TGH - Textainer Group Holdings: I Own The 7%+ Yielding Preferred Shares

2023-04-15 11:45:00 ET

Summary

- Textainer Group Holdings is one of the largest container lessors with a fleet of in excess of 4.5 million container-equivalent units.

- Thanks to a 6+ year remaining average lease term, the cash flows should be reliable and provide good visibility.

- I own the preferred shares for an additional layer of safety. There's $1.7B in equity ranked junior to the preferred shares.

Introduction

Textainer Group Holdings (TGH) is one of the largest container lessors in the world, and as most of its lease agreements have multi-year terms, the earnings visibility is pretty good. The average remaining lease tenor is approximately 6 years which means Textainer has a pretty good idea of the cash flows coming in over the next decade or so. And unless some of its lessees are going bankrupt, I am confident in Textainer's ability to manage the current fleet .

The dividend and asset coverage levels of the preferred shares still looks good

2022 was a year of consolidation. After massively expanding its asset base in 2021 (when Textainer's fleet grew from just over 4 million container-equivalent units to in excess of 4.5 million units ), the growth rate was much slower as Textainer took delivery of some pre-ordered containers to end the year with 4.58 million container-equivalent units.

{kind=link}

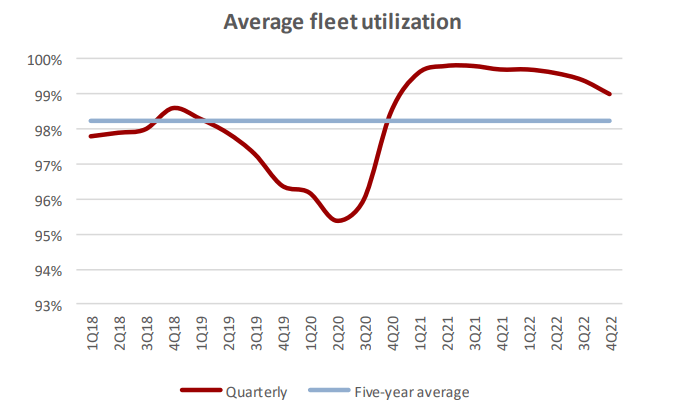

Although the massive demand spike we saw in 2020 and 2021 has died down, it's important to know the majority of Textainer's assets are on long-term leases with the lessees. The utilization rate of the containers remained very close to 100% in 2022 and that's ultimately what counts. The high utilization rate was not fueled by lower lease rates: in its annual report, Textainer confirmed it was able to increase the lease rate of its operating leases by 3.2% in 2022.

{kind=link}

As I'm mainly interested in Textainer's preferred shares, I wanted to make sure the company's asset coverage level and dividend coverage level remain strong.

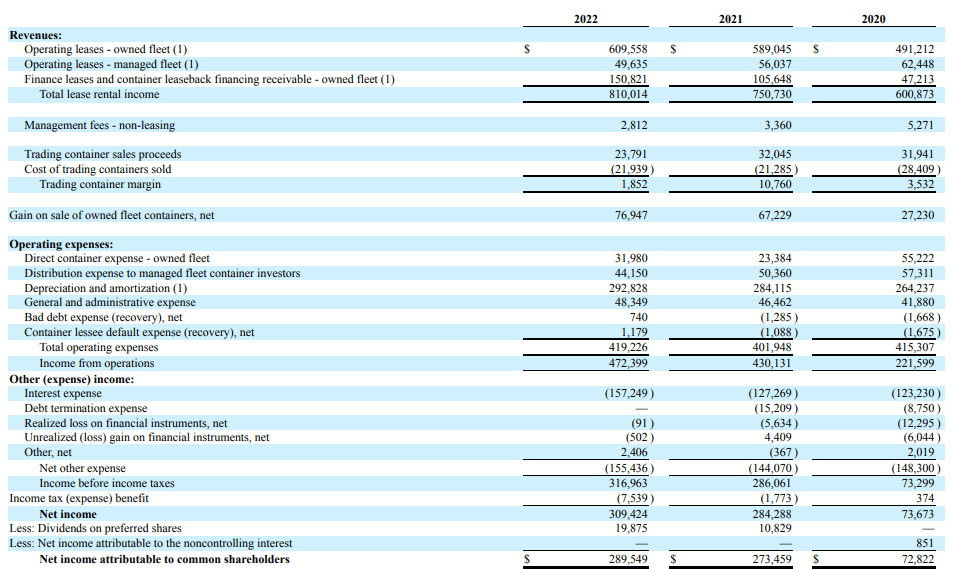

Starting with the latter, we see the company reported a total revenue of $810M, which resulted in a $472M operating income after deducting all the relevant operating expenses. As you can see in the image below, approximately 70% of all the operating expenses are related to the depreciation expenses.

{kind=link}

The cost of debt is another important factor as Textainer clearly saw its net interest expense increase in 2022. The total interest bill increased by about $30M but this was still sufficient to post a higher-pre-tax income and net income. The latter came in at just under $310M. After deducting the almost $20M in preferred dividends, the net income attributable to the shareholders of Textainer was just under $290M.

Not only does this mean the stock is indeed trading at just around 5 times the 2022 earnings result, it also means Textainer only needed about 6.5% of its net income to cover the preferred dividends. This means the preferred dividend coverage ratio exceeded 1,500%. While that is great, keep in mind I expect the interest expenses to increase in 2023. The Q4 interest expenses incurred by Textainer were approximately $43M which means that on an annualized basis, we should expect the net interest expenses to increase this year. And although this will weigh on the reported net income, there's very little doubt the preferred dividends are safe based on the current situation.

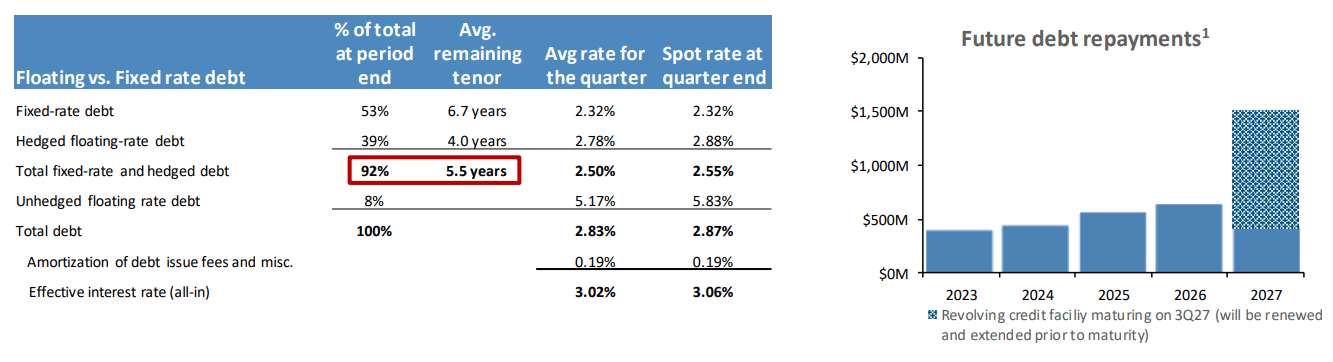

While the total debt of $5.54B (and net debt of approximately $5.4B) may sound high, especially compared to the $7.6B balance sheet, keep in mind a large portion of the debt consists of asset-backed securities .

Textainer Investor Relations

The majority of the debt either has a fixed interest rate or the interest risk has been hedged. And as you can see below, the debt repayment schedule will allow Textainer to gradually refinance existing debt. Over the past three years, Textainer generated on average close to $170M per year by selling old containers that have reached the end of their useful lives.

{kind=link}

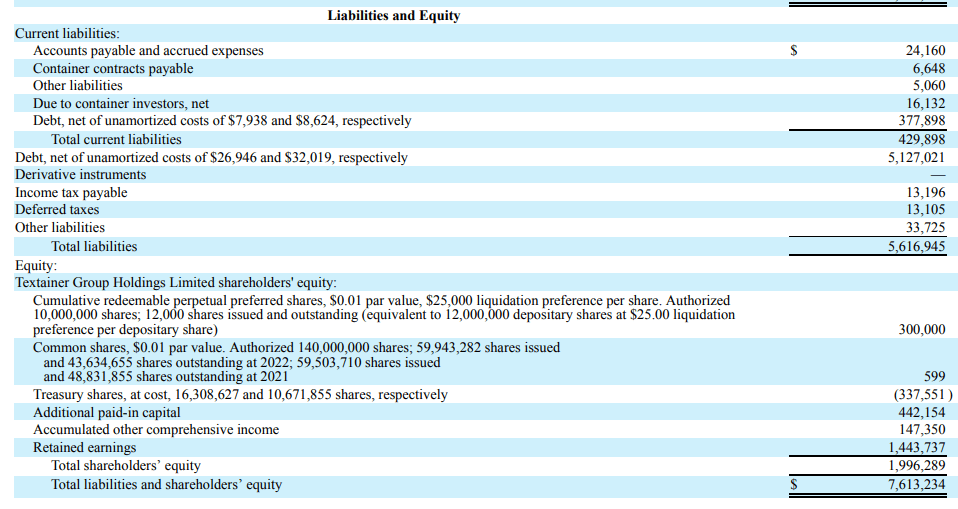

Looking at the liability side of the balance sheet, the total amount of equity came in very close to $2B. Of that amount, $300M comes from the preferred shares which means there is almost $1.7B in equity ranked junior to the preferred shares. Or in other words, the asset coverage ratio (total equity versus preferred equity) exceeds 600%.

{kind=link}

I own both the A and B series of the preferred shares

For a breakdown of the preferred shares I'd like to refer you to my previous article , but a very brief recap makes sense. The B-Series ( TGH.PB ) have a fixed preferred dividend rate of 6.25% per year ($1.5625 per share per year, payable in four equal quarterly installments) and based on the share price at the closing bell on Tuesday ($20.15), the yield is approximately 7.8%. Keep in mind there is no foreign dividend withholding tax on the preferred dividends (there obviously also is no withholding tax on the dividends on the common shares).

The Series A ( TGH.PA ) have a preferred dividend yield of 7% and closed at $23.93 on Wednesday, resulting in a yield of 7.3%. Based on these elements, the Series B have a higher yield and appear to be the offering the best value here.

That is true, but the A-series have a special kicker. After an initial five-year period (ending on June 15, 2026), the preferred shares can be called by Textainer. If that doesn't happen, the preferred dividend will be reset to the five-year Treasury rate plus a mark-up of 6.134% .

The 5 year US Treasury Bond currently has a yield of 3.53% which means that if the preferred dividend would be reset today, the preferred dividend would come in at $2.41 per share. Which would result in a yield of just over 10%. And if the Series A would get called in 2026, its owners will generate a yield to call of in excess of 8.5%. Both options are fine with me and the worst case scenario would be to see the 5Y US Treasury fall below 2% again which would reduce the likelihood of a call and would result in a somewhat disappointing dividend reset.

Investment thesis

I own both series of the preferred shares. I own the A-shares as a speculative position on either an attractive reset in 2026 or seeing the preferred shares being called by the company to lock in the capital gain. I also own the B-series to satisfy my longer-term needs. As a 6.25% cost of capital for equity is pretty low, I can't see the B-series being called anytime soon.

For further details see:

Textainer Group Holdings: I Own The 7%+ Yielding Preferred Shares