TGH - Textainer: I Like The 8.3% Yielding Preferred Shares

2023-10-06 10:30:00 ET

Summary

- Textainer has seen its revenues decrease but remains profitable despite a slowdown in the world economy.

- The company has been buying back its own shares and has stabilized its debt levels.

- The preferred shares of Textainer offer an attractive risk/reward ratio, with higher yields and potential for dividend resets.

Introduction

Although I currently have no position in the common shares of Textainer Group Holdings ( TGH ), I am keeping an eye on the company to make sure my position in the preferred shares is ‘safe’. While the world economy is slowing down, Textainer has seen its revenues decrease but fortunately the company didn’t get sucked in the interest rate vortex as almost its entire debt pile has a fixed interest rate. The higher interest rates on the financial markets will only be felt when Textainer refinances existing debt. And of course, the preferred shares rank senior to the common shares.

The company remains profitable despite a slowdown

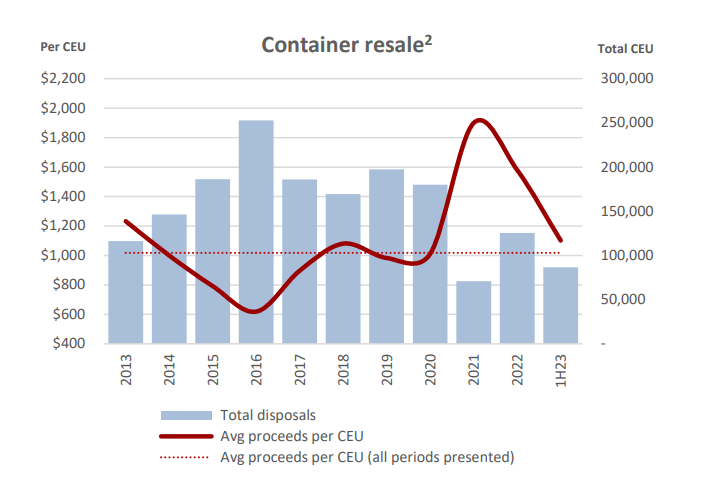

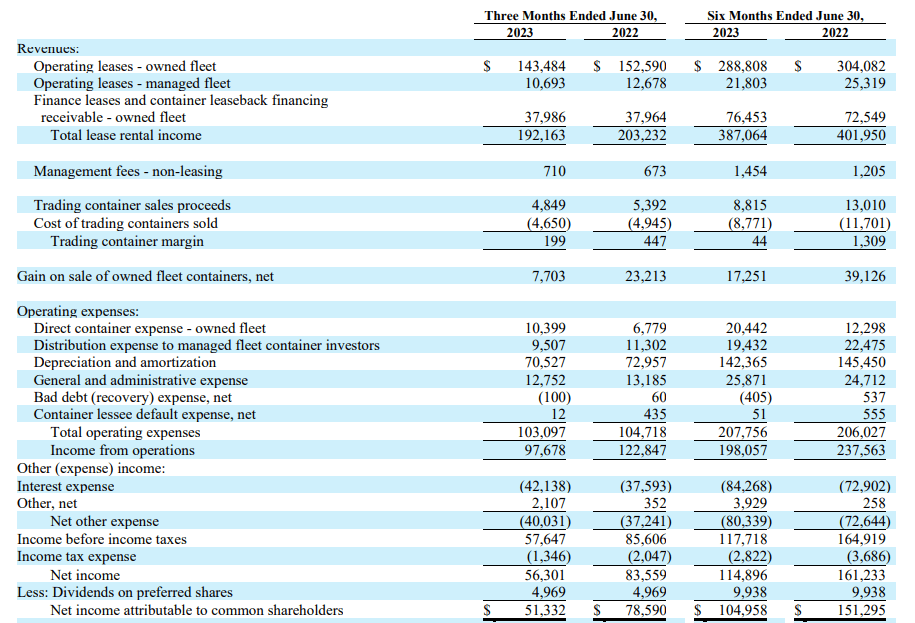

During the second quarter, Textainer reported a total revenue of $192M from the leases and rental income of containers. Meanwhile, there was a $0.2M margin on trading containers while the company also reported a $7.7M gain on the sale of containers. The latter is obviously lower than in the preceding few quarters and years not in the least because the value of second hand containers has come down. As you can see below, the total average resale proceeds on the market have dropped by about a third and this obviously reduces the profit per sold container as the discrepancy between market value and book value has decreased.

{kind=link}

On the other hand, the operating expenses remained pretty stable and thanks to the company’s policy to have fixed rate debt, the interest expenses are still very reasonable (but will be an issue the company will have to deal with upon refinancing).

{kind=link}

The total net income was $57.6M but you still have to deduct the $6.3M in profit attributable to non-controlling interests and this results in a net income of $51.3M attributable to the common shareholders of Textainer. This represents an EPS of $1.22.

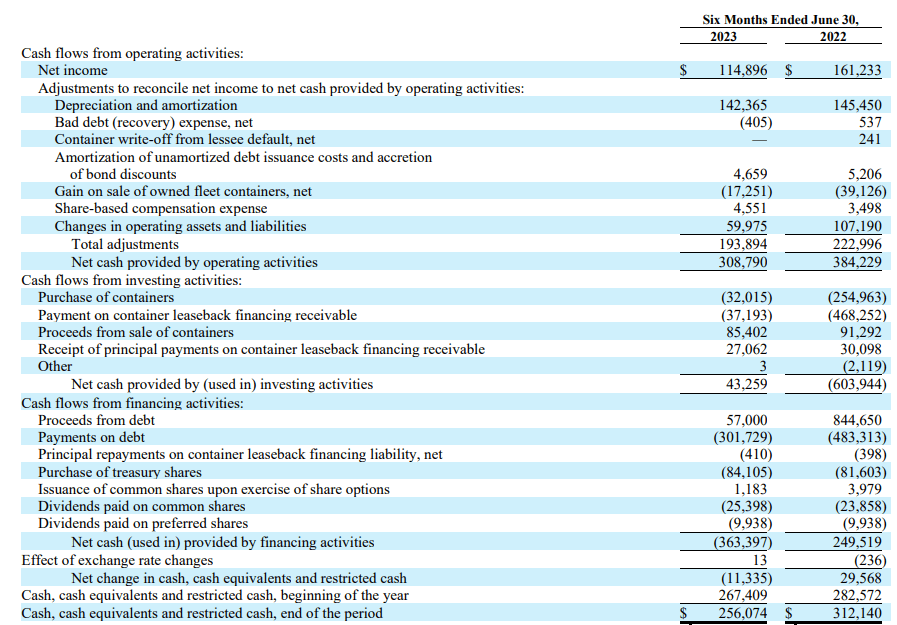

Looking at the cash flows of the company, Textainer is continuing to buy back its own shares. It has spent $84.1M on share buybacks in the first semester of this year and this allowed the company to retire about 2.4 million shares. As of the end of the second quarter, the net share count was approximately 41.3M shares, down from 43.6M shares as of the end of last year.

{kind=link}

While there’s nothing wrong with buying back stock, Textainer should obviously remain focused on its balance sheet as well. The total debt level will have to remain in line with the residual value of the containers while Textainer will also have to keep an eye on its refinancing needs.

{kind=link}

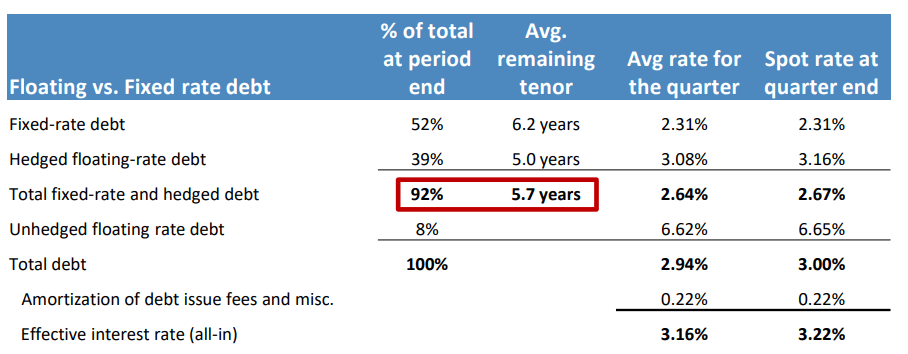

While the average cost of debt is very advantageous right now (see above), the company will have to deal with debt repayments and the interest expenses will increase.

Textainer Investor Relations

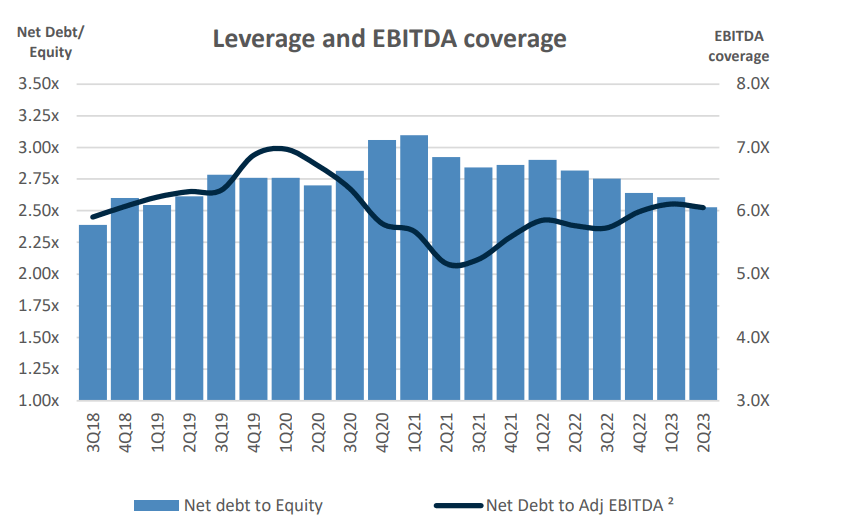

Fortunately Textainer has been doing the right thing and its net debt to equity ratio and its net debt to adjusted EBITDA ratio has stabilized.

{kind=link}

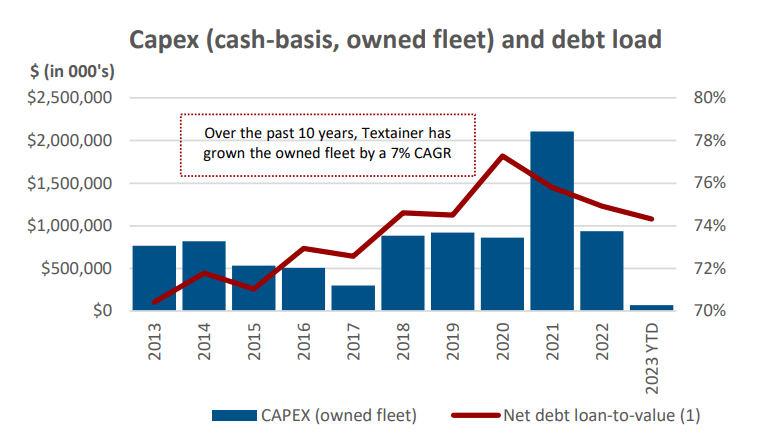

Fortunately the total capex has come down and this helps the free cash flow result but with an LTV ratio of in excess of 70% I would still prefer the company to spend more effort reducing its gross debt versus buying back stock. The board recently approved another $100M buyback program so it will be interesting to see the buyback pace in the third quarter. I am somewhat surprised the company isn’t buying back preferred shares at a discount to call value.

{kind=link}

The economic model makes a lot of sense but you’d also want to avoid the market starting to ‘bet against you’. The total gross debt level is $5.26B right now. And even if this would decrease to $4.5B but at a cost of debt of 5.5%, the interest expenses would increase by almost 50% to $250M per year. Still manageable, of course, but an additional $20M in interest expenses per quarter would reduce the EPS by $0.50.

I still have a long position in both preferred share issues

For a breakdown of the preferred shares I'd like to refer you to this older article , but a very brief recap makes sense. The B-Series ( TGH.PR.B ) have a fixed preferred dividend rate of 6.25% per year ($1.5625 per share per year, payable in four equal quarterly installments) and based on current share price of $18.74, the yield has increased to 8.34%. Keep in mind there is no foreign dividend withholding tax on the preferred dividends (there obviously also is no withholding tax on the dividends on the common shares).

I also have a long position in the Series A ( TGH.PR.A ) preferred shares, which have a preferred dividend yield of 7% and closed at $23.17 on Wednesday, resulting in a yield of 7.55%. Based on these elements, the Series B have a higher yield and appear to be the offering the best value here. But that’s not necessarily true and it depends on what you are expecting from the interest rates going forward. After an initial five-year period (ending on June 15, 2026), the Series A preferred shares can be called by Textainer but if that doesn't happen, the preferred dividend will be reset to the five-year Treasury rate plus a mark-up of 6.134%. The current 5 year treasury yield is 4.74% which means the preferred dividend would reset at almost 10.90% and that would represent a yield of north of 11.5% based on the current share price.

Of course a lot can change between now and the summer of 2026 but if the 5 year government bond stays at the current rate (or even if it would drop to 4%), I can imagine Textainer would be interested in calling that series of preferred shares. The yield to first call is about 9.5% which is attractive as well.

Investment thesis

I currently have no position in Textainer’s common shares but the risk/reward ratio of the preferred shares is attractive. While I will have to continue to monitor the balance sheet on a quarterly basis to make sure the preferred dividends are still fully covered (I don’t expect to see any issues here as the company needed less than 10% of its attributable net income in the second quarter to cover the dividend). More importantly, I will also keep a close eye on the asset coverage ratio. As of the end of June, there was about $1.22B in common equity which ranks junior to the $300M in preferred equity. That’s fine -especially considering the market value of the containers is still a bit higher than the book value – but it remains an element I will focus on.

I have a long position in both the Series A and B preferred shares. I may add on weakness but I’m in no rush given the current market circumstances.

For further details see:

Textainer: I Like The 8.3% Yielding Preferred Shares