TD - The Bank Of Nova Scotia: Value And High Yield

Summary

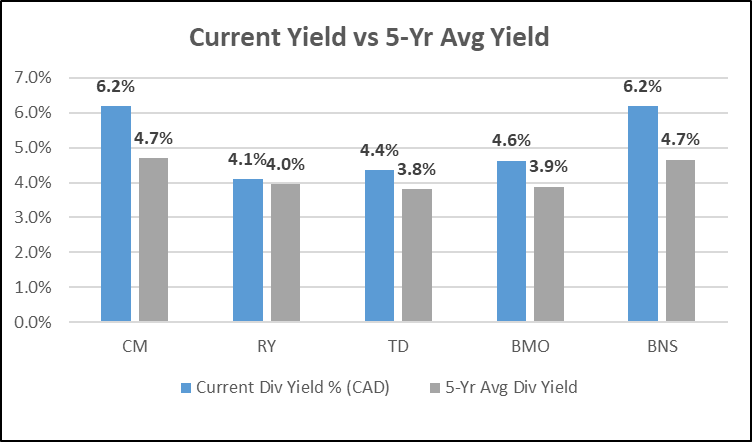

- The Bank of Nova Scotia is currently yielding 6.2%, a significant premium over its long-term average yield of 4.7%.

- The Bank of Nova Scotia dividend is well-covered with a payout ratio of 51%, in line with the bank’s 5-year average.

- The Bank of Nova Scotia declared its initial dividend on July 1, 1833 and hasn’t missed a payment since.

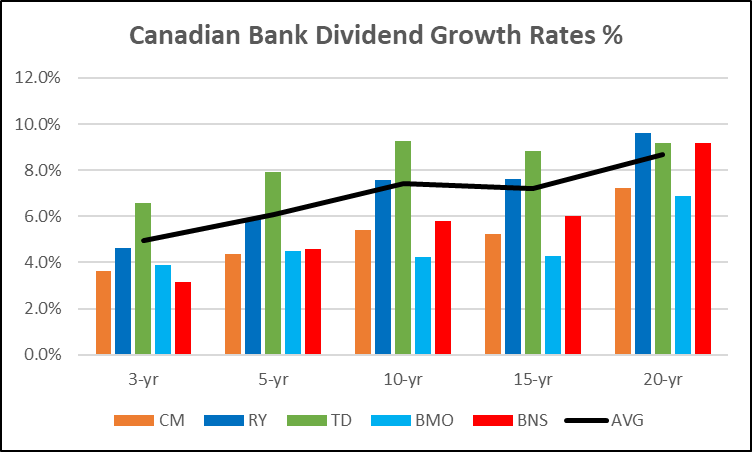

- Scotiabank has grown its dividend at CAGR of 9.2% over the last 20 years.

Author’s note: All figures in Canadian currency unless otherwise noted.

Opportunity

The Bank of Nova Scotia ( BNS ) ("Scotiabank") is a core holding for dividend growth investors. Scotiabank is currently yielding 6.2%, a 33% premium over its long-term average yield of 4.7%. The Bank of Nova Scotia declared its initial dividend on July 1, 1833 and hasn’t missed a payment since. Although the last few years have been slower, Scotiabank has achieved an incredible record of dividend growth with a CAGR of 9.2% over the last 20 years. While the share price may trade sideways in the short term as The Bank of Nova Scotia faces macroeconomic headwinds, the dividend is well covered and will continue to grow for decades to come.

Company Profile

Scotiabank is one of the six large banks in Canada that accounts for approximately 90% of the Canadian banking market. Limited foreign competition and high barriers to entry in the Canadian banking market make for high consumer switching costs and lower customer acquisition costs for the large incumbent banks.

The company operates predominantly in Canada, the United States and Latin America, especially the Pacific Alliance Countries of Mexico, Columbia, Peru and Chile. Scotiabank has reinvested the proceeds from its high margin Canadian operations, to build a significant presence in Latin America and the Caribbean. By market share, Scotiabank is a top three bank in Canada, Chile, and Peru and is the fifth and sixth largest bank in Mexico and Columbia respectively.

Scotiabank business mix (Scotiabank)

In recent years, the bank has made efforts to grow its wealth management business through large acquisitions such as Jarislowsky Fraser and MD Management in an effort to build up its lucrative wealth management business line.

The Bank of Nova Scotia has a market capitalization of $79B and assets of over $1.3T. The company has 90,000 employees and serves over 25 million clients in the Americas. Scotiabank trades on the Toronto Stock Exchange and New York Stock Exchange under the ticker “BNS” with daily average volume of 4.9M and 2.1M shares respectively.

Valuation and Recent Results.

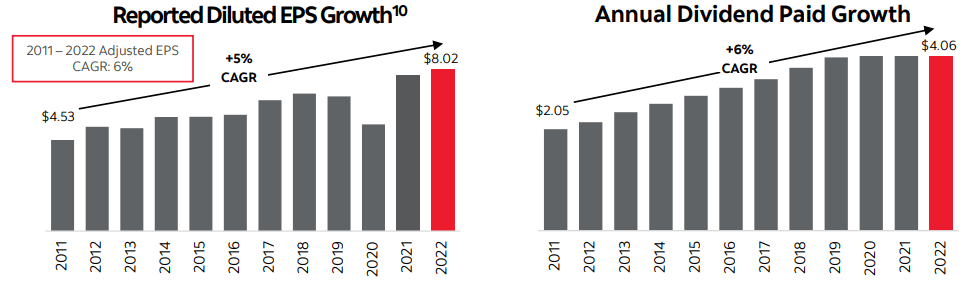

Shares of Scotiabank are down 27% over the past 12 months. As the bank prepares for the possibility of recession and slower lending activity, Scotiabank has set aside $529M in provisions for credit losses as of Q4 2022. While there is uncertainty for the year ahead, Scotiabank posted strong results for 2022 with reported Net income of $10.174B for the full year, compared to $9.955B in 2021. Over the same period, diluted EPS grew 4.2% to $8.02, from $7.70 in 2021.

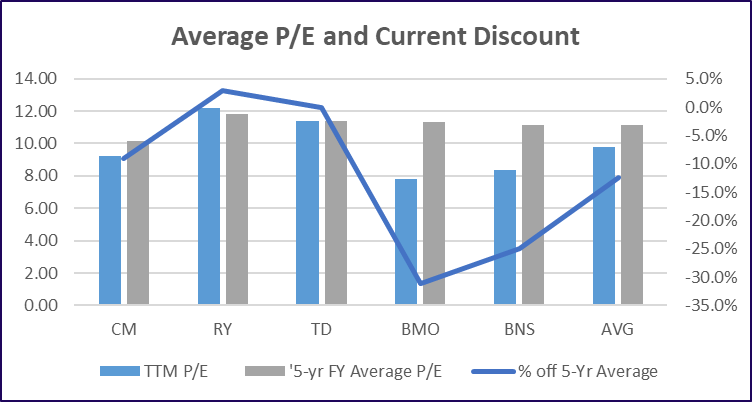

Despite these good results, Scotiabank’s shares have been under pressure. Scotiabank is currently trading at 8.27X earnings, a 24% discount to its 5-year average P/E of 10.87X. The consensus forward P/E is under 8.0X.

Average P/E and Current Discount (Table Source: Author; Data Source: Canadian Dividend All-Star List)

{kind=link}

Table Source: Author; Data Source: Canadian Dividend All-Star List.

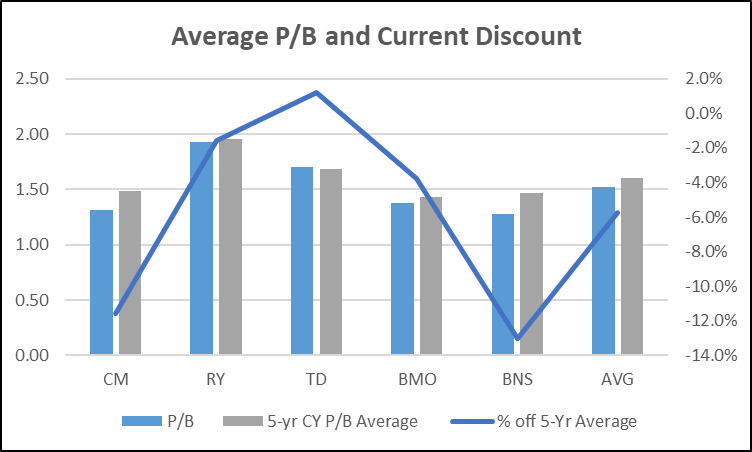

On a P/B basis, Scotiabank is trading at 1.27X, well below its historical average of 1.82x and the peer average of 1.63X.

Average P/B and Current Discount (Table Source: Author; Data Source: Canadian Dividend All-Star List)

{kind=link}

Table Source: Author; Data Source: Canadian Dividend All-Star List.

Both valuation metrics point to a substantial discount relative to the bank’s historic valuation and to its peers. Another indicator that share prices look undervalued is the company’s utilization of its NCIB. As of Q4 2022, Scotiabank had repurchased 32.9 million common shares, approximately 3% of total shares.

Compelling Dividend Opportunity

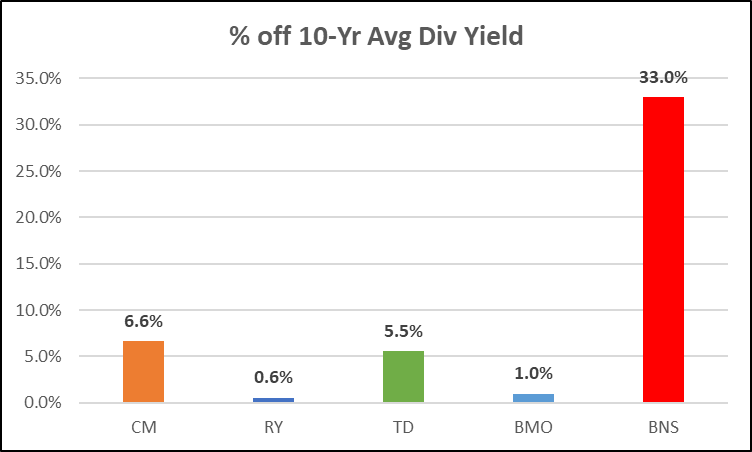

The Bank of Nova Scotia pays a quarterly dividend of $1.03 for an annual payout of $4.12. This dividend has doubled since 2011 when the company paid out $2.05 annually. At current share prices, Scotiabank is currently yielding 6.2%, a staggering 33% premium over the bank’s historic average dividend yield of 4.7%. This yield premium over the bank’s average provides an investor today the equivalent yield-on-cost of holding the stock for the past five years at 6% annual dividend growth.

% off 10-yr avg dividend yield (Table Source: Author; Data Source: Canadian Dividend All-Star List)

{kind=link}

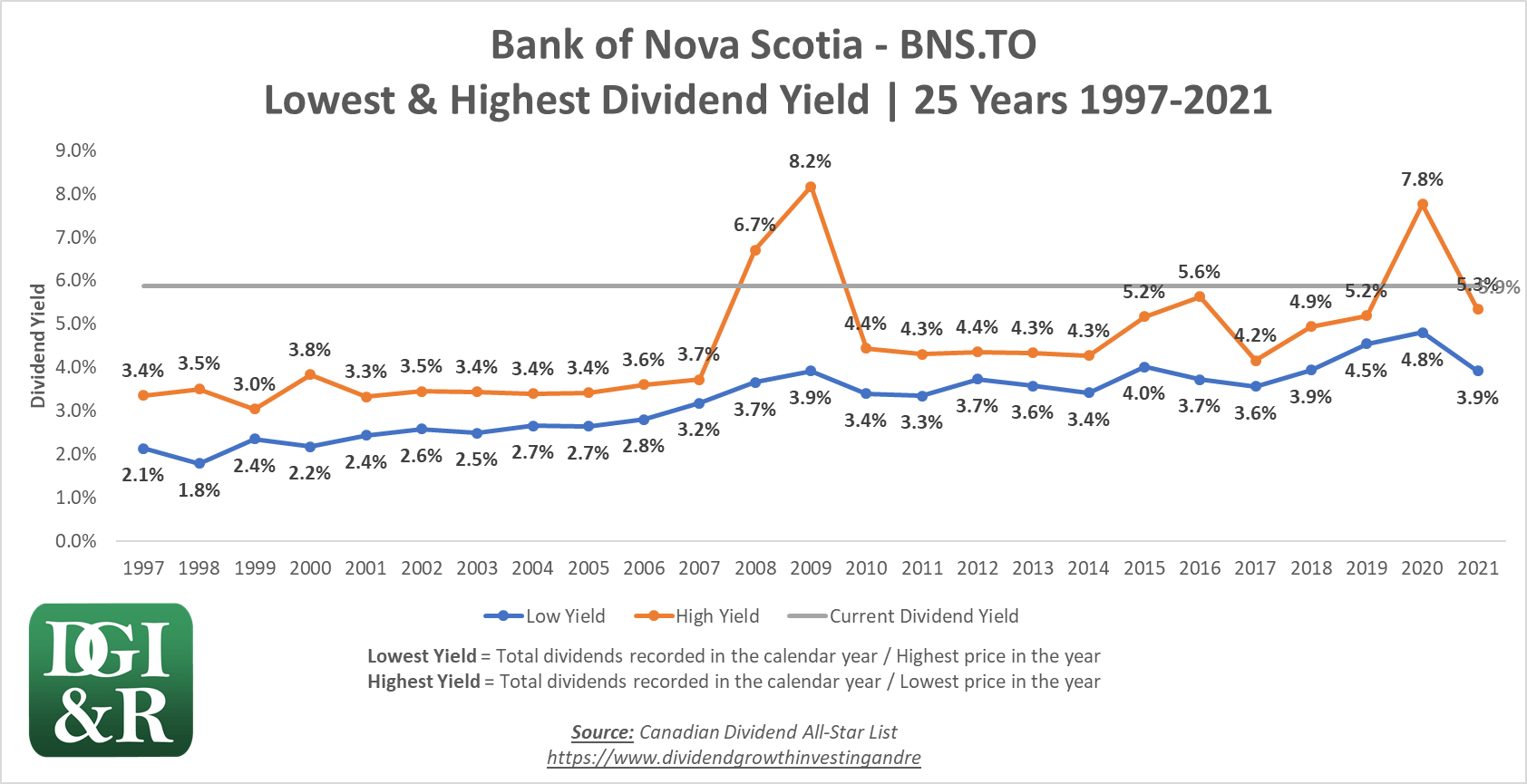

Scotiabank has an incredible history of dividend growth dating back 189 years. This dividend record has demonstrated the bank’s ability to continue to pay through wars and recessions. Scotiabank along with the other large Canadian banks maintained its dividend during the global financial crisis and throughout the COVID-19 pandemic. While the share price was battered during these two events, the dividend yield spiked, creating a great buying opportunity for dividend growth investors with long time horizons.

BNS Lowest and Highest Dividend Yield 25 yrs (Canadian Dividend All-Star List)

{kind=link}

Scotiabank's current dividend yield is very high relative to the company’s long dividend history. Over the past 25 years, the highest dividend during each calendar year has only surpassed the current yield of 6.2% on three occasions: 2008, 2009 and 2020. It is also a high current yield and yield premium relative to the other large Canadian banks.

Current & 5-Year Yield (Table Source: Author; Data Source: Canadian Dividend All-Star List)

{kind=link}

Steady earnings growth from Scotiabank's protected business model has resulted in dividend increases in 43 of the last 45 years. In the years since the global financial crisis, Scotiabank has offered dividend investors a 6% CAGR. This predictable dividend growth is supported by steady and resilient earnings growth, averaging 5-6% annually since 2011. The dividend is well covered, with a payout ratio of 51%, in line with the bank’s 5-year average of 53%.

{kind=link}

Relative to its peers, Scotiabank has an above average dividend growth rate over the long-term and an average dividend growth profile in recent years.

Canadian Bank Dividend Growth Rates (Table Source: Author; Data Source: Canadian Dividend All-Star List)

{kind=link}

Risk Analysis

During the COVID-19 pandemic, the Office of the Superintendent of Financial Institutions ((OFSI)) restricted Canadian financial institutions from increasing dividend payments to shareholders in an effort to ensure stability and adequate capital in the Canadian banking system. This restriction was lifted in November 2021 and the banks have resumed dividend increases. Should there be another material shock to the Canadian banking system, OFSI could impose similar restrictions to freeze dividends at current levels.

Scotiabank has more international exposure than its peers, making it vulnerable to political and economic risks from developing markets in Latin America. This positioning also promises tremendous growth potential however as the young population of the Pacific Alliance Countries is an attractive counterbalance to the more mature economy and demography of the domestic Canadian market.

Scotiabank has the least proportional exposure to the domestic Canadian market among the big six Canadian banks, with nearly 50% of operations outside of Canada. This helps to dampen its exposure to the Canadian housing market relative to other large Canadian banks with large mortgage books.

The Canadian banking sector could see slower lending activity in the event of a recession. Scotiabank's amassing of over $500M in provision for credit losses implies the bank sees that the coming year could bring an increase in loan impairment. Scotiabank is well capitalized to head into a recession with a common equity tier 1 ratio of 11.5%. As recently as April, 2022, DBRS reaffirmed Scotiabank’s Long-Term Issuer Rating at AA with all trends rated as stable.

BNS Senior Debt Ratings (Scotiabank)

For a closer look at Scotiabank’s operations and additional risk analysis, please see my other coverage of BNS here .

Investor Takeaways

For investors looking for an attractive dividend income name, this is an excellent entry point for a strong total return. There are other Canadian banks that I like better than Scotiabank overall including Royal Bank of Canada ( RY ) and The Toronto-Dominion Bank ( TD ), however with Scotiabank's current yield and cheap valuation, it is my preferred bank to buy today. This is a great opportunity to lock in a 6.2% dividend yield from a company that can provide visibility towards dividend growth and safety.

For further details see:

The Bank Of Nova Scotia: Value And High Yield