ADM - The Andersons Inc.: Stock Remains On My Watchlist Despite Cash Concerns

Summary

- ANDE's trade group continues to bring in more revenues as compared to the Plant Nutrient segment.

- The bolt-on acquisitions of Bridge Agri and Mote Farm were the highlights of Q3 2022.

- ANDE's expansion into the UK is strategic to support the US and Canadian grain market.

The Andersons ( ANDE ) recently announced earnings per share ('EPS') of $0.50 on revenue of $4.22 billion. This revenue topped expectations by $906.23 million. According to the earnings report, the sale of trade commodities, ethanol segments like corn, wheat, soybeans, oats, etc. (under ASC 815) outperformed revenues from specialty products like propane (under ASC 606) by $2.95 billion. The Andersons' shares are down 3.49% (YoY) and still down 38.18% from its 52-week high of $59.00.

Thesis

The Andersons, Inc is looking to capitalize on supply chain disruptions which are part of the disruptive market fundamentals expected to keep commodity prices at historical highs. ANDE is also evaluating its growth projects particularly aligned toward vital grain renewables, fertilizer sections, capital investments, and mergers & acquisitions (M&A). Ahead of its Q4 2022 earnings report slated for February 15, 2022; ANDE looks to end the FY 2022 with a stronger performance boosted by an improvement in base operations and investments.

Company overview and results analysis

The Andersons, Inc operates along three main business segments with two being the prominent revenue sources of the company. The first is the trade business which includes merchandising of commodities and terminal grain elevation operations. Within the first category is also found the renewable business sector that produces ethanol and related products. The second category contains the Plant Nutrient manufacturing business that deals with among other things fertilizers, corn-based products, and the distribution of agricultural inputs. Inevitably, the ongoing Russian-Ukraine war has led to a surge in fertilizer prices since Russia is a primary manufacturer of this commodity globally.

Revenue from Russian fertilizer exports in 2022 surged 70% (YoY) to $16.7 billion due to the increase in prices. ANDE’s Plant Nutrient segment recorded a decrease in operating income by $5.8 million from 2021 with gross profit in the sector dropping by $3.2 million. However, the segment realized an increase in sales and merchandising revenue that was primarily due to the 45% (YoY) growth in fertilizer prices.

ANDE has 5 ethanol plants charged with the processing of corn into ethanol. It falls under the renewables segment and is dubbed cheap, clean-burning, and high-octane fuel. The company consistently works to achieve a clean-burning concentration of this fuel considering that it makes up at least 10% of US gasoline. Estimates by the US Energy Information Administration ('EIA') indicated that 13.94 billion gallons of ethanol were found in 134.83 billion gallons of US motor gasoline consumed in 2021. This estimate shows that approximately 10% of ethanol is contained in US gasoline. Thus, raising the proportion of ethanol in gasoline would not only be good for business but would also mean the product would attain a higher percentage of clean fuel.

Additionally, ANDE managed to lower inventories of ethanol and grain products in the nine months leading to September 30, 2022, as opposed to propane and plant nutrients.

The Andersons

The reduction in inventory shows increasing demand in the period which was also followed by improved earnings. Robust ethanol margins in Q3 2022 ensured that ANDE’s Trade EBITDA rose 38.63% (YoY) from $44 million in Q3 2021 to $66 million in Q3 2022. In the trailing 12 months period, ANDE’s adjusted EBITDA from its continuing operations hit almost $440 million with trades and renewables posting major improvements in the quarter.

M&A Strategy

ANDE announced two bolt-on acquisitions in Q3 2022; Bridge Agri was to operate in the trade group while Mote Farm Services was set in the Plant Nutrient category. Bridge Agri will operate on the more lucrative side of The Andersons as compared to Mote Farm Services. As noted earlier, the trade segment falls under the ASC 815 revenue. In the three months ending on September 30, 2022, revenues under ASC 815 rose 41.03% to $3.583 billion against $635.4 million recorded for commodities under ASC 606. In the nine months ending on September 30, 2022, revenues under ASC 815 grew 42.94% to $10.38 billion.

The Andersons

I expect the $20 million investment in Bridge Agri Partners to pay off since it seeks to expand ANDE’s existence in the pet food ingredient market. With this acquisition, the company now expands its presence in the central northern part of the US and Canada. I am also considering this deal in ANDE’s strategy of growing its core grain and fertilizer business segment. This sector also includes premium food and related feed offerings.

Favorable Market Conditions

I am invested in Archer-Daniels-Midland ( ADM ) Company which increased its stake in the pet nutrition industry through its acquisition of Chinese firm Invivo Sanpo. ADM reported in its Q3 2022 results that operating profit in its nutrition segment rose 1% in the quarter due to high demand for plant-based proteins. Latin America posted lower results due to volume concerns but it was offset by robust volumes and marginal growth in North America. We can also factor in low demand from China due to sustained lockdowns in 2022. However, lifting these restrictions will raise demand and production levels in the greater Asia-Pacific region into 2023.

The global pet food industry was valued at $110.53 billion in 2021 and was expected to reach $163.70 billion in 2029. It is supposed to grow at a CAGR of 5.11% from 2022 to 2029. With this understanding, I expect Bridge and Mote Farm to be financially accretive in 2023 since they align with ANDE’s growth strategy.

The UK is also turning out to be a strategic manufacturing location for the Andersons and may soon attract considerable demand. In the Q3 2022 earnings call, CEO Pat Bowe explained that the UK subsidiary delivered stable organic feed business results. The company listed the Feed Factors Limited Company as one of its subsidiaries in the UK. It imports and distributes agricultural commodities such as fishmeal, oilseeds, grains, and derivatives. The expansion into the UK, alongside the US and Canada, is a strategic move considering the region’s high demand for organic feed. Despite the high cost of living, the forecast for the total cereal usage in the UK is set to hit 10.57 Mt from 219 Kt in 2023.

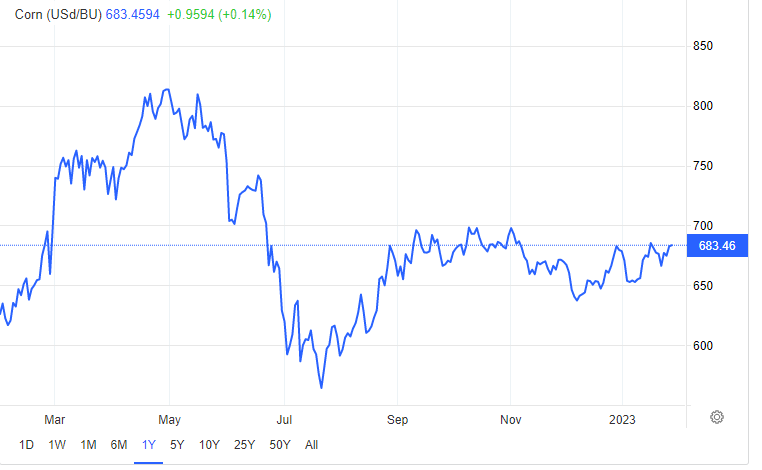

Global recessionary issues and competition in exports amid supply concerns continue to pile pressure on the European grain market. Still, renewed demand for grain in China post Covid19 related lockdown is likely to lower inventory into the year. Chicago corn futures in mid-January 2023 held above $6.7 per bushel close to its two-month high of $6.8 per bushel.

{kind=link}

The low supply of the commodity was caused by high production costs due to late planting in the US and the ongoing Russian invasion of Ukraine which accounts for at least 15% of the global corn exports. Global markets are dictating commodity prices in the US, Canada, and the UK, with future prices up on a marginal basis. However, prices are still below their 2022 peak levels.

Better Dividend yield

While considering the aspect of the partnership, The Andersons is continuously increasing its dividend payout to shareholders. The company declared a $0.185/ share quarterly dividend payable on January 20, 2023. This increase represented a 2.8% increase from the previous dividend of $0.18 and a forward yield of 2.15%. In the first 9 months of 2022, ANDE paid out $18.3 million in dividends up 4.6% (YoY) from $17.5 million paid in 2021.

{kind=link}

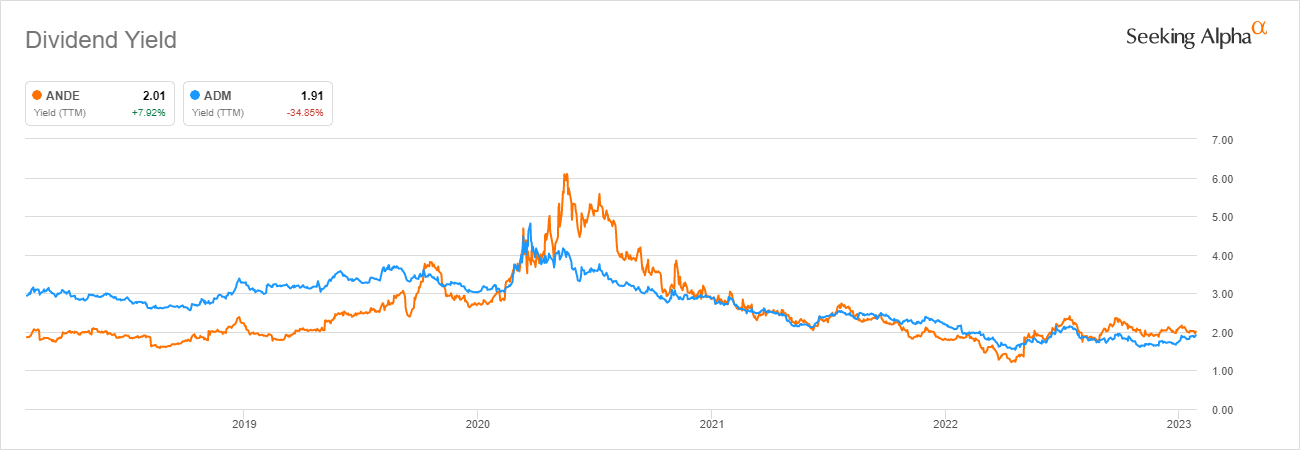

The dividend yield is yet to reach its record levels of +6% attained in 2020, although it seems the company’s payout record has been better than ADM’s. ANDE’s dividend yield stood at 7.98% ('TTM') as compared to ADM’s decline of 34.85% over the same period.

Risks to Consider

The Andersons is grappling with an increase in working capital that is eating into the quarterly cash flow generated from operations. Cash was reduced by 8.92% (YoY) due to capital concerns as a result of high commodity prices and business expansion. The company also has a lower short-term borrowing capacity as compared to Q3 2021. ANDE's short-term borrowing balance as of September 30, 2022, was $652.9 million supported by $1.1 billion in (ready) marketable inventories. This short-term debt has risen from $501.8 million recorded as of December 31, 2021, and $281.2 million incurred in the quarter ending on September 30, 2021. As seen, ANDE's short-term borrowing has grown 132.18% (YoY). However, about $1.98 billion had been made available to the company as of September 30, 2022 (as a line of credit) with the balance at $1.31 billion. Still, this borrowing capacity has been substantially reduced into 2023.

The Andersons’ long-term debt to EBITDA is below its target of 2.5. The bolt-on acquisitions of Bridge Agri and Mote Farm were stated to lower the rate to below 1.5. Additionally, cash used in operating activities rose 228.81% (YoY) in the nine months of 2022 to $153.4 million as compared to $119.1 million generated in the first 9 months of 2021. The net cash generated from investing activities also decreased 99.44% (YoY) to $2.9 million in 2022 from $519.52 million in 2021. The $2.9 million generated in this period is less than the $100 million planned for usage as CapEX for FY 2022. This consideration is vital since ANDE announced in its Q3 2022 earnings call that about $50 million will be needed as maintenance capital. Without considering the debt available, ANDE’s current cash balance of $147.7 million will support the company’s operations until August 2023. This understanding stems from the fact that it used up $153.37 million in its operations. However, the accounts receivables stand at $990 million which is adequate to help finance the operative business when converted into cash in the short-term.

Bottom Line

The Andersons’ performance in Q3 2022 was stable considering the company made two main acquisitions to boost its business segments. The trade group remains the company’s strongest revenue source with more work needed to support the Plant Nutrient section. I feel that the company will require additional capital to support CapEx into 2023 due to the high debt concerns. Still, the company has been raising its dividend yield better than ADM over the trailing twelve-month period. I will recommend a hold rating for the stock a before increasing my position as I await the Q4 and full-year financial release slated for mid-February 2023.

For further details see:

The Andersons Inc.: Stock Remains On My Watchlist Despite Cash Concerns