VRE - The 3 Most Overvalued REITs

2023-04-04 15:52:14 ET

Summary

- Even cheap sectors have overpriced stocks.

- We examine 3 of the most overpriced REITs.

- There are different categories of overvaluation and different ways to spot each kind.

While I have spent quite a bit of time lately pointing out how undervalued and opportunistic REITs are at current pricing, valuation tends to fall in a spectrum. Although the midpoint of REIT valuation has shifted into undervalued territory, there is still a significant portion of the bell curve that remains overvalued.

In a normal pricing environment, the valuation spectrum looks like this.

{kind=link}

Given how much REIT market prices have fallen while earnings grew the valuation spectrum for REITs now looks like this.

{kind=link}

The bulk of the curve is now undervalued, but even with the shift to the cheap side, a significant number of REITs remain overvalued.

Thus, it might be unwise to just run in to the cheap sector and buy at random. In this article we discuss three of the most overvalued REITs.

Veris Residential ( VRE ) is just too pricey given dilution from transition.

Originally called Mack Cali, Veris Residential embarked on a portfolio transition from office to multifamily. This happens fairly often in REITs where companies like to move into the hot sector and usually it does not go well.

One of the challenges in transitioning property types into the hot sector is that the in favor assets trade at significantly lower cap rates than the out-of-favor assets. So while multifamily fundamentals are substantially better than office fundamentals, trading between the two sacrifices a ton of NOI. I will commend VRE for getting out of office before the sector got really bad, but it was still a costly transition.

As a pure-play multifamily REIT VRE now has significantly diminished FFO/share and its market price has not yet adjusted down to the new level of earnings. FFO for the next four years is expected to range sporadically from $0.41 to $0.50.

{kind=link}

With a $13.65 market price this represents a multiple ranging from 26X to 33X depending on the year.

VRE's properties are high quality and well located in rent-controlled areas.

{kind=link}

Rent control is one of the most misunderstood concepts in apartments as it is purported to benefit tenants, but the financial benefits accrue to the landlords. Essentially, rent controls prevent competing supply from coming in and allow landlords to slack on maintaining their properties since the rent will be the same regardless. In the long run it creates undersupply which is good for incumbent landlords and bad for residents.

Thus, VRE's fundamental outlook appears fairly strong but the valuation is far too high. At 33X 2023 FFO it is more than twice as expensive as the sector median of 14.7X 2023 FFO.

{kind=link}

An investor can get similar or better growth with Camden ( CPT ), or NexPoint ( NXRT ) but can get that growth at a multiple of 14.5X or 13.1X, respectively. I see no reason to pay an extreme multiple for VRE when strong peers are trading so cheaply.

Overvaluation masquerading as value at Safehold ( SAFE )

Overvalued is typically thought of as synonymous with high multiple, but from an analytical perspective it is just the trading multiple relative to the fair value multiple.

A high price to earnings company can still be undervalued if the growth is sufficient that it warrants an even higher PE. Similarly a low or medium multiple company can be overvalued if fundamental weakness justifies an even lower multiple.

The latter is the case with Safehold.

SAFE has already fallen in price from about $55 to under $30 in the past year.

{kind=link}

It has now gotten to a price range where it could be mistaken as a value stock. The 17X FFO multiple is no longer high and it is even trading at a slight discount to NAV at 97%.

{kind=link}

Source: S&P Global Market Intelligence

However, we believe fundamentals point to a substantially lower fair value.

We have three main gripes with SAFE

- SAFE is not earning anywhere near their FFO due to differences between GAAP accounting and cash accounting on 99 year leases.

- Management seems to put themselves over shareholders.

- Debt duration versus asset duration

We have previously written about the first two here so for today I will discuss the new topic which is number three above.

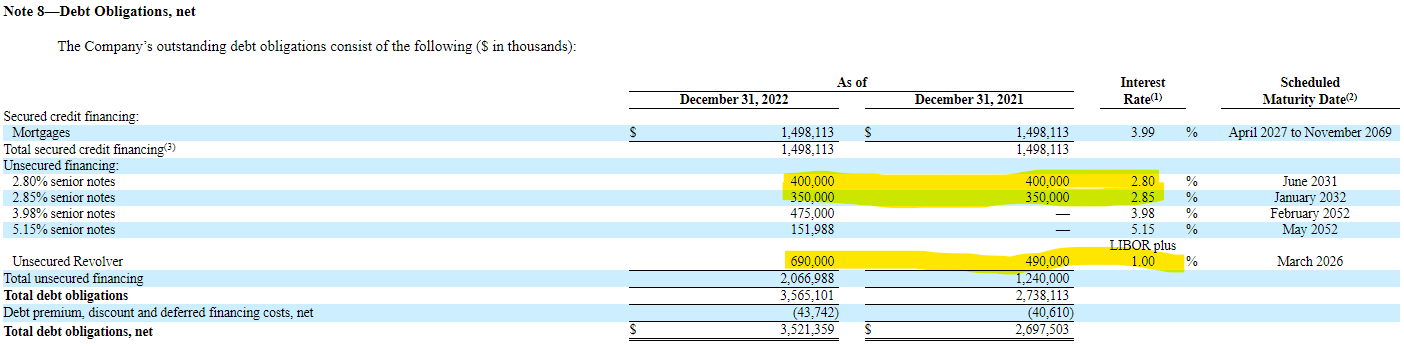

Below is Safehold's debt.

{kind=link}

Ordinarily I would consider this to be a fairly good debt structure with most of the debt termed out 8+ years.

Unfortunately for SAFE, its leases are as long as 99 years at signing so their debt will get marked to market far before their revenues do. Three loans in particular are concerning to me highlighted in yellow above.

$690 million on the floating rate revolver is already hurting as LIBOR has shot up. Another $750 million of very cheap debt comes due in 2031 and 2032 and will have to be refinanced at what will probably be significantly higher rates than the 2.80% and 2.85%.

As these costs of financing rise, the interest expense could go beyond what the associated assets are earning as SAFE entered into these assets when cap rates were exceptionally low. Some have cash yields around 3%.

It isn't likely to cause bankruptcy or be catastrophic, but I think it will pull earnings down. With declining earnings on top of the other problems plaguing SAFE, this is a company that should trade at a multiple far below the market average.

Clear overvaluation in Mid-America Apartment Communities ( MAA ) Preferred I (MAA.PI)

This one is not overvalued by a huge amount, but it is notable because of the high degree of certainty with which it is overvalued. Here are the vitals:

{kind=link}

Mid-America Apartment Communities is a solid company owning a large portfolio of class B apartments throughout most of America's land mass. I view the preferred as fairly low risk as I don't foresee the company having any trouble paying the distribution, even in a recessionary scenario. There is also a large equity base underneath so the preferred's spot in the waterfall looks well protected.

This is just a case of the market being blinded by the current yield and not thinking through all the factors. MAA.PI has an 8.5% face coupon with a $50 par value. It trades at $54.79 which takes the current yield down to 7.76%.

{kind=link}

7.76% would be a good yield relative to the risk and I think this is what the market is looking at in buying it at these levels.

However, it has a call feature exercisable on 10/1/26 which will almost certainly be executed due to the aforementioned strength of the company. MAA, even in today's high rate environment, has access to capital significantly cheaper than 8.5%.

Upon redemption shareholders would receive $50 in exchange for their shares which realizes a loss of $4.79 from today's price. Over the roughly 3.5 years until call MAA.PI will pay dividends of $14.87. Subtracting the $4.79 capital loss that is a total return of $10.08 over 3.5 years. Against a $54.79 price, that is a 18.4% return or a simple annualized return of 5.25%.

There are other similarly low risk preferreds with yields significantly higher than 5.25%. Don't be fooled by the high coupon as the premium to par will take a bite out of returns.

For further details see:

The 3 Most Overvalued REITs