OXY - Texas Pacific Land's Management Issues Coming To An End

2023-09-22 14:33:08 ET

Summary

- The new Cooperation Agreement will allow major shareholders of Texas Pacific Land to vote freely and improve governance.

- Although two of the major promoters of the legal issues will retire soon, they haven't ceased the lawsuit.

- TPL has the best business model to gain exposure to the oil and gas markets, but I consider the stock to be overvalued with a current fair price of $1,433.

Investment Thesis

Texas Pacific Land Corporation ( TPL ) has one of those outstanding business models that doesn't need great management to be successfully run, as we realized in its more recent history. Its management issues seem to be coming to an end with the recently signed Cooperation Agreement between the company and its major investors, which is great news since legal fee spending should decrease in the next quarters.

TPL has been reducing its revenue volatility adding the Water Services segment, which has been growing at faster rates than production levels. I believe this is a really positive achievement for a company that depends so much on oil and gas prices. Even though I believe those are positive steps in improving an already high-quality business, as I will show in this article, the company is currently overvalued, unless production volumes continue to rise in the Permian Basin, which has already slowed its growth pace, or oil and gas prices increase in the next years.

Company Background

Texas Pacific Land Corporation is the successor to the Texas Pacific Land Trust, formed in 1888 upon the bankruptcy of the Texas and Pacific Railway (T&P). 3.5 million acres of land were put into a trust for the benefit of bondholders who invested in the railroad, and in 1920 oil was discovered in the Permian Basin. A few years later, the first pipeline was built and TPL was listed in the NYSE in 1927.

During the next decades, the trust's mission was to generate revenues through oil and gas royalties and land sales (75% of acres have been sold since 1888), while returning the free cash flow to owners through dividends and buybacks. From the 1970s to 2010, the production has been in decline, but since 2015 new oil and gas production technologies allowed to access reserves that were previously too expensive to extract, boosting the oil and gas activity in the Permian Basin and TPL went from producing 1.7 thousand barrels of oil equivalent per day (Mboe/d) in 2014 to 24.9 during the 2Q of 2023 . In 2017, TPL announced the formation of Texas Pacific Water Resources ((TPWR)), a wholly-owned subsidiary focused on providing water services to oil and gas operators to meet the increasing demand for water used in fracturing activities.

Currently, TPL is one of the largest landowners in the State of Texas with approximately 886,000 surface acres, mainly in the Permian Basin. The company also owns non-participating perpetual oil and gas royalty interest (“NPRI”) under approximately 460,000 acres of land.

Trial and Management

To understand the most recent legal battle between some of TPL's managers and major shareholders, we have to go back and take a look at the governance structure that was in place before the transition to a corporation. TPL's Trust was managed by three trustees, and unlike in a corporation, they were not subject to annual elections and, in effect, were appointed for life. In February 2019, one of the three trustee positions opened up because of the resignation of Mr. Meyer, who was 83 at the time and served as a Trustee since 1991 and Chairman since 2003.

The other two trustees (John R. Norris and David E. Barry) nominated the retired General Cook , a candidate with an honorable and distinguished career at the Air Force but little experience in the oil and gas sector and no skin in the game, while Horizon Kinetics LLC ((HK)), SoftVest L.P., and ART-FGT Family Partners (the "Investor Group"), who at the time owned over 24% of the trust , nominated Eric Oliver, the President of SoftVest with extensive experience on the oil and gas industry in the Permian Basin.

During the following months, the two remaining trustees and the Investors Group battled through proxy statements until in May 2019 TPL filed a lawsuit against Mr. Oliver, alleging failure to disclose background information and conflict of interests. At the time, Mr. Norris and Mr. Barry, who filled the lawsuit, had 1,300 equity securities, while Mr. Oliver held over 130,000 equity securities.

The Investor Group responded by filing a motion in court alleging Mr. Barry was not validly elected back in 2017. In July 2019, TPL and the Investor Group reached a settlement agreement in which they dismissed their litigations and included three new members on TPL's Conversion Exploration Committee formed during the year to study if the Trust should be converted into a C-Corporation. Murray Stahl (Chairman of HK) and Mr. Oliver joined the committee.

The following year TPL announced it would convert into a corporation and in June 2020 a Stockholders Agreement was signed between TPL and the Investor Group, which originated the current legal issues. Since the long-term trustees didn't want to lose their decision power and they didn't have enough shares to decide, the agreement had some odd clauses. First of all, the nine board members were designated into three groups (I, II, or III), and the class III board members could only be dismissed for cause and could still serve even if they didn't get the necessary votes from the annual general meeting.

The agreement also limited HK to owning more than 23.5% ownership in TPL (the "Horizon Cap") and SoftVest to owning over 4% (the "SoftVest Cap").

Finally, and this is the point that triggered the current lawsuit is the voting commitment, which states that the Investor Group shall vote in accordance with the Board's recommendations, with the following exception:

The Stockholders shall not be required to vote in accordance with the Board Recommendation for any proposals (i) related to an Extraordinary Transaction or (ii) related to governance, environmental or social matters.

This point is what caused important issues when in September 2022 the Preliminary Proxy Statement for the Annual Meeting was released including an unconventional proposition to increase the number of shares (Proposal 4).

This was an unconventional proposition because, since the foundation, the company has been receiving significant free cash flows and returning them to shareholders as stated before, and HK and SoftVest considered it an extraordinary transaction that changed the dynamics of the business.

Management stated that the new shares would be used for a stock split since the company was trading over $2,700, but also acquisitions. Even though management didn't disclose more information about the acquisitions, they proposed to increase the number of shares from 7.75MM to 46.53MM shares. The 3-to-1 stock split proposed only required 23.13MM shares, leaving 23.4M shares for issuance.

If those shares were to be issued at the $2,000 price that TPL was trading back in October 2022 ($666 per share after the split), it would represent over $15.42B.

I fully understand HK and SoftVest's concerns, along with many other smaller shareholders, since the management had no significant experience in acquisitions, it would dilute ownership while creating an incentive to managers with low-skin-in-the-game that plays against shareholder value creation because of management's compensation structure.

Management's compensation structure consists of a fixed base salary, a short-term incentive program based on Adjusted EBITDA margins, FCF per share, and strategic objectives, and a long-term incentive program. This compensation structure, even could looks fine at the beginning, includes many variables that are not controlled by management, since EBITDA margins are highly dependent on the price of oil and FCF per share doesn't necessarily create value for shareholders if there is no return on capital metric in place.

Half of the long-term incentive program is time-based restricted stock units with a 3-year vesting period, and the stock ownership guidelines for executive management state the CEO should own x5 of its base salary, x2 times for other named executives and x1 for other executives, which seems low to align their interests with shareholders in my opinion.

Before the meeting that was expected to be held 16th of November 2022, TPL's management tried to convince shareholders to support Proposal 4, while the biggest shareholders were announcing the days before the meeting they were voting against and encouraging other shareholders to do so.

Since it was clear that Proposal 4 was not going to succeed because of major shareholders' positions against and the most organized smaller shareholder base I have seen through the TPLBlog , the management adjourned the Annual Meeting and took legal actions against HK and SoftVest for not voting as recommended by management and not fulfilling the Stockholders Agreement.

The trial was held on April 17, 2023, and the AGM finally took place in May 2023, where votes for Proposal 4 were 37% on the AGM , even though if HK and SoftVest had voted as recommended by management, the proposition would have succeeded. Post-trial oral arguments occurred in June 2023, and no ruling has been issued yet, so the results of this proposal will depend on the Delaware court ruling.

To the surprise of TPL's shareholders, on the 1st of August TPL announced a board refreshment and a Cooperation Agreement, which might be the beginning to the end of this long management battle and reduce the cost of legal and professional fees for shareholders, which have been over $26.78MM during the 1H 2023, compared to $2.88MM the same period the year before . The legal fees have been significantly higher for HK and SoftVest, since in addition to having to pay for his defense expenses, they have been also paying part of the accusation legal fees because of their large ownership. This new agreement terminates the original Stockholders Agreement and states that the two co-chairs Mr. Barry and Mr. Norris will retire from the board and will be substituted by two new independent members (Ms. Woung-Chapman and Mr. Roosa) with extensive experience in the oil and gas industry. Mr. Stahl and Mr. Oliver will remain on the board.

Even the management hasn't ceased the lawsuit, which is the only point of the new agreement that I see concerning, in case Proposal 4 is approved, the new management board members will have to be careful not to upset HK and SoftVest, since from the 2023 AGM, which should happen before the end of the year, they will be free to vote. Since HK and SoftVest have been pushing for a long time for a reorganization of the company and aligning management interests with shareholders, I see this agreement as an important step toward better governance and value creation for shareholders.

Business Model

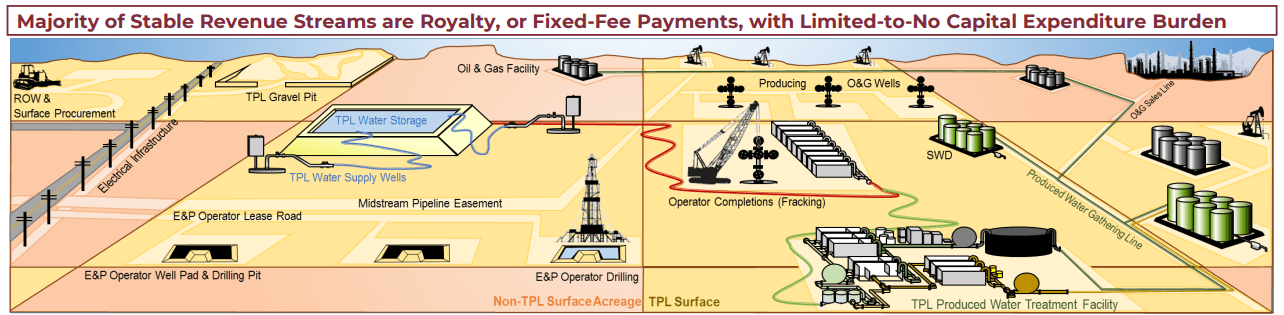

TPL's surface and royalty ownership allow it to generate revenues through the oil and gas value chain without committing large amounts of cash to an asset-intensive and highly cyclical industry. At the initial development phase where infrastructure is constructed, TPL receives fixed fee payments for the use of the land and revenue for sales of materials (Easements and surface-related revenue). During the drilling and completion phase, revenue comes from sourced or treated produced water (Water services) in addition to fixed fee payments for the use of land.

When production starts, TPL receives revenue from oil and gas royalty interests and also revenues related to saltwater disposal. In addition, the company generates revenue from pipeline, power line and utility easements, commercial leases, and temporary permits and continues to explore new opportunities related to renewable energy, environmental sustainability, and technology, among others.

TPL Investor Presentation February 2023

{kind=link}

TPL reports its revenues between the Land and Resource Management segment and the Water Services segment:

- Land and Resource Management: This business segment generated 67% of total revenue in 2Q 2023, which mainly comes from oil and gas royalties, but a smaller part comes from easements and surface-related income like pipeline infrastructure, and the sales of land. This segment has high margins with no capital requirement, but it is highly dependent on prices and production volumes of oil and natural gas. Oil represents 85% of the royalty revenues for this segment, while NGL generated 10.5% and natural gas the remaining 4.5%.

- Water Services: This segment generates revenues from produced water royalties and the sales of sourced and treated water, and while it requires higher Capex and presents lower margins as we will see later, the production levels are more stable and help reduce volatility at the same time that provide additional growth opportunities .

Before 2017, TPL allowed operators to explore for water and install their own infrastructure, and while it still generating royalties from these agreements, the management recognized an opportunity by developing water fields, providing water to operators, treating and recycling the water generated during wells competition (approximately 4 barrels of water for 1 barrel of oil).

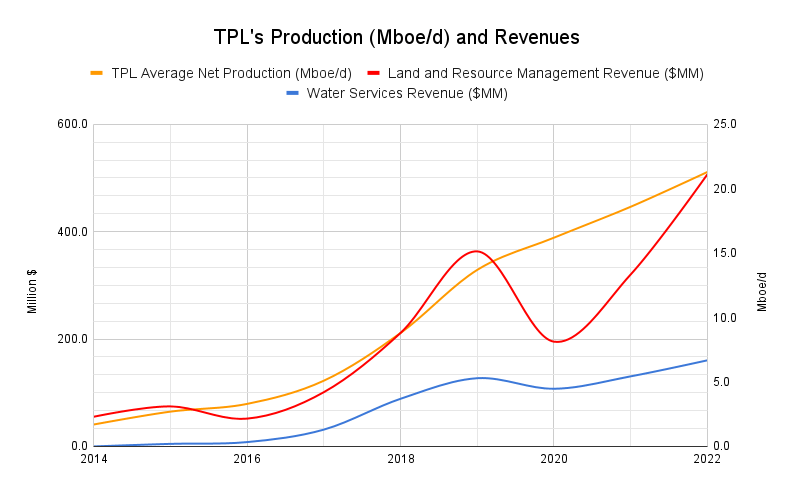

The Water Services segment represented 6% of total revenues in 2015 and currently represents over 33% of revenues and 28% of net income. From 2017 until the 2Q of 2023, TPL spent $118.3MM in Capex for this segment and generated over $747MM in revenues, with a net profit margin of slightly over 50%. In 2017, TPWR hired Robert Crain, who was the former head of water development for EOG Resources.

Author (Data from TPL Annual Reports)

{kind=link}

As we can see in the chart above, TPL's average production per day has been rising at 37.1% CAGR, which resulted in total revenues increasing at 36.6% CAGR from 2014. Oil prices haven't changed much since then, even with significant volatility along the way, since the average WTI crude oil price per barrel was $93.1 in 2014 and $92.9 in 2022. This exponential increase in production has been possible due to a significant break-even price decline for producers.

Even though revenues have been growing at a similar pace with production, there are some relevant aspects to take into account. The company has reduced its volatility thanks to TPWR. In the 31% oil price decline during 2020, Water Services revenues only declined 15%. The source of revenues has also changed significantly since TPL has reduced land sales, and easements have gone from weighting 39% of revenues in 2014 to 7% in 2022.

TPL's clients are major energy companies, and in 2022, 17.3% of revenues were from Occidental Petroleum Corporation ( OXY ), 14.2% from Chevron Corporation ( CVX ), and 10.2% from ConocoPhillips ( COP ). The company only employed 99 full-time people in 2022, of which 29 work in Water Services, and has strong FCF margins (66.5% LTM) and ROIC of over 100%.

Until 2017, TPL returned an average of over 80% of its FCF to certificate holders through repurchases and small dividends. But from 2018, the company increased the return of capital to shareholders through dividends, and while they usually represented 7% of the capital returned, in 2022, 77% of capital returned to shareholders was through dividends.

The company already bought 17,802 shares for $26.2MM during the 1H 2023 and still has available $223MM under the repurchase program (1.63% of outstanding shares). Even though I like the fact that TPL found a good use for capital in the water segment, I would prefer the company to continue with share buybacks instead of dividends, since it would benefit long-term shareholders to compound at a higher rate and avoid being taxed along the way.

Oil and Gas Market

Making predictions on the oil and gas market is always difficult because of the high amount of variables that can affect price and production, not to mention black swans. However, to value the expected growth of TPL, we will look at the available data to make some long-term assumptions.

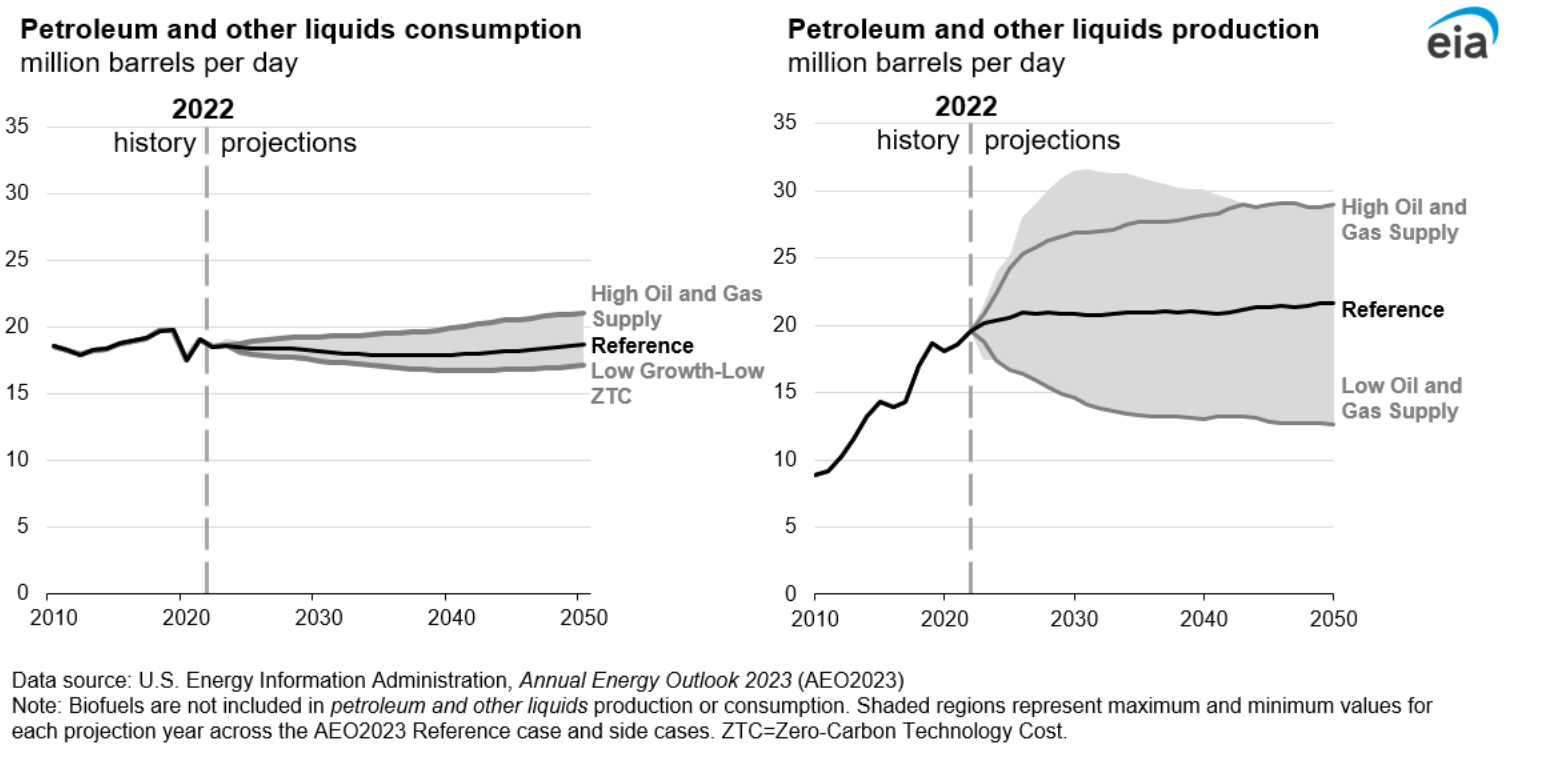

In the long term, even though renewable energies will grow at a fast pace and are going to take share from other sources, petroleum, and natural gas consumption are not expected to diminish for the next decades.

U.S. Energy Information Administration (EIA)

{kind=link}

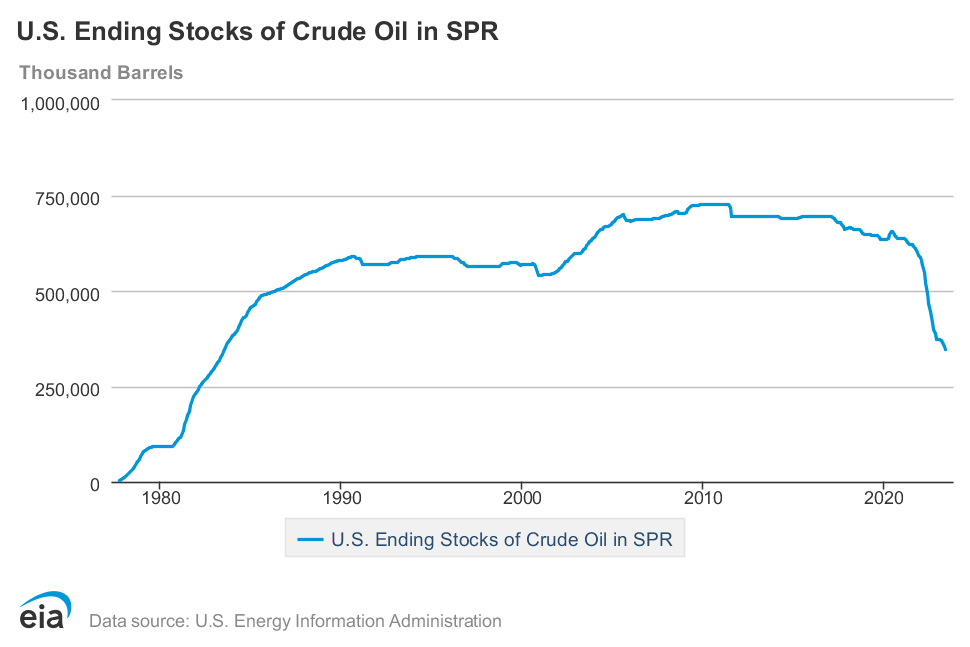

Even though the share of oil in the transportation sector will reduce during the next decades, there are many other sectors where it could be needed, like plastics, medical supplies, electronics, and even textiles, so I expect it will be a valuable commodity for a long time. In the most recent period of time, during 2022 oil prices were at their high range due to the continued oil supply cuts by OPEC+, Russia's attack on Ukraine, and strong demand. To help mitigate inflationary pressures, the United States released millions of barrels of crude oil from its Strategic Petroleum Reserve.

U.S. Energy Information Administration (EIA)

{kind=link}

The U.S. government has been able to reduce temporarily oil prices, but the reserves haven't been at current levels since the mid-'80s, and they are not going to be able to continue this policy for a long period of time. In addition, Saudi Arabia announced on the 5th of September they will extend its voluntary 1 million barrel per day (b/d) production cut through the end of this year and the EIA expects Brent crude oil spot price to average $93 per barrel in 4Q 2023, and $88 per barrel in 2024.

During the 2Q of 2023, the activity in the Permian Basin, where TPL operates, has remained robust, which confirms that we can expect similar or growing production levels in the near term since drilled but uncompleted wells ((DUC)), which in 91% of cases are completed within 12 months, have increased from 584 at the end of 2022 to the current 593.

The major risk for TPL would be a decline in oil prices and a reduction in demand because of an economic recession and lower production levels. In that particular case, production would be postponed until prices make it worthwhile for operators to drill, but even if it would be negative in the short time, it would expand the years of inventory for TPL.

Expected Growth

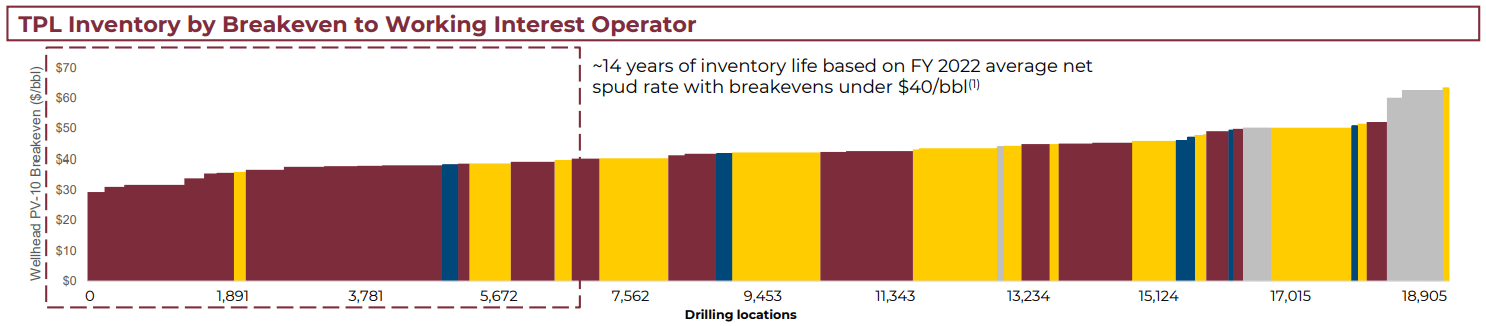

At current levels of production, TPL has an inventory level of 14 years at a breakeven price under $40/bbl, but it more than doubles if we raise the breakeven price to $50/bbl if more drilling locations are started in the Midland Basin, where production costs are higher. This is without accounting for any new technological developments, which seems conservative to me for such a long period of time.

TPL Investor Presentation February 2023

{kind=link}

To model TPL's fair value, in my base case scenario, I am assuming production continues at current levels in line with the EIA expectations, and price averages $88/bbl in 2024 and grows at 3% annually, in line with a consensus forecast made by the EIA, Shell ( SHEL ), Eni ( E ), and BP ( BP ).

The water segment has been growing at a significantly faster pace than TPL's total revenues and production, and even with the decline in oil prices in the last twelve months, it has managed to grow 38% YoY (25% production growth YoY). I expect it to continue growing at least 15% annually for the next 5 years, easements to grow at 3%, and no land sales.

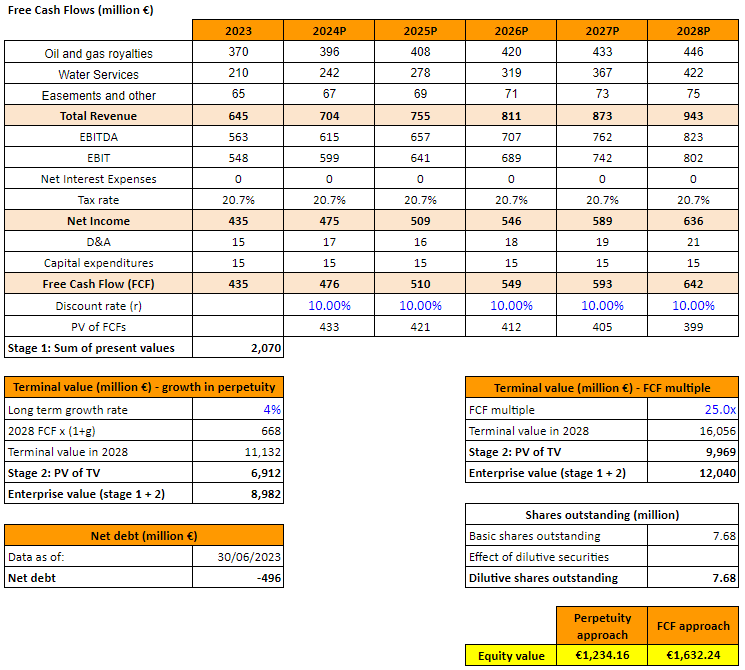

Using a DCF model with a 10% discount rate, the average fair price between a perpetuity approach and an FCF multiple approach is $1,433.

{kind=link}

When modeling future cash flows for the next 14 years, reducing water segment growth to inflation, the sum of FCF available to shareholders would be $9.5B, with a present value of $4.7B at a 10% discount rate and we would have to add the value the company can get for its 886,000 acres of land. This assumption I believe is conservative, since TPL can continue producing after the 14th year if oil prices make it worthwhile for operators, which would increase oil and gas royalties even if production doesn't increase. TPL is also exploring new opportunities in renewables, grid-connected batteries, and studies on carbon capture.

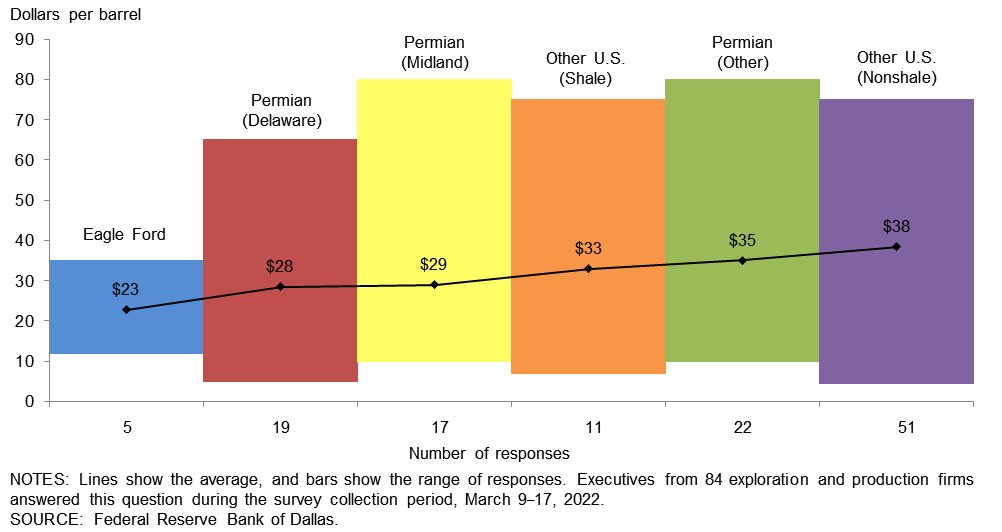

The assumption that production doesn't grow I believe is conservative, since as we highlighted before, the production in the Permian Basin has been booming over the last years and it continued growing in 2Q 2023. The land owner by TPL has one of the lowest breakeven prices in the U.S., so it would make sense if it continues at current levels or higher for the upcoming years.

Federal Reserve Bank of Dallas

{kind=link}

Valuation

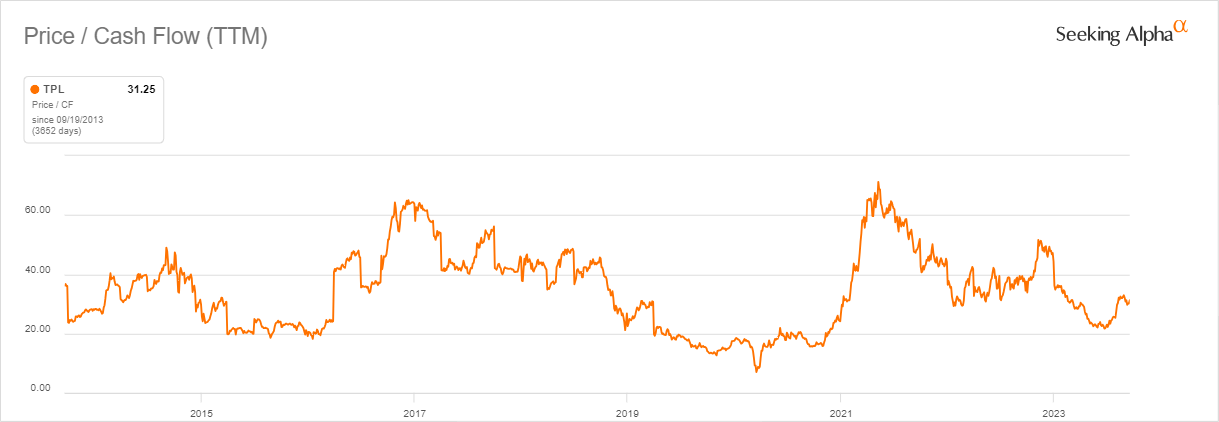

When valuing TPL assuming production doesn't grow in the following years and with a 25x FCF, the stock seems about 25% overvalued, but I believe this are conservative assumption given the current data available. At current prices, the market is expecting TPL's FCF to grow at 13% in the next years or a higher multiple (28x LTM FCF) that I used in my model.

{kind=link}

TPL has been trading at an average of 35x LTM FCF for the last 10 years, but I expect the valuation to decrease since production has already been growing at a slower pace since 2020 and higher long-term interest rates should push valuation lower.

Author (Data from TPL Annual Report)

In my base case scenario, I consider TPL to be overvalued, and even if I consider it a high-quality business and one of the best companies to get exposure to the oil and gas market without the risk of debt and large capex, I am not willing to pay the current premium, but I believe there is value under the $1400 price per share.

Risks

The major risks for TPL would be a decline in production or oil and gas prices. As we have previously explained, production is expected to remain at current levels over the long term, and given the quality of TPL's land and the fact the company is not using debt, even in a recessionary environment, it would perform better than many other oil and gas companies.

From the lawsuit perspective and the pending ruling from the Delaware Court, even if it decides to rule in favor of TPL, HK and SoftVest could appeal the decision. In case it rules against TPL, I don't expect the company to appeal and continue spending shareholders' money on that matter, since two of the main precursors of this lawsuit will leave the board soon, maybe earlier than the court's decision.

Conclusions

All in all, I believe over the long term TPL's shareholders can find value in holding such an outstanding business and gain exposure to the oil and gas market with lower volatility and risks compared to other players. As we recently saw, this is one of these business models that doesn't need to be run by outstanding management to be successful.

The recent Cooperation Agreement looks like the beginning of the end for management issues and even though it took some time, TPL is going in the direction that HK, SoftVest the majority of its shareholders want, based on the votes recorded at the last AGM.

Even though I recognize TPL's competitive advantage thanks to its premium land with lower extraction costs, I am not willing to pay any price. The market is pricing growing production levels or higher oil prices, which could make sense given the low levels at the U.S. Strategic Petroleum Reserve and Saudi Arabia's production cuts in place.

In conclusion, I would like to have some margin of safety and find the company to be overvalued at current prices compared to my fair price of $1,433 per share, assigning it a hold rating.

For further details see:

Texas Pacific Land's Management Issues Coming To An End