UMH - The 7.7% Preferred Dividend Of UMH Properties Has Become Even More Attractive

2023-10-17 02:12:02 ET

Summary

- UMH Properties has improved its debt metrics, making its preferred dividend safer.

- The preferred stock offers a fixed annual rate of 6.375% and is currently trading at a dividend yield of 7.7%.

- UMH Properties has exhibited consistent performance and growth over the last five years, with strong business momentum and potential for future growth.

About four months ago, I recommended purchasing the preferred stock of UMH Properties (UMH.PD) for its exceptionally high yield and the safety of the dividend. The only point of concern for most investors was the high debt load of the REIT. However, I stated that the debt load had resulted primarily from supply chain disruptions, which had forced the REIT to order more than 1,000 homes in order to meet the excessive backlog. Therefore, it was reasonable to expect improved income and lower expenses in the upcoming quarters.

Indeed, in the second quarter, UMH Properties greatly improved its debt metrics. As a result, its preferred dividend has become safer. In addition, the yield of the preferred stock has climbed from 7.5% in June to 7.7% now due to persistently high inflation, which has triggered a rally in treasury yields lately. Overall, the risk-adjusted return of the preferred stock of UMH Properties has become even more attractive for patient investors, who can maintain a long-term perspective amid the recent surge of treasury yields to 16-year highs.

Characteristics of the preferred stock of UMH Properties

The preferred stock of UMH Properties has a fixed annual rate of 6.375% at its par price of $25. The stock is currently trading at $20.80 and hence it is offering a dividend yield of 7.7%. It is also cumulative, i.e., any dividends that were not paid during a quarter due to lack of liquidity (a highly unlikely event) will be paid whenever dividend payments resume.

Moreover, the preferred stock can be called by the company at its par value of $25 at any time. However, as long as interest rates do not decrease significantly from current levels, UMH Properties is unlikely to call its preferred stock.

Business overview

UMH Properties is one of the largest manufactured housing landlords, with a 55-year history. It has 135 manufactured home communities, which are located across the Midwestern and Northeastern U.S.

The number of developed homesites of the REIT has grown from about 24,500 to 25,700 in the last 12 months. UMH Properties has also grown its rental portfolio from 8,800 to 9,600 units and expects to keep growing this portfolio by 800-900 units per year. In addition, the company has 3,600 vacant lots to fill and nearly 2,100 vacant acres and thus it expects to build about 8,500 future lots.

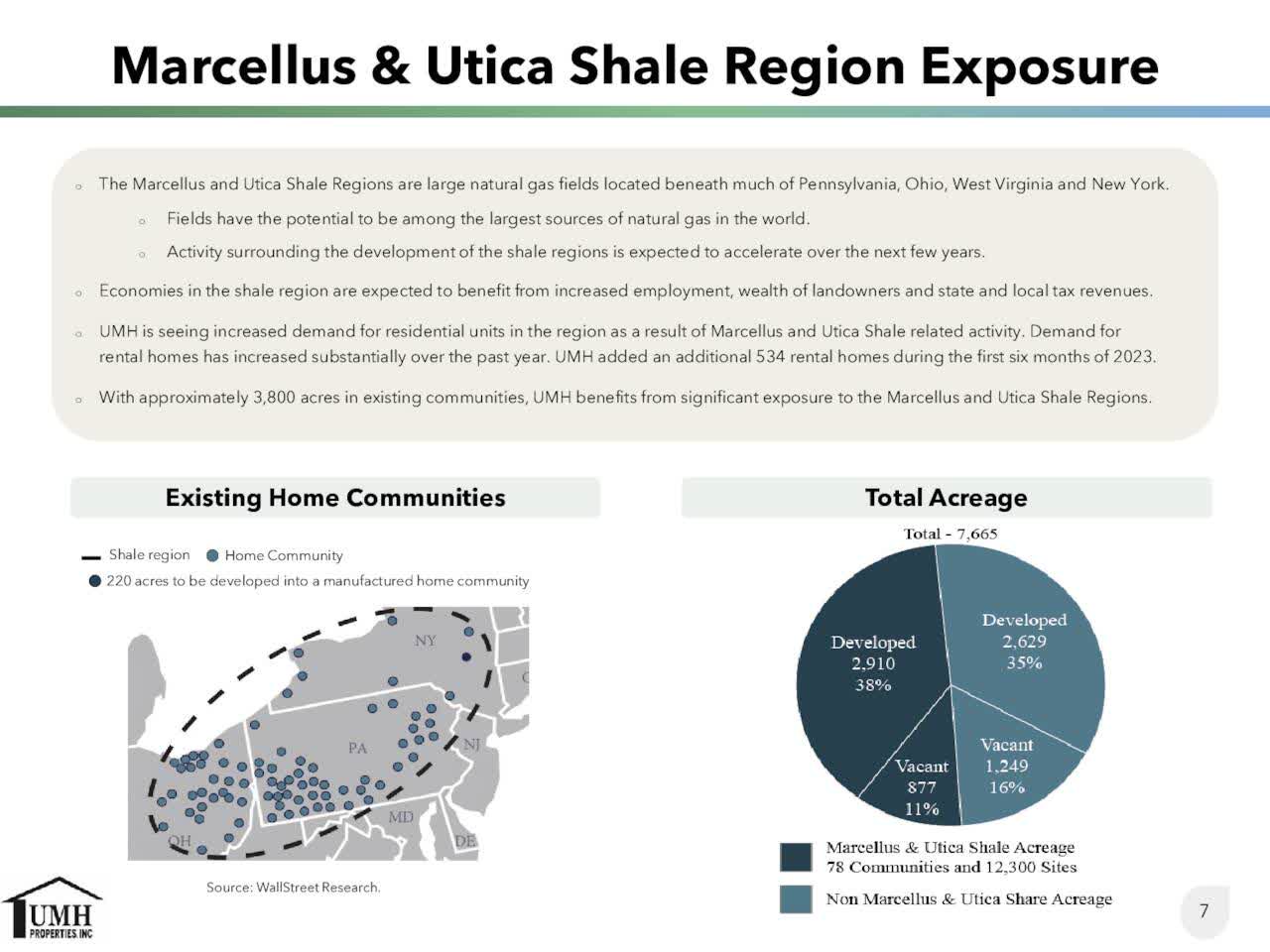

It is also worth noting that UMH Properties is ideally positioned to benefit from the shale oil boom in Marcellus and Utica shale regions. These regions, which are large natural gas fields located beneath much of Pennsylvania, Ohio, West Virginia and New York, have the potential to be among the largest producing areas of natural gas in the world.

Positioning of UMH Properties to Marcellus & Utica Shale Region (Investor Presentation)

{kind=link}

UMH Properties enjoys rising demand for residential units in this area thanks to increasing drilling activity. In the first six months of the year, the REIT grew its rental home count by 534, with no signs of fatigue on the horizon. Overall, the REIT has ample room for future growth in this area.

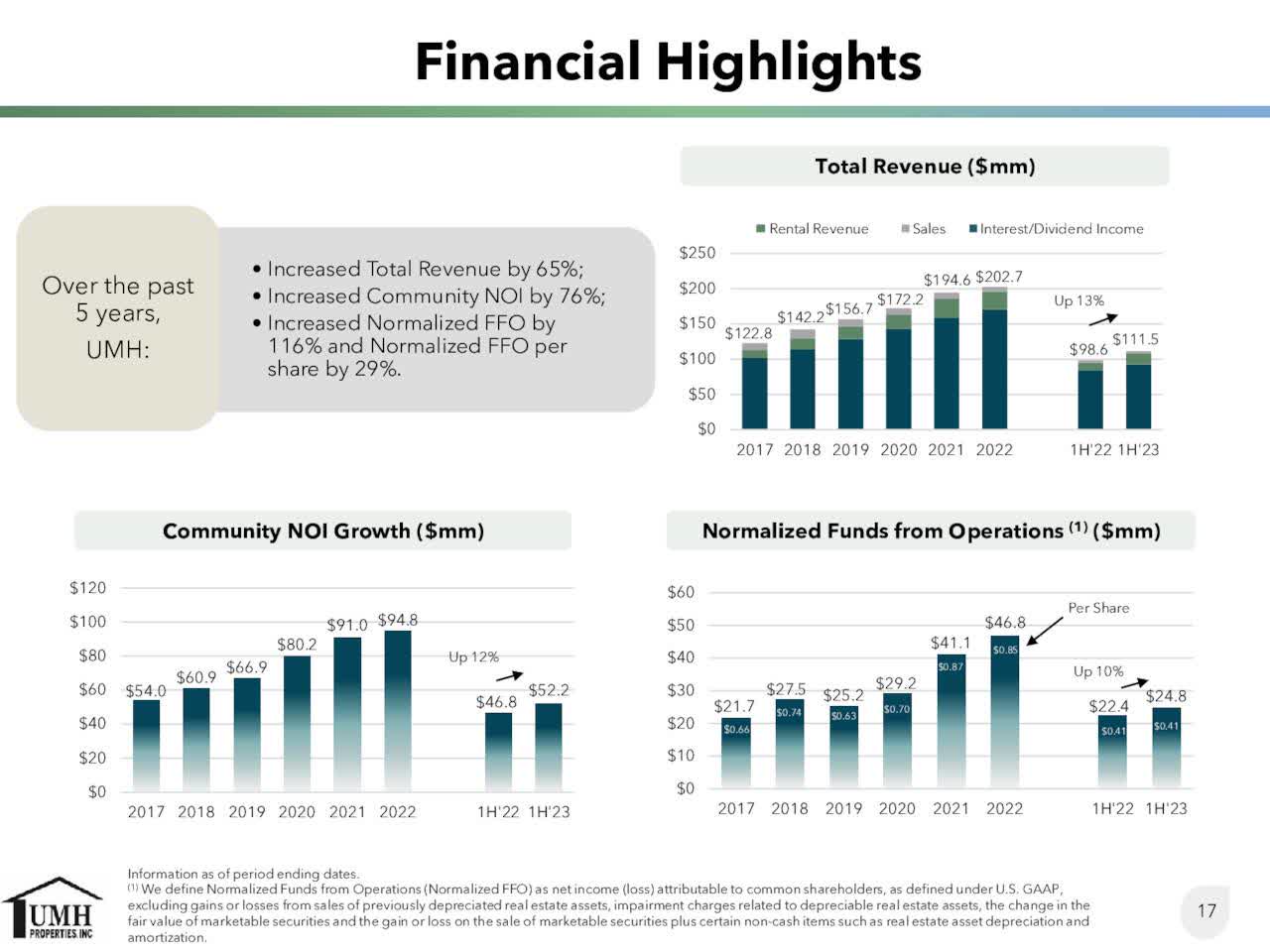

It is also important to note that UMH Properties has exhibited a consistent performance record over the last five years.

Financial Highlights of UMH Properties (Investor Presentation)

{kind=link}

During this period, the REIT has grown its revenue and its net operating income every single year, for total growth of 65% and 76%, respectively. The trust has also grown its FFO per unit by 29% over the last five years. The consistent performance record is a testament to the strength of the business model of the REIT and its reliable growth trajectory.

Moreover, UMH Properties currently enjoys strong business momentum. In the second quarter, it grew its rental income and its sales of manufactured homes by 11% and 18%, respectively, over the prior year's quarter. It also grew its same-property net operating income by 13% and enhanced its same-property occupancy from 86.0% to 87.9% while it reduced its same property expense ratio from 42.0% to 40.1%. As a result, the REIT grew its funds from operations [FFO] per unit from -$0.01 in the prior year's quarter to $0.21.

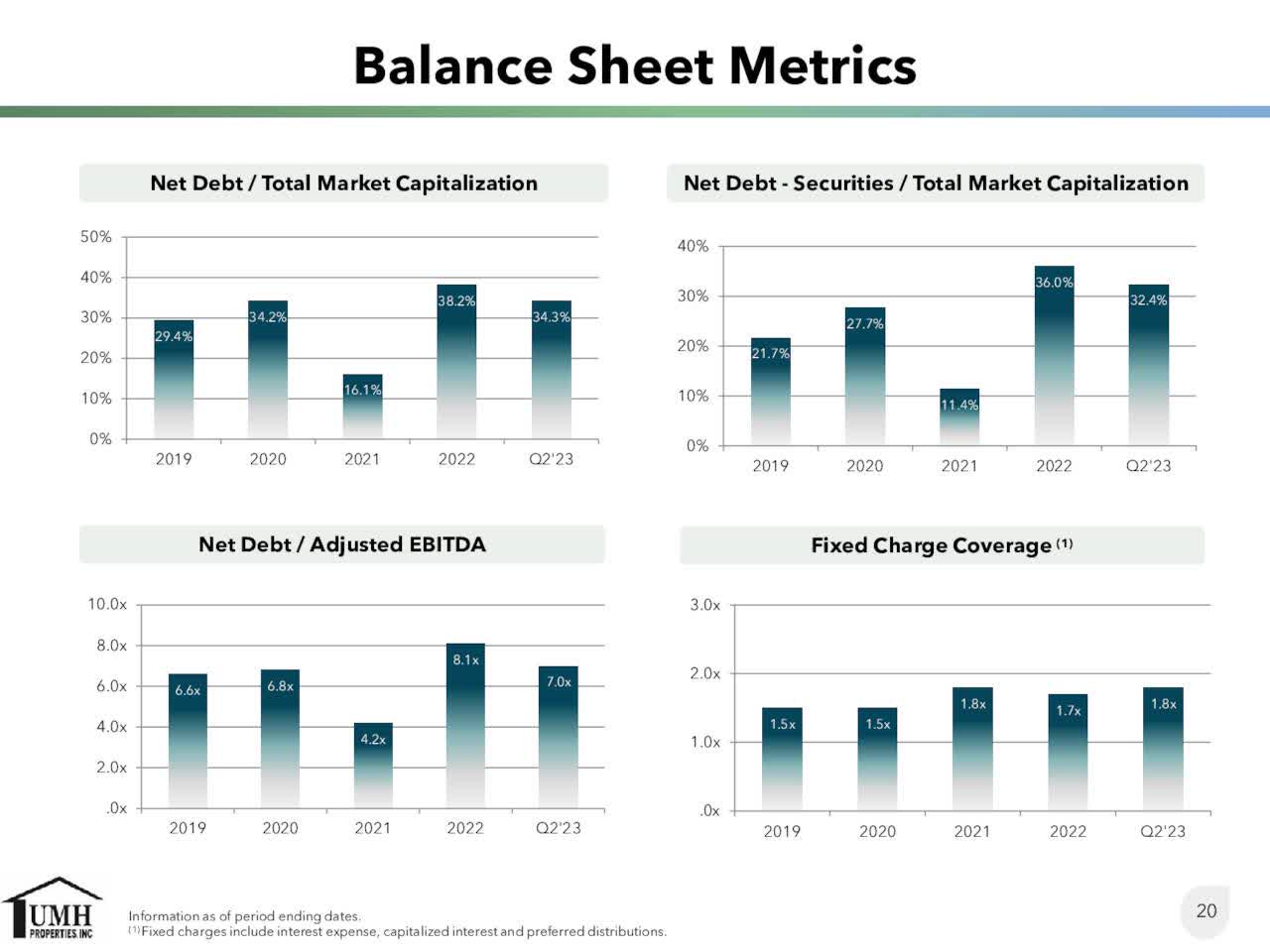

As mentioned above, UMH Properties had accumulated a high debt load due to an abnormally high number of orders of new homes, which resulted from supply chain disruptions during the coronavirus crisis. However, the REIT began to sell its houses at a fast pace in the second quarter and thus it drastically reduced its debt load.

{kind=link}

As shown above, UMH Properties reduced its leverage ratio (Net Debt to EBITDA) from 8.1x at the end of 2022 (and 7.7x in the first quarter) to 7.0x now. It also reduced its net debt to total market capitalization ratio from 38.2% at the end of 2022 (and 38.1% in the first quarter) to 34.3% now. Moreover, management recently provided guidance for further improvement in FFO per unit and a further reduction in debt levels and interest expense thanks to a great backlog.

Analysts seem to agree on the positive outlook of management. They expect the REIT to post nearly all-time high FFO per unit of $0.86 this year and grow its FFO per unit by 11% in 2024 and by 8% in 2025. Overall, UMH Properties appears to be on a reliable growth trajectory.

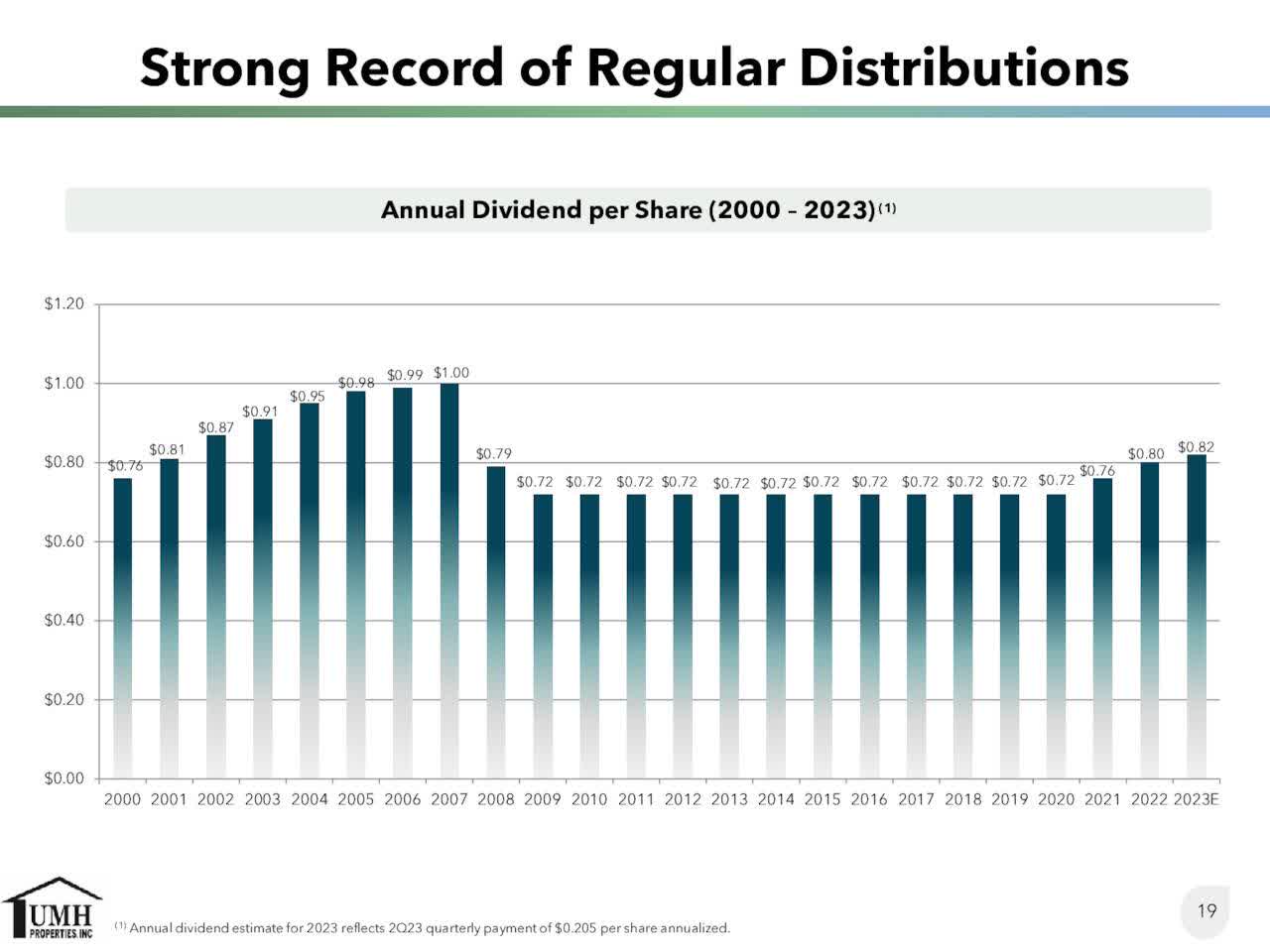

Dividend

The common stock of UMH Properties has a remarkable dividend record, as shown in the chart below.

{kind=link}

The REIT slashed its common dividend by only 28% during the Great Recession, which was the worst housing crisis of the last 90 years. This is a proof of the resilience of UMH Properties to recessions. Indeed, manufactured homes enjoy decent demand during rough economic periods thanks to their appealing prices.

UMH Properties currently has an AFFO payout ratio of 78% , which is somewhat high. However, thanks to the improving business momentum, the payout ratio is likely to decrease in the upcoming quarters. Moreover, in the last two conference calls , management has stated that it expects to keep growing the common dividend in the upcoming years. To cut a long story short, investors should rest assured that the common dividend of UMH Properties is not likely to be eliminated. As long as the common dividend is not eliminated, the preferred dividend is absolutely safe, as per regulations. Therefore, the 7.7% preferred dividend of UMH Properties appears to have a wide margin of safety.

Risk

As mentioned above, UMH Properties has proved resilient to recessions, including the Great Recession in 2008-2009 and the coronavirus crisis in 2020. Consequently, a potential recession does not pose a threat to the preferred dividend of the stock.

The only material risk factor for the preferred stock of UMH Properties is the adverse scenario of sticky inflation for years. In such a case, the Fed will probably keep interest rates exceptionally high and thus the 7.7% preferred dividend of the REIT will not be as attractive as it is under normal interest rates. In other words, investors should not worry about the safety of the preferred dividend but they should realize that the yield of the preferred stock will lose part of its attractiveness if interest rates remain around their 16-year highs for years.

However, the Fed has clearly prioritized restoring inflation to 2.0%-2.5%. Thanks to its unprecedented pace of interest rate hikes, the central bank has reduced inflation from a 40-year high of 9.2% last summer to 3.7% now. Given the focus of the Fed on taming inflation, the central bank is likely to accomplish its goal at some point in 2024 or 2025. As soon as it achieves its goal, the Fed is likely to begin reducing interest rates towards normal levels. When that happens, the preferred stock of UMH Properties is likely to rally towards its par value of $25, where it was trading until September 2022.

Final thoughts

The preferred stock of UMH Properties has shed 13% in the last 12 months due to somewhat more persistent inflation than initially anticipated. As a result, the preferred stock is now offering a 7.7% dividend yield. Investors should lock in the exceptionally high yield of the preferred stock of UMH Properties and wait patiently for inflation and interest rates to moderate. When that happens, the 7.7% yield on cost will probably be combined with a rally of the preferred stock from $20.80 towards its par value of $25.

For further details see:

The 7.7% Preferred Dividend Of UMH Properties Has Become Even More Attractive