a solar farm on TPL land or building pipelines and similar energy infrastructure benefits TPL.

The remaining revenues are generated in the company's water segment, which is essential in the production of oil as fracking is based on injecting high-pressure volumes of water, sand, and chemicals into existing wells to unlock resources.

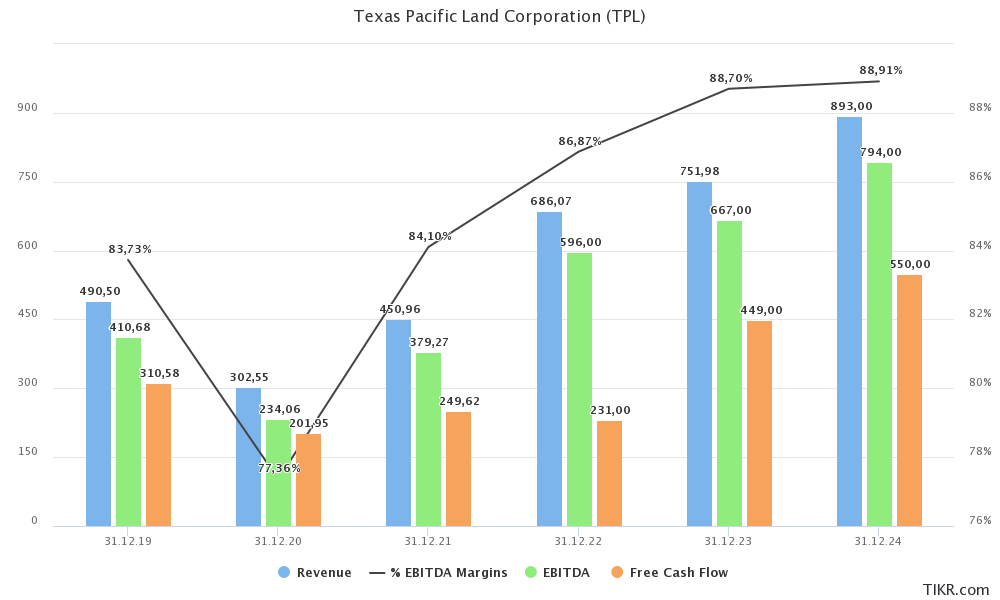

The company is doing this very successfully. In 2019, the company did $490 million in revenues, generating $410 million in EBITDA. This year, these numbers are expected to be $750 million and $670 million, respectively. Also note that EBITDA margins are consistently in the high-80% range, thanks to its asset-light model.

It also needs to be said that the company has no gross debt.

{kind=link}

Essentially, the company enhances its value without doing too much about it. All it needs is higher drilling activity, and more related activities like pipelines, fracking infrastructure, and renewables, and its revenues go up.

TPL's Shareholder Value

So far, so good. What matters now is to look into how shareholders benefit. After all, there are many ways to benefit from a strong American oil industry.

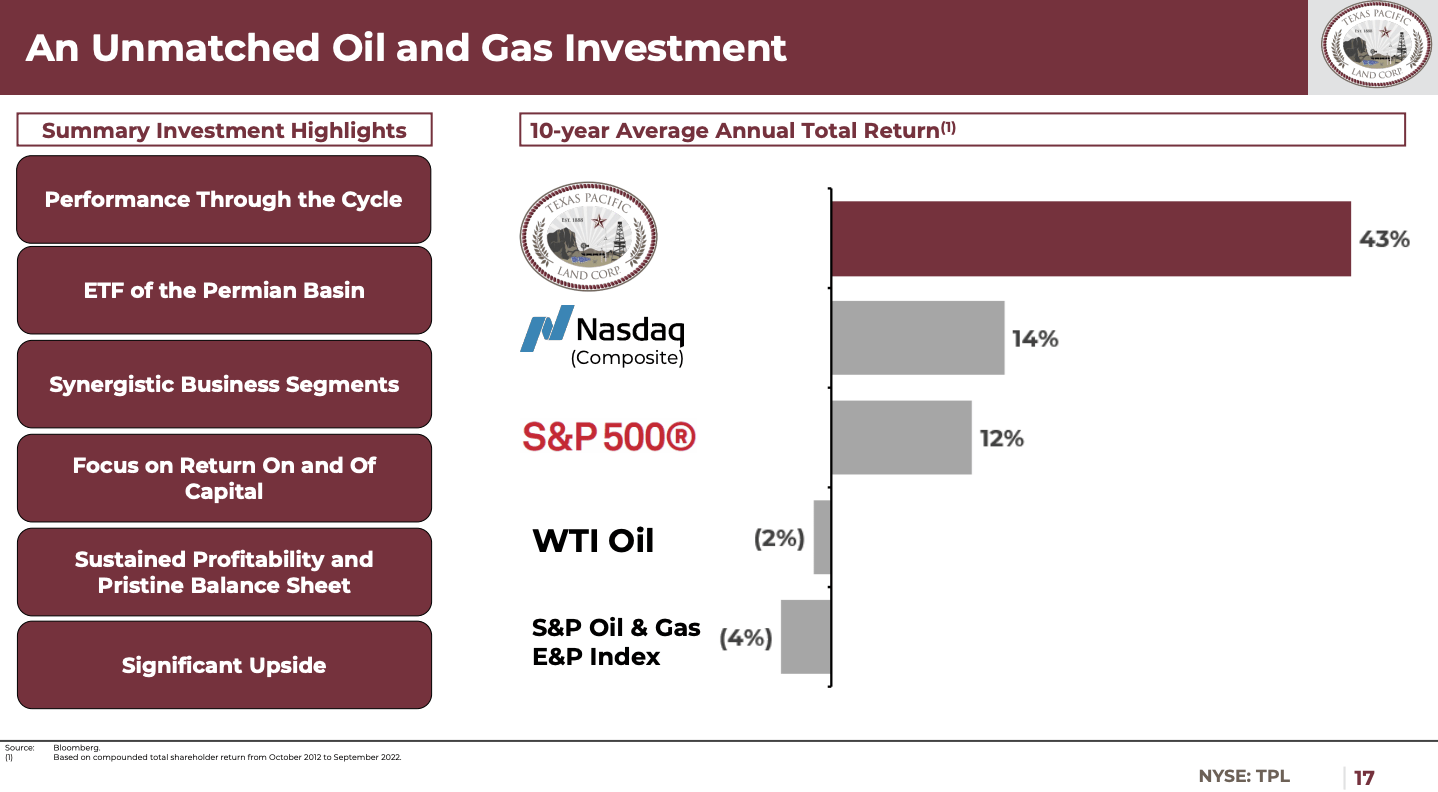

According to the company (as of September 2022), the company's stock has generated a huge return for its shareholders. The 10-year average annual total return is 43%, which beats the Nasdaq Composite by a mile.

{kind=link}

Since early 2013, TPL shares have returned close to 3,800%. I also need to mention that TPL shares are currently 30% below their all-time highs, which makes this 3,800% return even more impressive.

With all of this in mind, there are a few issues, as the risk/reward has become less attractive.

- The company's current dividend yield is 0.7%, based on a $3.25 per share per quarter dividend.

This dividend is not consistently growing and is dependent on its free cash flow. Moreover, investors seeking a high yield find plenty of alternatives on the market.

- The company's free cash flow yield isn't high. Using 2023 estimates of $450 million in free cash flow, the company achieves a 3.1% free cash flow yield. If the company were to distribute everything through dividends, the yield would be 3.1%.

- The company is trading at 30.4x 2023E EBITDA of $450 million. Historically speaking, a valuation close to 20x EBITDA is more attractive for new buyers. This number includes $1 billion in expected net cash in 2023, as high free cash flow is meeting zero in gross debt.

- The company is issuing shares. That's not the worst thing in the world. However, the company doesn't give a good reason besides that it is looking for financing tools giving it additional means to potentially grow the company in an accurate, value-enhancing way. That's vague and unusual, given that the company has no gross debt and healthy free cash flow. If the company has a major investment planned, why not tell investors? I'm not making the case that something shady is going on, but it doesn't give me confidence. Or to put it differently, if I were a shareholder, I would want to know everything. Diluting existing shareholders isn't something any company should take lightly.

On a side note, Atlas Equity Research did a great job covering these concerns in a recent article .

So, now what?

The Bottom Line

With all things being said, I think that the Texas Pacific Land Corporation is a fascinating company. The company owns land in the right region of the right state at the right time. It benefits from increased drilling activity in America's most profitable basin and everything related to these activities.

Since the start of the shale boom, shares have exploded, turning everyone lucky enough to hold shares into a very wealthy person.

The only problem I see is that the risk/reward isn't that attractive anymore. Free cash flow growth is fine, yet it's not high enough to support a high-yield dividend. Growth also isn't high enough to support the kind of total returns investors may have gotten used to.

This includes a lofty valuation and share dilution plans that aren't extremely transparent.

Investors looking for a higher yield might be better off buying low-cost drillers. Investors looking for low-yield dividend growth can find plenty of opportunities outside of the oil and gas industry.

That said, I still put the TPL ticker on my watchlist. However, I am treating it as a wild card. If the valuation falls to roughly 20x EBITDA, I might be a buyer, as I believe that the company can be a suitable dividend stock at the right price. Once that happens, I will cover the company again.

(Dis)agree? Let me know in the comments!

For further details see:

Texas Pacific Land Corporation: The Hidden Gem Of The Energy Industry?