XHB - The Bears Got 2023 Wrong But There Is Hope For Them Yet

2023-12-21 20:41:51 ET

Summary

- We foresee that the low-hanging fruits for alpha will become increasingly difficult to find.

- Even though we still expect 2024 to be a decent year for the S&P 500 Index, we think returns are more likely to be in the moderate 5%-10% range.

- This article is specially dedicated to the undecided bears. We are concerned that the undecided bear is in an increasingly precarious position of potentially missing out on a muti-year bull market.

- We still see opportunities for those who are late to the rally to play catch-up by investing in laggard themes including residential REITs, biotechnology, and healthcare.

- Instead of simply chasing the S&P 500 because of the fear of missing out, we think investors should be more strategic by investing in high-quality laggards.

If the title of this article appears to be hinting that we are turning bearish on U.S. equities, we apologise for baiting the bears. Not only have we taken advantage of the market bottom in October 2022 to overweight U.S. equities and aggressively load up on deeply discounted names that have outperformed meaningfully since, but we still see room for further gains in 2024.

Having said that however, we foresee that the low-hanging fruits for alpha will become increasingly difficult to find. With the S&P 500 Index ( SP500 ) trading at around 22.6x Trailing P/E at the time of writing, most of the good news may have already been priced in. Futures markets are already pricing in more rate cuts than the Fed is communicating. Leading technology stocks and AI-related themes, in particular, may already be reflecting optimistic future cashflows that may or may not materialize.

{kind=link}

Even though we still expect 2024 to be a decent year for the S&P 500 Index, we think returns are more likely to be in the moderate 5%-10% range instead of the strong 15%-25% range that the index is on track to achieve this year. At the time of writing the S&P 500 has already gained 22.4% year-to-date.

For passive investors who have adopted the buy-and-hold approach and rode the S&P 500 Index ( SP500 ) to near all-time highs, it might be sensible to temper expectations for passive equity returns in the year ahead. We think 2024 will be a year where active investing will play a much bigger role in generating equity returns and portfolio alpha.

But this article is specially dedicated to the undecided bears. We are concerned that n ot only is the undecided bear in an increasingly precarious position of potentially missing out on a multi-year bull market, but the long-term consequences of trying to time the markets and staying on the sidelines would only put retirement plans in jeopardy.

If you are an investor who is not convinced that the economy is going to do just fine and muddle through all that aggressive monetary tightening, yield curve inversion, bank runs, ballooning national debt, and even that long-awaited property market crash, then this article is for you.

It is not too late to recover from the mistake of missing the market bottom and to start investing with discipline, but time is running out.

The Risks Are Much More Manageable Than You Think

For the bears who are still holding out for a stock market crash, perhaps it is best to swallow their pride and move on.

Inflation has been trending lower since July of 2022 and is now just a whisker away from the Federal Reserve's (Fed) 2% target. In hindsight, the stagflation risks that were so confidently touted by the doomsayers have turned out to be nothing more than lingering memories of the 1970s.

Although there is conclusive evidence to show that economic activity is cooling and the risks of a recession are real, we argue that the Fed now has the option to stimulate the economy by cutting interest rates if needed. That option was unfeasible when inflation was 9%. But with inflation largely in control now, an economic recession becomes merely a policy consideration for the Fed.

Of course, the Fed's ultimate goal is to engineer a soft landing. And we think the Fed has a pretty good chance of nailing it this time. We understand that the Fed has an abysmal track record at engineering soft landings. But we think there are good reasons why this time could be different.

Property Prices Are Not Falling

First and foremost, we argue that the fate of the U.S. economy is intimately tied to the health of real estate, in particular, residential real estate. In previous rate hike cycles, residential real estate prices tended to fall significantly in response to higher mortgage rates depressing demand for new homes while sellers would dump speculative investment properties that were highly leveraged. In a normal economic environment where demand and supply of real estate are somewhat in a healthy equilibrium, shifts in interest rates would indeed have the intended effect on prices.

However, because the U.S. housing market was experiencing more than a decade of underbuilding and there was a persistent short supply of housing, higher mortgage rates did not cause home prices to crash. Furthermore, because investment properties are no longer as highly leveraged compared to during the subprime crisis of 2007, sellers are simply not rushing for the exit. Having already locked-in 30-year mortgages at a low 3%-4%, homeowners are also not keen to sell or upgrade their properties which are going to come with a much higher mortgage rate of around 7%.

Hoya Capital

On the other hand, many young families wishing to purchase a property today are increasingly being priced out of the single-family home market. Many will have little choice but to settle for multi-family homes. Some may have to resort to renting temporarily. In fact, there is so much pent-up demand for housing that we think any dip in home prices is only going to draw buyers back to the market.

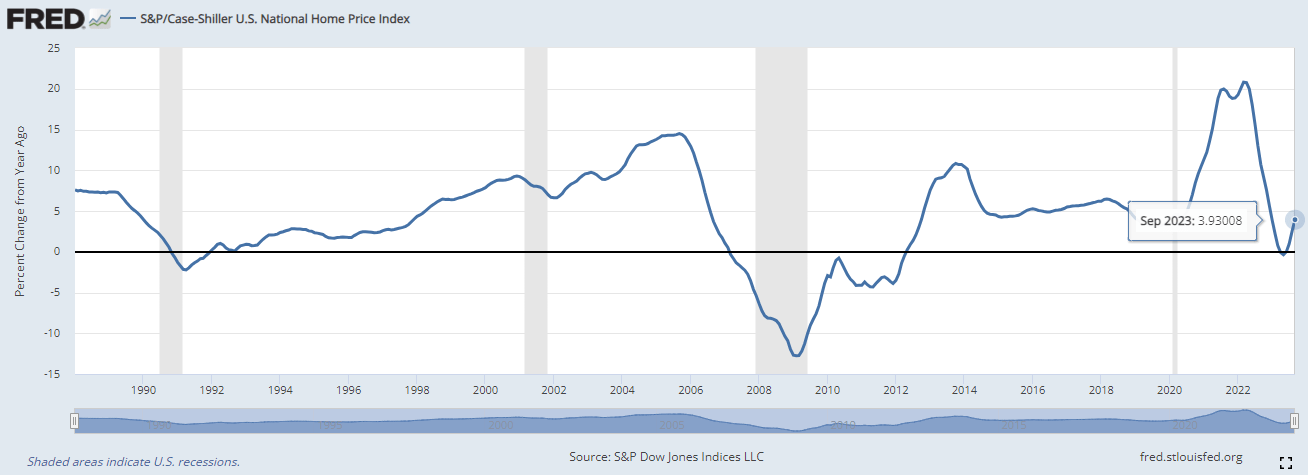

Despite all the sensationalized news offered by the financial media claiming that the housing market is experiencing a severe downturn and that home sales have collapsed, home prices have hardly fallen at all. As the accompanying chart shows, the S&P/Case-Shiller U.S. National Home Price Index only briefly went negative year-on-year in April-June before home prices continued to climb. As of September, home prices were still up 3.9% from a year ago.

{kind=link}

This pent-up demand for housing and the unwarranted pessimism that is still holding back the residential real estate market means that we see opportunities for residential REITs, homebuilders, and real estate asset managers to outperform in 2024.

Valuations on our favourite homebuilder names including D.R. Horton ( DHI ) and the broader SPDR Homebuilders ETF ( XHB ) have improved significantly since we initiated our bullish view . But residential REITs such as Mid-America Apartment Communities, Inc. ( MAA ) and Camden Property Trust ( CPT ) have only recently started to play catch-up with the S&P 500. We plan to initiate coverage on MAA and CPT with a bullish view soon.

As for real estate asset managers, our bullish view on Blackstone Inc. ( BX ) has played out really well and we have only recently dialled down our bullish view . Bridge Investment Group Holdings Inc. ( BRDG ) is currently our favourite real estate asset manager given that the stock has only recently begun to move up (we still maintain a "Strong Buy" rating on BRDG).

The Consumer Is King

The second reason that we think explains the exceptional resilience of the current economy, is the healthy job market, which in turn supports robust private consumption. The U.S. economy is rather unique compared to other developed countries in that around 70% of U.S. GDP is driven by private consumption. What that means is you only really have to understand the consumer to know how the economy is doing. This is an important point because the financial health of the consumer is subjected to the strength of the job as well as wealth effects.

The U.S. job market is robust for several reasons, but one of the main factors is the early retirement of older workers during the COVID-19 pandemic. This resulted in significantly more job openings than workers available to fill them, leading to moderate increases in real wages and supporting consumption.

In terms of wealth effects, we argue that because home prices did not crash as many were expecting, there was no destruction of wealth like in many of the previous recessions in the past. Generous cash handouts by the government, combined with other fiscal stimulus, also had lingering positive effects to this day. All of which have helped to keep private consumption resilient.

All these factors created a rather benign economic environment that supported our thesis for a resilient economy even in the face of aggressive monetary tightening by the Fed.

Equity Markets Need A Lot More To Crash

We see little reason to think that equity markets should crash just because there are some uncertainties in the economy. In fact, when has investing ever been an endeavour without uncertainties and risks? And this is the critical mistake we think the bears made.

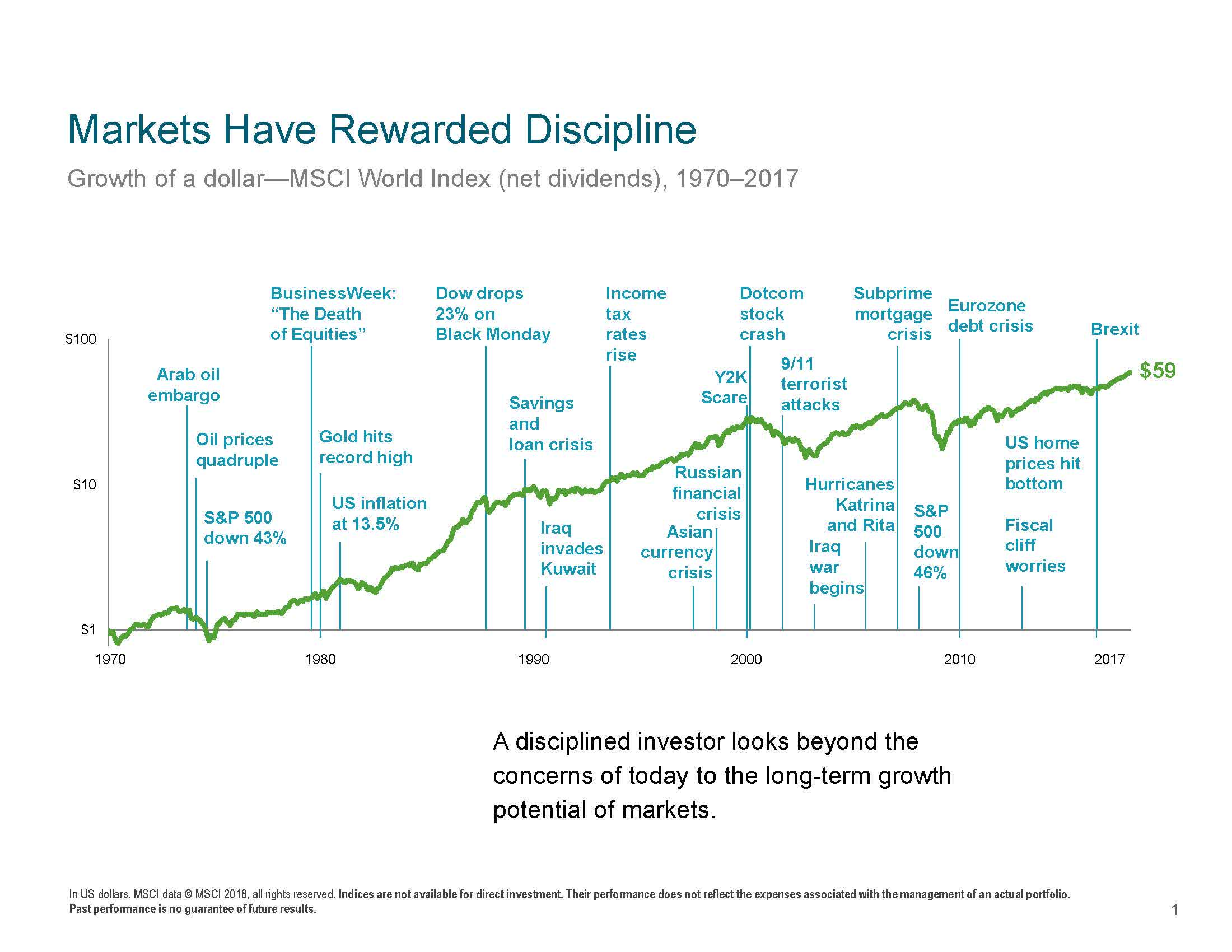

Recall the previous bull market from 2009-2020, which is one of the longest in U.S. financial history. That bull market weathered through the European Sovereign Debt Crisis that peaked between 2010 and 2012, Brexit in 2016, and the US-China trade war that began in 2018. There were countless mini-crises and risks along the way too and all these risks were sensationalized by the financial media every single time. The only event that eventually broke the bull market was the Covid-19 pandemic. Interestingly, Covid-19 was probably the least expected risk to trigger a bear market and of course, we can't blame anyone for failing to predict it.

{kind=link}

What the bears should understand is that economic recessions are necessary to justify predictions for a bear market, but economies do not simply go into a recession because of mere risks. Risks may temporarily impact business investment decisions, and cause concern for consumers, but risks alone rarely result in recession. More often than not, there has to be some form of tangible destruction of value or demand somewhere within the economy. Just like how investment banks suddenly realised that collateralized debt obligations on their balance sheet had become worthless in 2009. Or contagious bank runs or corporate defaults where losses reverberate through the economy. A drastic cut in government spending or monetary tightening by the Fed could have the same effect, all else equal.

Narrow Rally Means Don't Chase The Market, But Pick High-Quality Laggards

We still see opportunities for those who are late to the rally to play catch-up by investing in laggard themes including residential REITs, biotechnology, and healthcare. Instead of simply chasing the S&P 500 higher because of the fear of missing out, we think investors can be more strategic by investing in high-quality laggards. This strategy is not only suitable for the undecided bears but should also benefit passive investors who are sitting on huge gains from riding the equity rally. In essence, we favour investing in value over growth themes.

{kind=link}

We have already shared some ideas on residential REITs, but we also see our biotechnology picks such as the SPDR S&P Biotech ETF ( XBI ) and healthcare pick Pfizer Inc. ( PFE ) as potential outperformers in 2024.

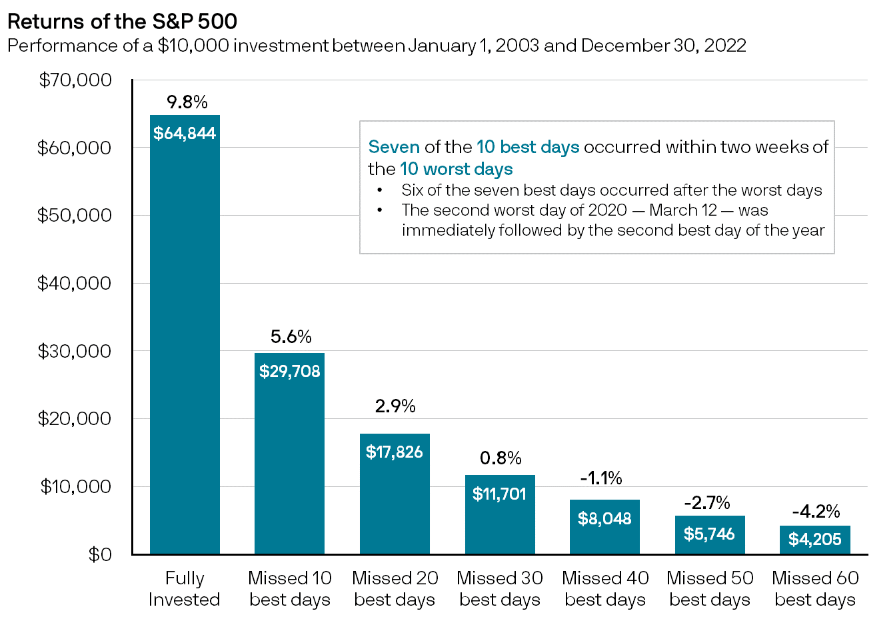

But such opportunities don't wait around forever and missing a bull market could prove to be extremely costly for one's retirement portfolio over time. Here is some interesting research . According to data compiled by the research team at J.P. Morgan, just missing the 10 best-performing days of a bull market would slash return performance almost by half during the period studied (2003-2022).

{kind=link}

Investors who try to time markets with precision are essentially putting their entire retirement portfolio at risk. And with compound returns, missing a multi-year bull market means compounding one's mistake over several years. We just don't see how sitting on the sidelines is a good strategy at all. Instead of adopting an "all or nothing" mentality to taking equity risk, why not accept realistic equity returns long term (~9%-10%) and compound those returns over time?

Often when we ask that question to traders, we get the same answer: if we can avoid the drawdowns entirely or perhaps do better than 10%, why not? Well, we think because if you do fail and most do, then your long-term retirement plan will become many times more difficult to achieve. It is just not worth taking the risk unless you are sure you have the right crystal ball to predict major market turning points. Greed is what drives the desire to time markets and this is why "all or nothing" short-term strategies will remain popular.

The sooner the bears understand they are fighting a losing battle with negative expectations and that they have looking at the wrong places all along, the sooner they can start looking for that real edge in investing.

For further details see:

The Bears Got 2023 Wrong, But There Is Hope For Them Yet