QQQ - The August CPI Chart Stock Market Bears Don't Want You To See

2023-09-13 11:50:44 ET

Summary

- We recap the August CPI report.

- A tick higher in the annual inflation rate made headlines, while the drop in the core-CPI is the more favorable development.

- We believe the Fed is done hiking rates this year, and stocks have room to rally going forward.

The best way to summarize the August CPI update is that this was a mixed report. Across the key data points, some inflation metrics came in a bit hotter than expected, while other indicators paint a more favorable picture. There are plenty of details to dig through and it's fair that everyone will find something to chew on. We'll offer our bullish take here.

{kind=link}

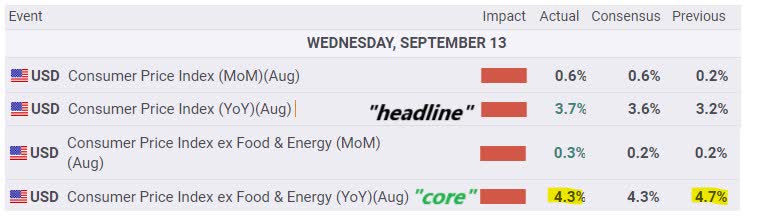

The annual CPI rate at 3.7% was above the 3.6% market estimate, reflecting a 0.6% m/m increase. This headline serves as fodder for some interpreting that inflation could be re-accelerating and that the Fed will need to do more. This angle would suggest further headwinds for the economy and stock market, presuming it forces a reset of expectations.

On the other hand, we see the bigger development here as the convincing drop in the core CPI, the measure that excludes more volatile energy and food prices. The figure fell to 4.3% in August, down from 4.7% in July, the lowest level in more than two years and, and also the sixth consecutive month in decline.

This is important because is that it's understood core inflation categories like shelter and services better capture segments of the economy where the Fed's policy actions have a more direct impact. The setup here is for the Fed to consider that the string of rate hikes over the last 18 months working as intended, and should be enough to keep the group on hold at the next FOMC.

All in all, we got further confirmation that we're on a soft landing, where inflation is stabilized lower without wrecking the economy. In our view, the setup here is positive for the stocks and risk assets.

{kind=link}

Dissecting the August CPI Report

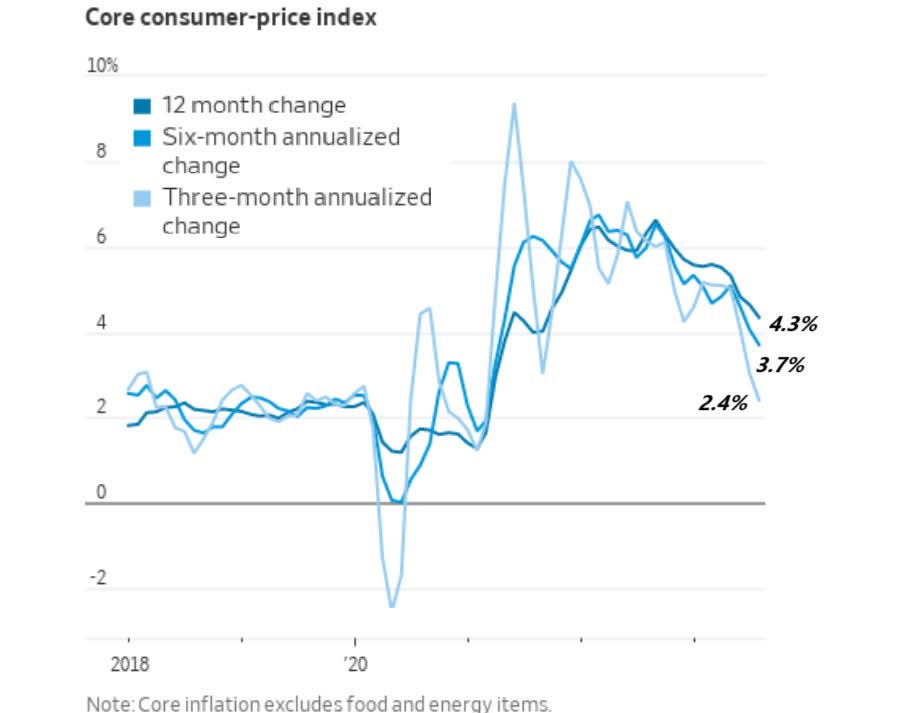

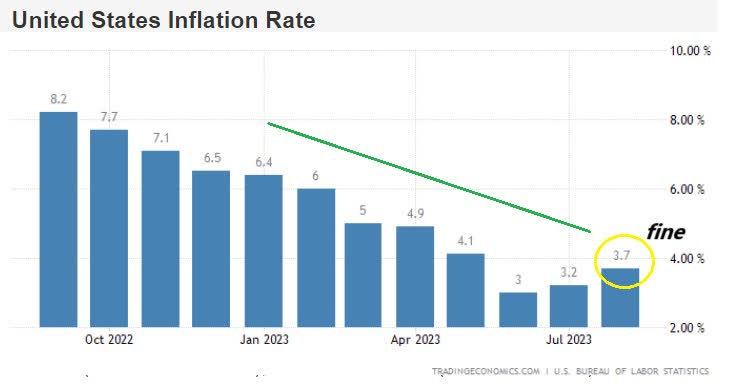

The argument we're making is that the trends in core inflation are what matters at this stage in the cycle. Over the past year, since the headline annual rate fell from a high of 9.1% last June, the stubbornly high or "sticky" side of core was seen as the Achilles heel in the disinflationary process. From there, it's encouraging to see core inflation finally making that big move lower.

Looking just at the core, the annualized monthly rate over the last 3-months of data is now at 2.4%. Not quite at the Fed's mythical 2.0% target, but clearly moving in the right direction.

{kind=link}

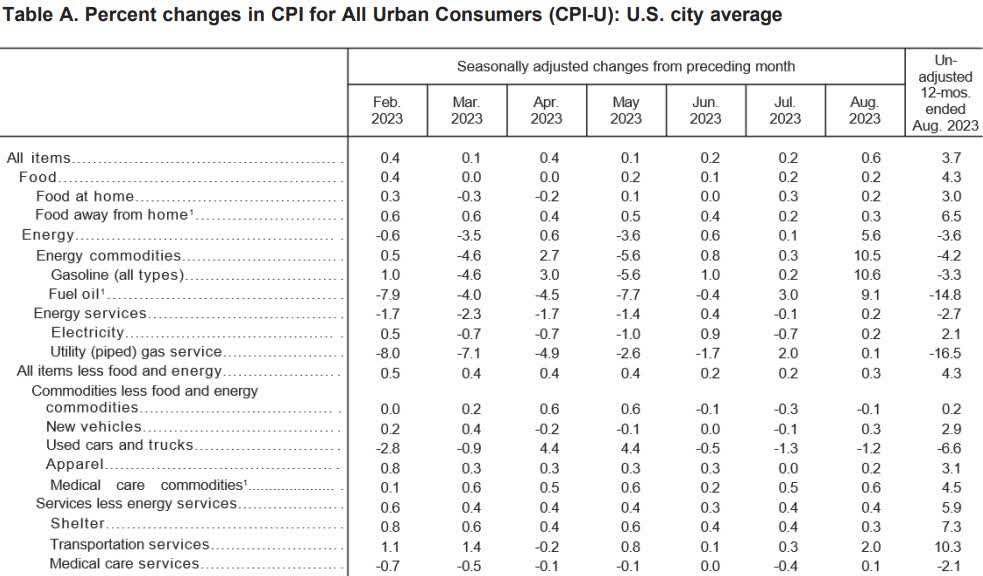

Shelter prices, for example, up 0.3% m/m in August represented the smallest monthly increase for this category since early 2021. The expectation is that shelter, reflecting home prices and rents for primary residences will continue to cool and could even turn deflationary with a negative number in the coming months.

This is because alternative market-based indicators like Case-Shiller have diverged lower compared to the +7.3% annual rate being reflected in the official BLS data. There is more downside in the coming months to the annual core CPI trend with Shelter CPI lagging based on some survey tracking quirks.

Used car prices have also been cooperating, down by -1.2% m/m in August, following a trend we've been watching in the " CarGurus Index " which tracks millions of live listings consumers are seeing in real-time. As with mortgage rates and auto loans, higher rates are working to pressure prices, and there simply isn't a reason to believe these categories will suddenly reverse sharply higher.

{kind=link}

The elephant in the room here is the rebound in energy prices with fuel and gasoline climbing by more than 10% m/m in August contributing the higher headline rate. Nevertheless, it's encouraging to see that the move remains relatively contained, and still negative on an annual basis. Even with crude oil at $90/bbl, the level remains well off from its highs above $130/bbl in 2022, recognizing the unique circumstances at the time.

The current national average for gasoline at $3.85 isn't high enough, in our opinion, to kickstart the cycle of cost-pull inflationary effects. This compares to a high of $5.02 in June 2022. We believe that oil can rally a bit higher here, but does not necessarily undermine an outlook for the ongoing disinflationary process. inflationary outlook.

In this regard, energy prices become a double-edged sword. They have added some volatility to the inflation trends, but also have the effect of pressuring demand-side inflation on other categories if consumers are being squeezed.

All that said, the big picture here is that inflation just isn't the problem it was back in 2022. Even at the headline, the average over the last 3 months at 3.3% is pretty good.

{kind=link}

What Will the Fed Do Next?

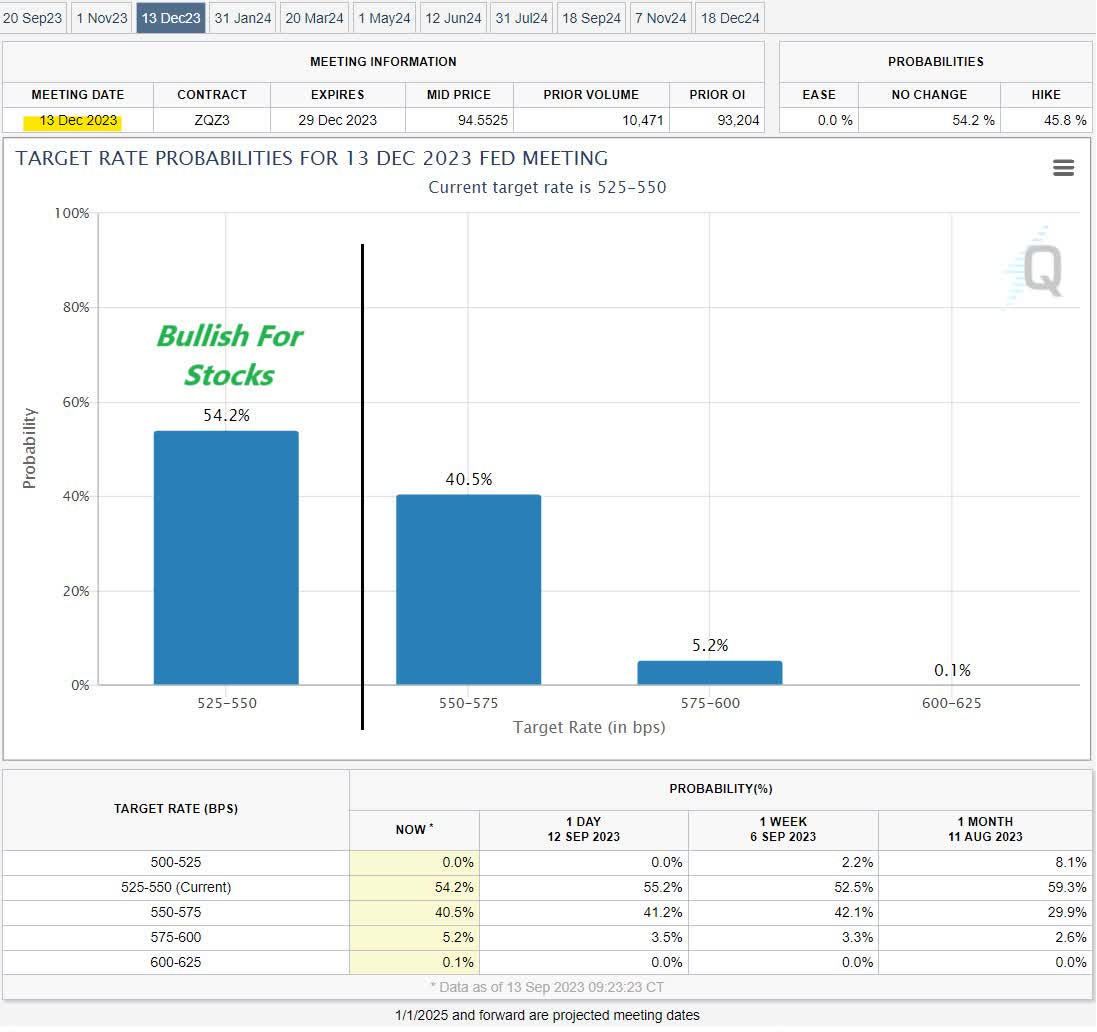

The broad consensus is that the Fed will hold rates steady at the upcoming September 22nd meeting. This is based on recent messaging suggesting the group will take a wait-and-see approach, and nothing in the August CPI report has changed that. This is also confirmed by current market implied probabilities.

That being said, the outlook becomes more interesting with a greater degree of uncertainty out to the December Fed meeting. Based on implied Fed funds rate futures prices, the market is nearly split with a 54% chance the Fed stays on hold through the end of the year against a 46% probability for at least one hike.

We bring this up as a proverbial line in the sand . One side of the market believes the Fed is "done," while another group believes rates will need to go higher. The hold camp represents the more bullish case for the stock market and risk assets in our opinion, because it would mean that inflation remains on the cooling path and the next couple of months can confirm that.

{kind=link}

Stock market bears are sort of hoping that inflation re-accelerates and becomes unanchored forcing the Fed to turn more hawkish, again. We're not going to pretend to have a crystal ball, but we view that inflation re-accelerating angle as the less likely of various circumstances. We know that economic indicators have been mixed between industrial production and ISM manufacturing while consumer spending is also up against high interest rates.

Factors like rising credit card delinquencies and even the re-start of student loan repayments have the net effect of pulling demand down, at least helping to keep inflation contained. It also appears the housing market has slowed.

We believe the Fed is looking at all of this and will ultimately er on the side of caution, to not raise rates while allowing more time for the transmission of monetary tightening to permeate through the economy.

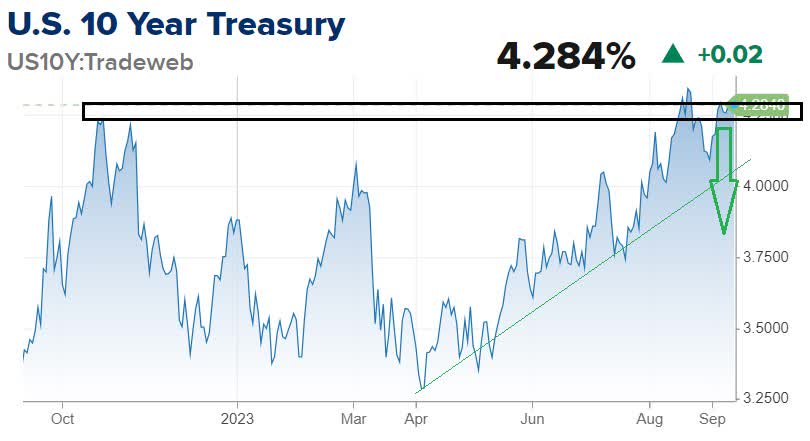

Ultimately, if we're correct and the market begins to move more towards the side of no further hikes, market rates, and bond yields have room to pull back lower. This would be a positive development in terms of risk sentiment we still expect to play out this year.

{kind=link}

What About Stocks?

We believe the positive momentum in stocks can continue. Bulls have been on the right side of the market trend all year and we can start looking ahead to 2024 where the backdrop could be the beginning of a new macro growth and credit cycle. Assuming inflation has a path to settle towards 2%, the Fed could have the confidence to cut rates working as a new tailwind for the economy.

Naturally, this should be positive for the operating environment of companies across cyclical sectors, supporting higher earnings and boosting stock prices. The bullish case for the S&P 500 is that companies continue to outperform earnings expectations into the Q3 and Q4 reporting season, with room for revisions higher to full-year estimates.

Finally, we'll end with the risks to watch. The first point here that would be concerning and force a reassessment of the outlook considers the possibility that oil and gas continue to rally significantly higher. A level of crude above $110/bbl would raise some eyebrows with implications for inflation in other sectors of the economy.

The potential that inflation expectations become unanchored would likely drive a new round of financial market volatility. There is also the ongoing Russia-Ukraine conflict that poses tail risks in some of the worst-case scenarios. Monitoring points over the next few months include housing statistics and trends in consumer spending.

{kind=link}

For further details see:

The August CPI Chart Stock Market Bears Don't Want You To See