TBBK - The Bancorp: A Bank That Stands Out From The Crowd

2023-05-26 07:42:53 ET

Summary

- The financial structure of this bank is atypical.

- Major banking risks are under control.

- Through an evaluation of tangible book value, The Bancorp seems overvalued, but it could still perform well in this macroeconomic environment.

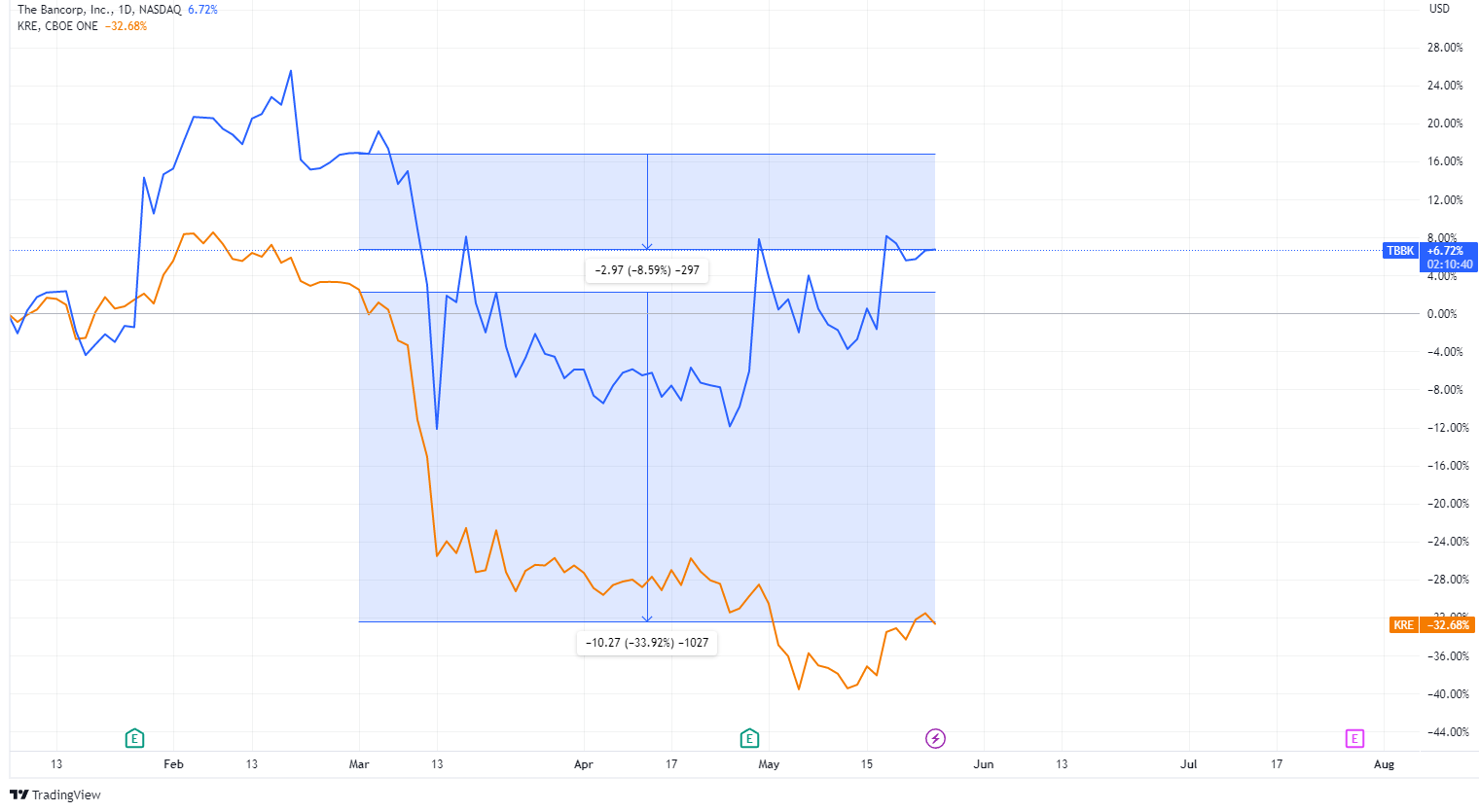

March 2023 is a date that regional banks are unlikely to forget; in fact, after SVB's bankruptcy, the SPDR S&P Regional Banking ETF ( KRE ) suffered one of the sharpest collapses, and is still 32% far from its pre-crisis levels. Still, there have been several exceptions, and some banks have performed better than others. One example is The Bancorp ( TBBK ), a bank incorporated in 1999 and headquartered in Wilmington, Delaware.

{kind=link}

The price per share of The Bancorp is only 9% far from pre-crisis levels, almost as if nothing had happened. But why hasn't this bank collapsed?

Why did Bancorp perform better than competitors?

To answer this question, it must first be understood that Bancorp is an atypical bank because it has a different financial structure from traditional banks. Typically, banking is about raising short-term funds through deposits and investing them over the long term to earn a return from the spread of the two interest rates. This process is called maturity transformation, and it is the basis of almost every bank.

In the case of Bancorp, the funds sourced through deposits are invested primarily in the short to medium term and at floating rates, so the yield on their assets tends to follow the trend of the interest rates. In a macroeconomic environment where the yield curve is inverted, the Bancorp's strategy is more efficient because the financial structure is much more elastic.

So, the recent rise in interest rates has been a favorable point for Bancorp, while any decline would be a disadvantage. Here are in detail the consequences of a change in the Fed Funds Rate:

The Bancorp Q1 2023

- If rates rise by 100 or 200 basis points net interest income is expected to rise by 14.05% maximum.

- If rates fall by 100 or 200 basis points net interest income is expected to fall by 14.18% maximum.

Thus, for the time being, Bancorp is positioned toward an eventual rate hike or stall, in accordance with the Fed's outlook. But what if the Fed decides against all odds that it will initiate a new expansionary monetary policy? A plan is already in place to reduce the sensitivity of assets to falling interest rates. This plan was discussed extensively during the conference call by CFO Paul Frenkiel . I attach his response in full:

Our mix is shifting every day now. So we're putting out fixed rate exposure, excluding the bonds in all our programs at a greater rate. And the new CRE loans obviously have very high floors on them, right? So we're getting less, less asset sensitive by the day. And if we have normalized rates over the next 18 months in the four plus range, there really will lock in a lot of, get rid of a lot of that asset sensitivity just with the loans that we're doing. Now, if we add to that a substantial purchase and fixed rate bonds, obviously as we top out our rates and they start to cut, the yield curve will disinvert hopefully, and then that's when we'll start the purchase program of fixed rate securities and that should really mitigate any downside.

In short, the company is waiting for the right time to gradually reduce the sensitivity of assets to rate cuts. Now it seems it is too early to do so; it is likely to start when there is the first rate cut by the Fed. At that point fixed rate bonds will be purchased, which, together with high floors on CRE loans, will reduce the sensitivity of net interest income to falling rates. For the time being, the strategy is not changing since the results are more than positive.

{kind=link}

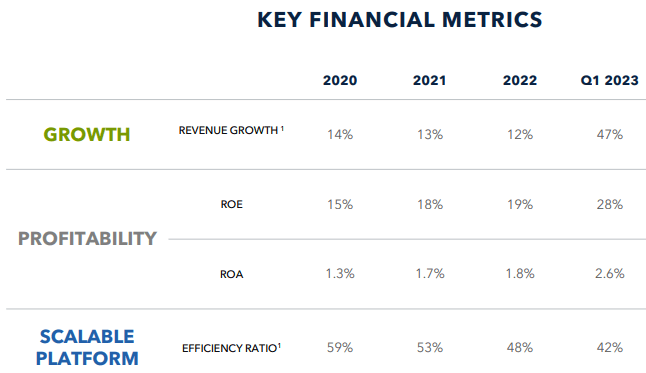

Compared to last year, revenues increased 47%, ROE is 28% (huge for a bank), ROA 2.60% and efficiency ratio is only 42%.

{kind=link}

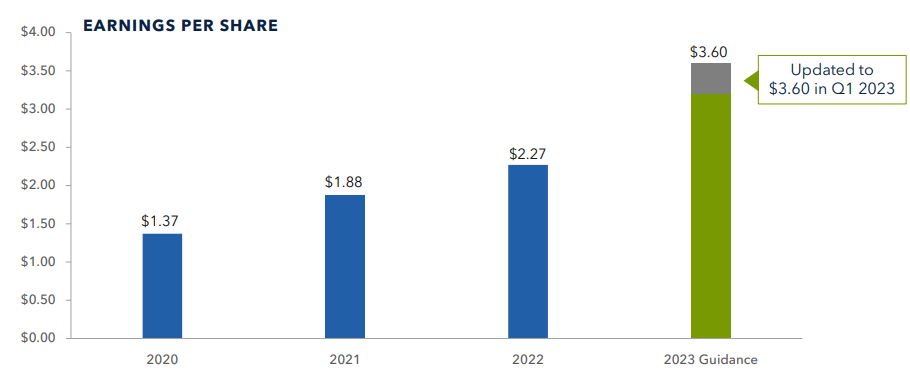

EPS has shot up and the guidance has also been updated. In short, unlike its competitors, the banking crisis is not adversely affecting Bancorp.

How solid is this bank?

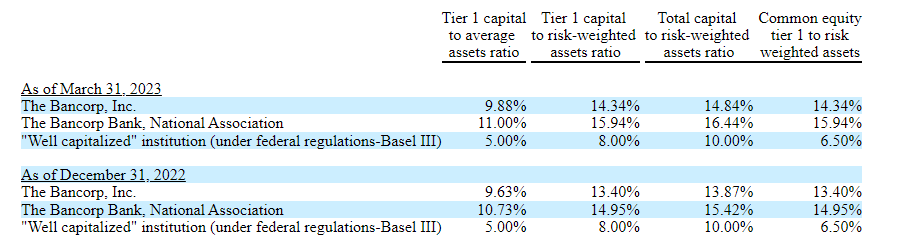

As a first step in assessing the soundness of a bank, its degree of capitalization must be taken into account. This tends to be measured by considering the minimum limits imposed by the current Basel III regulation.

{kind=link}

As we can note from this image, all ratios are above the minimum threshold, and not by a small margin either. CET1 to risk-weighted assets represents 14.34%, more than double the minimum threshold of 6.50%.

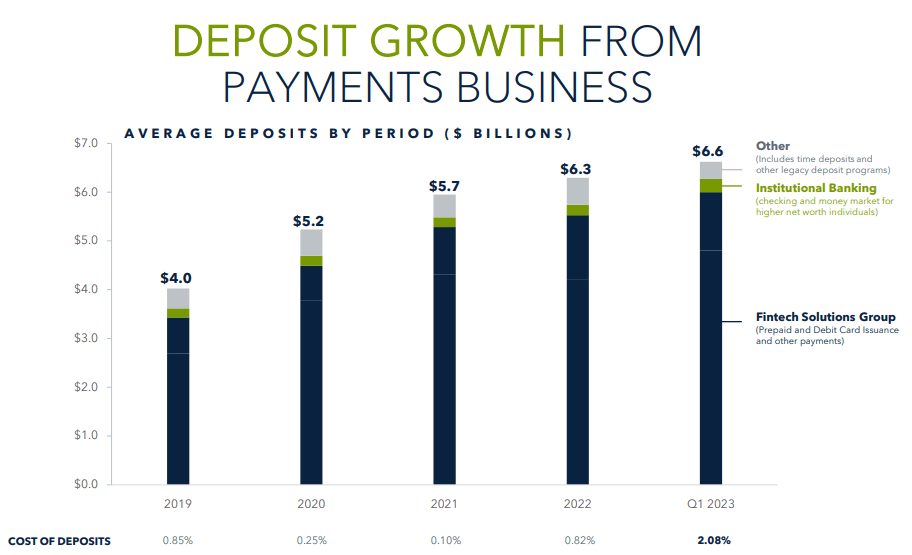

Let's take a look now at deposits, a topic much discussed in recent months. Many regional banks have experienced decreasing deposits since the banking crisis triggered by the failure of SVB, especially those with a prevalence of uninsured deposits. In any case, all these problems do not exist for Bancorp.

{kind=link}

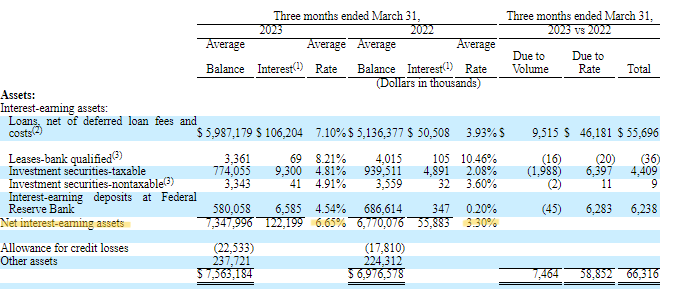

Average deposits compared to last year increased by $300 million, but as expected the cost also increased: from 0.82% to 2.08%. All in all, it still remains a solid performance, considering that interest-earning assets achieved an average return of 6.65% compared to 3.30% in Q1 2022.

{kind=link}

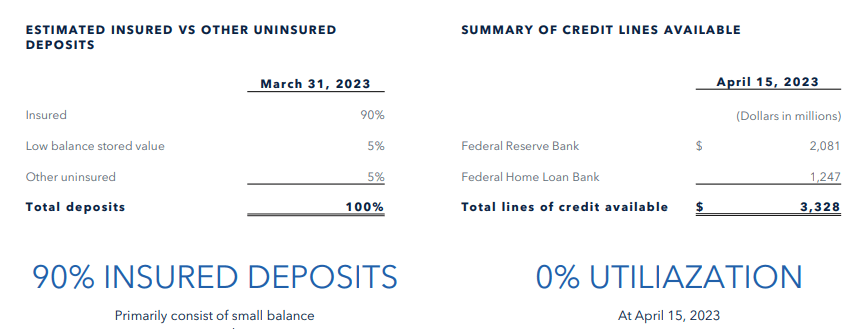

Finally, to conclude the discussion related to deposits, here are how many of them are insured.

{kind=link}

90% of deposits are insured, in particular we are talking about 130 million small accounts insured through the Bancorp's fintech ecosystem. Basically, the Bancorp's deposits are in a fortress, which is why the bank did not need any lines of credit to deal with a potential bank run. Many other regional banks have benefited from these lines of credit for precautionary purposes; in this case, there was no need.

In light of this data, liquidity risk is definitely under control at the moment. In any case, the same can also be said of the other major banking risks. Let us analyze them individually.

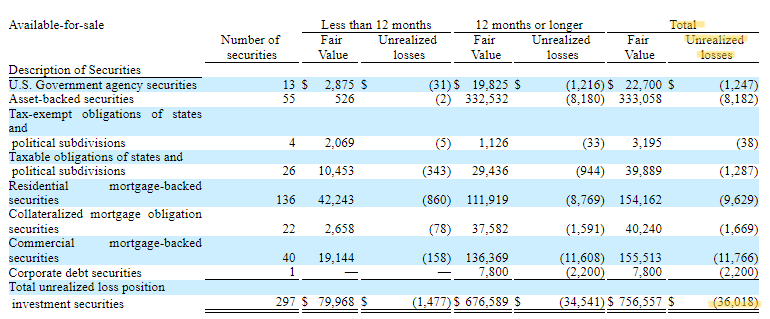

{kind=link}

Unrealized losses amount to about $36 million, only 27% of FY 2022 net income. In short, in no way they can be a problem; so market risk is also under control.

Let us now look at credit risk, starting with the current loan portfolio structure.

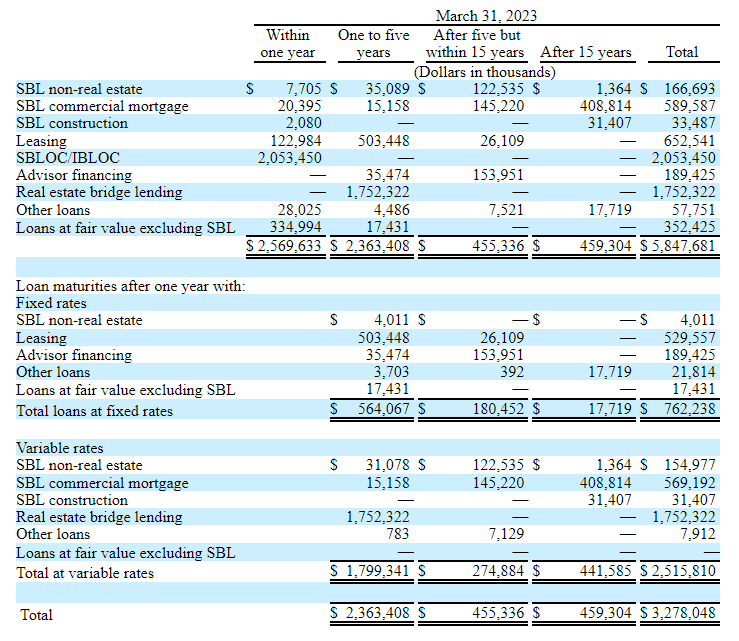

{kind=link}

As described in the opening section, the assets of this bank have the peculiarity of having mainly short- to medium-term maturities and a variable rate:

- Loans worth $2.56 billion, about 43% of the entire loan portfolio, will mature within a year. Much of it belongs to the SBLOC/IBLOC segment, or lines of credit whose collateral is securities within an investment portfolio.

- Loans worth $2.36 billion, about 40% of the entire loan portfolio, will mature between 1 and 5 years. Mainly these are real estate bridge loans.

- Loans with a maturity of more than a year amount to $3.27 billion and 76% of them have a variable rate. So it is not surprising that this bank has been performing very well since the Fed started raising rates.

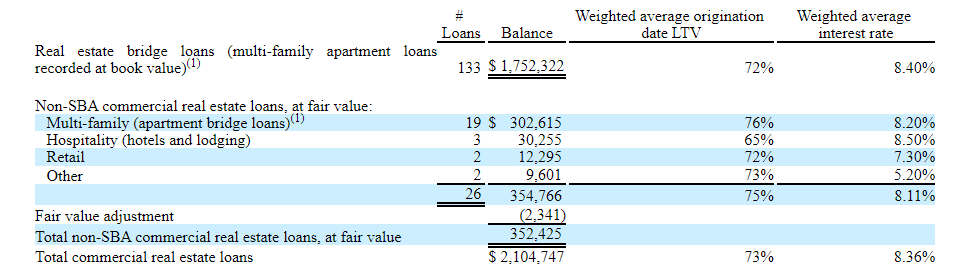

Going into more detail, especially in the risky CRE loans, here is the picture.

{kind=link}

In no segment the weighted average LTV exceeds 80%, and the weighted average interest rate is 8.36%. In short, two good results considering that delinquency rates remain low for the entire loan portfolio.

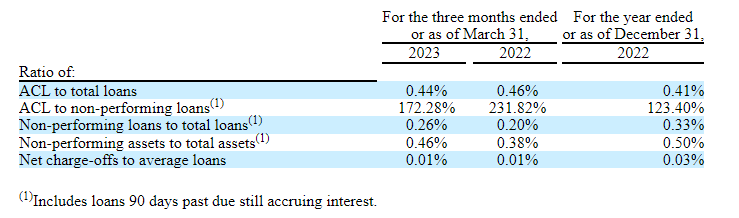

{kind=link}

Management is currently convinced that the increase in interest rates has not affected its customers' ability to repay their borrowings. CEO Damian Kozlowski also commented on this issue during the conference call:

The CRE is extremely stable. Now that the whole market has slowed down because there's been a huge repricing obviously because of the rise of interest rates. Our underwriting standards have not changed. We have interest rate caps on all the loans and floors and many times reserves. So we haven't had any dislocation whatsoever in that portfolio. And we've had a lot of the wind down of the old portfolio and people have been finding financing, take out financing. So we haven't had any, I can't really respond other than it slowed down a bit. I think that will pick up once you have, you stop having the steep curve in interest rates. But we have nothing to report really.

Conclusion

The Bancorp is an atypical bank because it has a predominance of short-term maturity assets and a variable interest rate. These two characteristics allowed its EPS to achieve a significant increase over last year, which is why its price per share has not collapsed like the benchmark ETF. Guidance for the full FY 2023 is positive, and at the moment the major banking risks are all under control. Of concern going forward is the major exposure to CRE, but the CEO does not see this as a problem right now.

Deposits are 90% insured, well diversified, and with a much lower cost than yield on assets. As for future strategy, in order to prevent net interest income from shrinking too much if the Fed lowers interest rates, fixed rate bonds will be purchased at the appropriate time.

Overall, I evaluate this bank positively, but I am quite doubtful about its current price per share. Over the past 10 years, the price/tangible book value per share has been 1.51x; multiplying this figure by the current book value per share of $13.11, Bancorp's fair value would be $19.79 per share. In short, the stock seems overvalued, and what's more, it doesn't even issue dividends. In any case, my rating is not a sell, as I think it can continue to do well in this macroeconomic environment with high interest rates.

For further details see:

The Bancorp: A Bank That Stands Out From The Crowd