FSUGY - The Bear Case For Iron Ore

2023-04-26 06:01:03 ET

Summary

- Mining companies heavily depending on iron ore extraction have booked high margins over the last years on the back of elevated ore prices.

- The majority of demand for iron ore comes from China, which is why expectations for this economy matter.

- Unfortunately, a shrinking population and slowing growth of the economy do not bode well.

- In addition, Chinese officials have indicated a willingness to curb 'unreasonable' ore prices and started to coordinate iron ore purchases.

- A diminishing population, reduced growth, and state-backed effort to control ore purchases are expected to put prolonged pressure on ore prices.

Since March ore prices have been trending down as re-opening of the Chinese economy has not led to the expected surge in demand. In spite of several companies maintaining an upbeat outlook considering the demand for iron ore ([[SCO:COM]], [[TIOC:COM]]), data presented in this article suggests otherwise.

The goal of this article is to help understand readers which risks are tied to a potential investment in iron ore oriented miners such as Rio Tinto (RIO), BHP (BHP), Vale ( VALE ) and Fortescue ([[FSUMF]], [[FSUGY]]).

Dependency on ore

Some of the largest miners worldwide have been profiting from elevated ore prices over the last two years. As a result, shareholders have been rewarded with generous dividends and share buybacks programs. While these outsized dividend yields may seem appealing, investors should assess the bear case before making an investment.

The next table shows the relevance of iron ore for several miners. For all of these companies the relevance of this commodity is huge and consequently the results largely depend on the pricing of ore.

Table 1 - Ore revenues versus total revenues (riotinto.com, bhp.com, vale.com, fmgl.com.au; table by author)

Instead of trying to predict the ore the price, and being a dividend investor, I've assessed at which price Rio would still be able generate a decent dividend yield. This number turned out to be comparatively low at US$81/t. In this article it will be explained why the number may not be so low after all.

Demand drivers

In a recent earnings call Fortescue's Fiona Hick struck an upbeat tone about the Chinese steel demand:

We're still quite optimistic on China's crude steel production and demand for certainly this calendar year and beyond. There have been rumours, you're right, of production cuts in recent weeks, but our analysis suggests that demand in China is actually going to increase year-on-year.

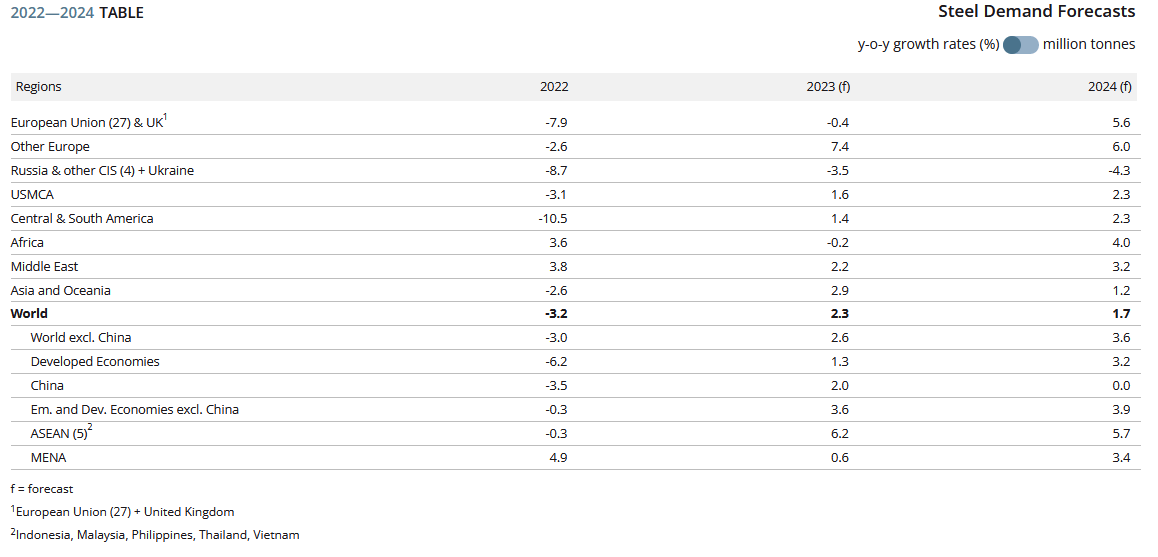

This remark stands in contrast to the latest outlook of the World Steel Association, see figure 1. The forecast shows Chinese demand will slightly grow in 2023, but is expected to remain flat in 2024.

Figure 1 - Steel demand forecast until 2024 (worldsteel.org)

{kind=link}

To give some more context to the numbers in this figure it must be mentioned that the steel demand of China alone covers 50% of total worldwide demand. Therefore, considering iron ore, it matters what happens in China. And the drivers for Chinese demand seem to be faltering.

An omnipresent cited reason for growing ore demand has been the re-opening of China after Covid. There are however multiple reasons why re-opening of the Chinese economy may not bring the expected tailwind for demand. The following four reasons will be discussed:

- Population shrinking

- Growth reducing

- Concerted buying

- Climate

Population shrinking

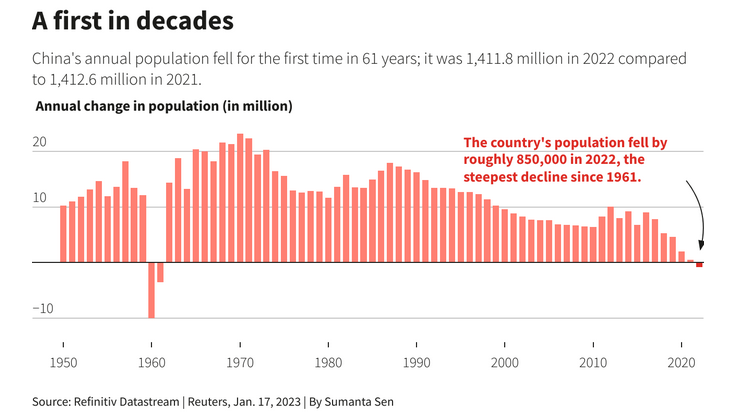

In January headlines surfaced indicating China's population was shrinking. Figure 2, compiled by Reuters, shows the annual change in population since 1950.

Figure 2 - China's annual change in population (reuters.com)

{kind=link}

Without a doubt population growth has been trending lower for decades eventually resulting in a decline last year. Inevitably this is the result of the one-child policy. Not visible in the numbers is the fact this policy has created a gender imbalance as well, with boys being favored as explained in the referenced article. This did not go unnoticed and policy changes have been implemented. The question is if this will make a difference over the short to medium term.

One effect of the one-child policy is pejoratively known as the little emperor syndrome . The narrative is children have been lavished with attention as they had no siblings. Whether or not this is true, children will more often have to take care of their ageing parents.

While taking care of one or two ageing adults can already be a demanding task, the additional responsibility of raising a new-born may be perceived as too much for someone who is used to be taken care of. Obviously, the assumption is made that sufficient income is generated in a household to make ends meet in the first place, and either of the adults can tend to family members.

Long story short, one can understand why 'U.N. experts see China's population shrinking by 109 million by 2050'.

Growth reducing

Growth has often been lauded as the hallmark of the Chinese economy. While this is certainly true, it must be said growth has been diminishing over the last decade, see figure 3.

Figure 3 - Chinese GDP growth (seekingalpha, ycharts)

Moreover, the IMF expects Chinese GDP growth will further slow towards the end of this decade, see figure 4. Linking figures 3 and 4, it can be seen high single digit growth percentages are a thing of the past. Moreover, it must be remembered the slowing growth after 2010 was booked at a time when Western governments were still supporting the economy and consumers were spending, supporting Chinese export.

Figure 4 - Chinese growth slowing (imf.com)

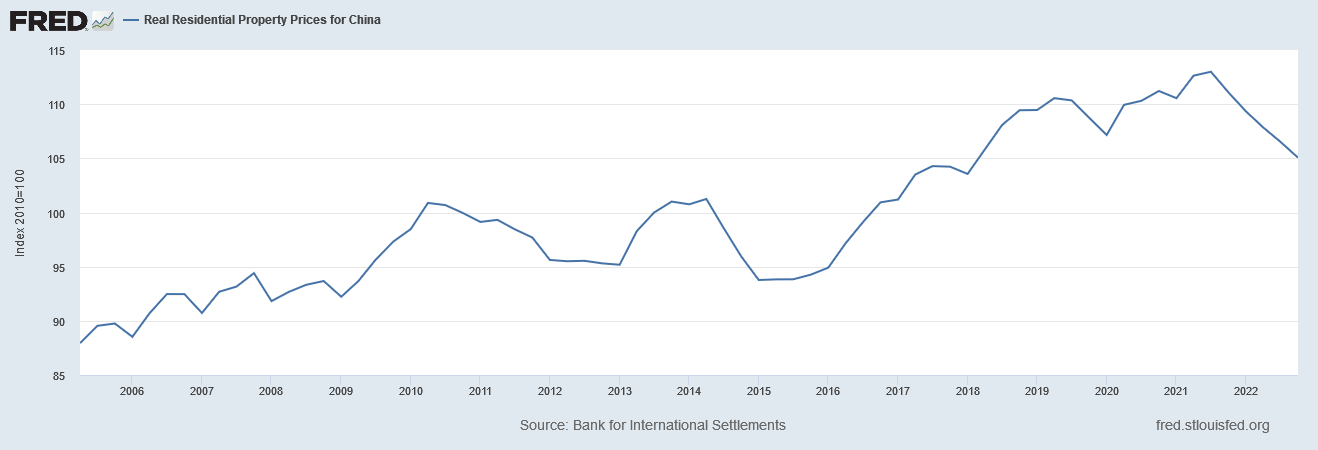

A telling sign of slowing growth is that residential property prices have been declining as well over the last quarters. Figure 5 shows property prices have been reducing since reaching a high in 3Q21. Even through lockdowns property prices have been climbing, apart from 1Q20, but this trend has now reversed. Probably the most high profile example of the state of affairs in the real estate market is Evergrande, the world's most indebted property developer.

Figure 5 - Residential Property prices for China (Bank for International Settlements, Real Residential Property Prices for China, retrieved from FRED, Federal Reserve Bank of St. Louis;)

{kind=link}

Concerted buying

Typically, the attention span of investors is shorter than that of Chinese policy makers. As demonstrated in figure 2, policy in China can span decades. The relevance becomes clear when its considered that state-backed China Mineral Resources Group (CMRG) was launched last year. This fact was highlighted before in an article on Rio Tinto, assessing how lower ore prices would affect the dividend.

The goal of CMRG is to strengthen the position of China when it comes to buying iron ore and as such reduce the price of this commodity. With China being the largest importer of iron ore in the world, CMRG is forecasted to become the largest buyer worldwide as soon as this year, 2023. Instead of just importing, CMRG 'is also aiming to develop domestic iron ore resources, and oversee development of mines overseas'.

Reverting to the point on policy, the creation of CMRG seems to be a further implementation of the Belt and Road Initiative . While inevitably this has an upside for China, investors should weigh this in their decision to hold shares in aforementioned mining companies, especially as China's Reform commission has been more vocal concerning the current level of ore prices:

China's National Development and Reform Commission said late Friday it would look again at measures to curb "unreasonable" iron ore prices and urged trading firms to avoid hoarding and inflating prices.

Climate

Besides macro-economic factors such as GDP, population growth and concerted buying, China possesses a more direct option to influence prices. As the Chinese capitalistic system is anything but a free market, the government has the ability to influence demand by imposing production curbs. A recent piece on Bloomberg noted the following:

The city of Tangshan, a steelmaking hub in north China, has started production restrictions to try to clear its skies ahead of some major political meetings in the country.

As officials are able to turn on and off the industry in a city as they wish, the potential exists to do this on a larger nationwide scale as well. And as it currently stands, this is exactly what is about to happen.

According to several media outlets China weighs the option to cut steel output for the third year in a row to meet emission targets. Whether the main reason for the cuts is to meet emission targets or sway ore prices is not exactly clear. What is clear however is that the country has multiple ways to affect ore prices, a notion investors should be astutely aware of.

Conclusion

While one may argue any of the reasons mentioned in this article is not sufficient to suppress ore prices single-handedly, this ceteris paribus assumption doesn't do just to the complexity of reality.

A diminishing population, reduced growth and state-backed effort to control ore purchases are expected to put prolonged pressure on ore prices. On top of this, policymakers in China have the ability to influence steel production at will. Even at lower ore prices an investment in miners such as Rio Tinto, BHP, Vale and Fortescue can yield satisfactory results as long as the bear case is kept in mind and deemed acceptable.

For further details see:

The Bear Case For Iron Ore