ANDE - The Andersons: Navigating Challenges Harvesting Success

2023-06-11 23:58:54 ET

Summary

- The Andersons continues to deliver strong performance in the agriculture industry, with its stock up 27% year-to-date and 45% since early 2022.

- Despite challenges in its joint venture with ICM, ANDE's overall ethanol business remains promising, and the Trade Group reported impressive earnings.

- While the Nutrient and Industrial business faced headwinds, future demand is expected to rebound, making ANDE an opportunity for investors looking to capitalize on agriculture tailwinds.

Introduction

The Andersons ( ANDE ) is one of my most important trades. Not because of its size, as it's very small compared to my large long-term investment, but because it's a stock I've been bullish on since the pandemic. Especially since early 2022, when the stock started to struggle, I wrote a number of bullish articles that reiterated my bullish view on ethanol, agriculture trade, and the company behind the ANDE ticker.

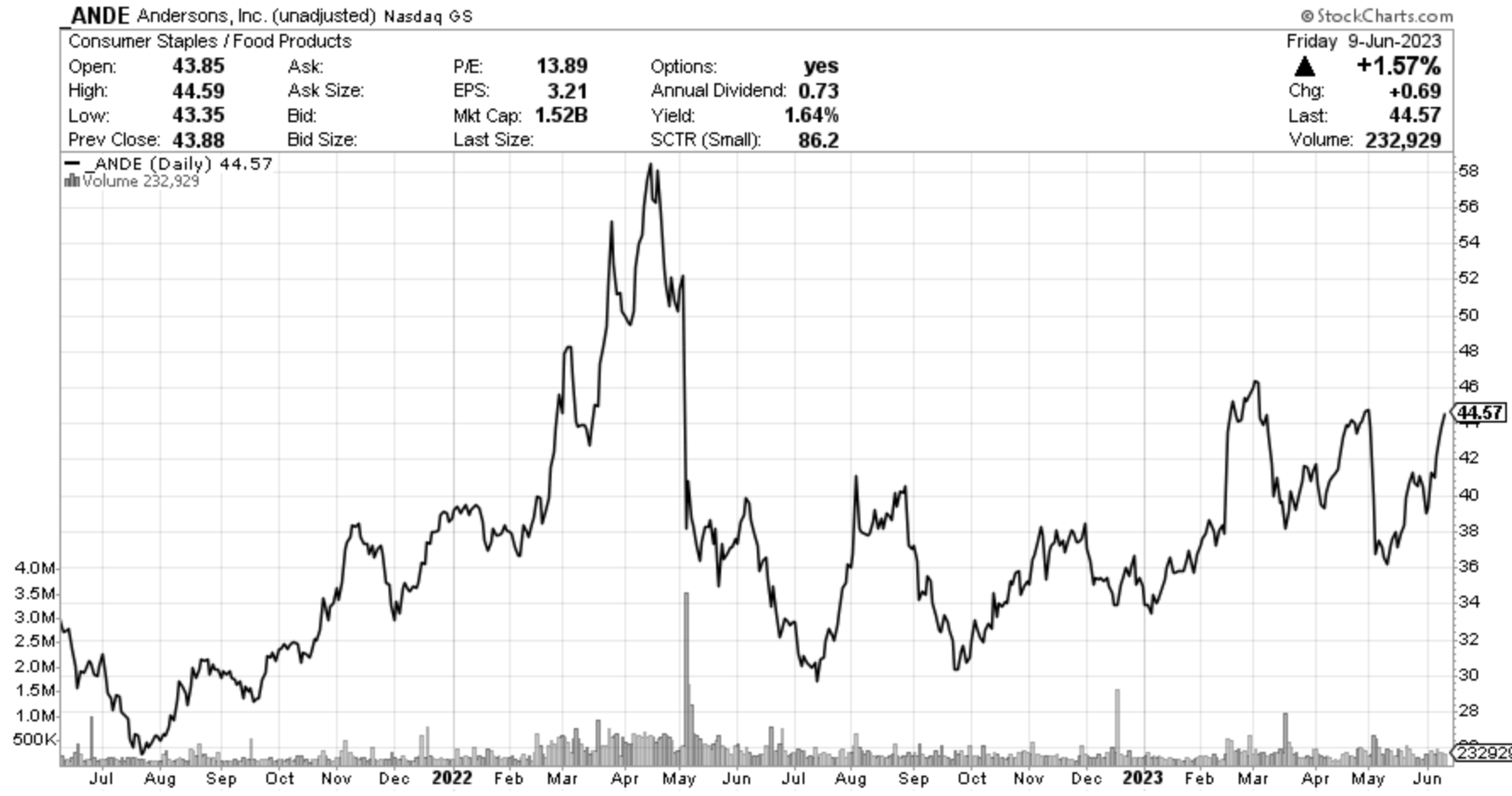

The good news is that the company continues to deliver. The company is just 4% below its 52-week high, 51% above its 52-week high, and up 27% year-to-date. The stock is up 45% since I wrote an article titled The Andersons: Moving Higher With Energy .

{kind=link}

Three months after writing my most recent ANDE article, it's time to update my bull case.

So, let's get to it!

Why I Care About ANDE

The Andersons isn't a large company - at least not compared to most of the companies you may have on your radar or in your portfolio.

With a market cap of $1.5 billion, ANDE is a dwarf compared to some of its larger peers.

However, ANDE isn't insignificant. Founded in 1947, the company is a heavyweight in the American agriculture industry.

{kind=link}

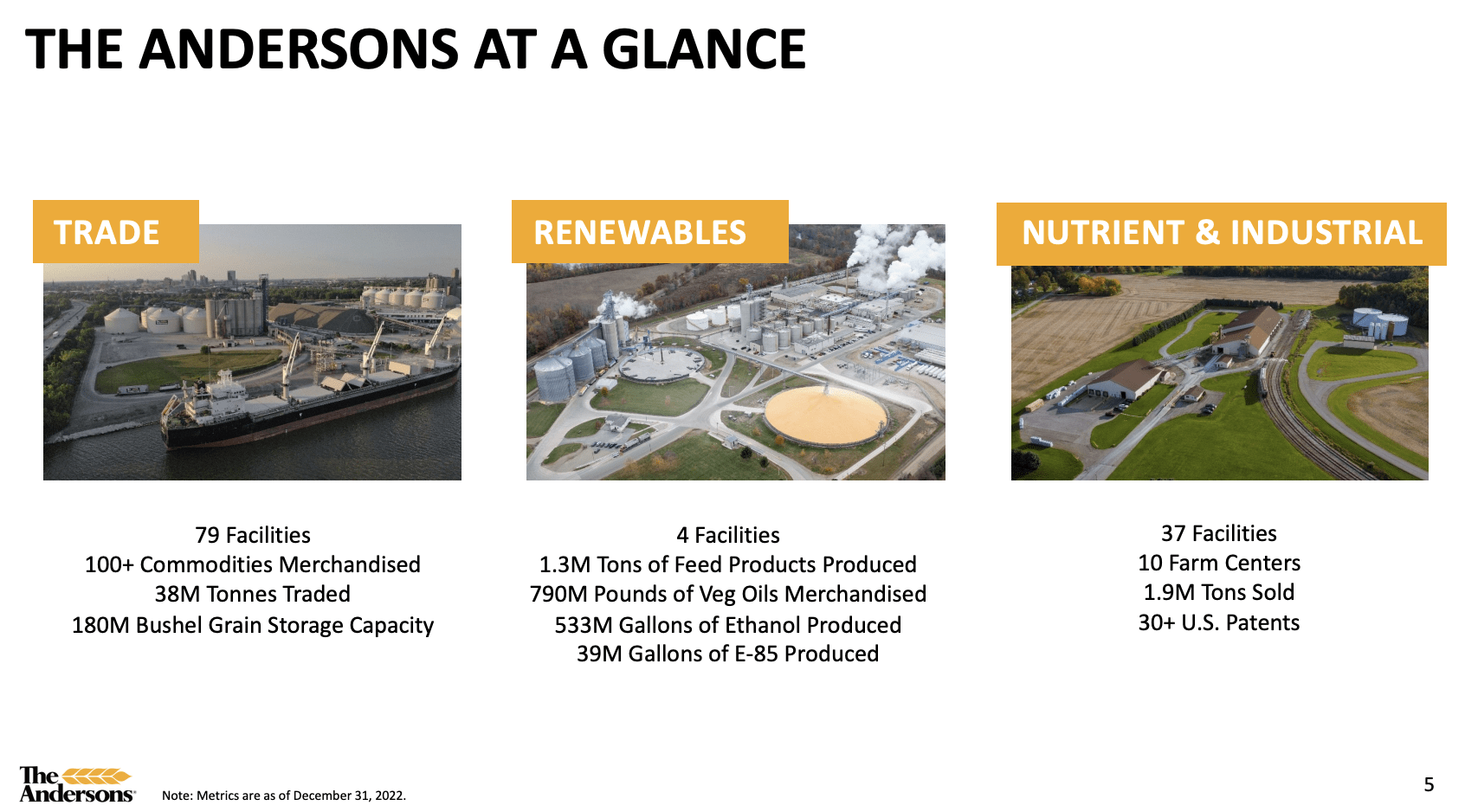

The company operates 79 trade facilities, which can handle roughly 180 million bushels of grain. It has four ethanol facilities producing more than 530 million gallons of ethanol per year and 37 facilities that provide farmers with fertilizers and related products.

In 2022, 75% of its revenues came from the trade segment.

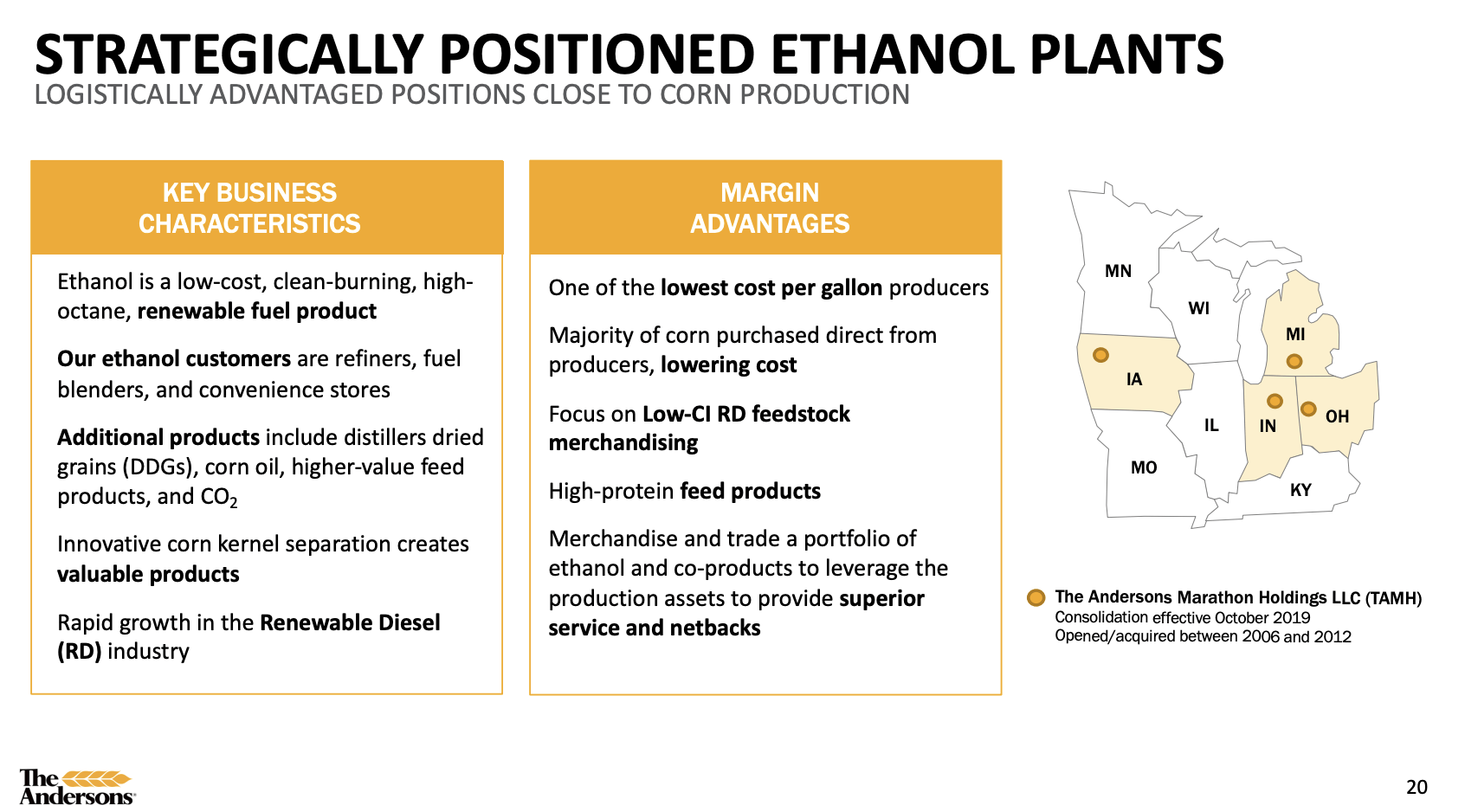

Through the aforementioned ethanol segment, the company connects farmers to energy markets and buyers of byproducts like high-protein feedstock.

{kind=link}

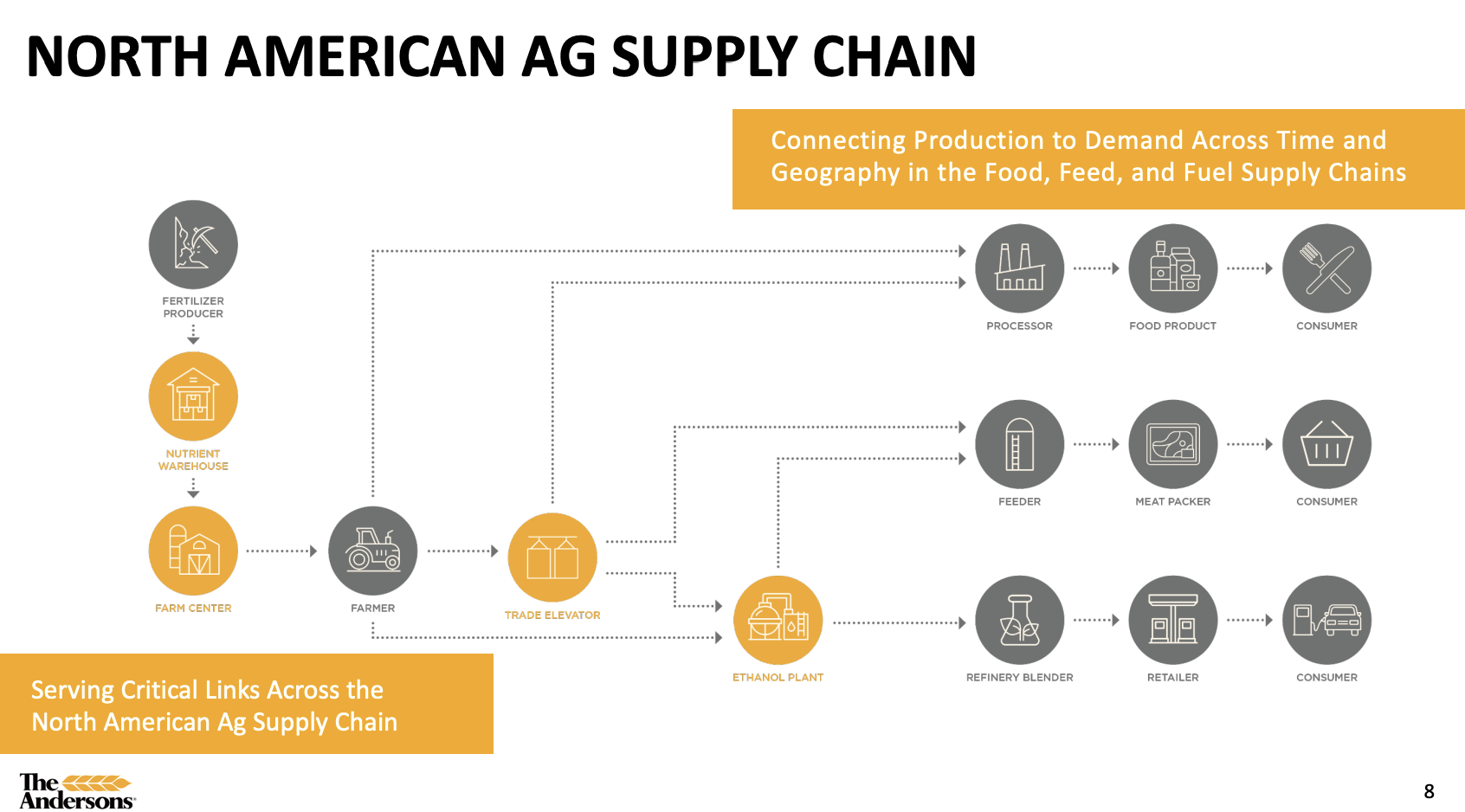

Furthermore, as the handy overview below shows, the company connects fertilizer producers to farmers and provides essential services like storage and ethanol production to support industrial companies, consumer product companies, and others further down the value chain.

{kind=link}

In other words, even if people don't care about investing in ANDE, we can learn a lot from this company, as it can tell us so much about the health of the agriculture industry. So, even if I didn't have a position in the company, I would still follow it.

ANDE Is Back

In the first quarter, the company's performance remained strong, with trailing 12 months adjusted EBITDA exceeding $411 million. The Freight Group and merchandising teams had a successful quarter, and the premium food and feed ingredients business delivered improved results.

The renewables business benefited from good merchandising of ethanol and co-products, as well as growing volumes in renewable diesel feedstock merchandising.

However, the nutrient and industrial segment experienced a slow quarter due to buyers delaying fertilizer purchases and increased interest rates affecting customer timing.

Despite these challenges, I'm not worried. The timing aspect was mentioned by all major fertilizer producers. We should see stronger numbers in the second quarter, as affordability has improved significantly.

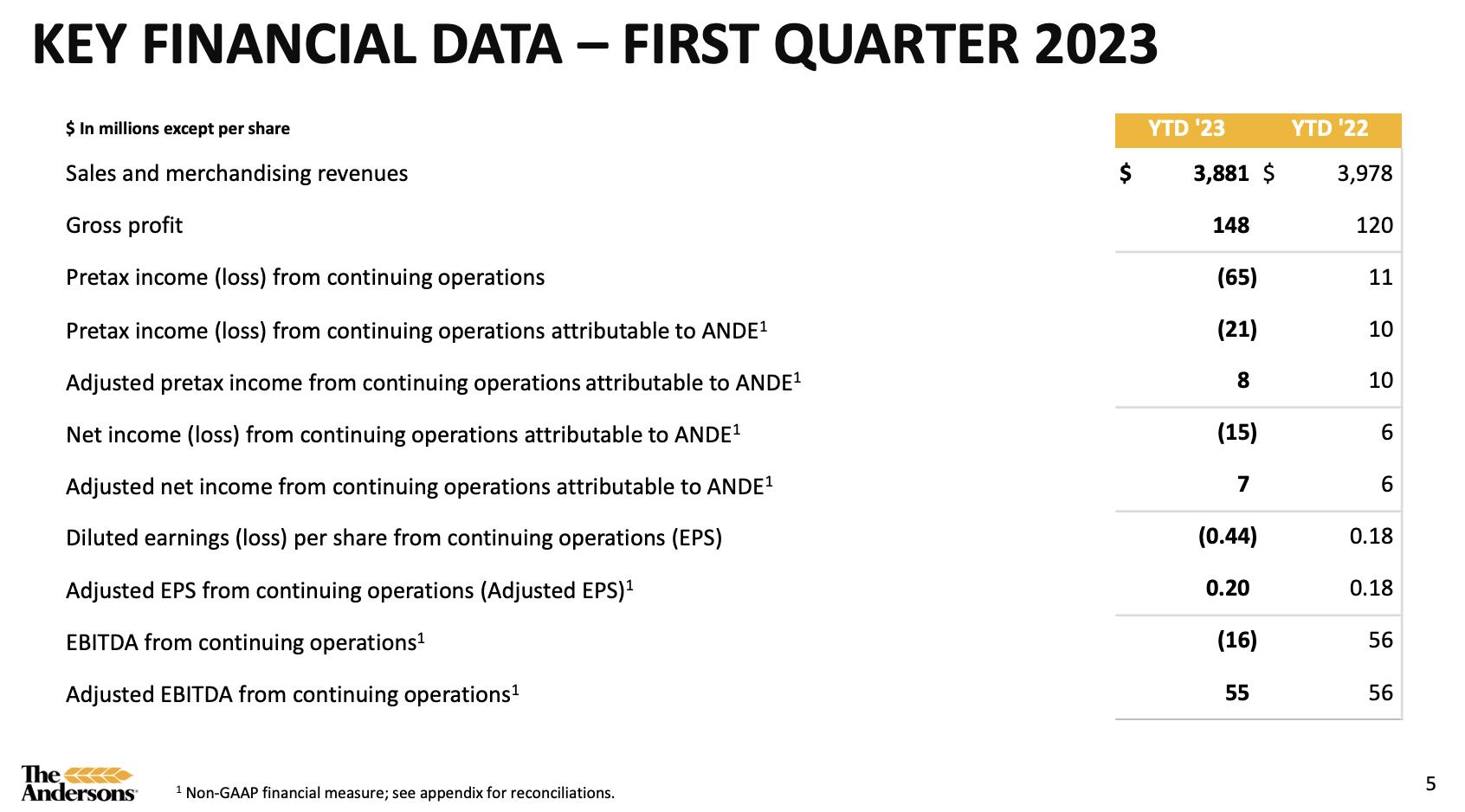

Zooming out a bit, the company reported a net loss from continuing operations of $15 million or $0.44 per diluted share, with adjusted net income of $7 million or $0.20 per diluted share. The adjusted EBITDA for the quarter was $55 million, similar to the previous year.

{kind=link}

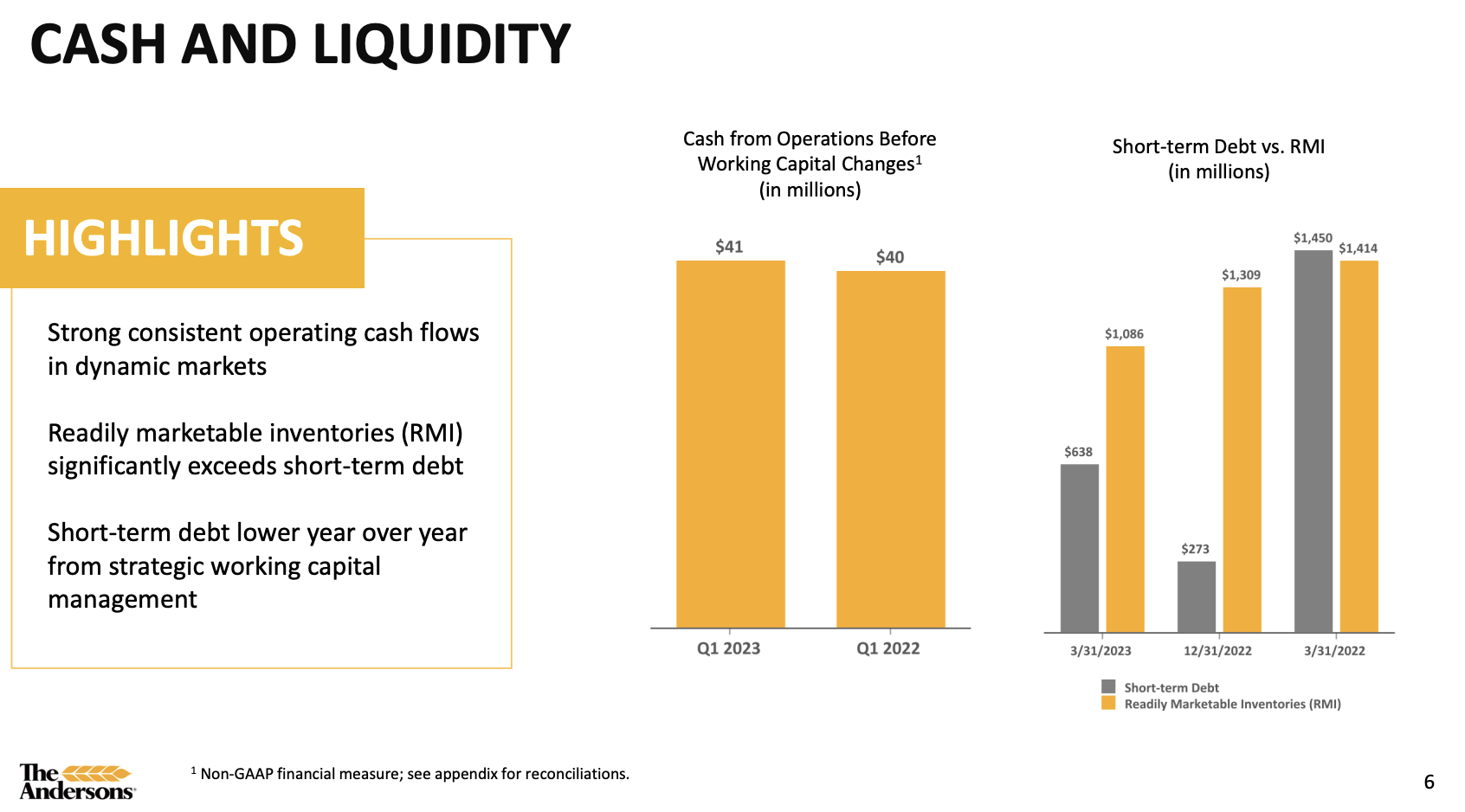

The Andersons had over $1 billion in readily marketable inventory, partially financed by $638 million of short-term debt. The long-term debt to EBITDA ratio was about 1.4x, well below the company's target of 2.5x. Note that readily marketable inventories are very valuable in this industry. Investors know that if needed, these can be sold at somewhat predictable prices. After all, these inventories are mainly grains, ethanol, and related commodities. That also explains why almost all companies in this industry mention the value of their RMIs.

{kind=link}

Furthermore, the company planned approximately $125 million in capital spending for the year, with a focus on maintenance capital. After all, its restructuring is going well, which erases the need for growth CapEx.

Also, the company reported issues related to its ELEMENT joint venture. In April, Seeking Alpha reported that the joint venture (ANDE holds a 51% stake) was placed into receivership.

In its first-quarter earnings call , the company elaborated on this issue.

Essentially, the Element facility, a joint venture with ICM, faced various challenges that led to the decision to put it into receivership. Operational challenges and market-based challenges impacted profitability, including a significant shift in California's low carbon fuel standard credits and high Western corn basis prices. Bear in mind that ethanol production is finding a balance between corn input costs and ethanol prices.

As a result, the company made noncash pretax impairment charges on the long-lived assets of the facility and is currently working through the receivership process.

However, despite these challenges, the company remains bullish on the rest of its ethanol business, particularly in the East. It also emphasized that this specific joint venture's failure does not change its longer-term forecasts, which is good news as this seems to be an issue specifically related to regulatory headwinds in California. After all, margin headwinds also impacted ethanol producers solely focused on the Corn Belt.

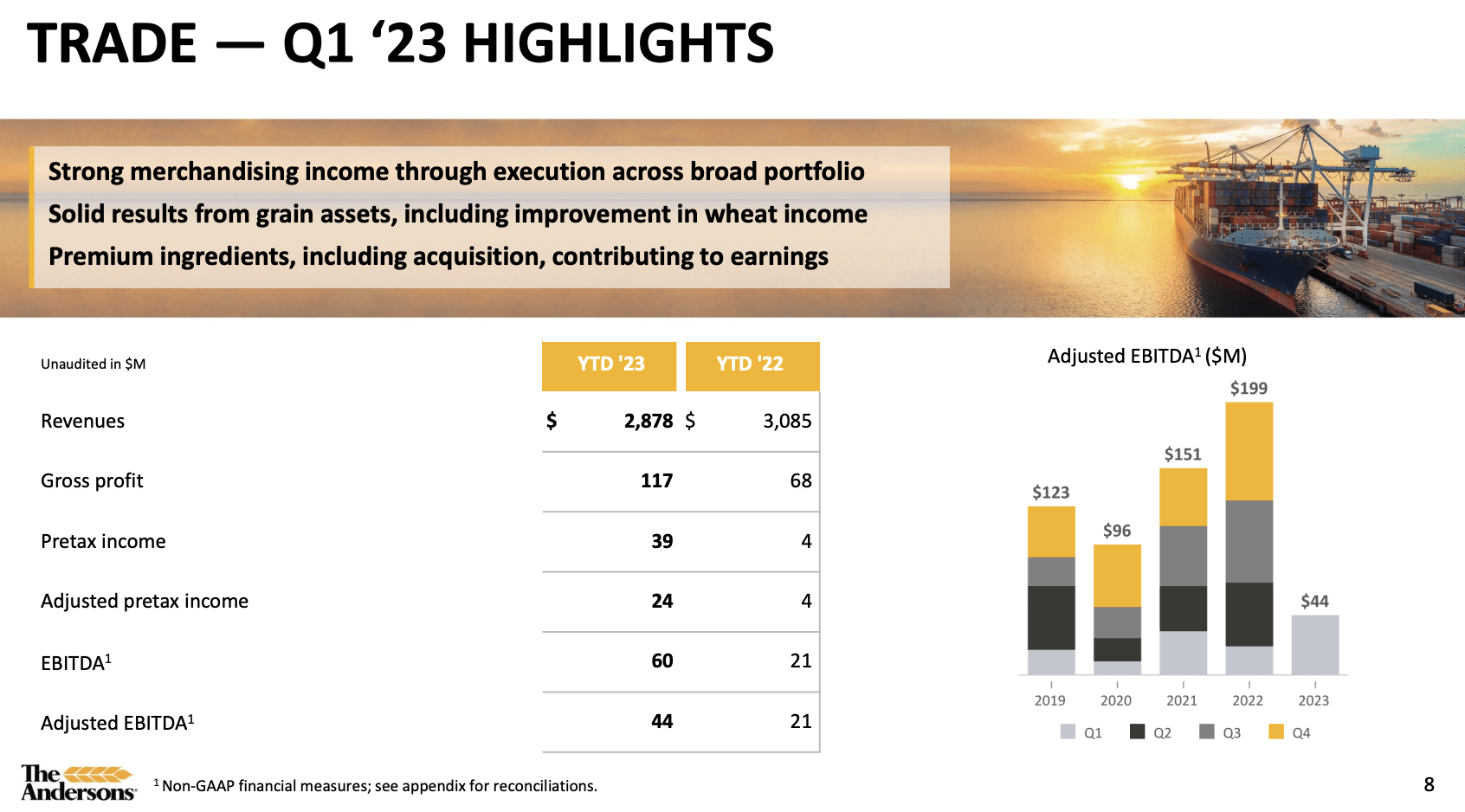

With all of that said, let's discuss the first-quarter performance of the Trade segment, which did tremendously well.

The Trade Group reported a pretax income of $39 million and an adjusted pretax income of $24 million. The grain assets and merchandising profit centers capitalized on market dislocations, leading to increased gross profit and pretax income. The premium ingredients business also performed well, pushing the adjusted EBITDA to $44 million, more than double the previous year.

{kind=link}

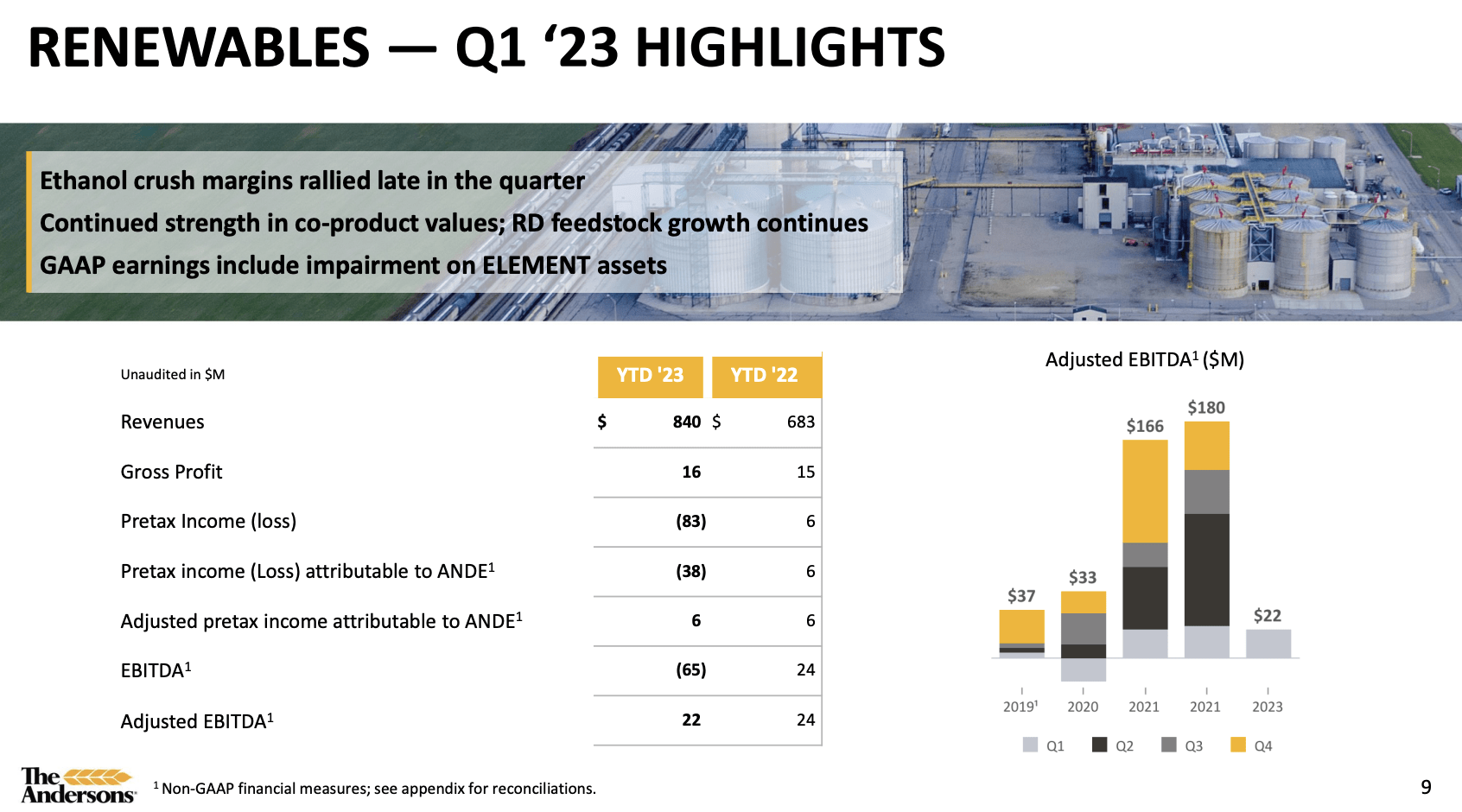

The Renewables (ethanol) segment had a pretax loss of $38 million, but adjusted pretax income improved compared to the previous year. The segment benefited from an improvement in ethanol crush margins and growth in renewable diesel feedstock merchandising volumes, which supports the company's comments regarding limited damage related to the ELEMENT situation.

{kind=link}

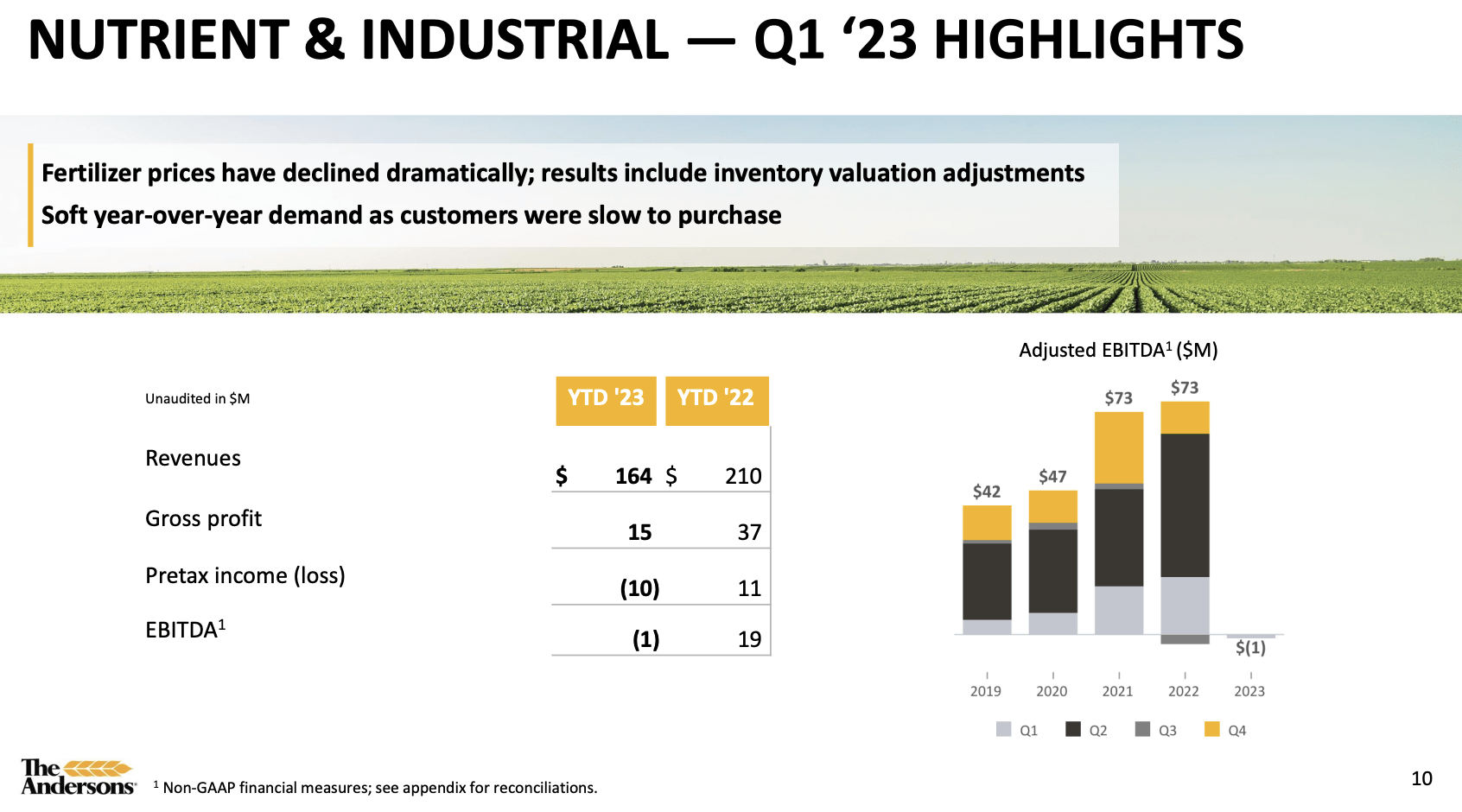

The Nutrient and Industrial business experienced a pretax loss of $10 million, a decline from record pretax income in the previous year. Falling fertilizer prices and limited customer engagement contributed to the decline. Again, I expect the company to report tailwinds going forward, as demand is likely to come back.

{kind=link}

Without fertilizer headwinds, 1Q23 would have been a total blockbuster quarter.

So, what about the outlook and valuation?

Outlook & Valuation

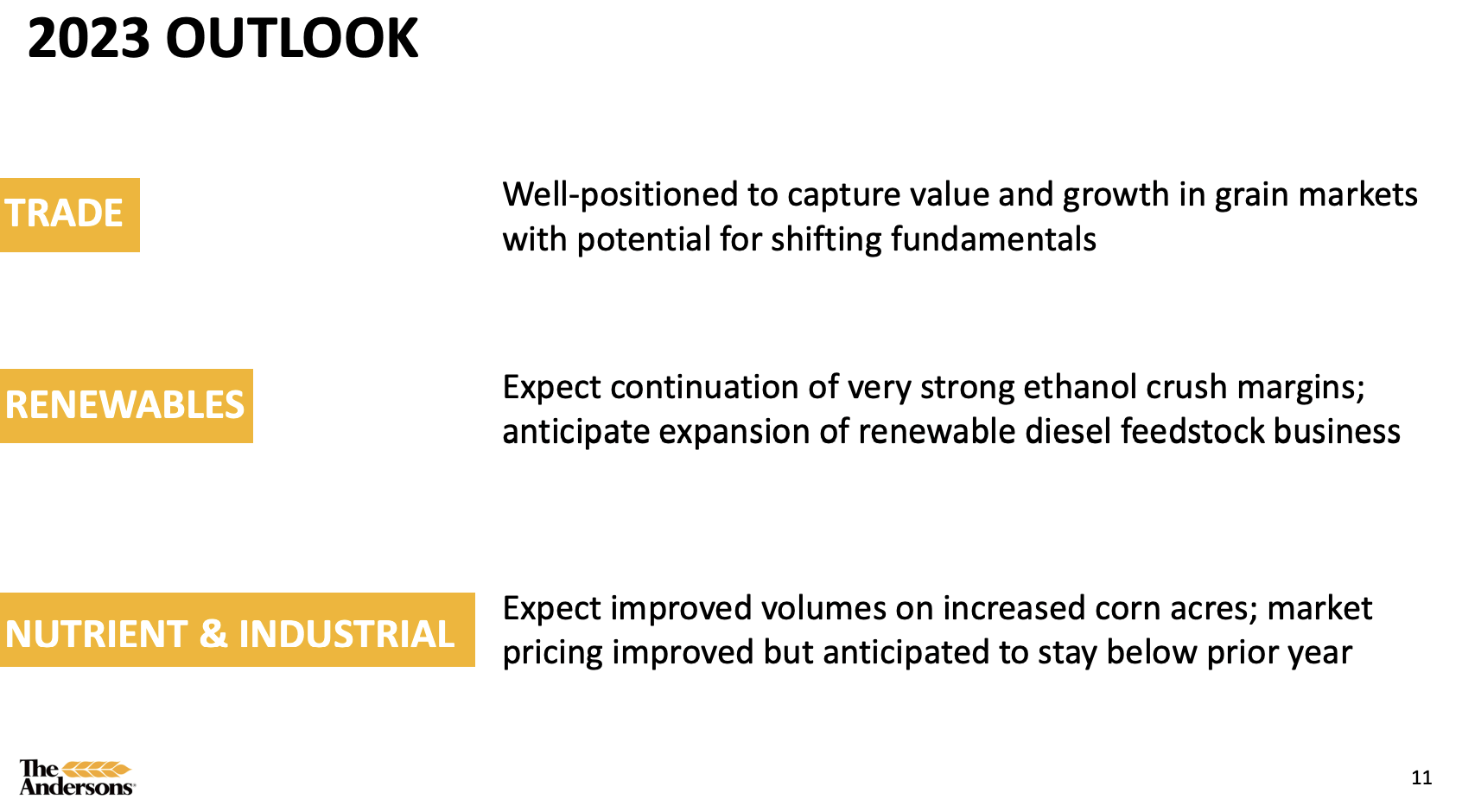

On top of satisfying results in 1Q23, the company's outlook for 2023 remains positive. Global supply and demand dynamics are expected to change with a large Brazilian crop and North American planting progress.

{kind=link}

The trade business outlook remains positive, and the company is well-positioned to optimize volatility and crop dislocation.

Furthermore, the Renewables segment anticipates continued improvement in ethanol crush margins, while higher corn basis levels pose challenges for Western plants.

The company plans investments to enhance the quality and yield of distillers' corn oil, a low carbon-intensive renewable diesel feedstock.

The Nutrient and Industrial business expected improved volumes and margins but not at the levels of the previous year.

ANDE is now trading at 8.1x NTM EBITDA. In March, the company was trading at 9.6x EBITDA. Back then, I wrote that the company should trade somewhere between $65 and $70 to incorporate its improved business structure and cyclical tailwinds.

The company is currently trading at $45 with a consensus price target of $53. My target is more bullish as I'm incorporating longer-term tailwinds in agriculture, which leads me to believe that ANDE is perfectly positioned to benefit from higher trade volumes, fertilizer demand, and energy margin tailwinds.

FINVIZ

However, while I am more bullish than the consensus, people need to be careful. We're dealing with elevated recession risks that could - at least temporarily - hurt energy demand and agriculture margins.

Also, as I know that most of my readers are long-term (dividend) investors, I need to make the case that ANDE isn't a must-own company. Long-term investors seeking agriculture exposure are better off buying companies like Deere & Company ( DE ) or Archer-Daniels-Midland ( ADM ).

As much as I like ANDE, it's too volatile for most investors. I will likely sell it once it has hit my price target and move that money into ADM or a similar company.

Needless to say, I fully stand behind every bullish thing I have said in this article. I'm only warning people because some take on too much risk or buy stocks that do not fit their strategy.

Takeaway

The Andersons has proven itself as a resilient player in the agriculture industry, delivering strong performance and remaining bullish despite challenges.

With a market cap of $1.5 billion, the company operates numerous trade facilities, ethanol production units, and fertilizer distribution centers, connecting various stakeholders in the agriculture value chain.

While the joint venture with ICM faced difficulties, ANDE's overall ethanol business remains promising. The Trade Group reported impressive earnings, capitalizing on market dislocations, while the Renewables segment showed improvement in ethanol crush margins.

Although the Nutrient and Industrial business faced headwinds, future demand is expected to rebound.

Trading at a favorable valuation compared to earlier this year, ANDE presents an opportunity for investors looking to capitalize on agriculture tailwinds.

However, due to volatility, long-term investors seeking agriculture exposure may find more stability in companies like Deere & Company or Archer-Daniels-Midland.

For further details see:

The Andersons: Navigating Challenges, Harvesting Success