THLLY - Thales Is Better Than Raytheon When Considering Cybersecurity

Summary

- The Eastern European conflict is translating into an opportunity for Thales whose stock has delivered an upside.

- There is also additional business for giant Raytheon whose backlog figures are simply dazzling.

- However, in its realignment exercise, the American company does not seem structured to take advantage of opportunities in cybersecurity, which is more immune to defense spending cuts and supply chain risks.

- On the contrary, the French defense play has a dedicated unit for cybersecurity, IOT, and e-Sim, which are all growing rapidly, and it is also investing in inorganic growth.

- The underlying theme here is that it is not necessarily the sales of sophisticated weapons that make the success of an Aerospace and Defense play.

While everyone is focused on the Javelin rocket used by Ukrainian forces co-developed by Raytheon Technologies ( RTX ), Thales S.A (OTCPK: OTCPK:THLEF ) (OTCPK: OTCPK:THLLY ) has been quietly bagging air defense systems contracts to be deployed on the war zone.

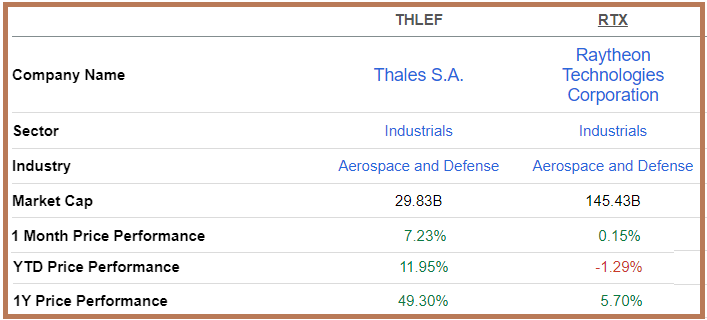

The French company is set to report full-year 2022 results on March 8 while the U.S. company already reported FY-2022 on January 24. Perfectly aware that neither these two manufacture the same products nor have the same scale of operations, the aim of this thesis is to show that investors are right in allocating more capital to Thales, which has outperformed its American peer both in the short and long term as shown below.

Comparison of Key Metrics (seekingalpha.com)

{kind=link}

For this purpose, I will perform a comparison of revenues, and operational cash while providing insights into their diversification strategies, namely with respect to cybersecurity.

I start with Thales.

A Diversified Defense Play

Thales is a major European manufacturer of civilian transportation and military aeronautics, space, and a provider of digital security. It was at the 14th rank of the top 100 arms-producing and military services companies in the world in 2020, an improvement over the previous year's rank. It specializes in air defense technologies that involve the protection against all types of threats, across the entire airspace, ranging from detection, identification, and even neutralization.

Its latest contract is for the delivery of a complete short-range air defense system to protect Ukraine, including a Ground Master 200 radar, which makes it possible to deal with the threats posed by drones, or long-range attacks of cruise missiles, helicopters, and fighter planes. In this case, with threats now becoming more stealthy, agile, and swift, air defense systems must be able to detect and track any type of target, providing adequate information on moving objects, in the air, on the ground, or on the water.

The fact that Thales has expertise in a wide range of air defense, ranging from anti-drone warfare to anti-ballistic systems including surface and airborne radars, command centers, communications, and associated terminals, and different types of effectors accounts for the bulk of its revenues.

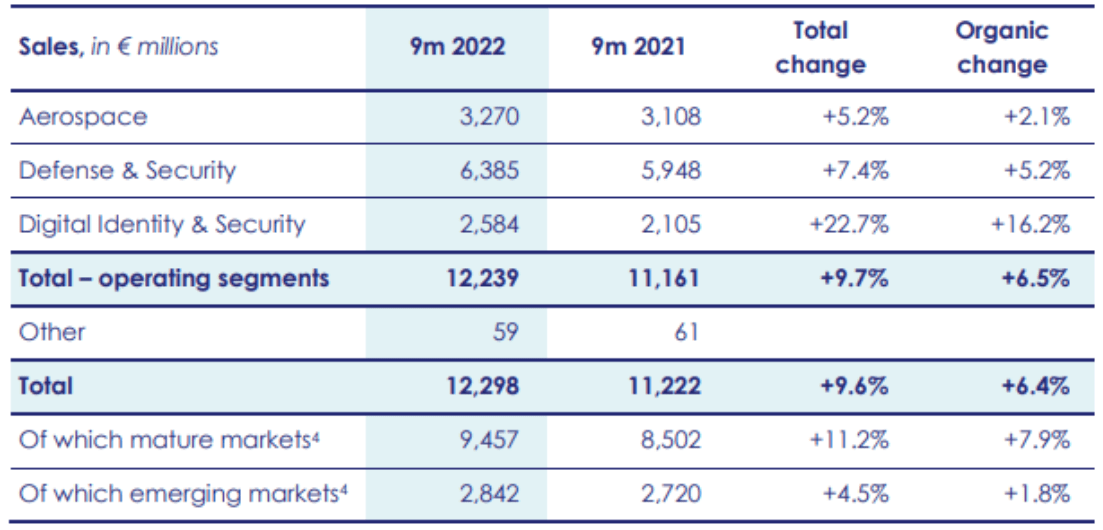

Thus, Defense and Security constituted 52% of orders in the first nine months of 2022 (9m2022) with the rest (48%) made up of Aerospace and Digital Identity and Security.

Sales for the first nine months of 2022 (www.thalesgroup.com)

{kind=link}

It has been suffering from supply chain issues for semiconductors and expected no further deterioration for the remainder of 2022 while benefiting from $15.4 billion of orders (backlog) for the 9m2022 compared to $12.3 billion of revenues. Thus, the book-to-bill or the number of orders received divided by the units shipped and billed is more than 1, signifying that the company has a buffer to withstand any adverse impact on demand.

The Aerospace segment grew at a slower pace, but the double-digit growth of Digital Identity and Security will be detailed later.

Raytheon's Realignment

As for the manufacturer of the Patriot, Stinger, and F-35 engines, it had a backlog of $175 billion at the end of December last year, or more than 2.5 times the FY-2022 revenues of $67.1 billion (table below) as a result of benefiting from spending increased military in the United States and Europe. Therefore, it has a more substantial buffer than Thales to withstand hard times, which could take the form of a ceasefire in Ukraine.

Total Revenues by Segment (seekingalpha.com)

Bottlenecks within its supply chains are weighing on growth, but it has diversified its supplier base and seeks additional sources for critical commodities. Progress has been made since sales reached $18.09 billion in the fourth quarter of 2022, up 6.1% from $17.04 billion a year ago.

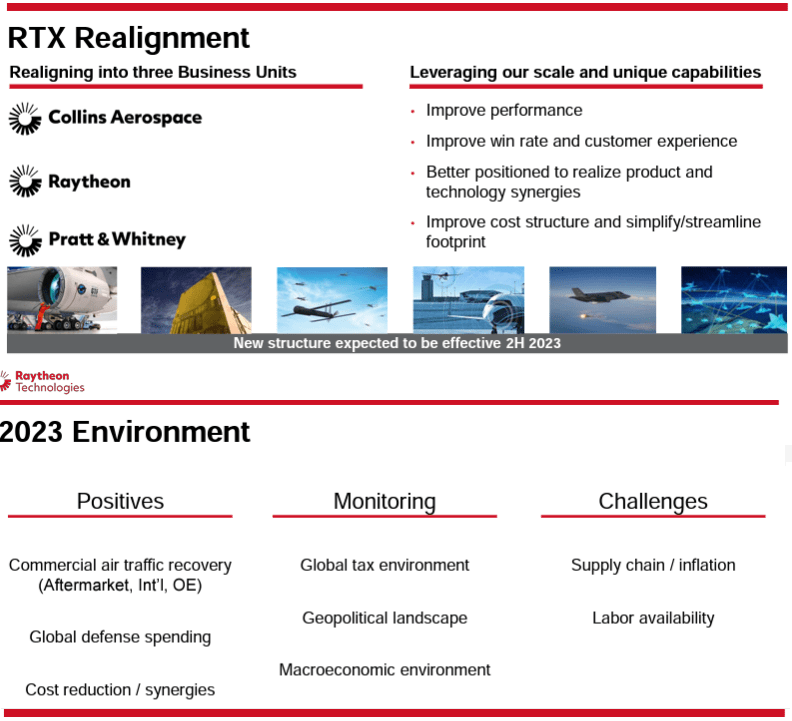

The group is currently realigning its four segments consisting of Collins Aerospace, Pratt & Whitney, Raytheon Intelligence & Space, and Raytheon Missiles & Defense into three. These are Collins Aerospace, Raytheon, and Pratt and Whitney as pictured below, all as part of a strategy to be better positioned in the market and improve cost structures.

Company presentations dated February 2023 (static.seekingalpha.com)

{kind=link}

In this respect, Raytheon operates in several industries including avionics, electric propulsion, hypersonics, and quantum physics. It even has a semiconductor foundry where it is working on producing military-grade gallium nitride. This vertical integration certainly merits be highlighted, but, I find it inappropriate that Raytheon's management did not come up with a separate and dedicated cybersecurity department, just like Thales, and this, while there is certainly an awareness of the importance of cybersecurity which formed part of Raytheon Intelligence and Space. This segment generated 18.7% of revenues in the fourth quarter of 2022.

Valuing Thales with its Dedicated Cybersecurity business, IoT and eSim

For this matter, the French company's cybersecurity activities are grouped under, the Digital Identity and Security segment further, a segment which generated 21% of sales for 9m2022, after growing by 22.7%. Going forward, it should grow even faster with the acquisition of two European cybersecurity companies, S21sec and Excellium, in October last year.

In this case, one of the advantages of cybersecurity compared to military hardware is that it is much more immune to defense spending cuts and supply chain challenges. The idea is also that defense plays like either Raytheon or Thales are in a unique position to offer cybersecurity services which have gradually evolved from the corporate space to occupy a more military dimension as state-backed actors try to steal data or damage America and its allies' IT infrastructures. In this environment of heightened geopolitical tensions, the number of cyberattacks has surged by 38% from 2021 to 2022.

As I had explained in a previous thesis , some cybersecurity companies' threat intelligence team goes to the point of monitoring hackers' infrastructure and funding mechanisms in order to be one step ahead. Also, the CEO of the company I covered (called Mandiant ) being a former military also reinforces the rationale that defense companies offer a unique perspective to cybersecurity that Thales has recognized and is taking advantage of.

Therefore, the French company should be better valued given that it has a lower trailing price to sales of 1.69x compared to Raytheon's 2.16x. Thus, adjusting for a P/S of 1.9x, I obtain a target of $156.7 ((139.38 x 1.9)/1.69) based on the current share price of $139.38.

Comparison of valuations and other metrics (seekingalpha.com)

{kind=link}

To further justify my bullish stance, Thales made it to the Gartner Magic Quadrant for its IAM (identity and access management) solutions in 2020. Now, the IAM market which was valued at $12.85 billion last year and is expected to grow by nearly three times 14.12% CAGR by 2030 has gained importance as the surface area of attack available to hackers has grown significantly as a result of employees working from home and organizations transferring their workloads to the cloud.

Moreover, Thales also proposes IoT (internet of things) and eSIM, whose market sizes were valued at $201 billion and $8.5 billion respectively in 2022 and are expected to grow at double digits in the years ahead. In this respect, while Apple (NASDAQ: AAPL ) has been one of the key catalysts for eSIM with its iPhone 14, Thales is one of the leaders in the integration ecosystem, including key wins from smartphone plays like Samsung (OTCPK: OTCPK:SSNLF ) and Google (NASDAQ: GOOG )(NASDAQ: GOOGL ).

Other Metrics Besides Revenue

For those who are still not convinced that the French company is a better choice, namely due to the fact that Raytheon generates much higher revenues as one of the top weapons suppliers, there is cash generation. Hence, operating cash margins or the operating cash flow as a percentage of revenues has been declining for Raytheon during the last five years as shown in the orange chart below, while it has been improving for the French company.

{kind=link}

Furthermore, the world's largest weapon companies in 2021 were American. This stems from the fact that the United States has the world's largest armament expenditure, with its weapon companies being shaped accordingly. Now, with Europe spending more money after the Ukrainian conflict, things are likely to change which bodes well for Thales.

To be realistic, Raytheon is better positioned as an end-to-end defense supplier ranging from missiles to the U.S. Navy's SPY-6 radar. It is also one of the few defense integrators which have the ability to deliver solutions to detect, track and engage threats in a market valued at $577.19 billion in 2023 and expected to grow at a CAGR of 5.6% till 2027. This is the reason that one cannot be bearish on the stock.

However, comparing this with the 12.4% growth for the cybersecurity market, the reason why I am bullish on Thales quickly makes sense. Again, to be fair to Raytheon, with its Cyber Systems Defense , it delivers the latest protection against threats for clients, but, it does not appear to be structured to make advantage of opportunities.

Concluding with Caution

Thus, this thesis has shown that Thales is better as it prioritizes cybersecurity alongside its military and aerospace businesses. However, contrarily to its American counterpart which benefits from a significant customer base in its home country, the French company is more dependent on exports in order to sustain its sales figures. Also, the tightness of the French market and its much smaller industrial and technological base does not allow the arms industry to bear the high costs of research, development, and production for the sort of high-tech weapons which the likes of Raytheon can produce.

Finally, while supply chain concerns are easing, there is high inflation to contend with on both sides of the Atlantic Ocean, with the effects likely to be felt on profitability in case the companies are not able to cut costs.

For further details see:

Thales Is Better Than Raytheon When Considering Cybersecurity