TPL - Texas Pacific Land: Owning Dirt In The Permian

2023-11-21 23:52:22 ET

Summary

- Texas Pacific Land Trust announced net income of $105.6 million in Q3, equating to $13.74 per share.

- The company has seen substantial growth in its oil royalties business from its land holdings in the Permian Basin.

- Texas Pacific Land Trust holds a significant asset in its land holdings in the Permian Basin with effectively no liabilities and calls themselves the Permian ETF.

- The company provides a good diversified investment to fight inflation but there are potentially better ways to accomplish the same end.

Texas Pacific Land Trust ( TPL ) is a land holding company that owns land primarily in the Delaware Basin of the greater Permian Basin. The company is currently valued around $13 billion and recently announced its third quarter results where they announced net income of $105.6 million which equates to $13.74 per share.

The Texas Pacific Land Trust has a unique business model in that they do not engage in the operating activities of a traditional E&P company but rather, they focus on obtaining a profit from royalties provided by the land and mineral rights which they own. They do this by providing services to E&P companies from their land as well as royalties from mineral rights.

In this article, I rate Texas Pacific a solid hold, due to overvaluation based on cash flows and land values. Appreciating land values and increasing royalty streams may prove TPL as a buy, but unless investors view TPL as a diversification tool, I would rather own an E&P company outright rather than a land and royalty holding company.

History

The company has a rich history that dates all the way back to 1871 when the United States contracted T&P to build a transcontinental railroad. The company didn't complete the transcontinental railroad, however, they completed nearly 1,000 miles of track which entitled them to the 3.5 million acre land grant.

The railroad eventually went bankrupt, but the company protected the land by holding it in a trust. Then in 1920, the first oil well from the Permian Basin began producing. The land was owned by Texaco beginning in 1962 but when Texaco was purchased by Chevron, Chevron became the primary operator throughout Texas Pacific's oil interests.

In 2009-10, the unconventional drilling technology began to be applied to the Permian Basin, unlocking a vast amount of new reserves. Previously, the basin had been in production decline since the 1970s. Today, the Permian Basin is ground zero for oil exploration in the United States, producing some of the most attractive returns compared to anywhere in the world.

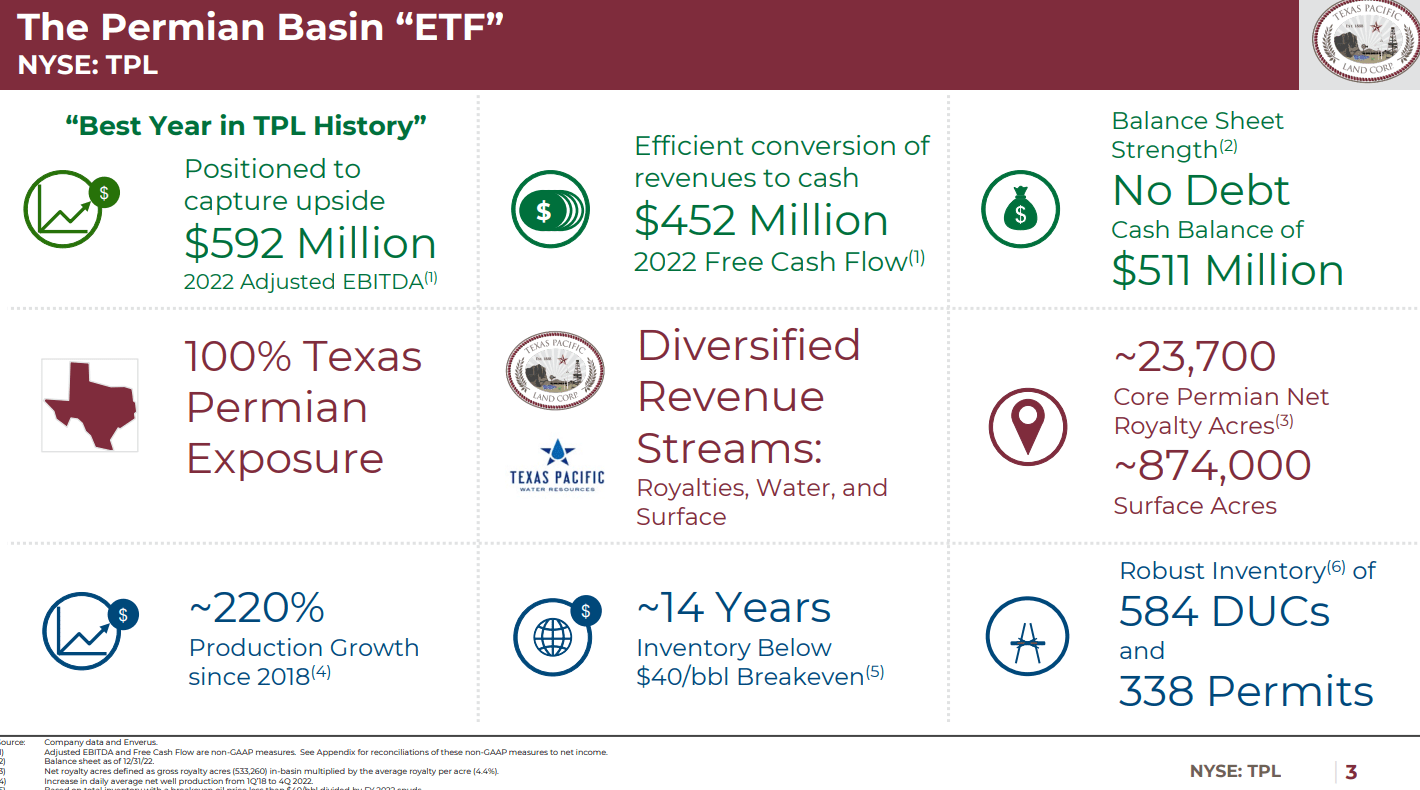

Somewhat appropriately, the company calls themselves the "Permian Basin ETF."

The Permian Basin ETF (Texas Pacific Land Trust Q2)

{kind=link}

Given the company's very stable and conservative business model, they publish one annual presentation rather than quarterly presentations. At the end of the year, they held 874,000 acres of land ownership which equated to 23,700 net royalty acres of Permian Oil Production. In the third quarter, the press release states they held slightly less acres at 868,000 acres proving again that their business is very stable.

Balance Sheet

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q3 2023 |

| Assets |

| 285.1 |

| 598.2 |

| 571.6 |

| 764.1 |

| 877.4 |

| 1,079.3 |

| Debt |

| 40.4 |

| 86.0 |

| 86.5 |

| 112.4 |

| 104.5 |

| 114.8 |

| Debt-to-Assets |

| .14 |

| .14 |

| .15 |

| .15 |

| .12 |

| .11 |

The company has no long-term debt to speak of. The debt(aka liabilities) you see on the balance sheet are deferred tax liabilities, unearned revenue, and accounts payable.

Shares Outstanding

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q3 2023 |

| Shares Outstanding |

| 7.8 |

| 7.8 |

| 7.8 |

| 7.7 |

| 7.7 |

| 7.7 |

The company's shares outstanding have remained level. Share dilution is not a concern with TPL.

Cash Flow

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q3 YTD 2023 |

| Operating Cash Flow |

| 195.4 |

| 342.8 |

| 207.0 |

| 265.2 |

| 447.1 |

| 439.4 |

| Capital Expenditure |

| (47.9) |

| (32.2) |

| (5.1) |

| (15.5) |

| (19.2) |

| (16.8) |

| Free Cash Flow |

| 147.5 |

| 310.6 |

| 201.9 |

| 249.7 |

| 427.9 |

| 422.6 |

The company's cash flow remains strong and increasing. Thus far, through Q3 of 2023, the company has had operating cash flow that is nearly equal to the 2022 full year's cash flow.

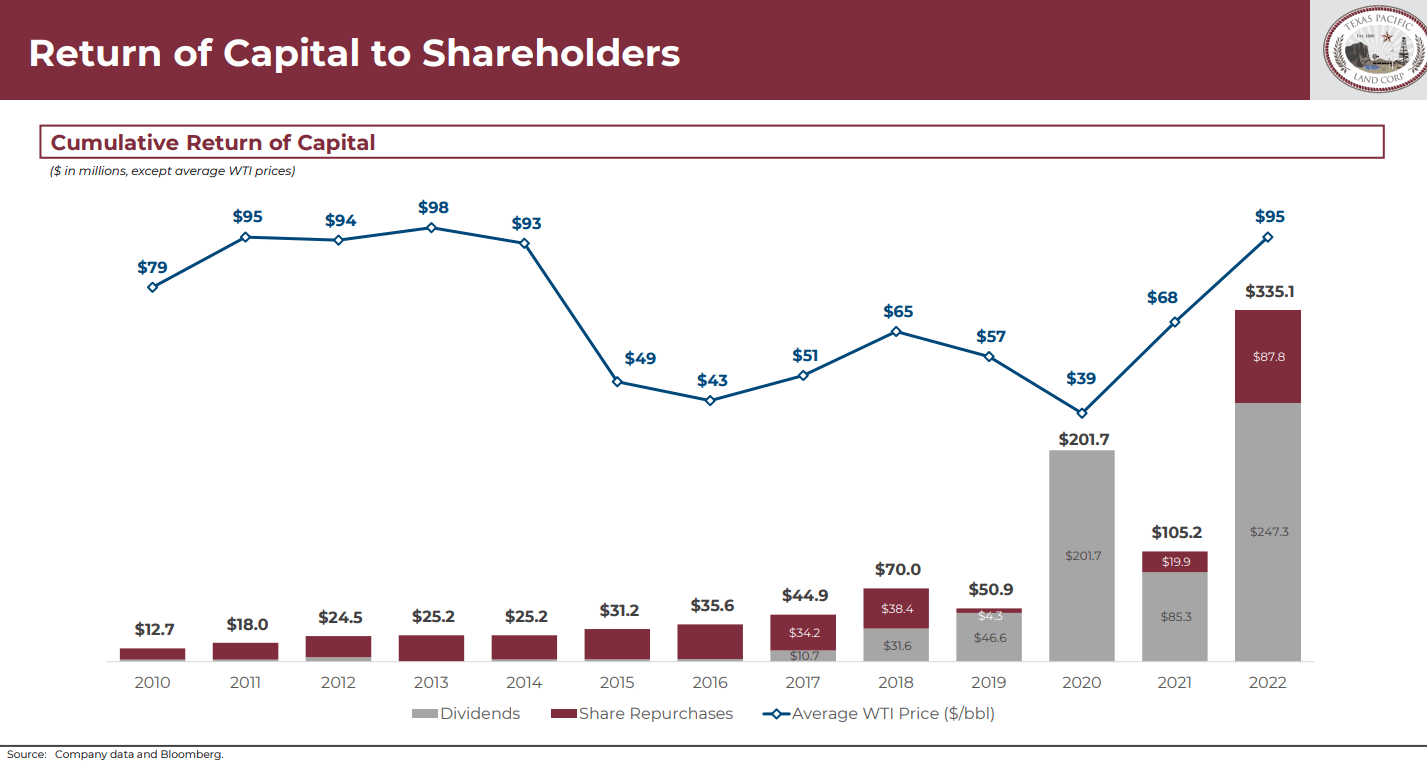

The company is focused on returning their free cash flow to shareholders. The bar chart below shows the impressive increase in cash returned to shareholders over the past decade as the Permian Basin saw unconventional development skyrocket.

Return of Capital to Shareholders (Texas Pacific Land Trust Annual Presentation)

{kind=link}

Growth Potential

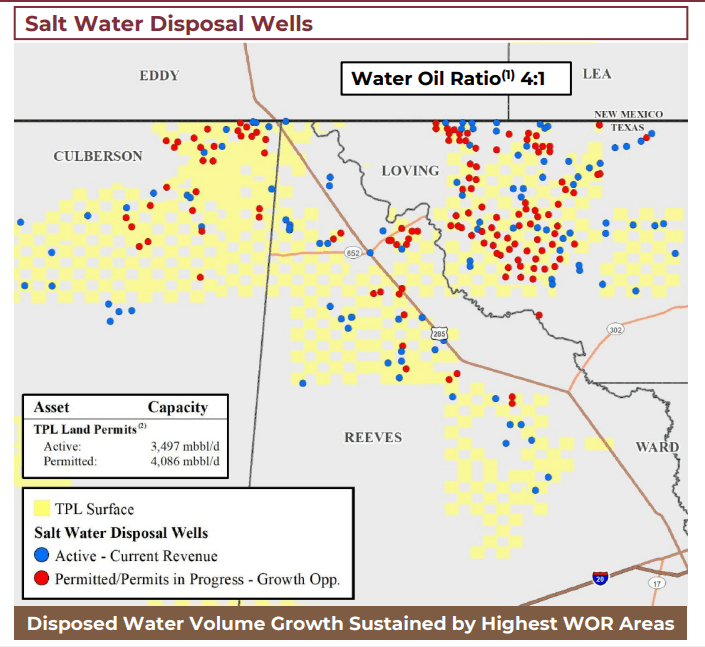

Shares of the company have grown tremendously over the past decade. So the question becomes, are investors too late to the party? Is there any growth potential left in the company? Here are some potential sources of growth. One of the company's sources of revenue comes from its salt water disposal wells. This slide demonstrates how many more salt water disposal wells the company has permitted for the future, relative to what is currently actively being used for disposal of salt water.

Salt Water Disposal Wells Active vs Permitted (Texas Pacific Land Trust Annual Presentation)

{kind=link}

The company also produces water for fracking which is another growth opportunity for the company. One can see how water royalties have increased each year for the company.

Water Royalties Over Time (Texas Pacific Land Trust Annual Presentation)

{kind=link}

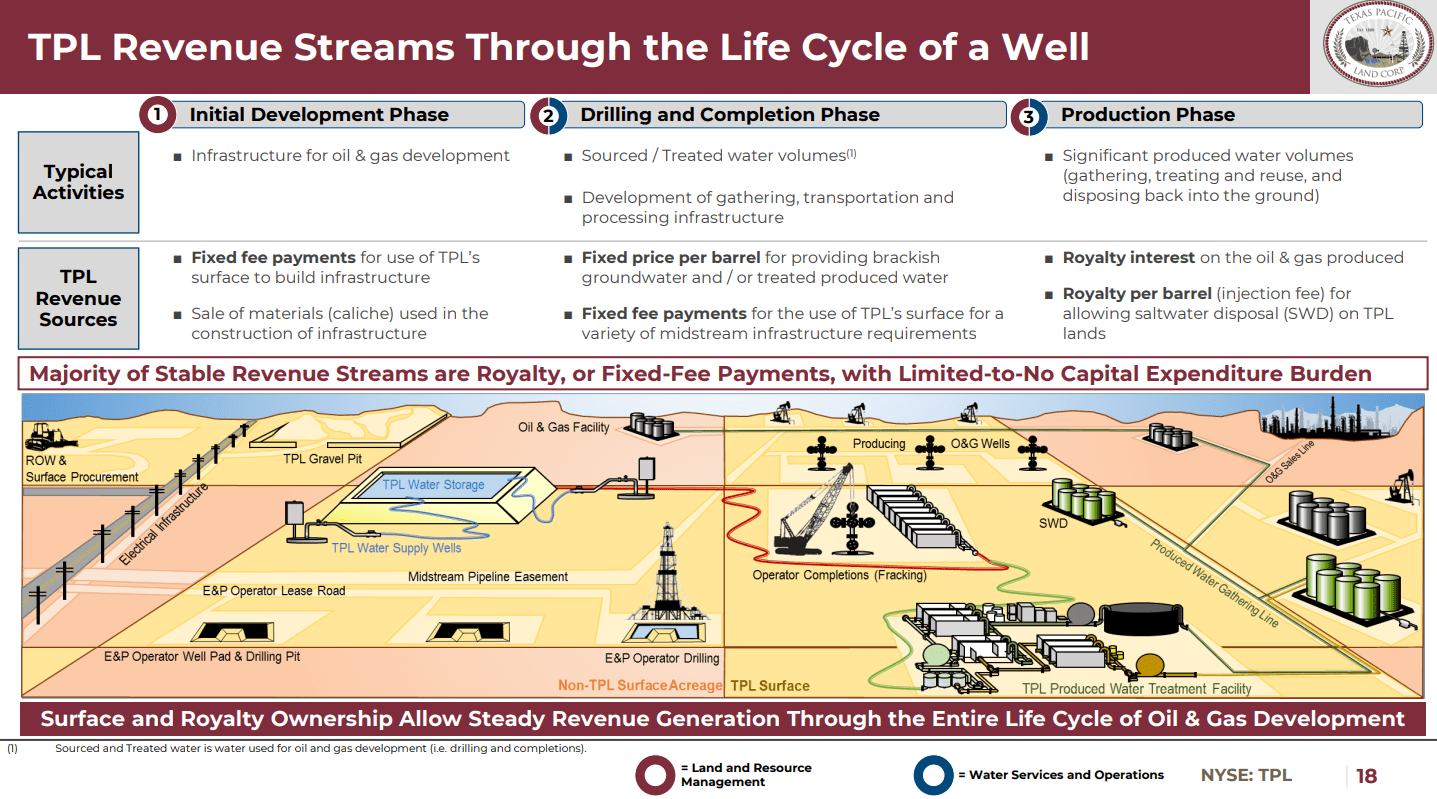

Here is a list of revenue streams that Texas Pacific Land benefits from. The graphic below provides a visual representation of the life cycle of a well to gain a better understanding.

- Fixed fees for surface infrastructure use.

- Sale of caliche for surface infrastructure. Caliche is basically the surface rock/soil that is used to build roads and well-pads.

- Sale of water per barrel they provide for completions

- Payments for easements that midstream companies obtain for their operations.

- Royalty payments for oil and gas produced.

- Royalty/variable payment for saltwater disposed in TPL saltwater disposal wells.

- The company generates revenue from other activities not related to oil such as hunting leases and other land leases as well.

Life Cycle of a Well TPL Revenue Streams (TPL Annual Presentation)

{kind=link}

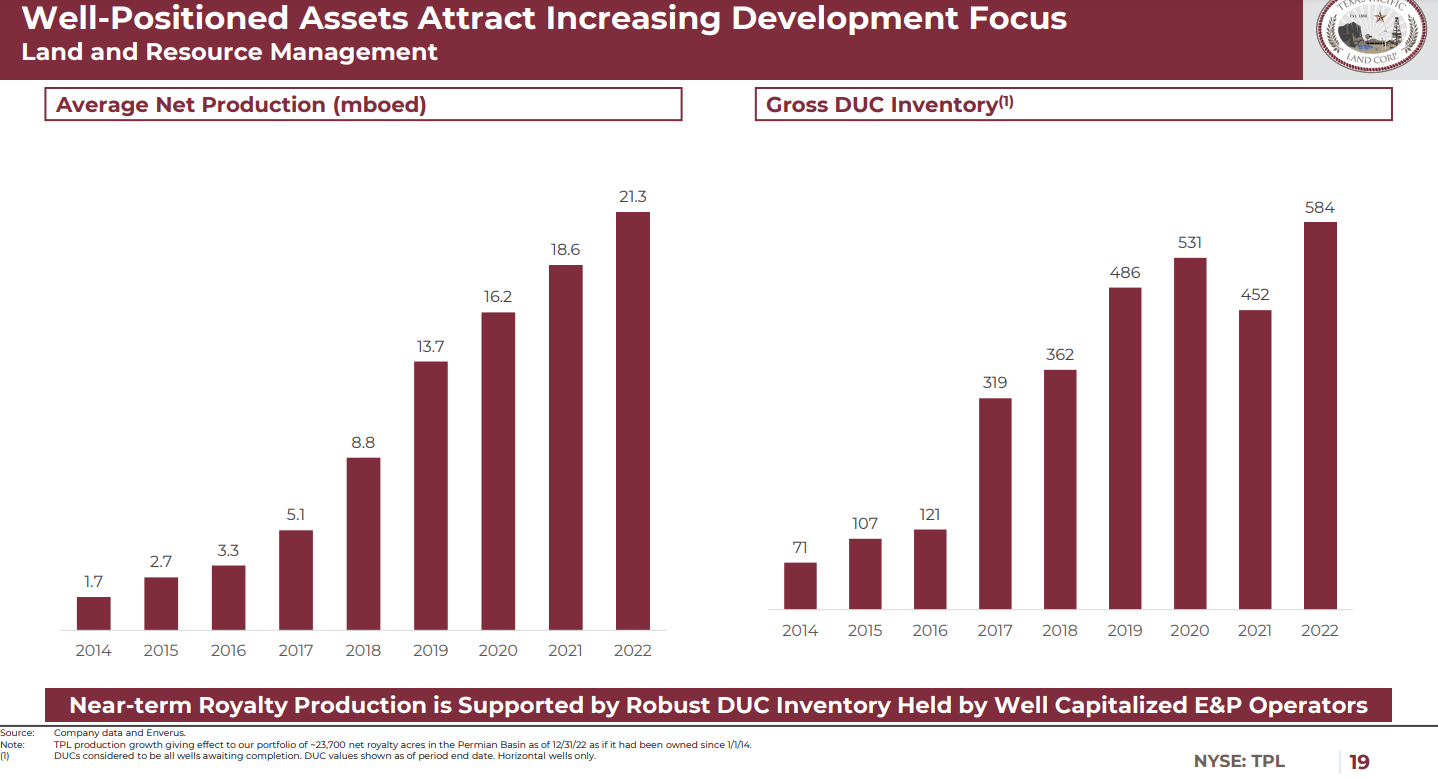

Finally, the company sees growth coming from continued increases in oil production from its oil wells. In this slide, you can see how the average net production has increased each year and it is set to increase again in 2023. That's because the company has a deep inventory of wells in the process of being completed. DUC stands for drilled-uncompleted and TPL's inventory of drill but uncompleted wells continues to grow each year. At the end of the third quarter , TPL reported that they had 50 drilling rigs working on TPL's royalty acreage and claims that "spudding" activity increased substantially from the second quarter. Spudding is a term used to describe when drilling activity for a well is started.

Drilled Well Inventory (TPL Annual Presentation)

{kind=link}

Measuring Value

How do you measure value for a company like Texas Pacific Land Trust? This is a difficult question since there are so many different sources of value. We must understand the company's revenue and cash flow projections and then on top of that, the company owns an appreciating asset in the 868,000 acres of land that they hold.

Texas Pacific Land Trust is in a similar situation to a company called MicroStrategy ( MSTR ). You might find this comparison strange, but I make it because MicroStrategy also holds a valuable, scarce and appreciating asset on its books called bitcoin. This is in addition to the company's core business of providing technology and software solutions. To make some kind of prediction of future value, yes, we can project the future value of cash flows, however, in these kinds of situations, we must also value the company's assets just as importantly as its cashflows. In the case of valuing scarce assets, understanding the value of the company's assets requires us to understand the value of the dollar, a non-scarce asset.

Value of the Land

An acre of land in the Permian Basin without royalty interests, sells for between $1,500 to $5,000 per acre depending on various factors. TPL's value of its land holdings without royalty interests equals $1,500/acre x 868,000 acres equals $1.3 billion. If each acre was valued at $5,000, then its land holdings would be worth $4.3 billion. This gives us a range of value for its land ownership. Below, I will discuss the value of the dollar to make the point that this may be a gross undervaluation of the company's land holdings. And remember, this valuation is not considering their other sources of cash flow.

Value of the Dollar

In an environment where the Federal Reserve and the US Treasury is on a path to continually devalue the dollar via money printing and endless deficits, the value of scarce assets such as land deserves a premium. How much of a premium? Let's examine this in a little more detail.

Texas Pacific Land Trust has experienced tremendous growth in share price over the course of the past decade? They've had a couple strong tailwinds in a depreciating dollar and growing oil production in the Permian Basin. Let's take a closer look at the value of the dollar and how it is decreasing. Some of you might be thinking, "what do you mean by a depreciating dollar? It has largely held its value relative to other currencies. Just look at the dollar index! ( DXY )" Yes, it is true that the dollar index has appreciated during the past few years. However, this is a misunderstanding of the dollar's value. Yes, it has appreciated relative to other currencies, but it has depreciated relative to the everyday things that people need to survive. This is the true dollar index everyone should care about.

To understand how this phenomenon is possible, you need to understand that the Federal Reserve banking system is an international banking system. The various central banks located throughout the world, behave in a coordinated manner. By coordinating things such as money supply and interest rates, the major nations of the world keep their currencies mostly stable relative to one another. Each nation uses fiat currency and so supply can be increased together at the same time and interest rates can be manipulated to reach the desired end.

However, when the dollar is measured against assets that can't be "printed out of thin air," the value of the dollar and all fiat currencies suffer significant declines in value. This includes assets such as land, oil, and yes, even bitcoin.

So to accurately value a company like Texas Pacific Land Trust, we should understand that the value of the dollar is in perpetual and likely accelerating decline. This is why a company like TPL (and MicroStrategy) receives a premium valuation, in addition to the fact that vast oil reserves sit below the ground.

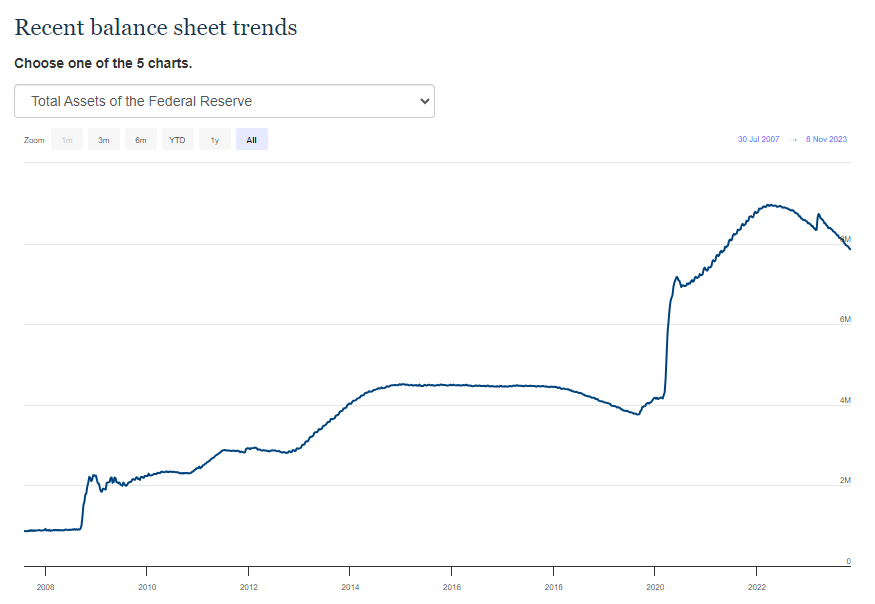

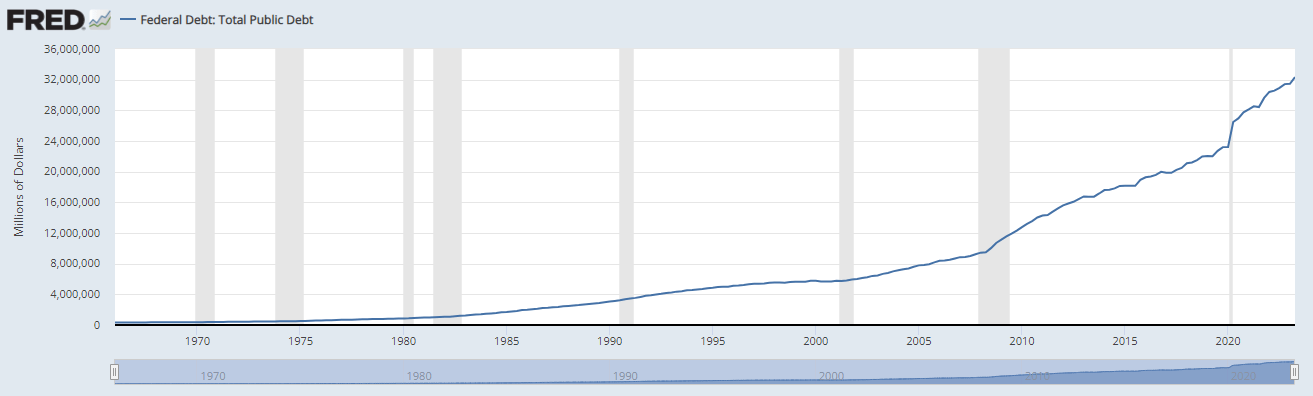

Federal Reserve Balance Sheet and US National Debt

Below I provide a visual of the Federal Reserve's Balance Sheet as well as the United States Federal Debt. Since the end of 2021, these two graphs have begun moving in different directions. Eventually, and likely very soon, the United States economic conditions will reach a point where interest rates will have increased so much, that the Federal Reserve will once again need to increase their balance sheet to purchase/monetize more of the Federal Debt than they already are. When this inflection point happens, you'll begin to see the balance sheet increase once again.

With the federal debt advancing at the rate that it is, it doesn't really matter whether or when the Federal Reserve increases the balance sheet. Either way, the US debt is debasing the currency and it will need to be paid for via inflation. That's why owning scarce assets such as land in the Permian Basin, could be an excellent strategy. This is also why it's difficult to determine how much of a premium companies like TPL should deserve.

Federal Reserve Balance Sheet (Federal Reserve Balance Sheet Trends Website)

{kind=link}

US Federal Debt (FRED Website)

{kind=link}

Value of Cash Flows

The company is on pace to report over $500 million of FCF for the full year 2023. In the present year, that cash flow is worth exactly $500 million. If we projected this cash flow out 10 years and assume cash flows will grow at a humble annual rate of 10 percent and then discounted it back to the present value with a 10 percent discount rate, this cash flow is worth about $5 billion.

I think a growth rate between 10 to 20 percent annually is probably reasonable for TPL for the next 5 to 6 years. However, this growth rate won't remain this high forever.

Risks

Owning Texas Pacific Land Trust could be a smart decision to hedge against the declining fiat currencies of the world. However, if your primary concern is hedging against inflation, then there are risks with owning stock certificates of Texas Pacific Land Trust. The biggest concern is that owning a "paper claim" to an asset is not the same as owning an asset outright. Robert Kiyosaki, the author of Rich Dad, Poor Dad is constantly pointing this out in his various podcast interviews. Kiyosaki focuses on owning land and oil wells outright and doesn't concern himself with purchasing stocks on exchanges. This article is not about outlining Mr. Kiyosaki's strategy, but I make this point simply to say one of the risks of owning Texas Pacific Land Trust is that you are only owning a paper certificate. As long as the law in America is upheld, then this isn't a bad strategy, but we are witnessing a degradation in the strength of upholding laws in America. Of course, this is a risk for owning any stock, but I wanted to highlight this since part of the allure of owning Texas Pacific Land Trust is the value of the underlying asset, the land.

Similarly, if someone was wondering if they should purchase MicroStrategy stock, I would say sure, it's not a bad strategy to hedge against a declining dollar...but it would better to hold and self-custody bitcoin outright. The same goes for someone with the means to purchase land outright. For anyone watching, we have entered an interesting period and assuming the status quo will continue may not be the only scenario to prepare and plan for.

Secondly, another risk is oil prices and Permian oil production. A decline in both of these will naturally affect the value of Texas Pacific Land Trust. As many readers know by now, that is not my expectation which is why I primarily write about oil production companies. I'm long-term bullish on oil and energy.

Conclusion

The company is seeing increasing revenue from all facets of their business. They are providing water for oil wells, salt-water disposal wells, and caliche for building roads and well pads. After all of that they are also getting revenue from granting easements, and providing leases such as hunting leases. And last but not least, they are getting revenue from oil production royalties. As they said, they are sort of like the Permian Basin ETF.

However, as we try to arrive at a value for the company, I think it is potentially overvalued. A lot of things have to go right in order to justify its value. Not only that, but I favor the alternative of owning oil company's themselves.

If you want to own land in the Permian Basin with royalty interests, there is tremendous advantages to simply purchasing TPL and holding it for the long-term time horizon. I think investors who do this have the potential to do very well into the future. And make no mistake, for investors who had the vision and bought TPL in 2010ish, and held, they have likely made some life-changing money. But in order to justify TPL's current valuation, oil royalties will need to increase, dollar debasement will need to continue, and land values will need to increase. And I believe all three of these will happen. However, I would rather own an oil company outright, rather than be the land owner that receives royalties. For those who want to own a broad piece of the Permian Basin, TPL could be a great way to invest as it leverages you to the land ownership but also the various services that TPL provides as well.

Also, if you expect land values to grow faster than the value of a barrel of oil, then TPL is definitely a better way to invest. And you may be right, however, I expect the price of a barrel of oil to grow faster than the value of land, and so I would rather invest in companies like Permian Resources ( PR ). And in a similar way, TPL will benefit from increasing land prices that derive themselves from increasing oil prices. To continue speaking out of both sides of my mouth, if you want to diversify your investments throughout the Permian Basin, then TPL could be a good long-term investment for its leverage to oil.

I am the kind of investor who likes to make more focused, targeted investments rather than spreading my investments out among many different investments. But you have to invest according to your risk tolerance and strategy, which is why TPL may make a great diversification piece to your portfolio.

For further details see:

Texas Pacific Land: Owning Dirt In The Permian