TPL - Texas Pacific Land: Still Expensive And With Principal-Agent Problems

Summary

- Even after the recent correction, the spread between TPL’s earnings yield and the 2-year US treasury remains negative.

- The company is in the process of suing some of its investors.

- The correction may not be over, given the rising rates environment.

Back in November, I covered Texas Pacific Land Corporation ( TPL ) and expressed an opinion that the company is overdue a correction. Now that the share price has fallen roughly 20% since then, it's time to take a second look at the company. It appears that the correction was not enough to lift the earnings yield above the 2-year Treasury rate, and the spread between the two remains negative - well below historical averages. In addition, there seem to be corporate governance issues with the company as management is suing a group of investors. In light of these reasons, I remain bearish for the stock.

Brief company overview

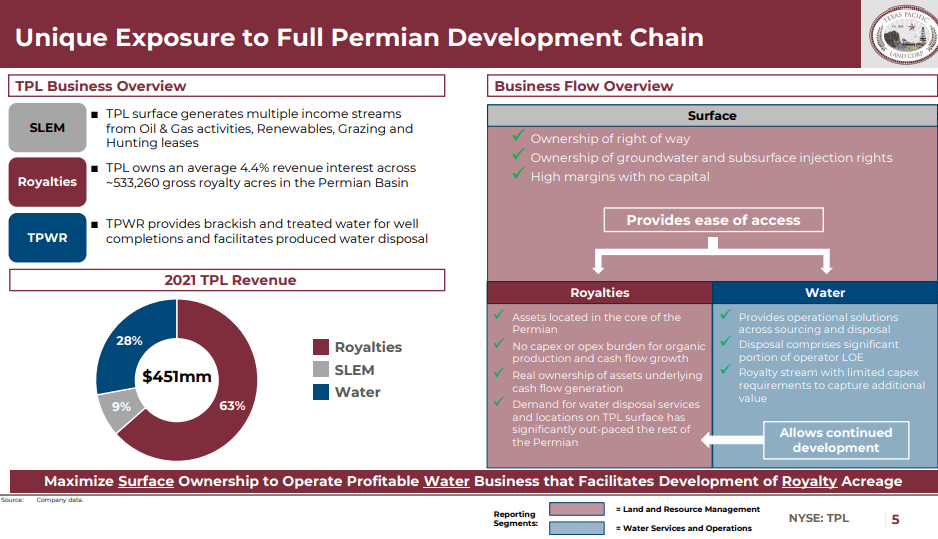

Business Overview ((TPL))

{kind=link}

In my last article about TPL, I covered the business at more length, so more information regarding that could be found there. But in short, TPL is a large land owner (more than 880k acres) in Texas. As such, the company makes its revenues from oil and gas royalties and water services. The fossil fuels segment is the primary source of revenue.

The valuation picture

The royalty business model is generally considered very low risk, which in the case of TPL would justify much higher multiples than an oil & gas producer. Also, TPL is quite unique and there are no good matches to be compared with, as it owns much more still undeveloped land than a typical royalty company. Despite the low risk of the company, it's quite hard to consider it less risky than a 2-year government bond so I think it should offer higher earnings yield than that. Such a comparison could be justified, given that TPL could hardly be considered a growth company, which expects an exponential growth in revenue. For these reasons, I decided to look at the spread between the TPL's earning yield and the yield on the 2-year US treasury in a 10-year historical period.

It appears that the spread is negative, indicating that the 2-year US treasury offers 1.24% more yield than TPL. Historically, it was the other way around, with the treasury yielding 1-2 p.p. less than the company's earnings yield. In light of this, the upside looks very limited. Instead, I expect some mean reversion, with the spread going to a positive territory again.

Corporate governance issues

Besides the very low earnings yield of the company, there seem to be corporate governance issues as well. Recently, the 2022 annual shareholder meeting, which was to be held on 14 February was adjourned for 18 May. The reason is the pending court case against a group of large institutional shareholders. At the root of the lawsuit is the fact that they submitted a proxy vote against a proposal, which was giving the green light to management to raise substantial amounts of capital through stock offerings. On this issue, TPL's management believes that:

the Investor Group is required to vote for the Share Authorization Proposal pursuant to the voting commitments in their stockholders' agreement with the Company.

At the same time, it's quite surprising for a company like TPL with a debt-free balance sheet and US$446.6M cash position to seek permission to raise capital without giving a compelling reason why. In the Q3'22 earnings call, when asked about it, the CEO responded :

a share authorization just provides a normal course financing tool and gives us additional means to potentially grow the company in an accretive, value-enhancing way.

However, many shareholders are most likely worrying about potential dilution with unclear effects on the enterprise value.

This pending court case is just the latest example of deteriorating principal-agent relationship in the company. Previously, there was a campaign by some shareholders to declassify the board structure of the company, making the change of directors easier.

Conclusion

Despite the recent pullback, I still consider TPL as overvalued as its earnings yield is substantially lower than the yield on the 2-year US treasury. On top of that, I think there are corporate governance issues as management is suing a group of shareholders over their refusal to approve a share issuance authorization.

For further details see:

Texas Pacific Land: Still Expensive And With Principal-Agent Problems