SPEU - The Apartment Sector: Increasing Demand For Affordable Living

2023-10-25 02:35:00 ET

Summary

- We will focus on the apartment sector in the U.S. and Europe, with an emphasis on the moderately priced, or affordable segment of the market.

- Over the past 12 months, demand for apartments has remained near record levels across key strategic markets and vacancy rates are well within their equilibrium ranges.

- Strong rent growth since the start of the pandemic has continued to fuel impressive NOI growth as leases have continued to roll up to market asking rents.

By Indraneel Karlekar, Ph.D., Senior Managing Director, Global Head of Research & Portfolio Strategies; Arthur Jones, Senior Director, Global Research; Daniel Tomaselli, Manager, Global Research; and JD Stehwien, Senior Analyst, Global Research

In this paper, we will focus on the apartment sector in the U.S. and Europe, with an emphasis on the moderately priced, or affordable segment of the market, which we believe offers the most broad-based exposure to renter demand due to shifting demographics and income distribution.

A need for more housing…

Over the past 12 months, demand for apartments has remained near record levels across key strategic markets and vacancy rates are well within their equilibrium ranges.

Strong rent growth since the start of the pandemic has continued to fuel impressive NOI growth as leases have continued to roll up to market asking rents.

Since 2020, U.S. apartment rent growth has averaged 5.6% on an annualized basis, and in Europe that figure is 3.7%. The impact of mark-to-market rents with more frequent rollovers than other property sectors and low vacancy rates have translated into annual NOI growth in the low double digits.

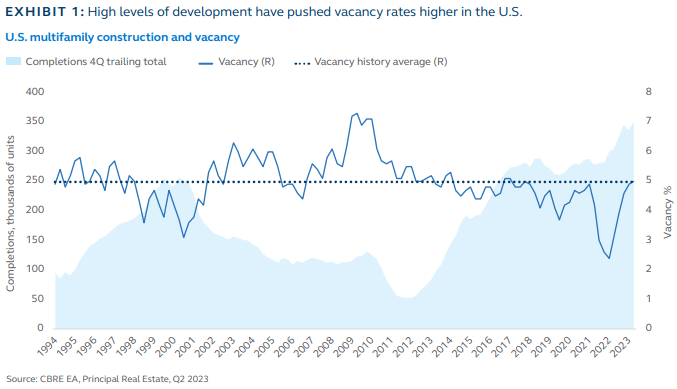

If there has been a question mark regarding the apartment sector in both regions, it has been the high levels of development. In the U.S., the pace of new deliveries has pushed vacancy rates up toward their long term historical averages for institutionally managed properties (Exhibit 1).

{kind=link}

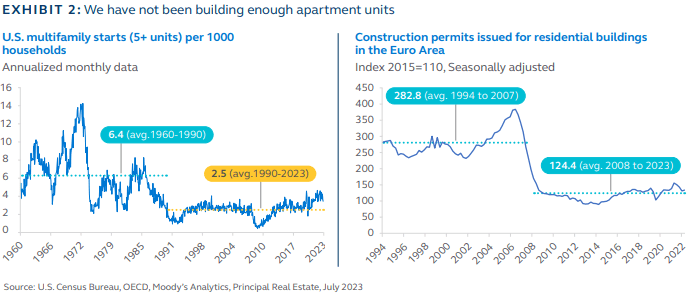

Recent supply and demand trends may be somewhat misleading, however. Despite an increasing number of projects that are under construction, apartment units have been under-delivered over the past decade.

Consequently, there has been a shortage of housing which has resulted in an affordability crisis in many major cities for both the rental and for-sale markets.

In the U.S. for example, Exhibit 2 (left chart) shows that since 1990 only 2.5 new multifamily units have been built for every thousand households - well below the average of 6.4 between 1960 and 1990.

In Europe as well (right chart), construction permits issued for residential dwellings have yet to recover to their preGlobal Financial Crisis ((GFC)) levels.

{kind=link}

Most major markets in the U.S. and Europe are now facing a housing deficit with many needing more units to accommodate population growth than are currently being supplied. In fact, a research report from Freddie Mac - a U.S. government sponsored entity founded to provide liquidity to the residential sector - recently stated the U.S. needs an additional 3.8 million housing units to meet current demand growth. 1

In Europe, the construction of new residential buildings is also unable to keep up with demand. The German Property Federation for example has reported that the deficit of housing in the country has reached its highest level in 20 years and that by 2025 the shortage may increase to 700,000 flats. 2

As a result, across both sides of the Atlantic, the outlook for current landlords and developers remains positive and suggests that secular demand through demographics will provide a steady flow of new renters looking for space.

Demographics driving demand

While all property sectors rely on demographics as a primary demand driver, the residential housing sector, especially apartments, has an outsized reliance on population growth in prime renter age groups.

Of particular importance is the shape of the population pyramid, which dictates where demand falls. Other important factors in conjunction with demographics are cultural norms that impact household formation and homeownership trends across regions.

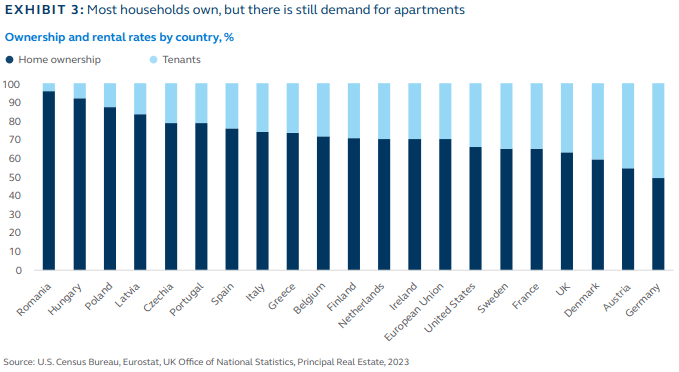

In the U.S. and Europe, a majority of households own their homes. Homeownership rates can vary greatly by country, however, with Romania having the highest rate of home ownership at 95.3% and Germany the lowest at 49.1%.

Such high homeownership rates among Eastern European nations are an artifact of the rapid shift from planned- to market-based economics in the early 1990s.

Due to the fiscal stress placed upon most former Eastern Bloc nations, tenants were offered a chance to purchase the dwellings in which they lived at low prices from the government.

When we take into consideration amenities and quality of dwellings, high homeownership rates in these countries should not necessarily indicate a lack of demand for newer and higher-quality rental units.

Rather, in many Eastern European nations, the relatively poor quality of existing housing stock could offer an interesting entry point for developers to provide more modern and highly amenitized apartment communities.

{kind=link}

If we look more broadly at the demographics associated with the rental population base, we establish that in both the U.S. and Europe, it is quite large.

If we include the UK, there are roughly 357 million households in these regions, of which 32.1% are renters, meaning there are nearly 115 million rental households.

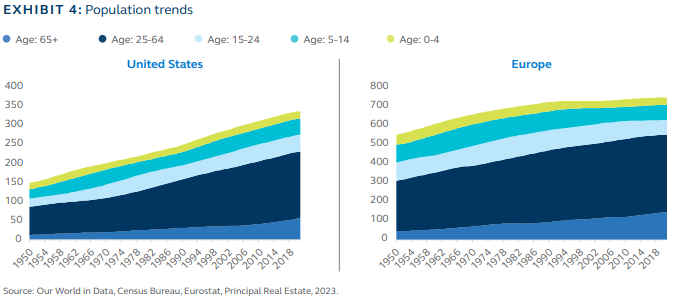

The population trend charts suggest that in addition to existing rental households, there is an ample pool of renters that can provide increasing demand over the next decade.

Millennials - those aged 27 to 42 - remain a dominant population group in both the U.S. and Europe, accounting for 20% of the population. Including Generation Z, the prime-renter age group expands to nearly 40%.

While the U.S. and Europe are getting older with median ages of 38 and 44 years old respectively, younger generations have officially taken over from the Baby Boomers (Exhibit 4).

{kind=link}

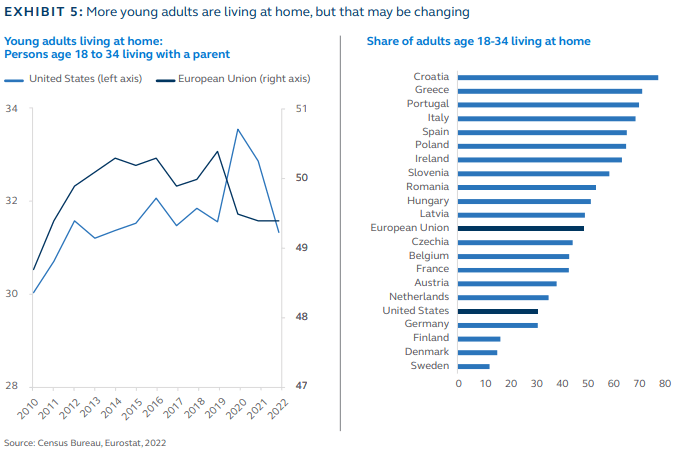

Young adults living with parents are another source of untapped demand. In many countries young adults are living at home longer than ever before. Data from the U.S. Census and Eurostat shows that between 2010 and 2022 (the last year of available data), the share of young adults has increased.

In the U.S. for example, people in the potential renter category living at home increased from 30% in 2010 to 31.4% in 2022, which represents roughly one million additional individuals who could form households and increase the demand for apartment units over the next few years.

In Europe, the share of young adults living at home is structurally higher but has also increased over the past decade. More recently though, the share of young adults living at home has started to decline particularly post-pandemic, which will help drive demand for apartment units over the next cycle.

{kind=link}

The affordability question: It’s not just a single-family problem

Although the decision for young adults to live at home may be driven by numerous considerations, including cultural and social norms, family ties, and structural factors, it is also increasingly the case that affordability is becoming a larger issue.

While affordability cuts across all segments of the residential sector, the current interest rate environment is both a blessing and a curse for the rental market. Monetary policy in the U.S. and Europe is very restrictive.

In the U.S. for example, the 30-year fixed mortgage rate - the most popular financial options for homeowners - has increased to over 7% adversely affecting home price affordability, particularly for first-time home buyers looking for an accessible entry point into the for-purchase market.

Historically, housing affordability has been dictated by a simple rule of thumb that allows a potential home buyer to estimate affordability as a house price of roughly three times their annual income.

This has generally held up when applied to the median household when mortgage rates conform to spreads at equilibrium long-term rates. Nearly a decade of extraordinarily accommodative policy has rendered that relationship useless.

House price-to-income ratios in the U.S. and the UK for example, have increased to roughly 5.5 due to exceptionally low interest rates following the GFC and again during the COVID-19 pandemic.

In the U.S. for example, the median price of an existing house was $284,488 in December 2019 with an average commitment rate on a 30-year fixed rate mortgage of 3.7%.

Today in the U.S. the median house price is roughly $400,000. Put another way, the rise in both interest rates and prices has increased the average payment for a home buyer by about $1,200 per month.

The apartment sector to date has been a primary beneficiary of pricing increases within the singlefamily for-purchase market in both the U.S. and Europe. Just following the pandemic, U.S. markets saw net absorption in 2022 of 627 msf, which exceeded the prior record by more than 200 msf.

The net result was a tightening of the market that saw apartment rents increase by 21% between 2020 and 2022 and, with it, a decline in overall affordability.

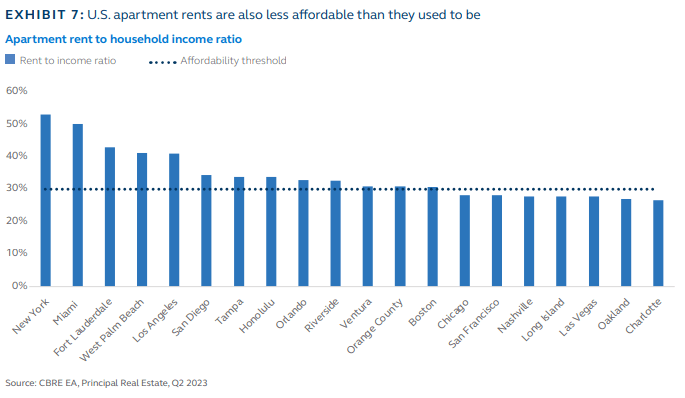

In the U.S., the Department of Housing and Urban Development ((HUD)) defines affordable housing as housing on which the occupant pays no more than 30% of gross income, including utilities. 3

In the U.S., roughly 25% of markets we track would be deemed either unaffordable or at risk solely based on average asking rent and median household incomes across metro areas (Exhibit 7).

{kind=link}

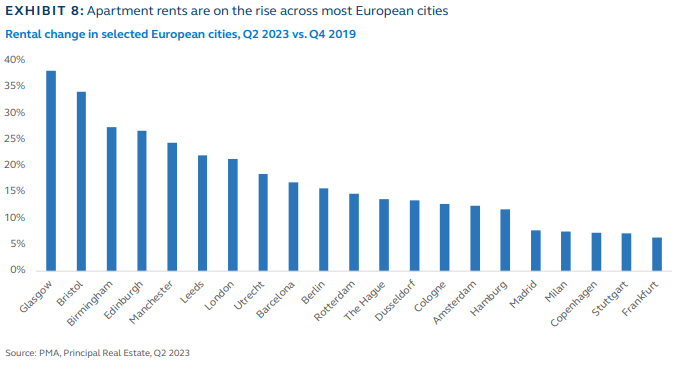

On the other side of the Atlantic, statistics from Eurostat revealed that 50% of market renters spent at least 40% of their income on housing in the European Union in 2021.

Although more recent figures are not yet available, the spike in the cost of living and the rise in rents that occurred over the last year and a half have certainly worsened the average housing overburden rate, as nominal wages failed to keep up with rampant inflation.

In Greece and the Netherlands for example, renters spend more than 30% of the income on housing. Across most European capitals, renting a one-bedroom flat in a central location can easily exceed the average worker's salary.

{kind=link}

Moderately priced rental housing

The erosion of apartment affordability amid tight market conditions and strong rental increases recently has presented a quandary for many investors. While apartment rental values remain attractive relative to home ownership, they continue to stress household balance sheets on a practical basis.

Portfolio managers looking to increase their allocation to the living sector and apartments are increasingly cognizant of rising cost pressures, particularly when it impacts new demand and tenant retention.

While data on affordability are ample, hard data on the affordable housing market’s performance are more nuanced and elusive. Many investors have multiple terms and definitions of what they deem to be affordable and there exists no hard benchmark for performance.

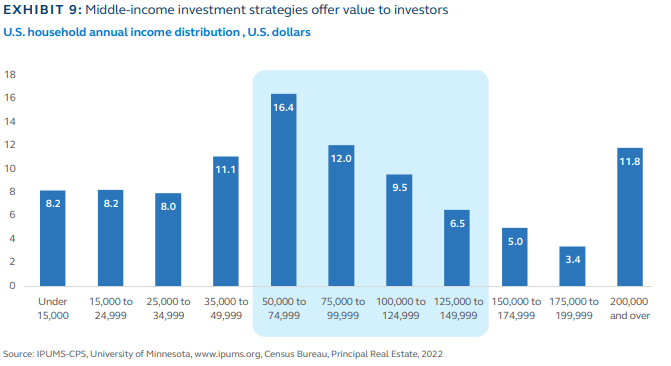

Using HUD’s definition of no more than 30% of a household’s budget as a guideline for affordability, we can calculate the threshold for an affordable unit. At the median household income of $74,580 for 2022 in the U.S., the limit for an affordable unit would be $1,854 per month.

Investors using a range around median household income of between 60% to 120%, which is typical in the industry today, would be able to target households with incomes between $ 45,000 to $ 90,000. This translates into a rental range of between of $1,120 to $2,240 per month.

In the U.S., the national average for an institutionally managed two-bedroom unit is near the top of the affordable range. Fortunately, within the U.S. and Europe, there is a wide disparity between regions and apartment formats that provide investors with diversity.

We suggest that investors focus on matching households in the middle of the income distribution with appropriately priced rentals. In the U.S., the middle of the household income distribution, as shown in Exhibit 9, ranges from $50,000 to $150,000 and represents 44% of all households and creates a very meaningful investment opportunity to serve.

{kind=link}

By focusing on middle-income households and diversifying investment portfolios across regions where apartment rents are more affordable, investors can ensure the ability to retain tenants and push moderate rent increases, thereby ensuring solid NOI growth and, ultimately, capital appreciation.

While there is a decided lack of performance data for affordable or moderately priced housing, the literature suggests that such a strategy can offer both higher returns and lower volatility over time.

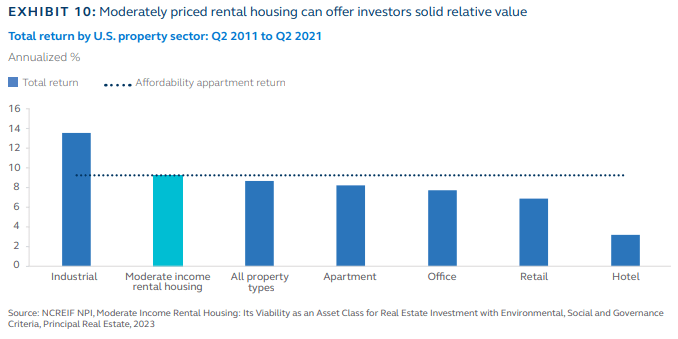

A recent research paper, Moderate Income Rental Housing: Its Viability as an Asset Class for Real Estate Investment with Environmental, Social and Governance Criteria, used NCREIF data to estimate the performance of moderately priced rental properties against other segments of the NPI Apartment index, as well as comparing those results across other sectors.

It found that between 2011 and 2021, moderately priced apartment properties produced a 9.3% return, outpacing all other major property sectors except for industrial (Exhibit 10).4 The study can provide investors with some perspective and confidence as they look to increase exposure to the apartment sector.

{kind=link}

Conclusion

The apartment sector in both the U.S. and Europe continues to benefit from several structural tailwinds that are reshaping the way individuals live. Shifting dynamics within housing affordability and the distribution of income and wealth should provide the sector with a steady pace of demand over the coming decades.

As the younger generations take over to become the dominant demographic groups in both size and spending power, we believe that investors should focus on the needs and desires of this growing pool of potential renters.

The economic climate will dictate that investors focus on underserved segments of the income distribution, which will provide a stable renter base amid lower levels of affordability in the for-purchase market in both the U.S. and Europe.

Shortages of rental units are also driving rents to unsustainable levels in many U.S. and European cities, thereby forcing many younger people to live at home longer.

This has created a pool of untapped demand for the apartment market, particularly for affordable or moderately priced units. We believe that investors should concentrate on these underserved groups, particularly those in the middle third of the income distribution, which will allow for a diverse economic cross-section of renters at attainable entry points.

1 Freddie Mac , May 2021

2 Reuters , February 2023

3 Department of Housing and Urban Development, 2011

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Apartment Sector: Increasing Demand For Affordable Living