PHD - The Best Distribution Is The One That Was Just Raised

Summary

- Bond funds suffered the worst year in decades in 2022, yet still outperformed stocks.

- With rising yields, depressed prices, and improving credit spreads, fixed income funds offer a once in a lifetime opportunity for income investors in my opinion.

- Several fixed income CEFs increased the monthly distribution multiple times during 2022, yet still trade at discounts to NAV offering investors potential for capital appreciation along with increasing income.

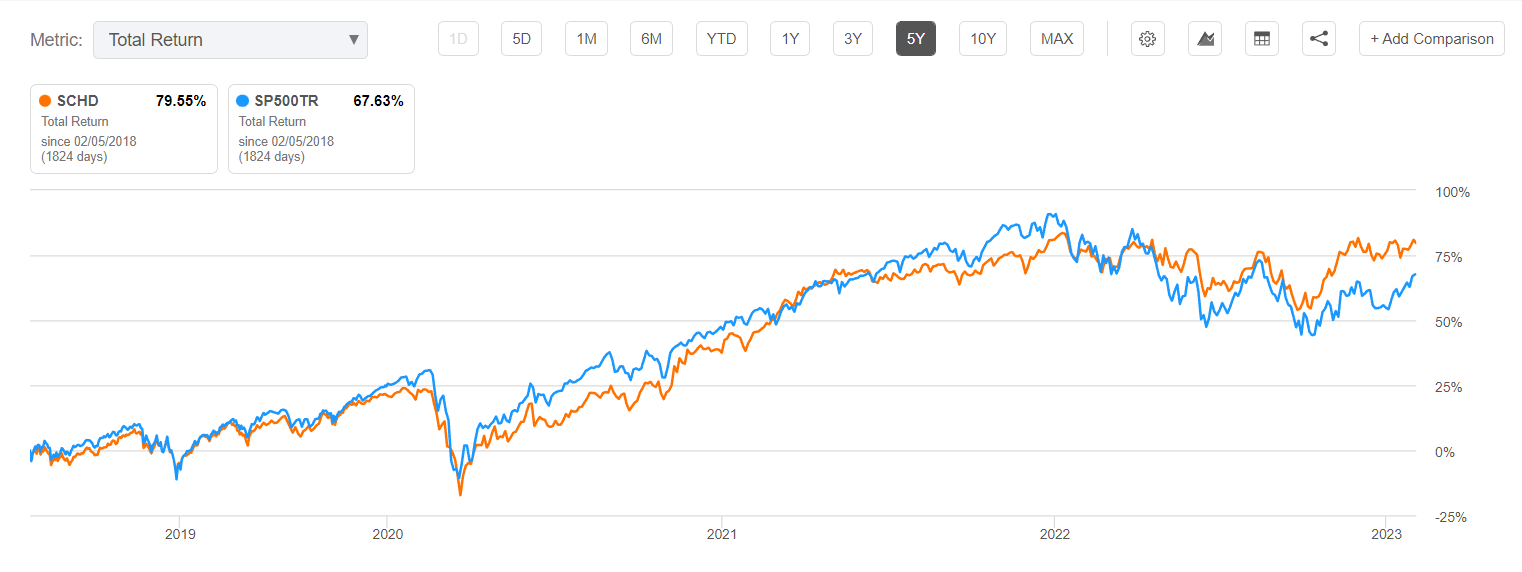

What is the best investment for generating income in retirement? Some might say an annuity because it offers guaranteed returns with peace of mind knowing that despite a recession or stock market crash, that income stream is still there when you need it (at least, until it matures). Others may prefer the long-term performance of stocks, including dividend growth investors who like the DGI approach to offset inflation over long periods of time. One popular fund that offers investors a DGI approach in an ETF format is the Schwab U.S. Dividend Equity ETF ( SCHD ), currently offering an annual yield of about 3.3% with some potential for price appreciation. Over the past 5 years, SCHD has slightly outperformed the S&P 500 index by about 12% based on total return with dividends reinvested.

{kind=link}

The drawback to SCHD for someone like me who is approaching retirement age is that I would have to sell part of my capital investment in SCHD in order to realize those gains if I needed the income. The 3.3% distribution by itself is not enough income to live off, with inflation currently above 6% and interest rates approaching 5%. If my goal was to increase my total return over the next 10 years, then I would find SCHD very attractive and would probably include it as part of a diversified retirement portfolio. That is, unless stocks enter an extended bear market that some predict could last for the next 10 years, in which case SCHD may not continue to generate those strong positive forward returns that it has over the past 5 years.

Many income-oriented investors are looking at a once in a decade opportunity in fixed income. At least, according to Pimco, 2023 is the beginning of a new Bond cycle that offers the highest yields, spreads, and total return potential in years.

We believe fixed income markets offer better value than they have in years. Real yields are the highest since 2008 and spreads are robust, which could be conducive to both attractive income generation and potential capital gains.

While stocks generally outperformed bonds by nearly 2 to 1 from 2009 to 2021 according to this Forbes article from May 2021, the trend started to turn at the end of 2022 as bonds performed better than stocks in 2022, although both stocks and fixed income performed poorly for most of the year.

In fact, 2022 was the worst year for bonds in the 97-year history of NASDAQ. Bonds, as measured by the Vanguard Total Bond Index ( BND ), lost 13.7% in 2022. But in the one-year period from January 2022 to January 2023, bonds performed less poorly than stocks.

{kind=link}

Now as we begin the second month of 2023, both stocks and bonds are turning bullish again, however, the prices of many fixed income funds remain depressed and trade at discounts to NAV even though the NAV of those funds is beginning to trend upward again. And according to some market watchers such as BofA Securities , the first half of 2023 offers fixed income investors an advantage over stocks as fears of recession continue to loom.

In 2022, financial markets sustained a number of shocks, particularly from inflation and interest rates, which were very destructive for bond and equity prices. But we’re a lot of the way through those challenges now, and for 2023, we’re bullish on bonds in the first half of the year and on stocks in the second half.

For investors who wish to buy low and realize the rewards of fixed income funds that offer high yield distributions at relatively low risk, now is the time. I am taking advantage of this opportunity to add several fixed income funds to my No Guts No Glory retirement portfolio so that I can compound that income over time as the distributions continue to be paid, and in many cases are increasing. The market prices of the funds also offer some capital appreciation for those interested in total return as the NAV also rises.

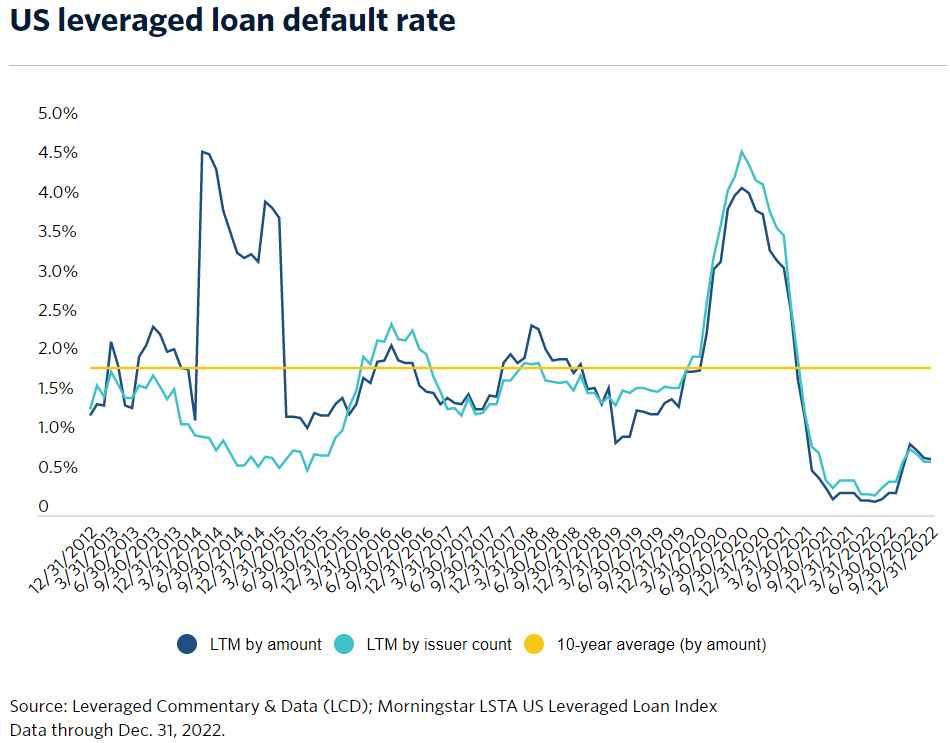

Furthermore, financial conditions appear to be easing as inflation is coming down and the Fed is looking to put the finishing touches on rising interest rates in the first half of the year. The bullish optimism in the markets may be too much too soon, but in the meantime, default rates on leveraged loans remain near historic lows despite rising slightly in January as indicated in the chart below from Pitchbook . Historically low default rates offer an enhanced level of risk mitigation for fixed income funds that generate income from senior secured loans and corporate bonds.

{kind=link}

Falling NAV, Rising Distributions

Based on many comments that I have been reading lately, there is a bit of a debate raging between income investors such as myself, and total return investors who are more concerned with the capital appreciation plus income generated over time. I have reviewed several fixed income funds recently that offer high yield distributions while often trading at a discount to NAV, and some commenters have noted that the NAV is “falling” and therefore the fund is not worthy of consideration. In this article, I would like to briefly discuss several fixed income funds that offer forward distribution yields exceeding 10% annually, that have all raised the monthly distributions at least 3 times over the past year, and in one case, 6 times!

It is true in some cases, that the NAV of fixed income funds has been falling over the past several years due to the poor performance of fixed income assets overall. But as I mentioned above that trend appears to be changing and this could offer income investors an opportunity to get in while the getting is good!

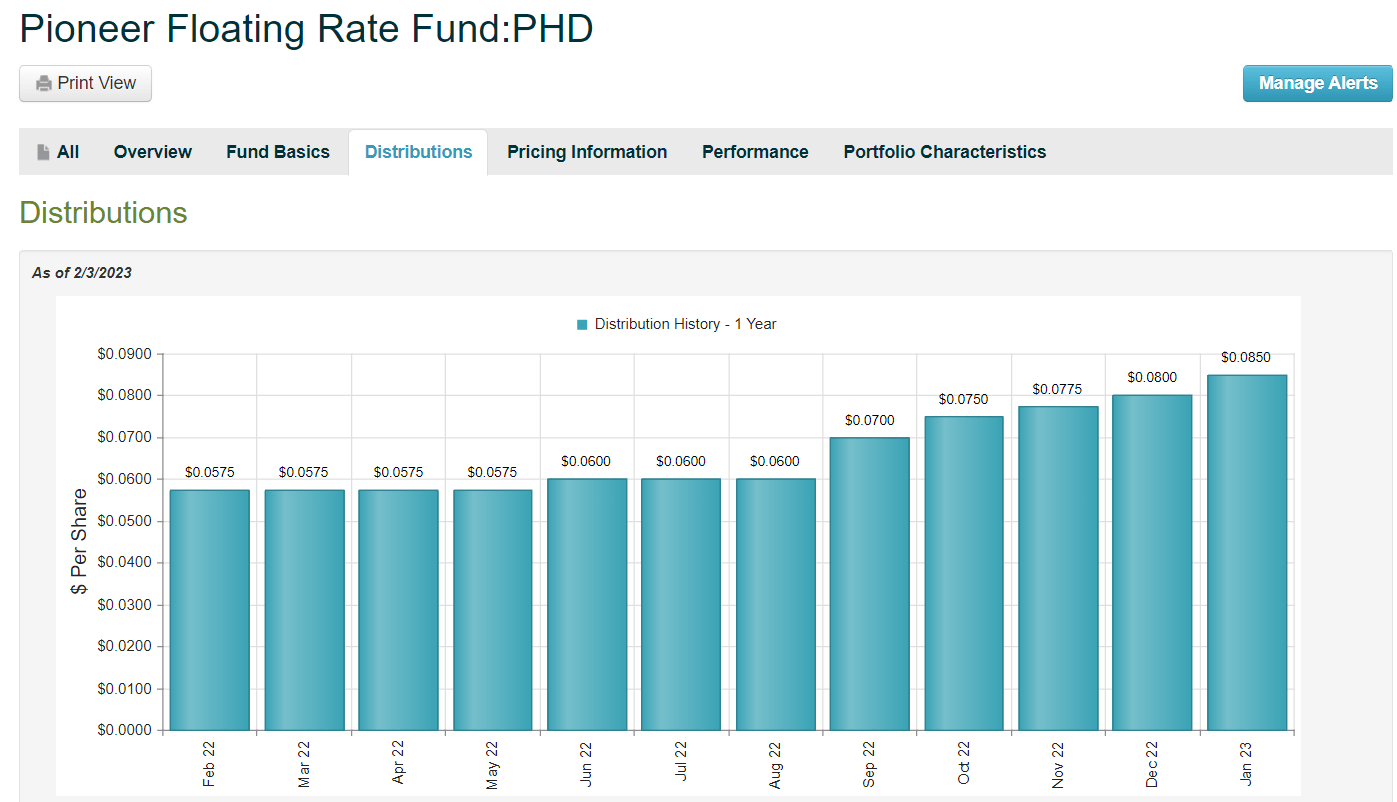

PHD

Without further ado, let’s get started. First up is Pioneer Floating Rate Trust ( PHD ). Not only is it a great ticker symbol (as my daughter is working toward her PhD in Neuroscience), but it also offers a forward yield of more than 11% based on the recently raised distribution of $0.0875, the 6 th increase in the past year. I recently covered PHD in some detail back in December, so I will leave it to you to read that article for more coverage of this fund than I will offer here. The key to this fund is the fact that it is a floating rate fund so it actually benefits from rising interest rates as the fund can rotate into higher yielding loans as older loans mature and get paid off, further increasing the income it generates. PHD currently trades at a discount of -10.6% as of 2/3/23.

I will include a chart of the distribution history for this fund (using CEFconnect) as well as each of the others that I will mention in this writeup.

{kind=link}

AIF

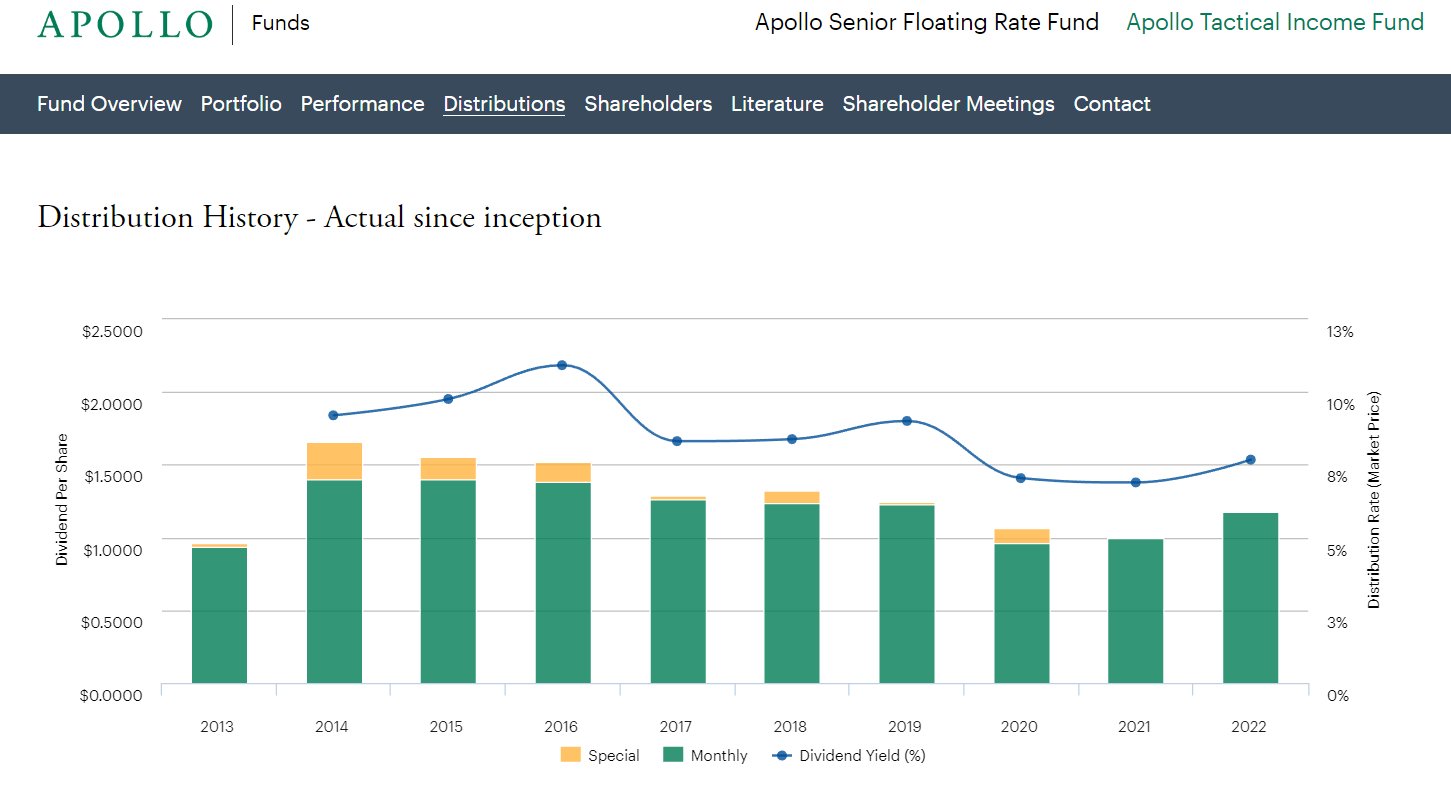

The next fund is one of two from Apollo ( APO ) that offers a high yield monthly distribution and trades at a discount to NAV. The Apollo Tactical Income fund ( AIF ) has raised the distribution 5 times over the past year. It currently trades at a discount to NAV of -9% and offers a forward annual yield exceeding 11% based on the latest monthly distribution of $0.1220.

The Fund’s primary investment objective is to seek current income with a secondary objective of preservation of capital by investing in a portfolio of senior loans, corporate bonds and other credit instruments of varying maturities. The Fund seeks to generate current income and preservation of capital primarily by allocating assets among different types of credit instruments based on absolute and relative value considerations. Under normal market conditions, the Fund invests at least 80% of its managed assets (which includes leverage) in credit instruments and investments with similar economic characteristics.

Looking at the past performance of AIF may give total return investors an uneasy feeling as the NAV has appeared to decline since inception. However, looking at the fund’s history of distributions since its inception in 2013 shows a steady high yield income stream with special dividends offered in every year except 2021 and 2022. This trend of a steady high yield monthly income stream continues into 2023. Meanwhile, the NAV tends to fluctuate over time based on what is happening in the Leveraged Loan markets.

{kind=link}

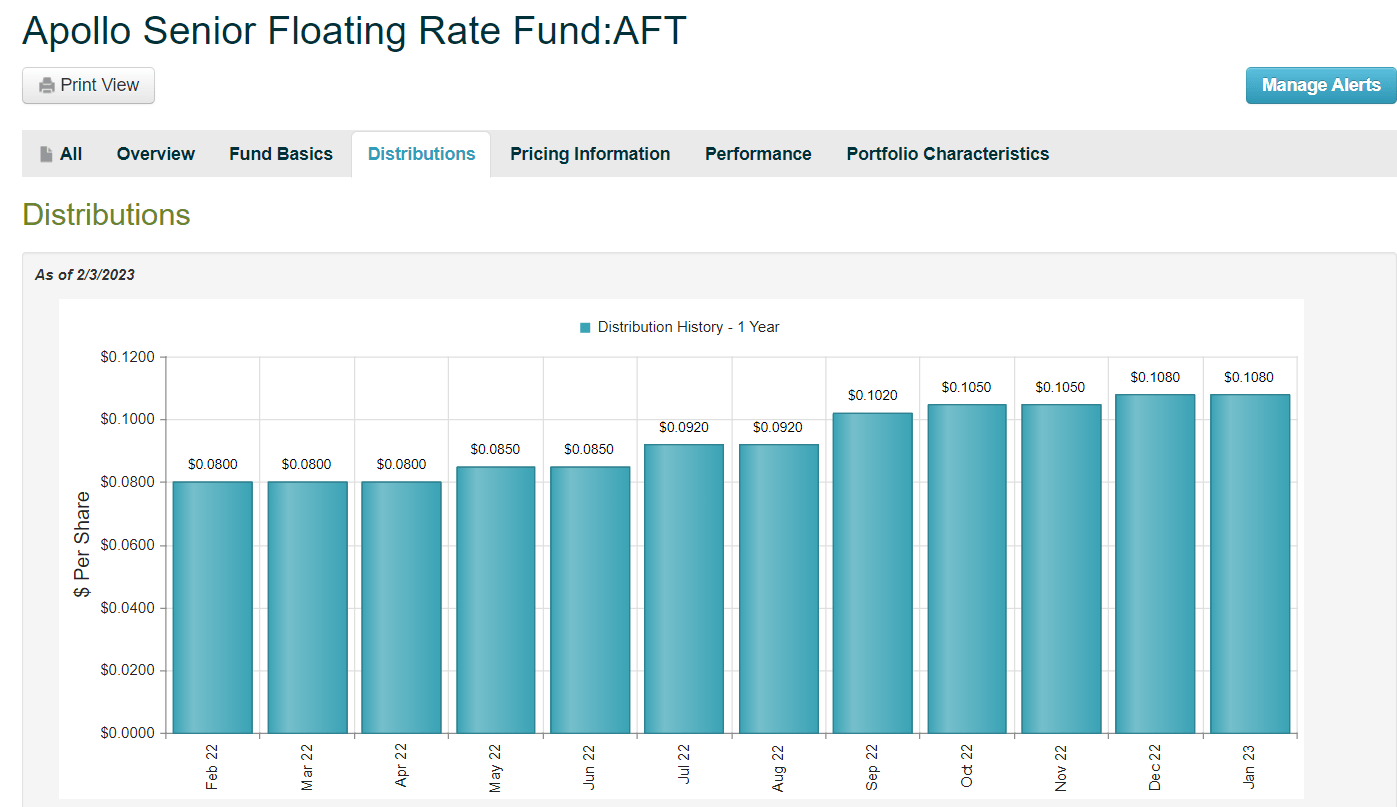

The other high yield income fund from Apollo that I do not currently own is Apollo Senior Floating Rate fund ( AFT ). That fund has also raised the distribution 5 times over the past year, offers a monthly distribution of $0.1080 yielding 9.77% and trades at a discount of -10.6%. It is also a floating rate fund and therefore also benefits from rising interest rates and should also be considered a strong candidate for current income and potential capital appreciation in 2023. Fellow SA contributor Nick Ackerman recently covered AFT if you are interested in reading his thoughts.

{kind=link}

JFR

The Nuveen family of funds include four that are proposed to be merged. On January 19, 2023, Nuveen issued this press release :

The Boards of Trustees of Nuveen Senior Income Fund (NYSE: NSL), Nuveen Floating Rate Income Opportunity Fund (NYSE: JRO), Nuveen Short Duration Credit Opportunities Fund (NYSE: JSD), and Nuveen Floating Rate Income Fund (NSYE: JFR) have approved a proposal to merge the funds. The proposed mergers, if approved by shareholders, would combine each of NSL, JRO, and JSD into JFR. The mergers are intended to create a larger fund with lower net operating expenses, enhanced earnings potential, and increased trading volume on the exchange for common shares.

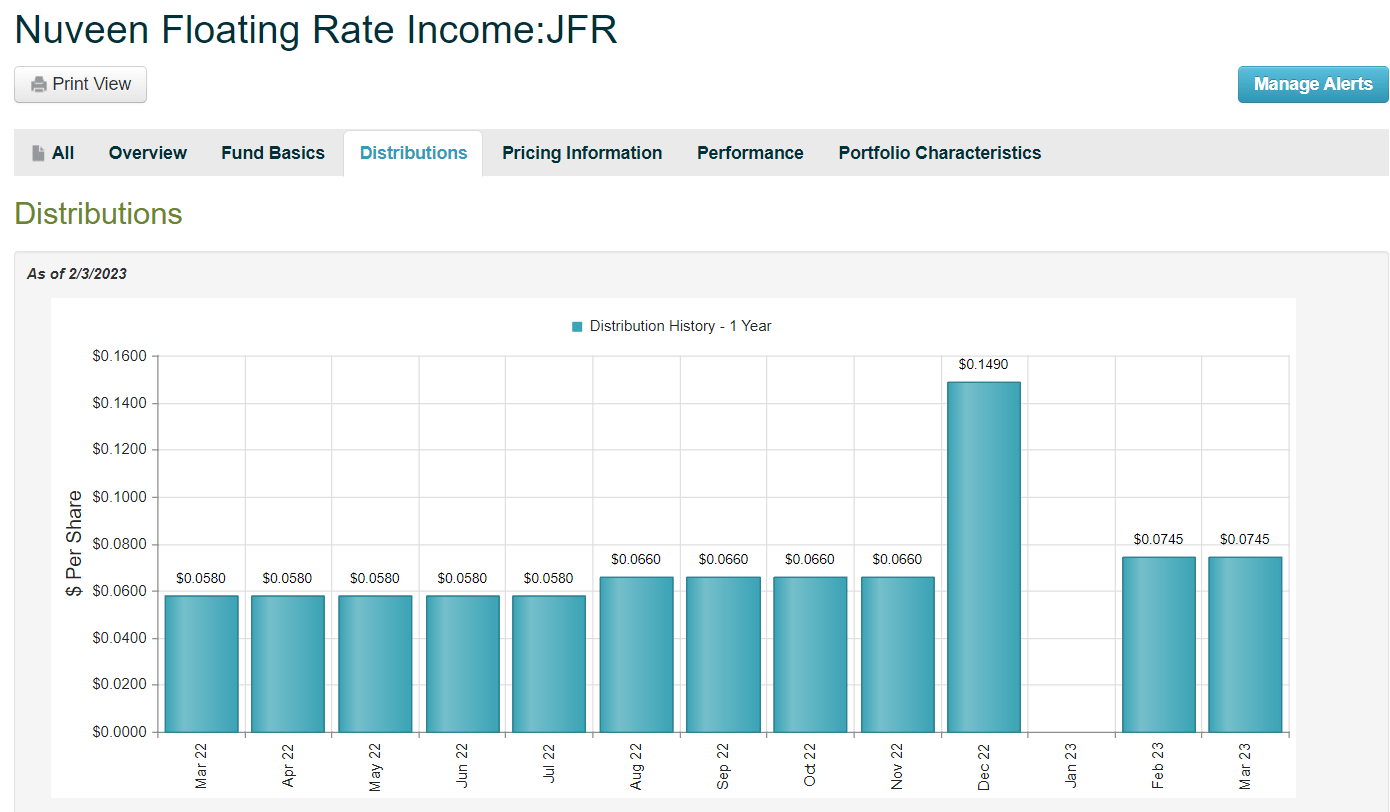

Of those four, I previously held JRO and covered the floating rate income fund in December. But now I will discuss JFR, another floating rate fund that will emerge as the combined fund if the merger is approved by shareholders. Like the other fixed income funds that I discussed previously, JFR has also raised the distribution multiple times in the past year. The dividend history shows a double dividend in December because the payable dates were the 1 st and the 30 th of that month.

{kind=link}

The JFR fund attempts to achieve a high level of income by investing in a portfolio of adjustable rate senior loans and other debt instruments. According to the fund website :

At least 80% of its managed assets will consist of adjustable rate loans; at least 65% of these must be senior loans secured by specific collateral. Other loans may include unsecured senior loans and secured and unsecured subordinated loans.

The current forward distribution rate is 10.37% and it trades at an -8% discount to NAV as of 2/3/23. The fund’s inception was in 2004 at an inception market price of $15. The fund has paid out total cumulative distributions of $15.1693 since then. The fund holds 480 individual holdings as of 12/31/22 with an average leverage-adjusted effective duration of 0.64 years. Roughly 82% of the holdings are senior loans, 13% corporate bonds, and the remainder in various other investments including 2.8% common stocks.

VVR

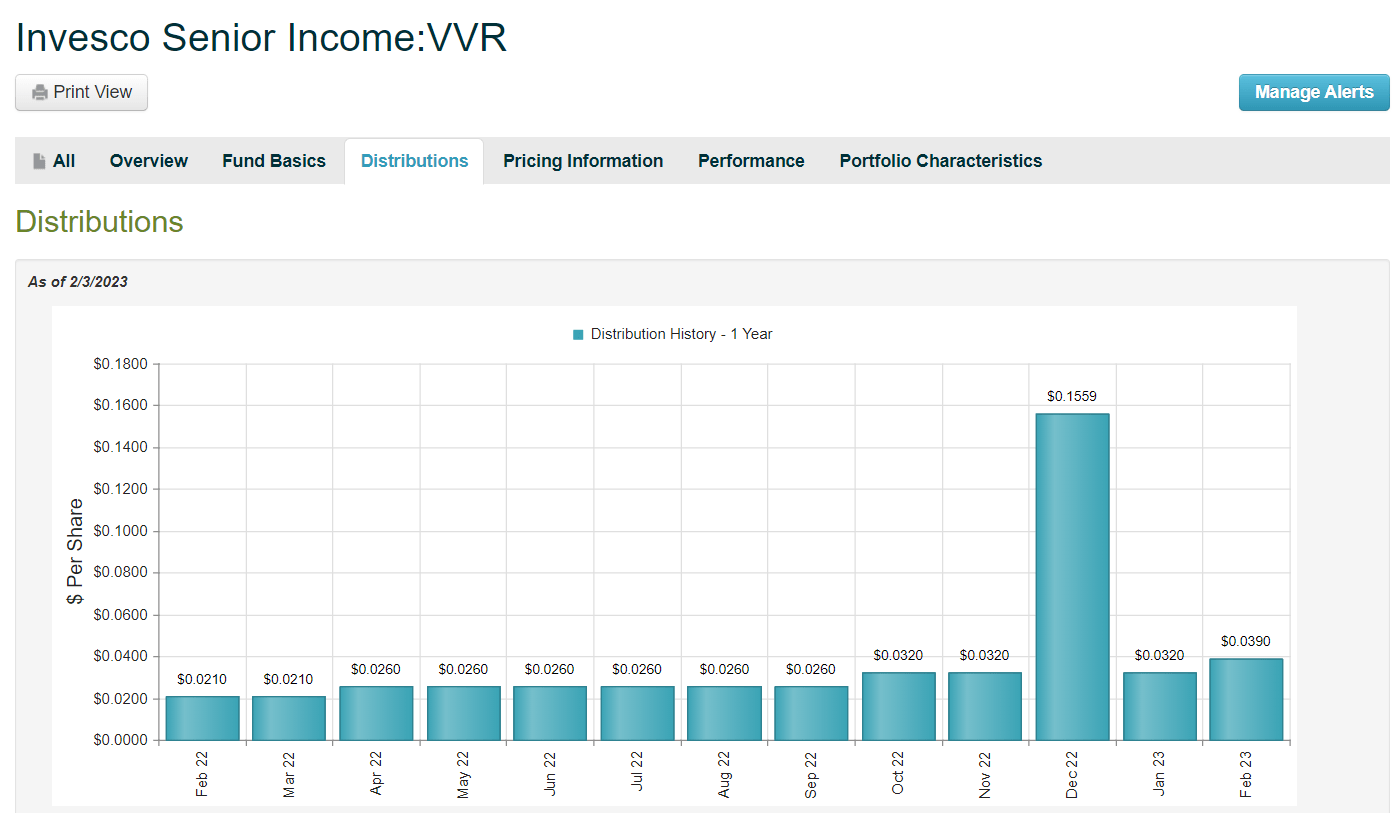

The final fund in the list today includes another fixed income fund that has raised the regular monthly distribution 3 times in the past year and also paid a special dividend at the end of 2022. The Invesco Senior Income trust ( VVR ) holds senior loans and corporate bonds and attempts to achieve a high level of current income consistent with capital preservation. In January the fund announced an increase in the regular monthly distribution of nearly 22% above the previous month. The distribution of $0.039 per share was increased from $0.032 in December and now offers a forward annual yield of 12% at the market price of $3.88 as of 2/3/23.

A recent article from SA contributor Power Hedge discusses the VVR fund in some detail, and he agrees with me that there is a lot to like in this fund.

{kind=link}

Like several of the other funds I mentioned above, most of the loans that VVR holds are floating rate and therefore also benefit from rising rates. The fund has been in existence since 1998 and currently trades at about a -6% discount.

Concluding Remarks

There are generally only two reasons for a closed end fund to increase the amount of the distribution it pays out each month or each quarter, depending on the fund. Those CEFs that offer a variable distribution rate, typically based on some percentage of the calculated NAV each month, may pay a higher distribution than the previous month if the NAV increased, or a lower distribution if it decreased. But in the case of those CEFs that pay regular monthly (or quarterly) distributions, a raise probably indicates that the fund managers believe that the increased distribution can be maintained for the foreseeable future, and that is typically based on some other measure of distributable income such as NII (net investment income). Some equity funds use a managed distribution policy because the value of the underlying stocks is easier to determine than the mark to market value of fixed income investments, which are typically more stable from month to month.

An assumption that may be incorrect when evaluating the past performance and future potential of a CEF that specializes in providing current income from debt backed securities is that the NAV of the fund is indicative of the health of the fund. That is not always the case as can be evidenced from my review of the funds described above, which have seen the NAV fall throughout 2022 while raising the monthly distribution multiple times. Part of the reason for that is because the NAV is often calculated based on the mark to market value of the underlying loans in the fund’s portfolio, as explained by Pitchbook :

Beginning in 2000 the SEC directed bank loan mutual fund managers to use available price data (bid/ask levels reported by dealer desks and compiled by mark-to-market services), rather than fair value (estimates based on whether the loan is likely to repay lenders in whole or part), to determine the value of broadly syndicated loan portfolios.

In addition, most of the funds that I reviewed in this article invest primarily in floating rate debt instruments such as senior secured loans, which offer:

- Attractive yields with very low duration, providing cost-effective, inflation-hedged income.

- Senior secured position in the capital stack for durable income generation with lower volatility than other high yielding fixed income.

- Favorable credit spreads in an improving economy such as what we are seeing thus far in 2023.

In summary, I encourage income-oriented investors to take a closer look at the fixed income funds that have been regularly increasing the monthly distributions and ignore the fluctuations in NAV. As the economy begins to recover from the horrible, awful, disappointing year for bond funds in 2022, opportunities abound for investors to take advantage of the low prices and high yields to generate future income streams for retirement, or whatever purpose one may have in mind.

For further details see:

The Best Distribution Is The One That Was Just Raised