ANDE - The Andersons: Positioned For High Growth In North American Agriculture

2023-03-07 14:02:42 ET

Summary

- The Andersons is one of the most dominant agriculture players in North America, thanks to its operations in various stages of the agriculture supply chain.

- The company sees a strong growth trajectory ahead, thanks to its own capabilities and solid industry fundamentals.

- While margins have come down going into this year, the company remains undervalued with room for its stock price to rise to $65-$70.

Introduction

Let's delve into one of my favorite topics - agriculture. I have been particularly drawn to The Andersons (ANDE) , a diversified agriculture player based in Maumee, Ohio, since the start of the agriculture bull market in 2020. In my latest article , dated November 8, 2022, I highlighted how attractively valued the company was and how it had the potential to offer more long-term upside. Fast forward to today, and the stock has surged by nearly 20%, reaching its highest levels since the start of the agriculture bull market.

Thus, it's high time for an update, and the recently-released 4Q22 earnings provide us with valuable insights into the state of North American agriculture. Additionally, ANDE has shared its long-term developments, which further affirm that the company continues to be significantly undervalued.

So, let's get to it!

The Andersons Biggest Issue Is Its Margins

Despite lower margins, 4Q22 and FY2022 results were terrific.

Founded in 1947, The Andersons has gone through an impressive transition. The company is a major player in the North American agriculture supply chain, as it does business in trade, renewables (ethanol production), and plant nutrients.

In 4Q22, the company reported $4.68 billion in revenue. This beat estimates by a whopping $400 million. It was also 23.7% higher compared to the prior-year quarter. Adjusted EPS came in at $0.98, which was $0.49 higher than expected.

It's one of the reasons why the stock is now trading at $44, one of the highest levels since the start of the agriculture bull market in 2020 and more than 50% above its 52-week low.

FINVIZ

With that said, let's discuss the company's business segments in detail. After all, it will tell us a lot about the state of the North American agriculture supply chain. For the convenience of new readers, I will also elaborate on the core operations of each segment.

The trade segment is focused on capturing profits through merchandising and managing logistics across a wide range of commodities. This includes the movement of physical commodities such as whole grains, grain products, feed ingredients, and domestic fuel products, among other agricultural commodities. ANDE operates grain elevators across the United States and Canada, earning an elevation margin, and offers a number of unique grain marketing, risk management, and origination services to customers and affiliated ethanol facilities.

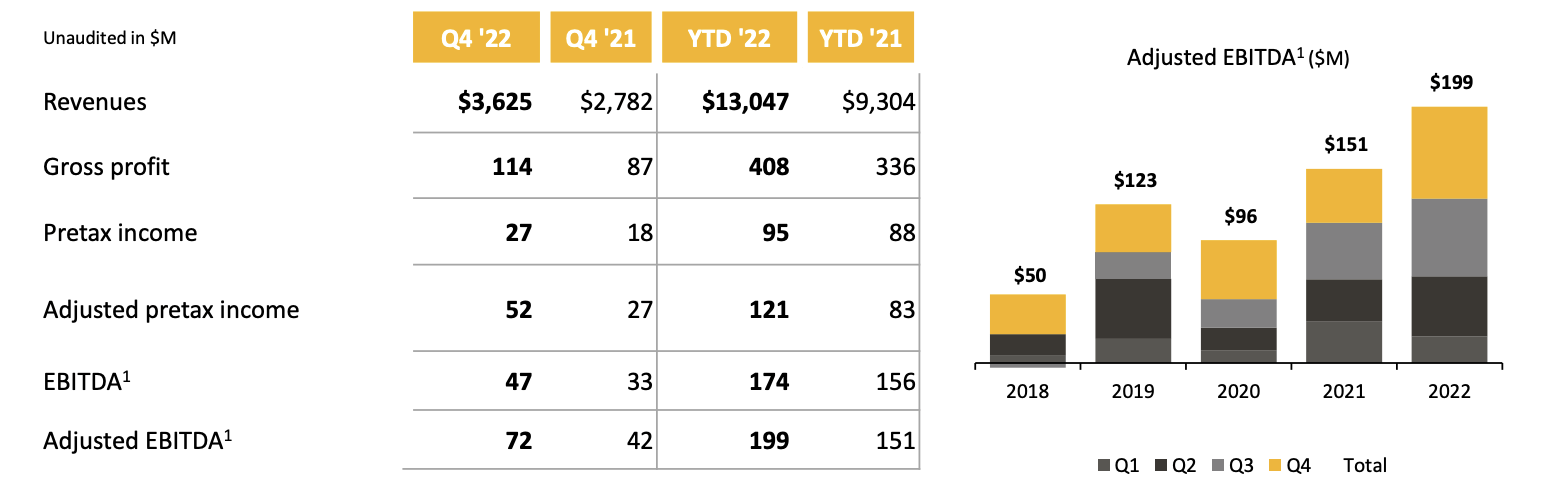

The Andersons (Trade Segment Results)

{kind=link}

In 4Q22, the company grew sales from $2.8 billion to $3.6 billion, resulting in an adjusted EBITDA surge from $42 to $72 million. On a full-year basis, the company did roughly $200 million in adjusted EBITDA, its best result ever. It's more than twice what the company did in 2020 when global supply chains and prices were suffering.

According to the company :

Our merchandising teams continue to execute well in these dynamic markets, with gross profit increasing 30% and adjusted pretax income nearly doubling from the prior year. Increased elevation margins and our grain assets also improved significantly from the fourth quarter of 2021.

The renewables segment produces, purchases, and sells ethanol and co-products, offers facility operations, and provides risk management and marketing services to the ethanol plants it invests and operates in. It owns and operates ethanol plants in five states, with a combined capacity of 405 million gallons.

The company also owns 51% of ELEMENT, LLC in Kansas. This adds another 70 million gallons to its capacity.

{kind=link}

In 4Q22, the company reported close to $800 million in segment revenues. Unfortunately, EBITDA declined from $78 to $36 million. On a full-year basis, EBITDA improved by $14 million.

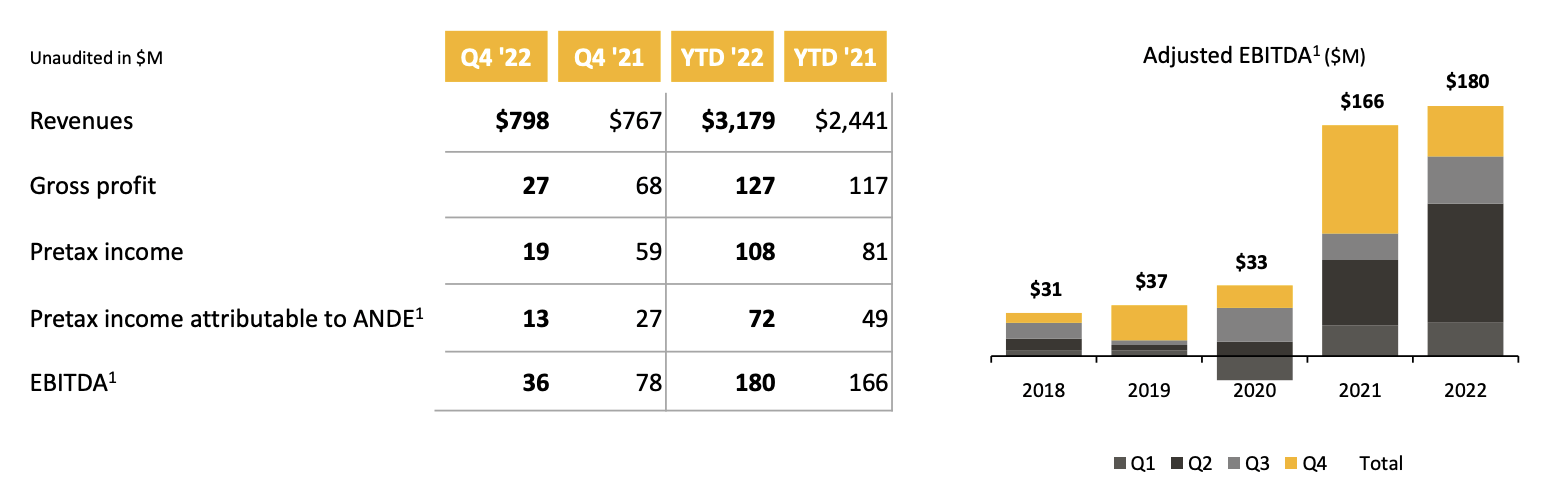

The Andersons (Renewables Segment Results)

{kind=link}

According to the company, this was mainly due to ethanol crush margins.

Ethanol crush margins were substantially lower during the quarter, especially compared to the extreme highs in the fourth quarter of 2021. Continued strength and corn oil values and execution by our renewable diesel feedstock merchandising team helped offset the lower ethanol crush margins.

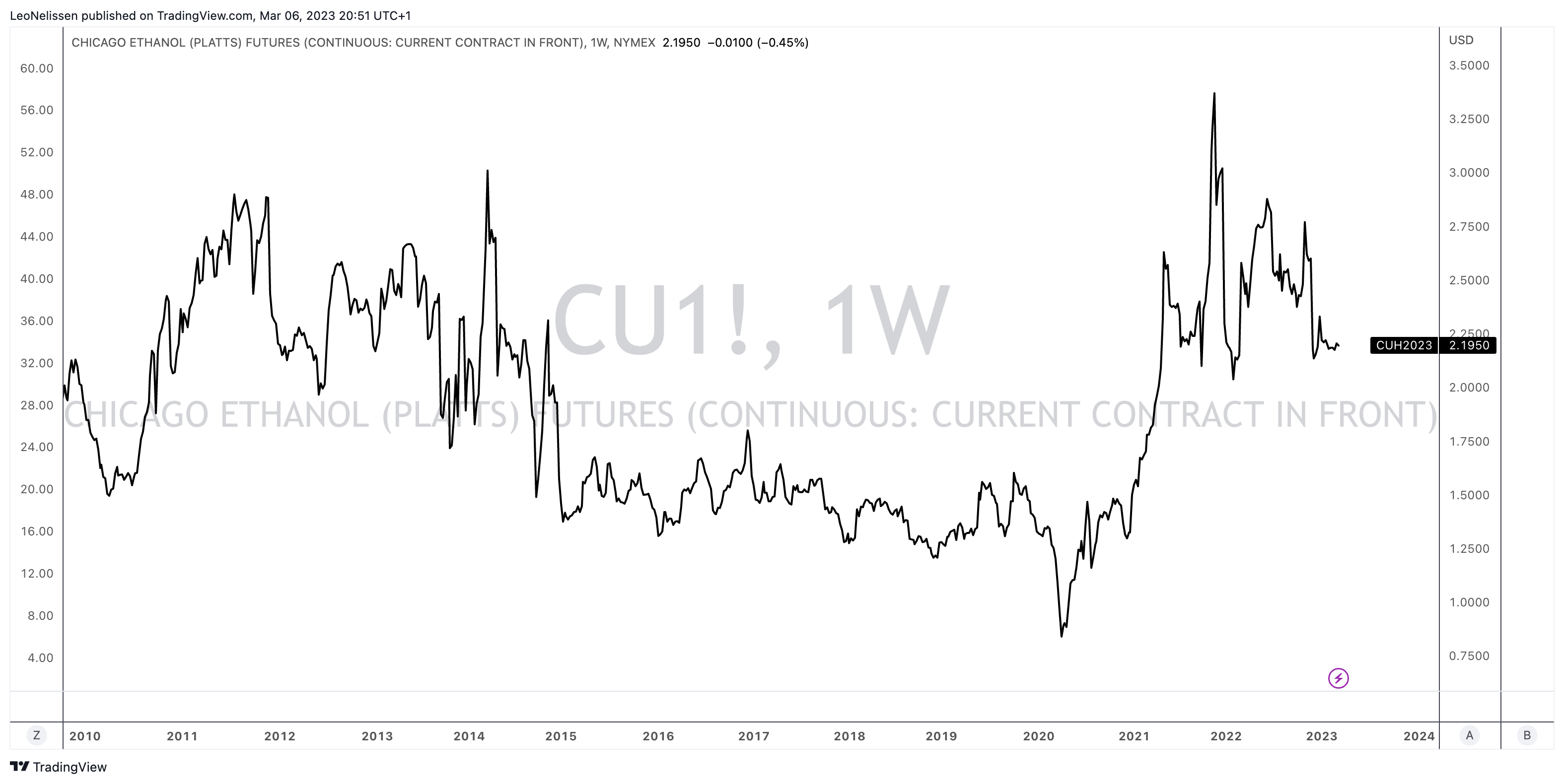

As the chart below shows, ethanol futures have come down substantially at the end of last year, which negatively impacted the fourth quarter.

{kind=link}

With that said, there's one segment left.

The plant nutrient segment is a leading manufacturer, distributor, and retailer of agricultural and related plant nutrients, liquid industrial products, corncob-based products, pelleted lime, gypsum products, and various turf fertilizer, pesticide, and herbicide products. The segment has three divisions: Ag Supply Chain, Specialty Nutrients, and Retail.

In the fourth quarter, the company boosted segment revenues from $234 to $255 million. Unfortunately, adjusted EBITDA fell from $24 to $11 million.

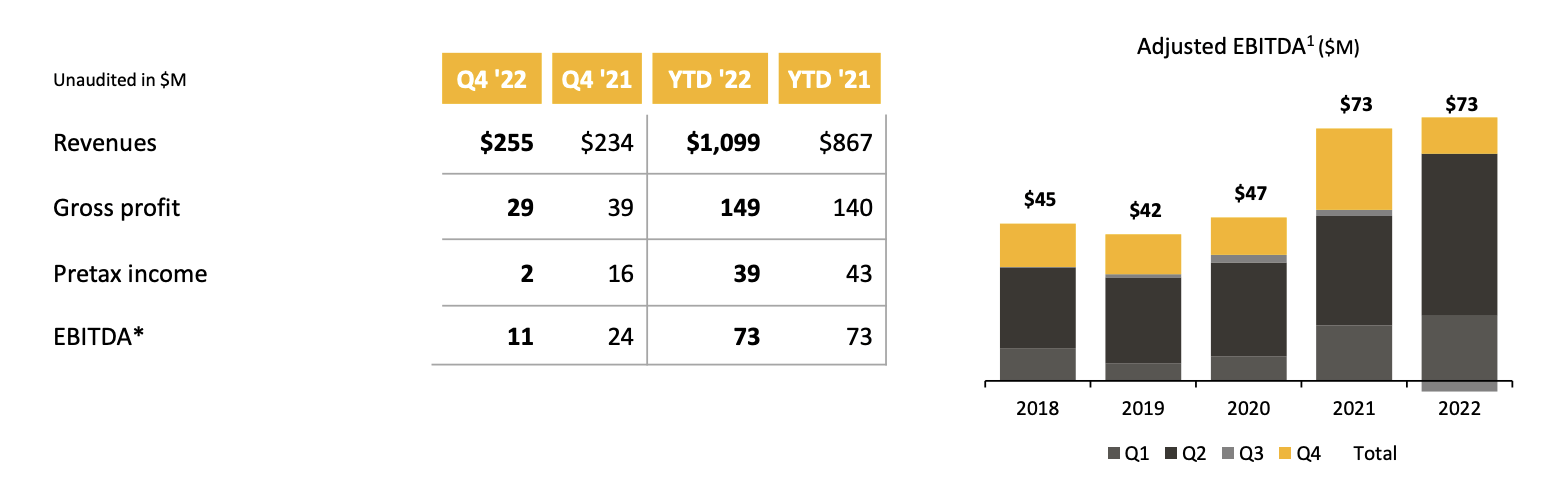

The Andersons (Plant Nutrient Segment Results)

{kind=link}

The overview above shows that, on a full-year basis, the company grew segment EBITDA by $1 million. Unfortunately, the fourth quarter was a bit of a disappointment. However, it was an expected disappointment, as weird as that may sound.

According to the company, the main issue was margins.

The business experienced lower margins in our agriculture products, as fertilizer prices continued to drop dramatically during the quarter. Farmer income remains high, which supported higher margins in our specialty liquids products. However, volumes were lower in anticipation of further declines in fertilizer prices. Our manufactured lawn products business also experienced slower demand and some additional inventory write-downs which we believe are now behind us.

When I said that it was an expected disappointment, I meant that sell-side analysts knew that margins would come down. After all, fertilizer prices have been in a steady decline since the price explosion caused by the Russian invasion of Ukraine in early 2022.

Bloomberg

In other words, the company benefits from strong demand across all segments. The only issue is margins, as ethanol and fertilizer operations suffered from lower price benefits, which was expected.

The Outlook Remains Solid

Backed by an attractive valuation.

So far, so good. However, what matters more is what the company expects to happen in the future.

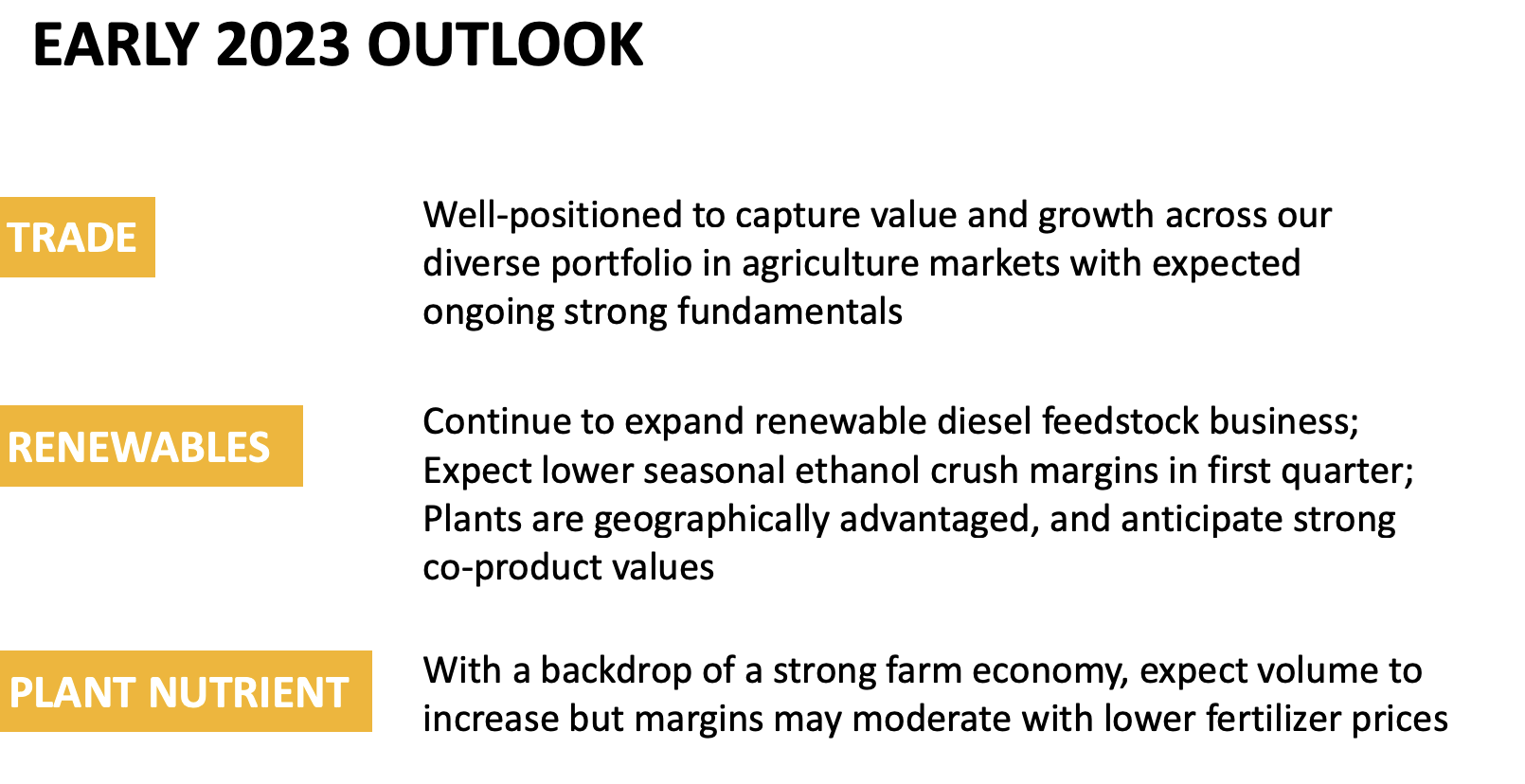

In its investor presentation, the company mentioned strong fundamentals in trade, lower 1Q23 margins in ethanol, yet high co-product values, and lower fertilizer margins to (partially offset) stronger volumes.

{kind=link}

With that said, there are some more takeaways from its earnings call - especially when it comes to its outlook.

The company expects higher corn planting volumes, which is positive for all of its business segments.

This is confirmed by the USDA , which said the following:

Based on the market conditions that existed with the October WASDE, the area planted to corn is projected to rise by 3.4 million acres in 2023/24 to 92.0 million acres before tapering to 89.0 million acres by 2032/33.

USDA

Needless to say, we'll continue to monitor yield estimates once the planting season starts, as this will have a major impact on the final output. While I have some expectations, it's too early to comment on that.

Moreover:

- Ethanol crush margins have been low to start the year, but ANDE believes that heading into spring, three maintenance shutdowns and increases in driving miles may positively influence the second quarter.

- ANDE is making a number of investments in its plants to improve both the quality and yield of distillers' corn oil, a low carbon-intensive input to the renewable diesel industry. It continues to benefit from strong oil values.

- Farmer income and increased corn plantings are expected to continue to drive demand for ANDE's fertilizer, especially liquid products.

- ANDE believes that declining prices in this period prior to fieldwork have kept buyers on the sidelines. It expects to see higher volumes in plant nutrients as we approach the spring planting season, but likely with more normalized margins lower than last year's peak.

With that said, the company's long-term outlook is even more impressive. This is the data the company provided:

{kind=link}

The company had established an EBITDA goal of $300 million by 2020, which was double the 2017 result, and subsequently increased the target to $375 million by 2025. The company has now exceeded these goals ahead of schedule and revised its 2025 EBITDA target to $475 million, which represents a CAGR of nearly 20% from 2018 to 2025E.

As seen in the lower part of the chart above, the company expects to benefit from long-term growth in all of its segments.

Needless to say, growth won't be linear, yet the company is positive that it can aggressively grow its business without needing strong industry tailwinds. In other words, growth is mainly coming from business improvements.

Additionally, The Andersons intends to maintain discipline in its approach to capital investment, keep its long-term debt-to-EBITDA ratio less than 2.5x, and continue to improve ROIC while optimizing its portfolio.

With that said, the company is trading at 9.6x EBITDA - implying that EBITDA remains close to $400 million despite margin challenges. When incorporating the company's massive inventories, the valuation drops to roughly 7x EBITDA.

So, as I wrote in my most recent article, I stick to a fair price target of $65 to $70 per share.

Takeaway

In this article, we discussed The Andersons, a leading agricultural trade that reported a stellar fiscal year and fourth quarter, even amid waning margins. The company's promising position in the agriculture supply chain, robust ethanol production, the projected uptick in fertilizer volumes, and potential for new mergers and acquisitions have management feeling optimistic about future growth potential.

Given these factors, I maintain a positive outlook on ANDE shares and believe they are currently undervalued by at least $20 per share.

That said, ANDE is a holding in my trading account. I do not have a lot of ANDE exposure. I invest most of my money in conservative dividend (growth) stocks. ANDE is highly cyclical and volatile. Please keep that in mind when assessing whether ANDE is the right stock for you.

For further details see:

The Andersons: Positioned For High Growth In North American Agriculture