AES - The AES Corporation: Promising Initiatives Are In Place Hold Until They Pay Off

2024-01-02 17:34:24 ET

Summary

- AES Corporation has underperformed the S&P500 by 33.18% in the past year due to heavy debt and poor profitability.

- The company is subject to regulatory uncertainty in the energy sector, particularly with the proposed clean-energy subsidy rules by the Biden administration.

- AES is implementing measures to improve profitability, including selling non-core assets, reducing debt, and increasing investments in renewable energy. However, patience is recommended before investing in the stock.

Investment Thesis

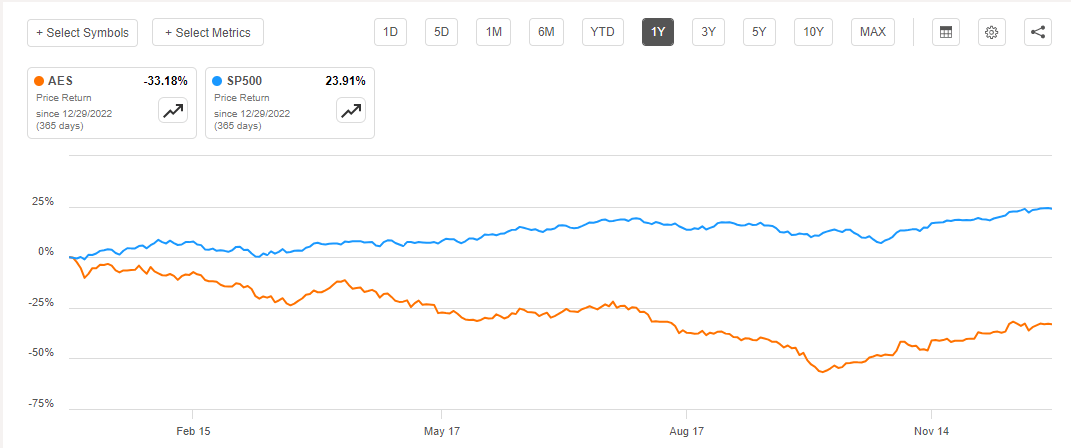

The AES Corporation ( AES ) is down about 33.18% over the last year underperforming the S&P500 by a margin of about 57%.

{kind=link}

This might be because of its heavy debt load and poor profitability, in my opinion. These factors, along with the hazy regulatory landscape in the energy sector, may have contributed to the underwhelming stock performance, in my view.

Although the company's impressive dividend history may be a strong argument for investors to purchase this stock, I believe that investors should exercise patience as the company takes steps to become profitable and pay down its debt, particularly in light of the current inflationary climate. Furthermore, I believe that there is a great deal of uncertainty regarding this company's prospects due to the unpredictability surrounding the legislative landscape. In light of this, I recommend holding this stock until its debt load decreases and its profitability improves.

The Regulatory Landscape

Numerous challenges and uncertainties have emerged in the energy sector as the world moves toward a more sustainable, lower-carbon future, with the regulatory landscape being one of the most significant. AES, as an industry player, is subject to the effects of the industry's dynamic regulatory environment . To explain this aspect, as an example, I'll use the strict climate subsidy regulations put forth by the Biden Administration, which are among the most recent pieces of proposed legislation.

The Biden administration recently proposed a set of strict rules for a clean-energy subsidy that would benefit hydrogen producers who use renewable electricity to make green hydrogen, a low-carbon alternative to fossil fuels. The rules are part of the Inflation Reduction Act , a major climate legislation that aims to reduce greenhouse gas emissions and promote clean energy in the US.

AES is a global power company with power plants in 15 countries , including the United States. It has also made investments in renewable energy projects such as wind and solar, and it intends to build green hydrogen facilities in collaboration with other companies. This implies that with its existence in the US, it is subject to the impact of this legislation.

The impact of Biden's strict climate subsidy rules on AES depends on how well it can meet the criteria for the tax credit, which requires the use of 100% renewable electricity to produce green hydrogen. If it can comply with the rules, it could benefit from the subsidy, which could cover more than half of the cost of a typical green hydrogen project. This could help it expand its green hydrogen business and reduce its carbon footprint. However, if it cannot comply with the rules, it could lose out on the subsidy and face competition from other companies that can qualify for the tax credit. This could limit its growth potential and market share in the green hydrogen industry.

In light of this, let's examine AES's position to ensure that it gains from this policy and does not lose out to rivals who might be eligible. The company along with Air Products intends to develop new wind and solar energy sources to produce hydrogen as part of a $4 billion Texas initiative that would satisfy the requirements proposed by the Biden administration.

Therefore, AES is well positioned to benefit from the climate subsidy, as it demonstrates its commitment to clean energy and innovation. However, some energy companies and industry groups have warned that the strict rules could stifle the growth of the hydrogen sector and drive investment overseas. The company may face some challenges and competition in the hydrogen market, as well as regulatory uncertainty and public perception issues. In addition, the project is set to begin commercial operations by 2027 which could be too late to reap the full benefits of this policy unless it extends its life span without amendments until then.

This example clearly shows the uncertainties that revolve around the regulatory environment because the viability of some legislation is not definite. Further, some regulations may be enacted and find some companies weakly prepared and eventually lose their market share and competitive advantage to their competitors who are favored by these policies, AES not being an exclusion.

Weak Profitability

The following indicators demonstrate AES's recent struggles with profitability:

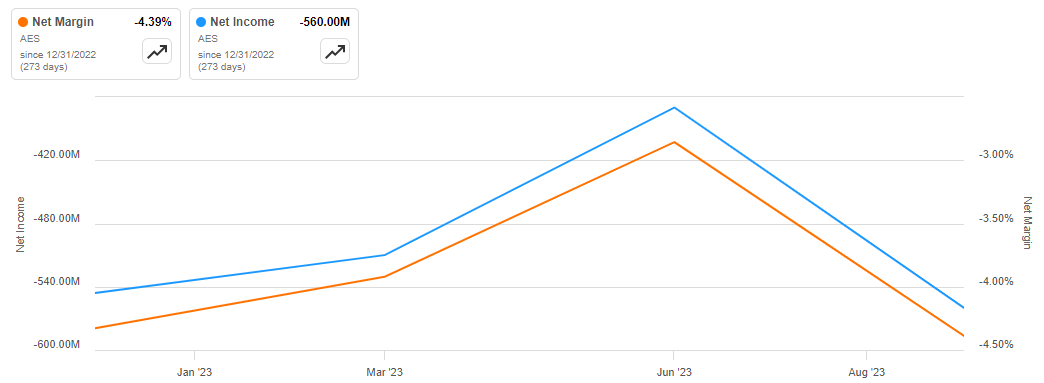

- The company's net profit margin, which measures how much of its revenue is left as net income after deducting all expenses, has been trending down recently and remained below zero in the third quarter of 2023. This means that the company is losing money on every dollar of sales.

{kind=link}

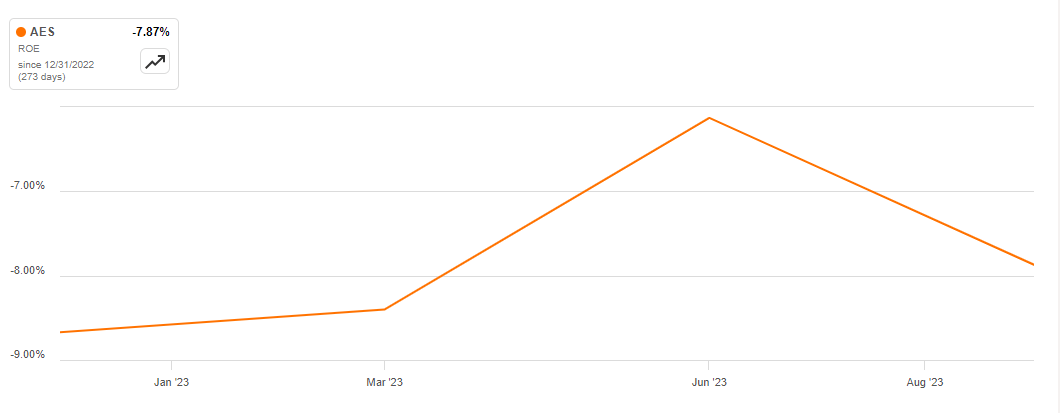

- Its return on equity, which measures how well it uses its shareholders' funds to generate profits, is also negative and trending downwards, and declined further in the third quarter of 2023. This means that the company is destroying shareholder value.

{kind=link}

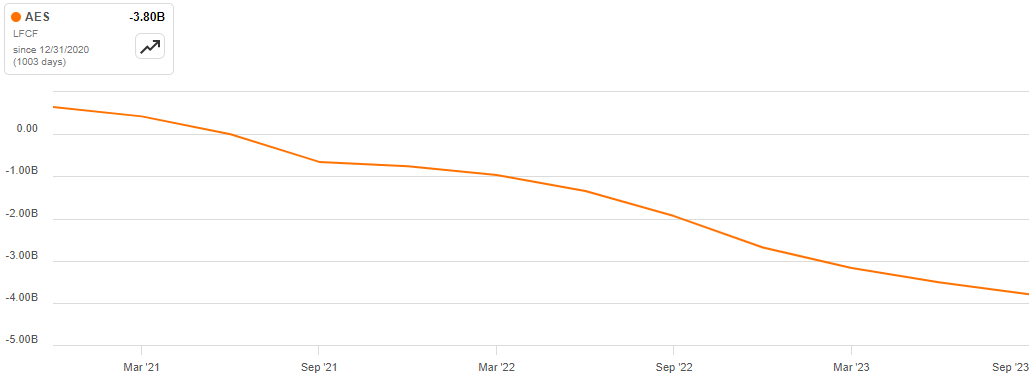

- The company's free cash flow, which measures how much cash it generates from its operations after investing in capital expenditures, has been negative since 2021 and turned even more negative in the third quarter of 2023. This means that the company is spending more cash than it is generating.

{kind=link}

Given this weak profitability, I think this could be due to several reasons such as;

- The company has a high level of debt, which increases its interest expenses and reduces its financial flexibility. As of today, the company has a total debt of $27.39 billion, which is more than four times its total equity of $6.679 billion and more than eight times its EBITDA, indicating a high debt risk. Its interest total expenses have increased from $911 million in 2021 to $1.27 billion TTM, marking a net impact of about $359 million on its profit margins.

- High capital expenditure. The company has invested heavily in renewable energy projects, such as solar, wind, and hydro, which require large upfront costs and long payback periods. Its CAPEX / Sales ratio is 55.92% TTM, much higher than the sector median of 30.07%.

- Unusual items: AES has incurred significant losses from unusual items, such as impairments, restructuring charges, and litigation settlements. These items reduced the company's net income by $1.42 billion in the TTM.

These factors have negatively affected the company's profitability metrics, such as its gross profit margin, net income margin, return on equity, and free cash flow margin. Its profitability score, which consolidates various profitability indicators into one single number, is 47/100, below the sector average of 60/100.

Turnaround Measures

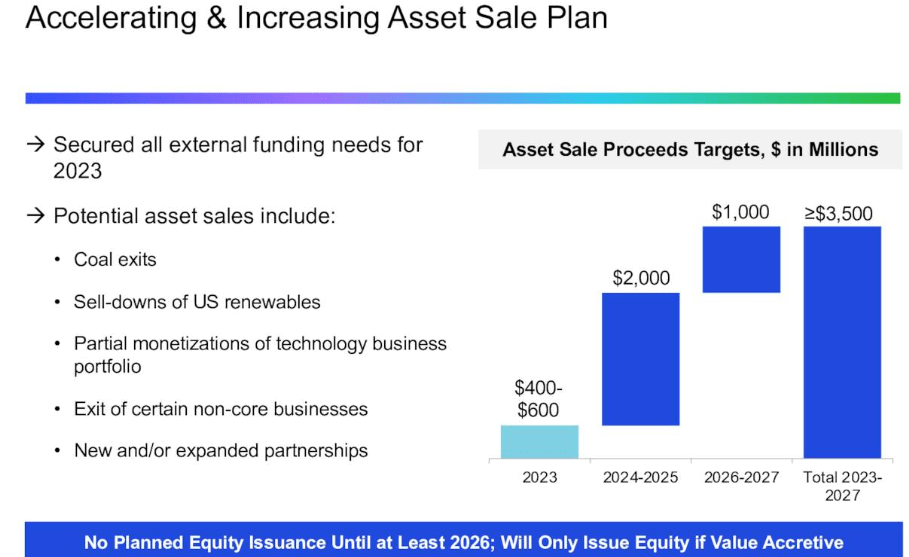

Although this company's profitability has been a concern, it appears that the management has taken some steps to optimize resources and achieve efficiency to improve profitability. To begin with, the company has been pursuing a strategy of simplification and focus, which involves selling or exiting non-core or underperforming assets, reducing its debt and leverage, and increasing its investments in renewable energy and digital solutions. The company expects to generate $2 billion from asset sales by 2024 and 2025 and reduce its net debt to EBITDA ratio to below 3.0x. It also intends to phase out coal entirely by the end of 2025, triple its renewables portfolio by 2027, and improve customer experience and operational efficiency through digital transformation.

{kind=link}

Secondly, AES has been maintaining a strong liquidity position and a disciplined capital allocation policy, which enables it to weather market volatility and fund its growth initiatives. As of today, the company has $2.3 billion of cash and cash equivalents. The company also has a payout ratio of 43.66% and retains the rest for reinvestment.

Lastly, the company has been leveraging its competitive advantages and growth opportunities in its markets, such as its diversified portfolio , its long-term contracts, and customer relationships.

{kind=link}

The company believes that it can deliver an average annual growth rate of 7% to 9% in its adjusted earnings per share and 10% to 12% in its free cash flow per share through 2025.

In conclusion, AES has been facing profitability challenges due to its high debt, among other reasons. However, the company is implementing various measures to improve its financial performance and position itself for long-term growth and value creation. I am confident in its turnaround strategies such as the selling or exiting of non-core or underperforming assets. This will not only help the company exit what has been cost centers but also raise capital to fund other high-quality projects. Further, its long-term contracts give the company financial visibility in the future. I am optimistic about the company's long-term performance in light of its development projects and turnaround initiatives.

Bottom Line

Profitability concerns, a high debt burden, and regulatory uncertainty in the energy sector are currently plaguing AES. However, I am optimistic about the company's long-term prospects because it is implementing measures to optimize resources and reduce debt. Furthermore, given that the current legislative changes are aimed at encouraging and promoting safer and cleaner energy, the company's massive transformation to triple its renewable portfolio by 2027 will be in line with these policies, potentially putting the company in a better position to reap the benefits of such policies and use them as a competitive advantage. However, given that these initiatives and development plans are long-term in nature with longer payback periods, I recommend patience before investing in the stock until its turnaround measures pay off, perhaps, when it achieves profitability and sustains it.

For further details see:

The AES Corporation: Promising Initiatives Are In Place, Hold Until They Pay Off