TRTN - Textainer Holdings: A 9.1% Yield To Call On The Preferred Shares

Summary

- Textainer is one of the largest container lessors in the world.

- The preferred dividend coverage is excellent, making the preferred shares attractive from a risk/reward perspective.

- The company will likely spend excess cash flow on reducing its gross debt, to smoothen out the impact of interest rate increases.

Introduction

I like the preferred shares issued by container lessors. In a recently published article, I had a closer look at Triton International ( TRTN ) and its preferred shares, and as it has been a while since I last discussed the preferred shares issued by Textainer Group Holdings ( TGH ), I figured it is time for an update here as well.

Stellar results in the third quarter, while the cash flows also remain strong

During the third quarter, Textainer's total revenue came in at $205M while the operating expenses were just $106M (including in excess of $73M in depreciation and amortization expenses. Throwing in the $22.8M in gains on the sale of containers results in an operating income of just over $123M. That's an increase of approximately 8% compared to the third quarter of 2021.

{kind=link}

The interest expenses increased (and will likely continue to increase) but this still meant the company was able to post a pre-tax income increase of more than 20% thanks to the non-recurring debt termination expenses which was incurred in the third quarter of last year. Textainer pays virtually no taxes and the net income for the third quarter was $81.4M. The preferred equity required almost $5M in cash payments to cover the preferred dividends which means the bottom line shows a net income attributable to the common shareholders of Textainer of $76.4M, for an EPS of $1.66 based on the average share count of 45.9M shares outstanding. As of the end of the third quarter, the exact share count had already decreased to less than 45M shares which will provide an additional boost to the EPS in the next few quarters.

The strong third quarter helped to boost the reported net income in the first nine months, and Textainer reported a net income of just under $228M for an EPS of $4.82. This is based on an average share count of in excess of 47.2M shares and that share count is now more than 5% lower.

{kind=link}

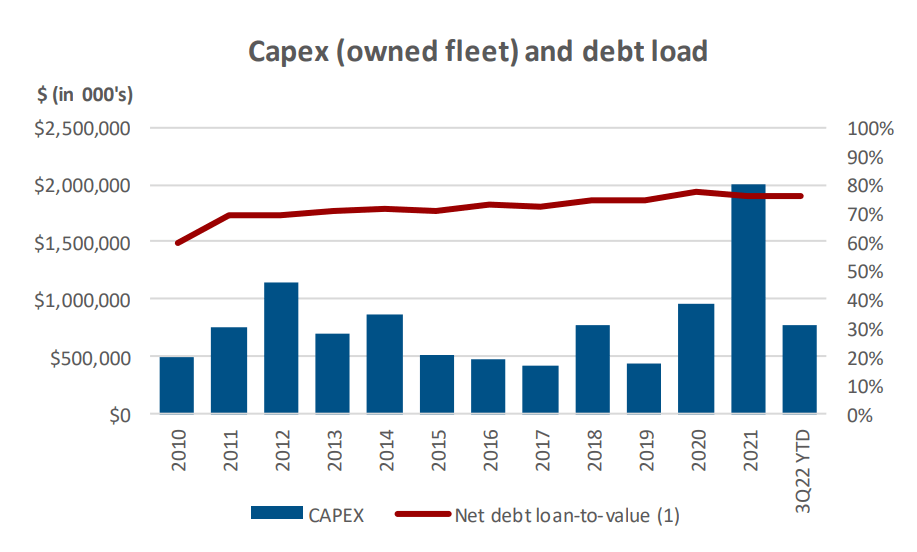

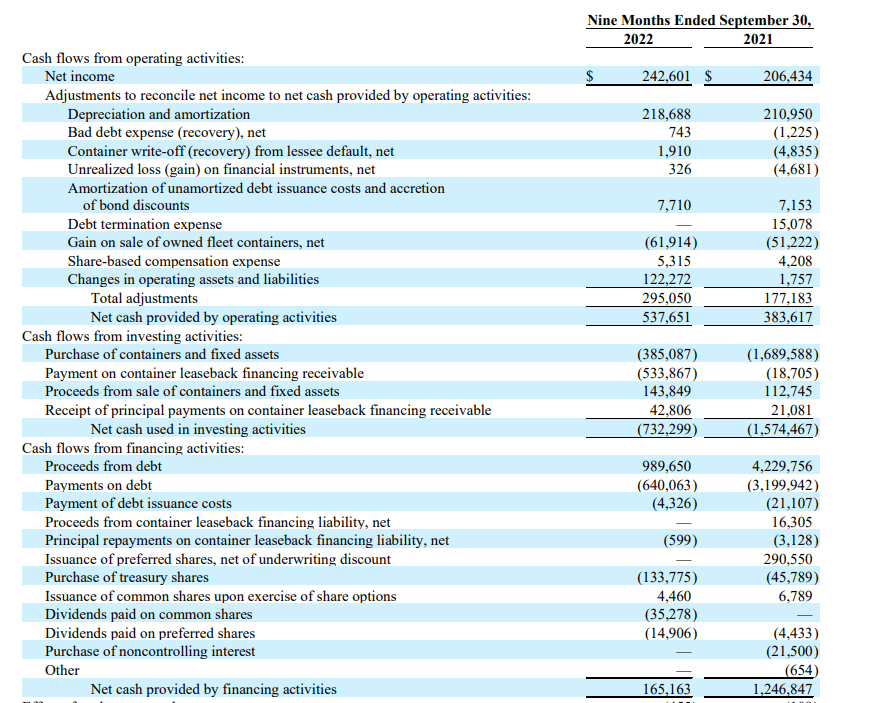

As the initial craziness on the container market is now over, Textainer's capex has dropped off a cliff. The cash flow statement below shows the company reported an operating cash flow of $538M in the first nine months of the year, but this includes a contribution of $122M from working capital elements while we still need to deduct the $15M in preferred dividend payments.

{kind=link}

On an adjusted basis, the operating cash flow was approximately $400M, which is still more than 5% higher than the $382M in the first nine months of 2021.

The capex will likely continue to be pretty low in the foreseeable future as on the Q3 conference call , Textainer's management mentioned it sees limited capex opportunities and prefers to pay back debt to avoid getting hit with higher interest rates.

As we noted earlier, we expect limited CapEx opportunities in the near term, and we may elect to deliver the unhedged components of our debt financing in order to minimize the impact of higher interest rates from this portion of our debt.

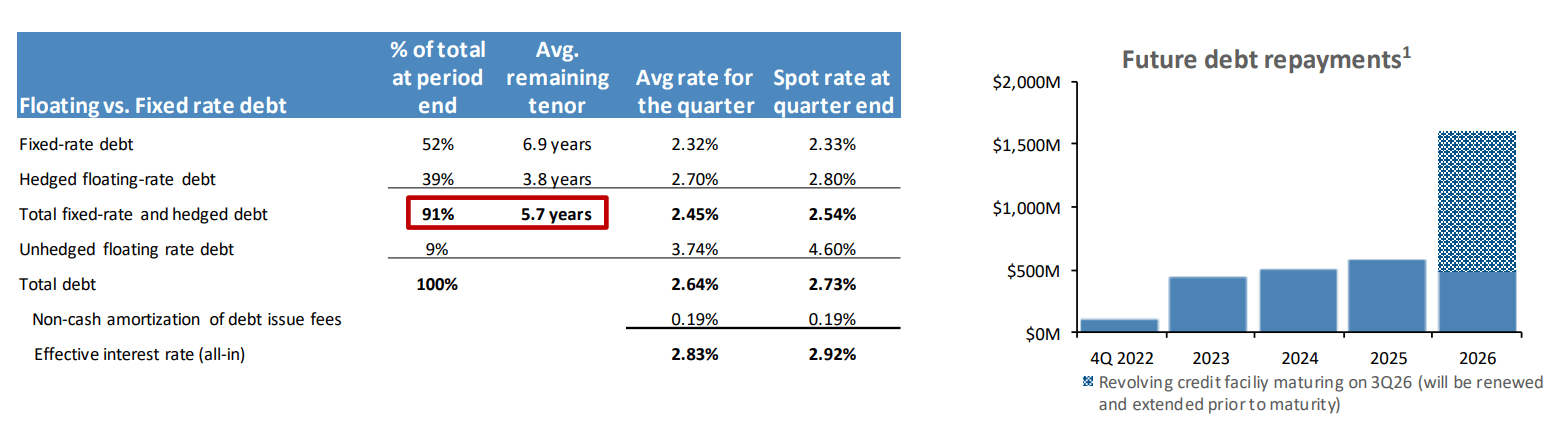

I'm not too worried about the debt as the vast majority either has a fixed interest rate or is hedged. But looking at the repayment schedule, about $400M in debt will have to be refinanced this year and we will likely see a gradual increase of the cost of debt.

{kind=link}

I own both series of the preferred shares

For a breakdown of the preferred shares I'd like to refer you to my previous article , but a very brief recap makes sense. The B-Series ( TGH.PB ) have a fixed preferred dividend rate of 6.25% per year and based on the share price at the closing bell on Wednesday ($20.33), the yield is approximately 7.7%.

The Series A ( TGH.PA ) have a preferred dividend yield of 7% and closed at $23.47 on Wednesday, resulting in a yield of 7.45%. It appears the choice is easy and the Series B have a higher yield.

That is true, but the A-series have a special kicker. After an initial five-year period (ending on June 15, 2026), the preferred shares can be called by Textainer. If that doesn't happen, the preferred dividend will be reset to the five-year Treasury rate plus a mark up of 6.134% .

As you can see below, the 5 year US Treasury Bond currently has a yield of 3.6% (down from close to 4.5% just a few months ago). This means that if the preferred dividend would be reset today, the preferred dividend would come in at $2.43 per share. Which would result in a yield of almost 10.4%.

{kind=link}

So while the current yield is a bit lower than the Series B, as long as the 5 year US treasury yields in excess of 1.15%, the A series will reset at a higher rate than the B-series currently yields. You may also wonder how keen Textainer is on seeing its cost of preferred capital increase to almost 10% and that makes a call possible. Not necessarily likely (it was more likely when the 5Y US Treasury was yielding closer to 4.5%), but definitely possible. In that case we need to work with the yield to call which in this case is just over 9%. Still very attractive of course, and that's why my position in the Series A is higher than in the Series B.

I don't anticipate any issues when it comes to the affordability of the preferred dividends: in the first nine months of the year, Textainer only needed just over 6% of its net income to cover the dividends.

{kind=link}

Investment thesis

I own both series of the preferred shares. Although the Series A would be the clear winner, I also already wanted to get a decent long position in the B-series as those are less likely to be called in a few years given the fixed preferred dividend which isn't even very high in these changed market circumstances.

While I wouldn't mind seeing the Series A being called in 2026, I am fine with just keeping the Series B and get my quarterly preferred dividend. I also have a small long position in the common shares of Textainer, but as this is a non-core position and pretty small, I have written call options against it and am expecting the current position to be called away soon. Not because I don't believe in the common shares, but because I'm happy with just pursuing the quarterly income with the preferred shares.

For further details see:

Textainer Holdings: A 9.1% Yield To Call On The Preferred Shares