ACWI - Thanks To A Transfer My IRA More Than Doubled: Now What?

2023-09-12 08:00:00 ET

Summary

- A recent inflow of cash from my Pre-Tax 401k account required those funds to be deployed. The focus of this article is how that was/is being accomplished.

- How my IRA fits into our overall retirement and estate plan is also covered as no account should be evaluated without taking a look at the complete strategy.

- Links to articles that provide more details on our total investment strategy are provided.

Introduction

As a follow-up to my Strategy Change: I've Started Transferring Funds From My 401k Plans To My IRAs article, I thought an article that covered its effect on one of the receiving accounts was in order, especially after the attention the original article received. I’ll say upfront that my IRA could double in size again if I choose to close out my Pre-tax 401k account. How successful the strategy I implemented now and discussed here works (still in process as you will read) will help in making that decision.

Investment accounts overview

My wife and I look at our accounts as four parts of our retirement and estate plan.

- Taxable accounts : We have three at this point for two reasons: state tax savings and access to a financial consultant . We hope to collapse these into one when our situation changes.

- Roth IRAs : We both have one that are still receiving contributions. All the beneficiaries are members of our extended family. Odds are that we will never have to touch these accounts for funds.

- 401k (Pre-tax, Roth) : Right now the extended family is listed as beneficiaries, but there is a good chance most of these funds will move into other accounts. This article covers how I am investing the last Pre-tax move into my traditional IRA.

- Traditional IRAs : Here, we have three, as my wife inherited her dad’s. My folks’ IRAs are going to charity, so there won’t be a fourth! Right now, only the inherited IRA requires RMDs, which we satisfy via QCDs .

The account covered here is my Traditional IRA, which had not had an inflow in decades since opening my Roth IRA.

Strategy undertaken

First, I had to decide the allocation split between equities and fixed income assets and then allocations within both of those. My targets are:

- Domestic equities: 50%

- International equities: 10%

- Cash/CDs: 15%

- Fixed income funds: 15%

- PFDs, Notes and Baby bonds: 10%

Achieving those targets used different approaches. All three CDs were new to this account and are spaced to allow for replacing one every year with a new 3-year CD starting in 2024. That weight was chosen to match the weight of the Stable Value Fund assets that flowed into this account.

I already owned the VanEck Fallen Angel High Yield Bond ETF ( ANGL ) and Cohen & Steers Limited Duration Preferred and Income Fund ( LDP ). For LDP, I just bought more shares. For ANGL, I used the strategy that is also employed for most of the equity exposure additions: writing put options on that ticker.

All the Preferreds/Notes are new, but I held other investments from two of the four. I liked what I found when reviewing Stifel Preferreds , resulting in the purchased of the Stifel Financial Corp. 4.50% DEP PFD D ( SF.PR.D ). I became aware and liked the FTAI Aviation Ltd. 8.25% RED PFD C ( FTAIN ) after another SA Contributor covered it. All these were done using Limit trades. The two Notes mature in 2028 and will provide 7+% YTMs, assuming they are not called before then (earliest one is in 2025).

With the exception of adding shares in the Wasatch Emerging India Fund ( WAINX ), I chose to mostly use my Cash-Secured-Puts strategy to expand my equity holdings. I made note of where each was trading at the time to evaluate later whether this was a good strategy to use. All the strikes were near the market price at the time the option trade was placed. In the meantime, the cash is earning close to 5%, though potential dividends are being missed. Expiration dates go into January of 2024. This strategy works best in a flat to declining market.

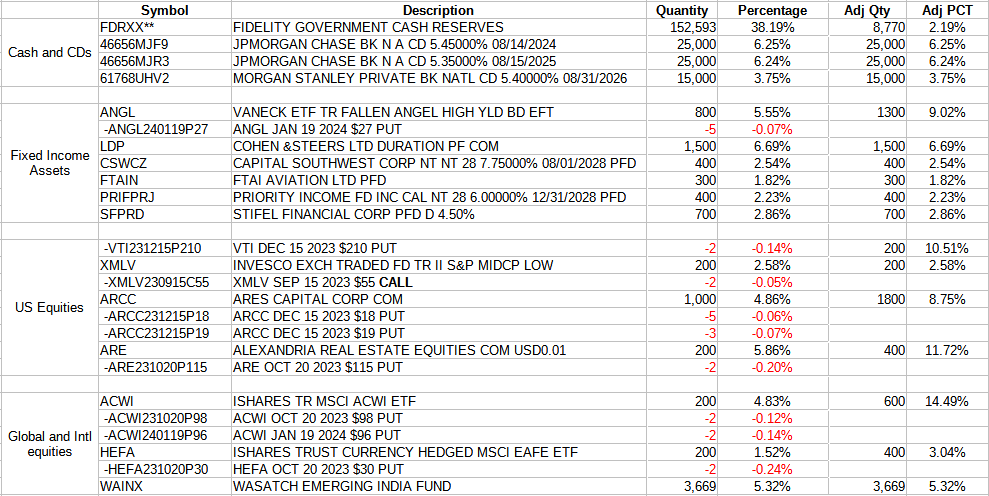

This is what the account looks like today.

{kind=link}

Author's Investment XLS

The options all show negative quantities since I am short those contracts. The adjusted quantity column assumes all options get assigned. The Adjusted Percent column reflects that and uses a 67/33% US/INTL split on the iShares MSCI ACWI ETF ( ACWI ) weight, matching its global allocations. I picked the iShares Currency Hedged MSCI EAFE ETF ( HEFA ) for part of my international equity exposure as hedging has worked well over the past decade and the other international funds are not hedged. I like the Vanguard Total Stock Market ETF ( VTI ) as a Core holding for US equities and while new to this account, I hold it elsewhere.

You might have noticed I have Calls written against my Invesco S&P MidCap Low Volatility ETF ( XMLV ). There are better Mid-Cap ETFs to hold, plus with the addition of the VTI ETF, that segment will be covered; no need to have a separate ETF.

Assuming all goes to plan, the account would end up with the following allocations, slightly off from my targets.

Author's Investment XLS

By closing out contracts where the potential allocation is too high, I can bring all the allocations in line to what my target levels are.

Other actions required

With the large movement of funds into this IRA and my Roth IRA, who gets how much from where was drastically altered! This required me to adjust the beneficiaries on almost every account to realign the beneficiary allocation back (or close to) what they were before. As future movements between accounts occur, this will need to be done again. I track all this in XLS at both the Primary and Secondary level. Designations are already setup to handle most changes in the makeup of the extended family.

Portfolio strategy

The key part for us is the division of our assets into the four segments listed above. The risk level for each account is then set based on that, and most were discussed in prior articles for those interested in the details:

- Taxable : Growth oriented, but with a low equity ratio and highest cash allocation to cover bill paying and emergency needs.

- Traditional IRAs : About 60/40 split, with Fixed Income allocation geared to generate funds needed to meet RMD/QCD payments. ( Article link )

- Roth IRAs : My wife’s has a 70/30 allocation. I use mine to write Cash Secured Puts, so it’s all cash unless I am holding an assigned stock/ETF waiting to be sold. ( Article link )

- 401k : The plan doesn’t allow for different allocations between the Pre-tax and Roth components. One reason I might not close these is having access to the Stable Value Fund, though as the linked article states, that now comes with a large opportunity cost. ( Article link )

Now retired four years, we have a better understanding of our income as both are now drawing on Social Security early and what “normal expenses” will be. Of course, the recent burst of inflation has required upward adjustments there. Key for me is to keep reviewing what we hold in terms of allocation shifts I might want to adjust or if a holding isn’t performing as expected. Retirement gives me plenty of time to monitor the accounts. A new strategy is using the same ETFs/MFs in each account, not just similar ones, as I had been doing.

Final thoughts

My recent review of the 401k plan shows the funds available there are performing as well as what I would probably use if I closed it out completely into my Fidelity IRA accounts. A recent law changed now means I do not have to move my Roth 401k to avoid RMDs, pointing out the constant need to stay alert to changes in retirement account rules.

One difference between a pre-tax 401k and a traditional IRA is the 401k does not allow QCDs to replace RMDs; the IRA does. Whether I need more QCDs to cover all our charity donations will influence more conversions.

For further details see:

Thanks To A Transfer, My IRA More Than Doubled: Now What?