KMLM - The Best Way To Invest $1 Million And Earn $53000 In Annual Dividends

2023-10-14 07:30:00 ET

Summary

- Good retirement planning must plan for you or your spouse to live to 100 (15% probability).

- A safe withdrawal rate for retirement is usually around 50% of the expected long-term return of your portfolio.

- For the standard 60/40, that's about 3% to 4%. But in this article, I show how to safely get a 6.1% withdrawal rate from a 5.3% yielding portfolio.

- An allocation of 67% Schwab U.S. Dividend Equity ETF™ and 33% KFA Mount Lucas Index Strategy ETF is the safest way to earn a 5.3% safe yield today, with zero stock-picking for retirees with no interest in tracking companies.

- The portfolio is expected to deliver 12% returns in the future compared to 10% to 11% historical returns, and our calculation is that this is 99.56% likely to beat a 60/40 over 50 years and 80% likely to beat S&P 500 returns. Its historical declines in bear market are 50% smaller than the S&P, and its almost 100,000X less likely to fall 30% in any given year.

One of my best friends recently asked me a very interesting question.

My father has $1,000,000 in fidelity and is 55. My mom gets $1800 SS and will draw in 5 years @ $2000. He wants to figure out the best plan to enjoy life but deplete over the next 20 years slowly- he said after that, the quality of life goes down anyway. Has a home paid off for 300k and a vacation home for 200k with no debt. Thought for best fidelity approach?" - Adam S.

I told him a few of my thoughts (while on a walk with a puppy) to take to a fiduciary-certified financial planner, which Fidelity has a lot of.

So my first thought is your father's plan to run out of money at 75 seems rather risky. Because it sounds like he wants to have that million dollars invested in working for him while he's drawing it down.

The drawdown rate to get rid of it at 6%. I don't have a calculator with me and I'm on a walk right now. But I know that it's above 5% because 100% / 20 is 5% per year. But even a 60/40 does 7% overtime.

So in order to deplete your savings you have to go above 7%. You're looking at between 8 and 10% annual withdrawals. Meaning that at the very minimum in year one he'd be pulling $80,000 out of this account. And with your mom looking at around $20,000 in income You're talking $100,000 per year for about 20 years.

That is indeed a really good lifestyle depending on where you live. However while quality of life can decrease over time it's not necessarily true and if you get hit with some kind of illness that requires a nursing home those can cost about $85,000 a year. So I would certainly recommend talking with a fiduciary certified financial planner I'm sure Fidelity has plenty, And I'm sure they would say the same thing You do not want to plan to run out of money at 75 unless you're eating three steaks a day and plan to drop dead at 75.

About 6% of couples have someone make it to 100. So the 30-year time frame for retirement the reason that that's so important is because the 4% rule is designed that you don't actually run out of money after 30 years. In fact most of the time in the last century you would have gotten richer after 30 years.

And the reason that is so valuable is that money is a safety net. Imagine if at 74 your father is struck by something say dementia and he needs round the clock care and it's 100,000 a year. Well Medicaid will not help at all unless you are literally below the poverty line Your father would have to get rid of all of his assets and essentially penniless. At which point Medicaid would pay. But Medicare won't at all. Now I can't legally provide personalized investment advice, SEC has firm rules about that.

But if you just looking for a very simple retirement portfolio that is essentially risk-free meaning over the long term you cannot lose all your money, SCHD for high yield dividend growth stocks that historically do 13% are expected to do 13% in the long term, and KMLM the Warren Buffett of managed futures as a hedge.

KMLM historically the index that it tracks has done about eight and a half percent per year and it pays out all annual profits as a annual dividend. SCHD if you were 66% allocation and 33% KMLM. You get a very smooth ride basically in the Great recession you fell half as much as the market at the scariest time in March of 2009. In terms of yield You looking at around a 5.3% yield and long-term returns expected to be between 11% and 12% per year." - my response (dictated on my phone via Facebook).

Crunching The Retirement Planning Math

Now that I have more time and access to my tools and computer, let's get the specifics from my mental math during my walk.

According to: "Helping consumers and providers manage defined contribution ((DC)) wealth in retirement" by Dr Paul Cox, Department of Accounting and Finance, Birmingham Business School, University of Birmingham...

{kind=link}

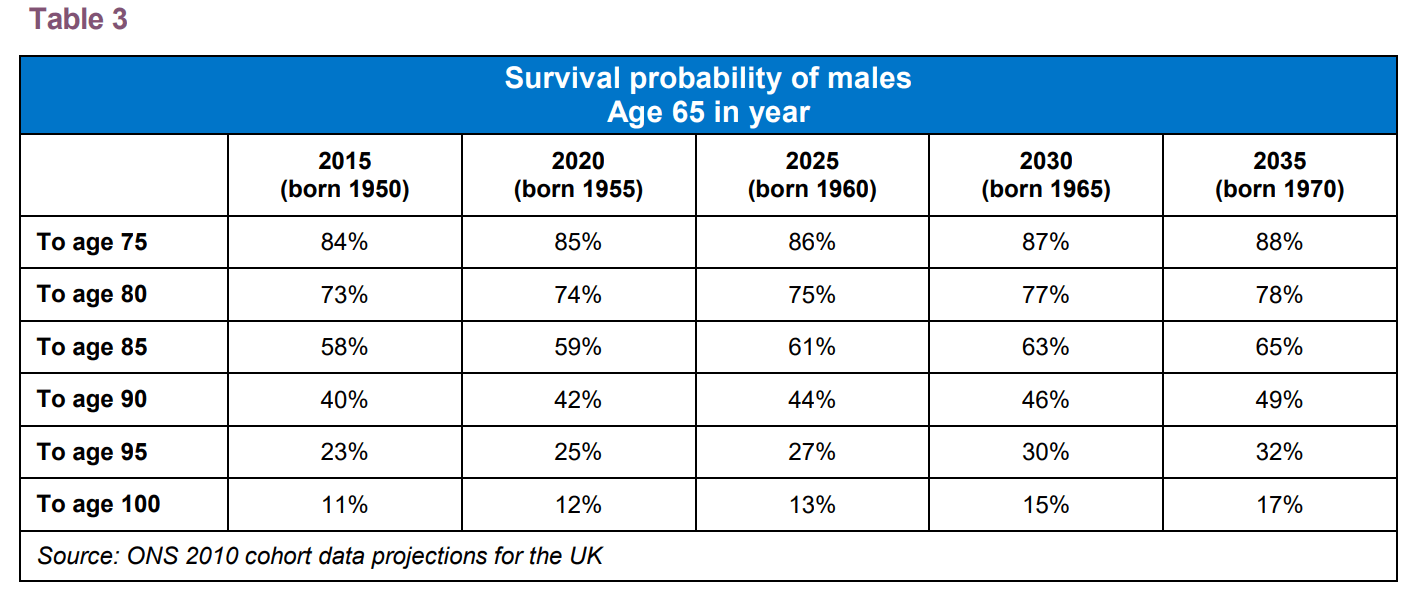

If you're 65 today and ready to retire, your chances of living to beyond 75 if you're a male (UK and American men are assumed to have similar life spans) is 84%.

Using 50+ as your base case, you need to assume you'll live to at least 85, and there is a very good chance, 40%, that you'll live to 90.

And let's not forget your spouse.

{kind=link}

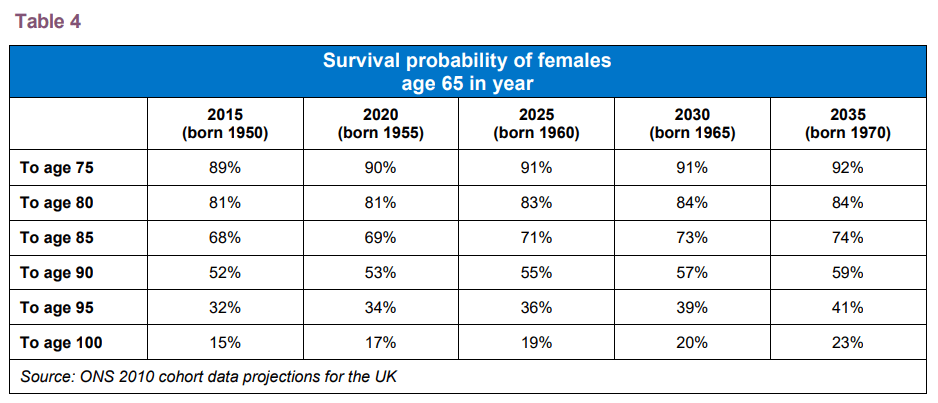

If a woman is alive at 65, she has a coin flip's chance to live to 90 and a 15% chance of making it to 100.

{kind=link}

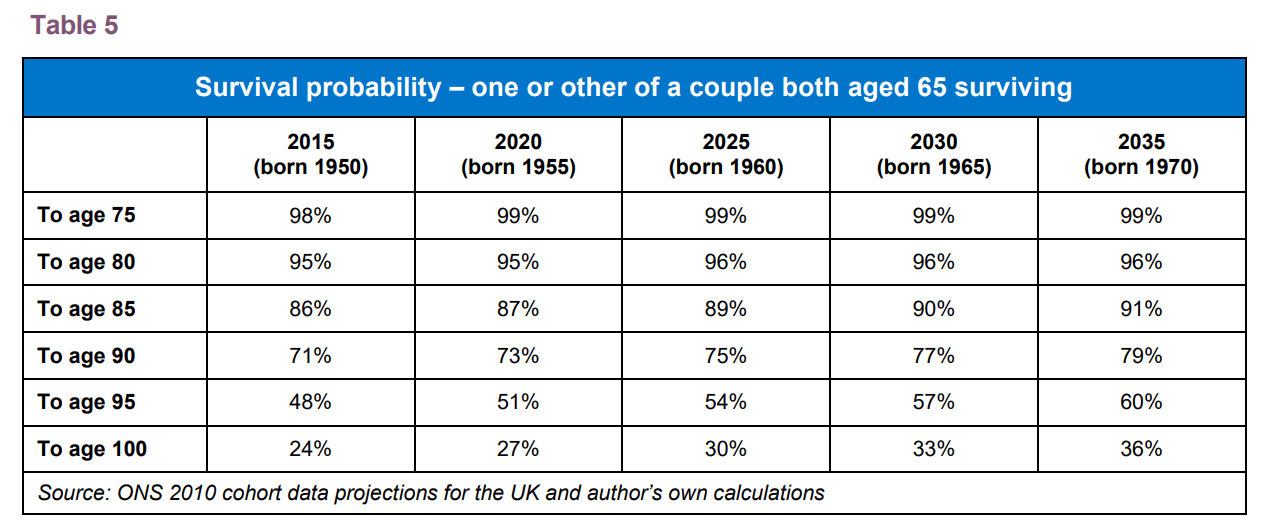

According to this research, the probability of a couple at 65 today serving past 75 is 98%.

The probability of one of them making it to 95 is a coin flip, and a 24% chance of someone surviving to 100.

A $2,000 inflation-adjusted Social Security check will hardly lead to a dignified life for a surviving spouse (statistically the widow).

What Is A Safe Withdrawal Rate?

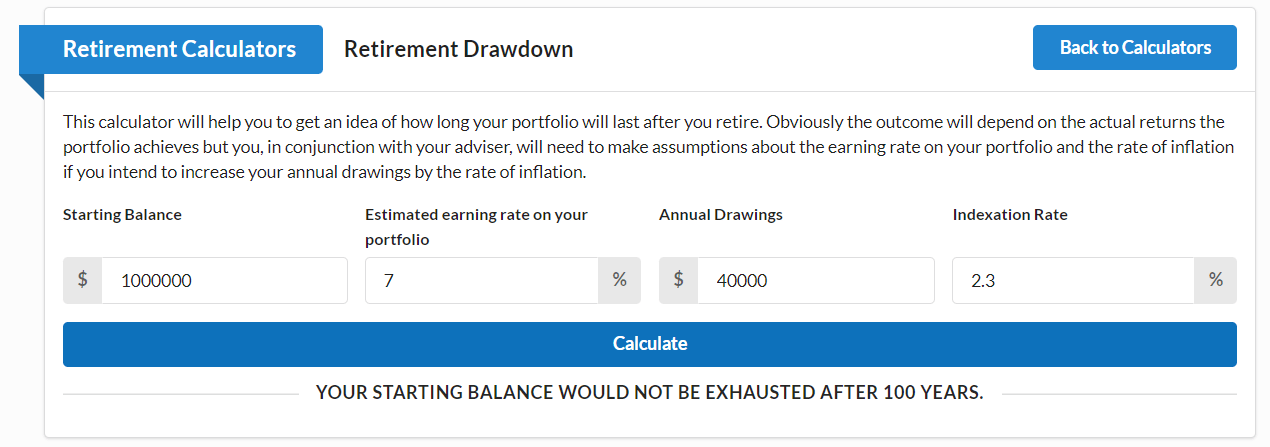

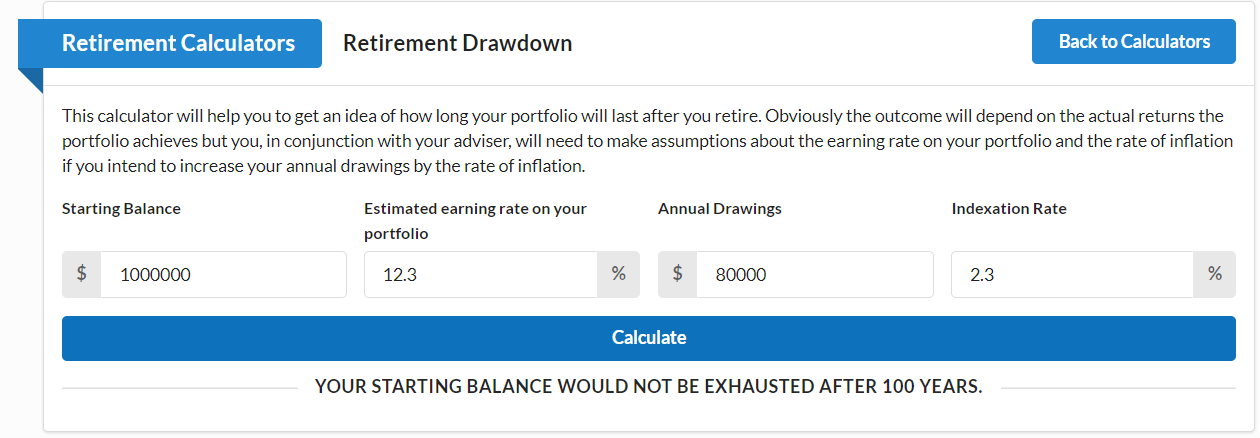

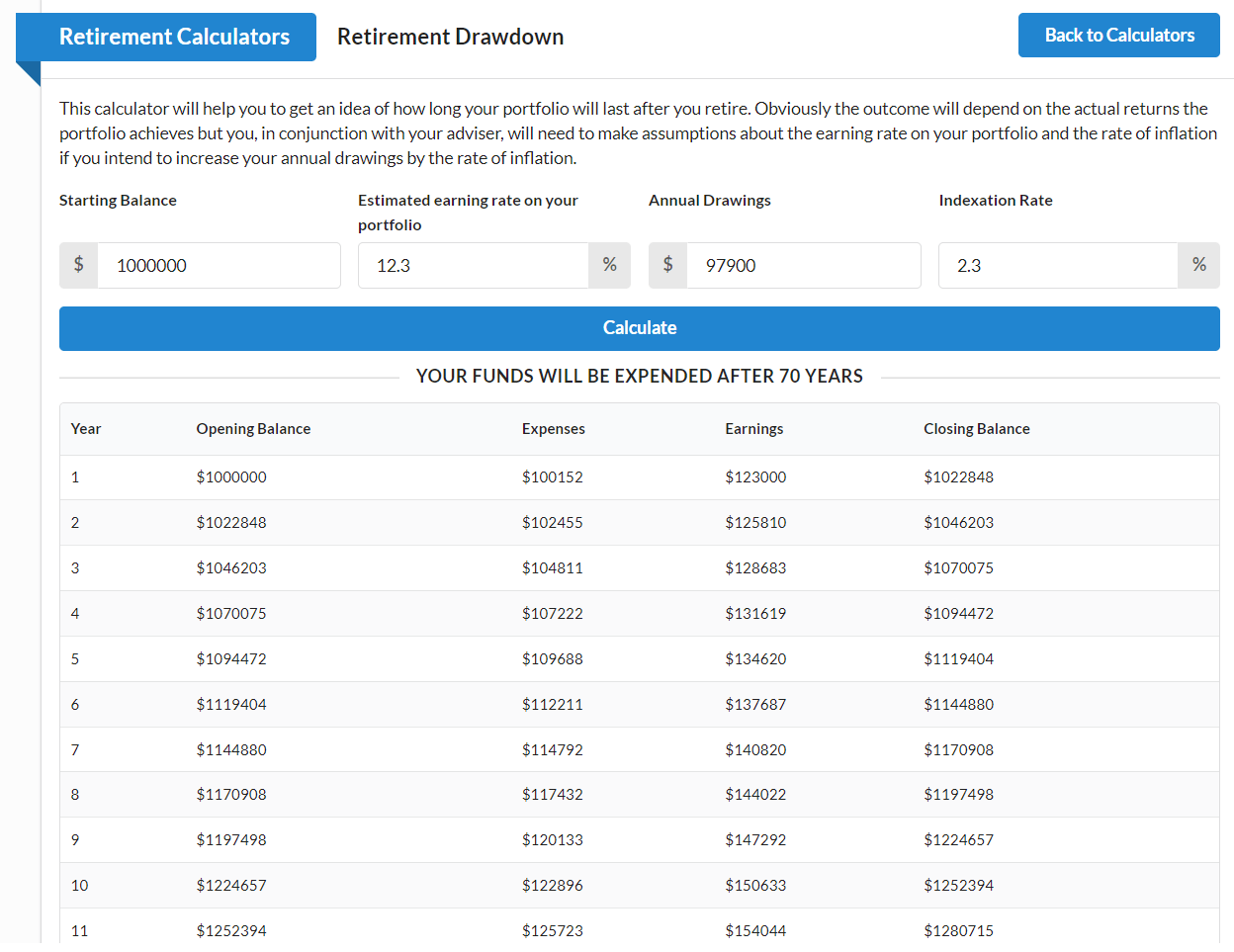

Here is a useful free calculator for estimating withdrawal rates, and portfolio drawdowns in retirement.

{kind=link}

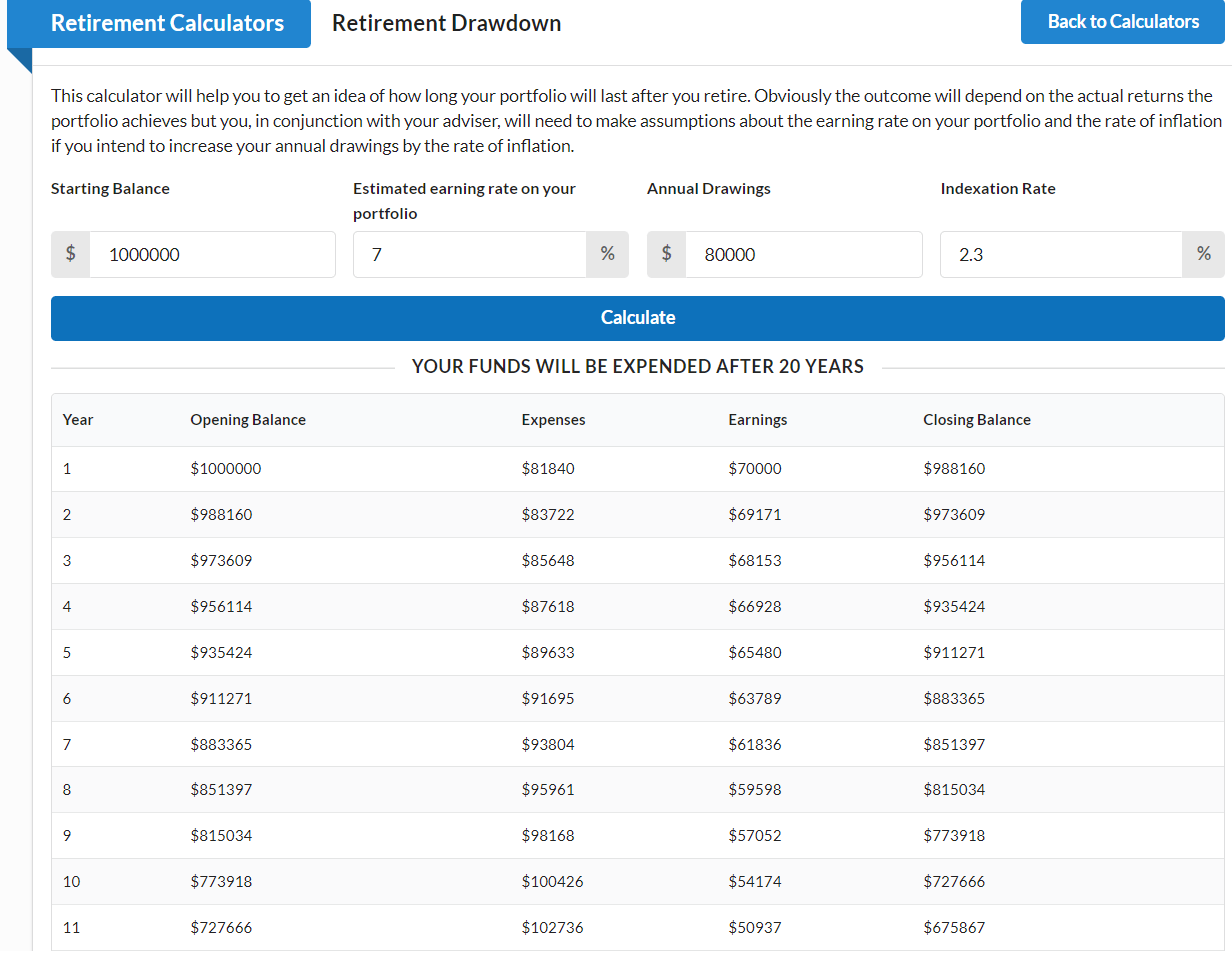

Suppose we use the bond market's 2.3% long-term inflation estimate for indexing our withdrawals and starting with the classic 4% rule and 7% historical and consensus future 60/40 retirement portfolio return. In that case, we can see that statistically speaking, a person starting with $1 million is likely to never run out of money.

{kind=link}

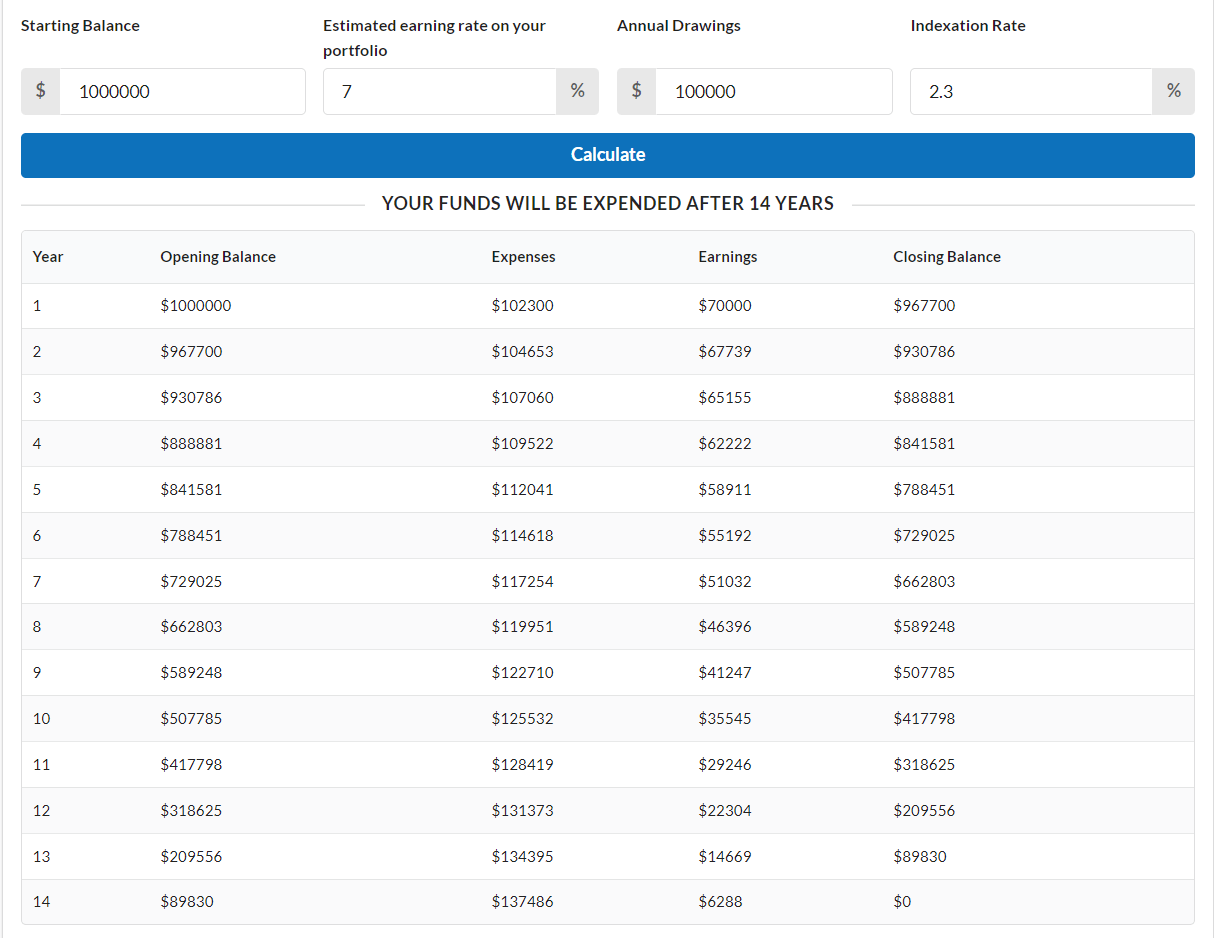

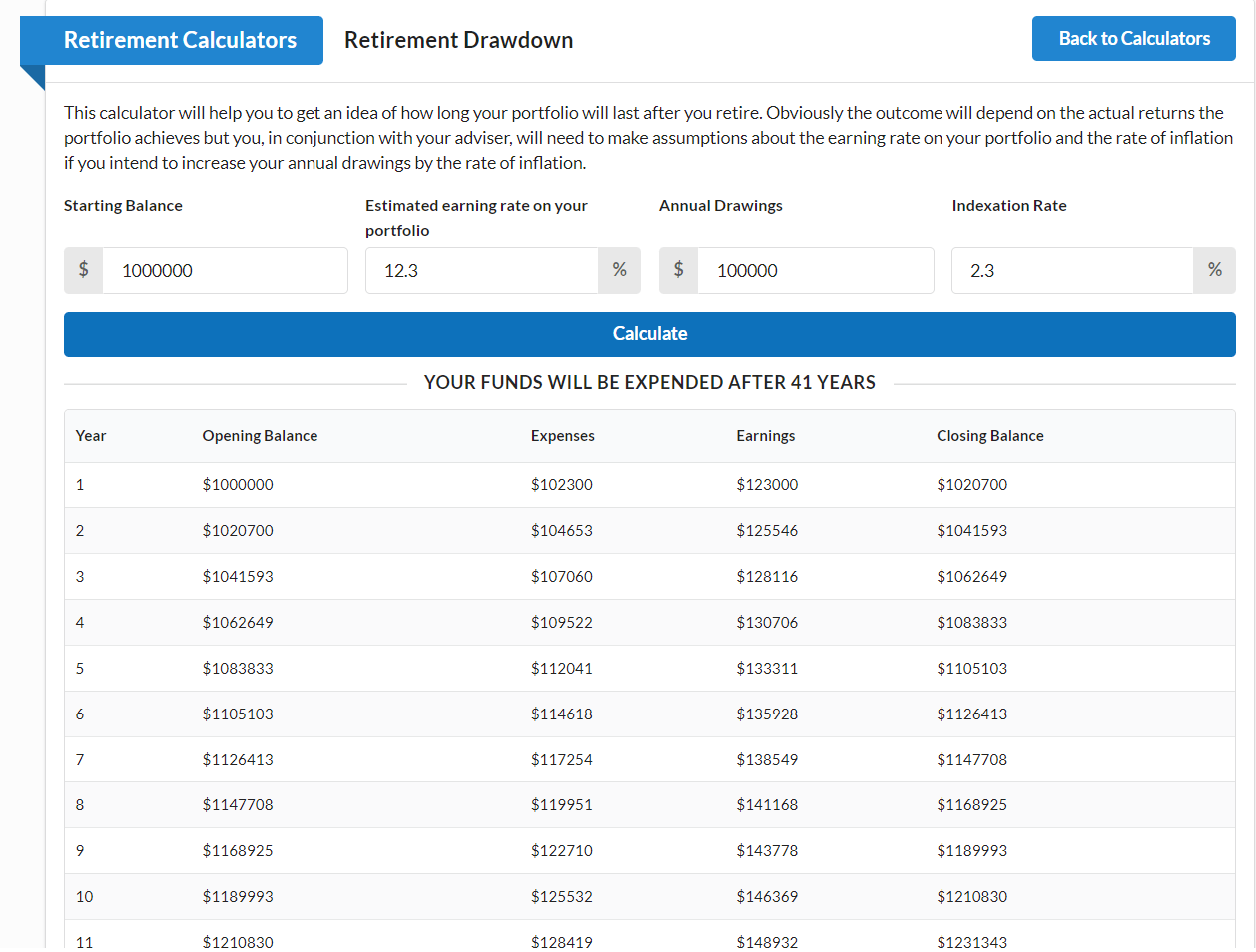

At a 10% withdrawal rate, you statistically run out of money after 14 years if you're invested in a 60/40.

{kind=link}

8% is the withdrawal rate to run out of money using a 60/40 assumption.

The Power Of High-Yield Dividend Investing

| Stock |

| Yield |

| Growth |

| Total Return |

| Weighting |

| Weighted Yield |

| Weighted Growth |

| Weighted Return |

| (SCHD) |

| 3.7% |

| 10.5% |

| 14.2% |

| 66.67% |

| 2.5% |

| 7.0% |

| 9.5% |

| (KMLM) |

| 8.5% |

| 0.0% |

| 8.5% |

| 33.33% |

| 2.8% |

| 0.0% |

| 2.8% |

| Total |

| 3.1% |

| 13.8% |

| 16.9% |

| 100.00% |

| 5.3% |

| 7.0% |

| 12.3% |

(Source: DK Research Terminal.)

12.3% is almost double the return potential of a 60/40, and the yield is far superior.

| Metric |

| 60/40 |

| ZEUS |

| X Better Than 60/40 |

| Yield |

| 2.1% |

| 5.3% |

| 2.52 |

| Growth Consensus |

| 5.1% |

| 7.0% |

| 1.37 |

| LT Consensus Total Return Potential |

| 7.2% |

| 12.3% |

| 1.71 |

| Risk-Adjusted Expected Return |

| 5.0% |

| 8.6% |

| 1.71 |

| Conservative Time To Double (Years) |

| 26.0 |

| 11.4 |

| 2.29 |

(Source: FactSet, Morningstar.)

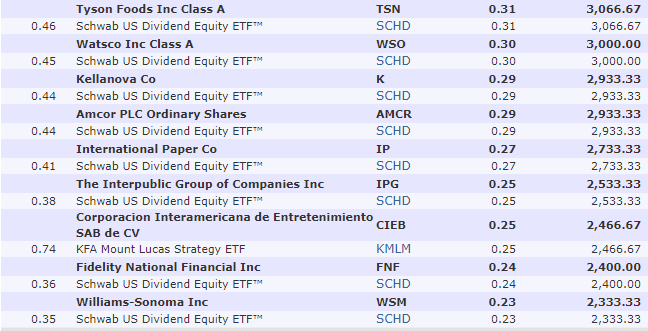

Portfolio Summary

Morningstar Morningstar Morningstar

{kind=link}

{kind=link}

{kind=link}

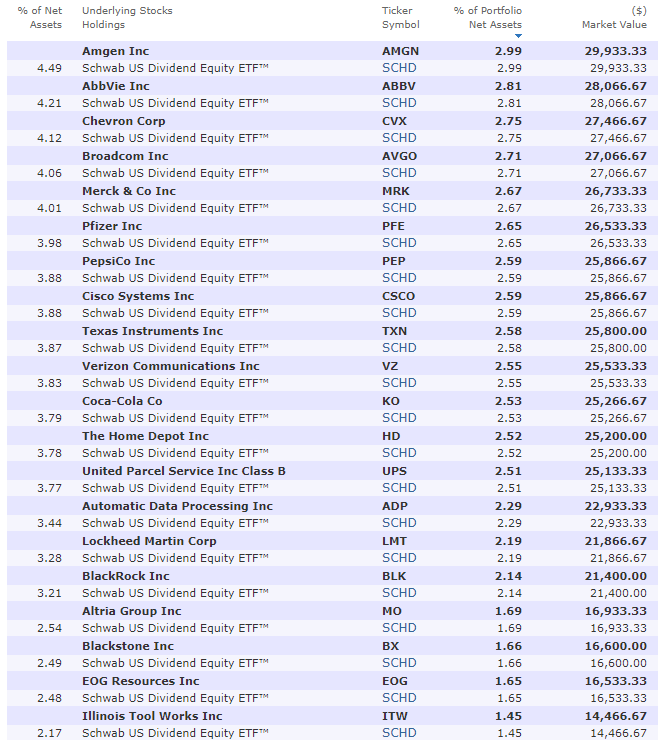

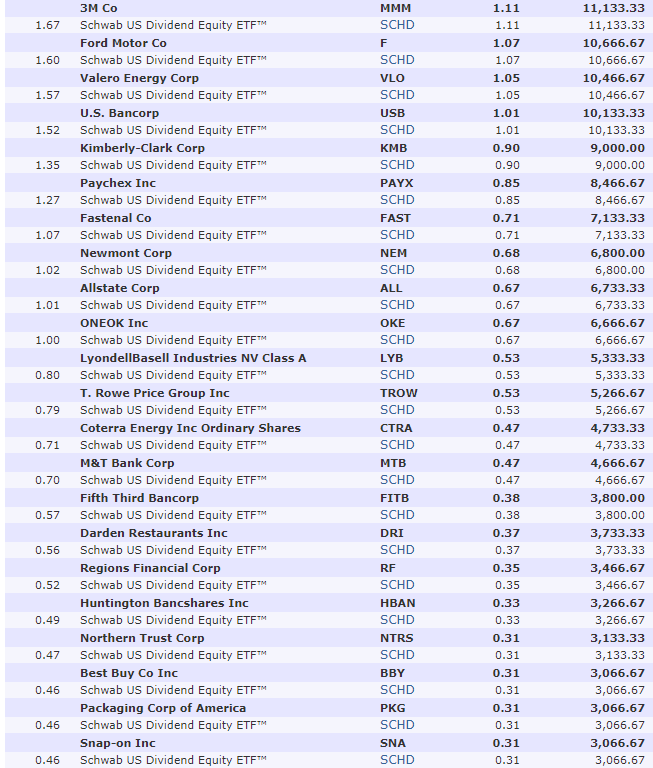

While a few of these companies I'd prefer not to own due to weak growth prospects (like K, TSN, and IP), this is an overall Ultra SWAN high-yield portfolio.

{kind=link}

This is a 54% value portfolio, as you'd expect from the ETF king of high-yield.

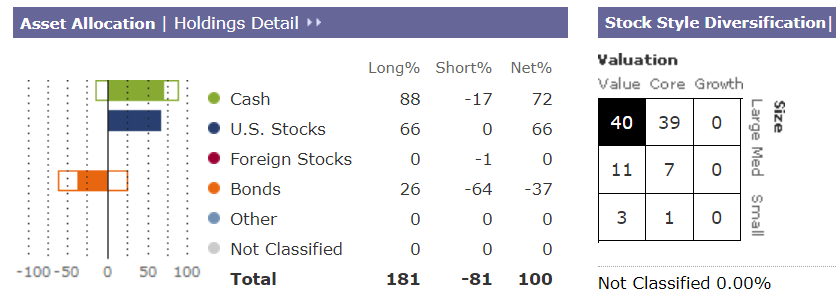

- KMLM is currently 37% short bonds.

Morningstar Morningstar Morningstar

The 60/40 is an 18X forward P/E, while ZEUS is under 14.

Withdrawal Rate Analysis

So, let's see what happens to that 8% withdrawal rate with this Schwab U.S. Dividend Equity ETF™ (SCHD)/ KFA Mount Lucas Index Strategy ETF (KMLM) ZEUS portfolio.

- ZEUS = Zen Extraordinary Ultra Sleep Well At Night portfolio

- based on 67% stocks/33% hedges (optimal asset allocation for the last 50 years, assuming you want to maximize negative inflation-adjusted total returns).

{kind=link}

An 8% withdrawal rate now results in a perpetual trust for a retired couple.

- 9% withdrawal rate also lasts over 100 years.

{kind=link}

With a 10% withdrawal rate, my friend's parents would likely make it to 96 (or his father would) before running out of money.

- 48% statistical chance one of them lives that long.

How about the 20-year withdrawal? 11.7% annual withdrawal rate.

- $117,000 per year to start and indexed to inflation

- $141,000 + his father's social security

- $165,000 total gross income, assuming the father gets the same SS.

But how about a conservative withdrawal rate? One designed to get them to 125, the longest that medical science believes humans can live to?

{kind=link}

Using this ZEUS portfolio, 67% SCHD and 33% KMLM, a 9.79% annual withdrawal rate appears to be statistically safe.

That's a highly generous retirement consisting of $97,900 per year in inflationary-adjusted income and $48,000 in Social Security.

- $145,900 per year inflation-adjusted income for life.

That's nearly 2X the median U.S. household income.

Deep Dives On SCHD and KMLM

- SCHD Vs. VIG: 3 Reasons One Is The Hands Down Better Buy

- Why I Have 22% Of My Life Savings Invested In Three 9+% Yielding ETFs (KMLM Deep Dive).

Let me explain why I consider SCHD + KMLM the safest high-yield way for someone with zero interest in stocks (like my friend's father) to invest 100% of his life savings.

First, there is no stock-picking risk. You're not buying any individual companies that might fail in the future.

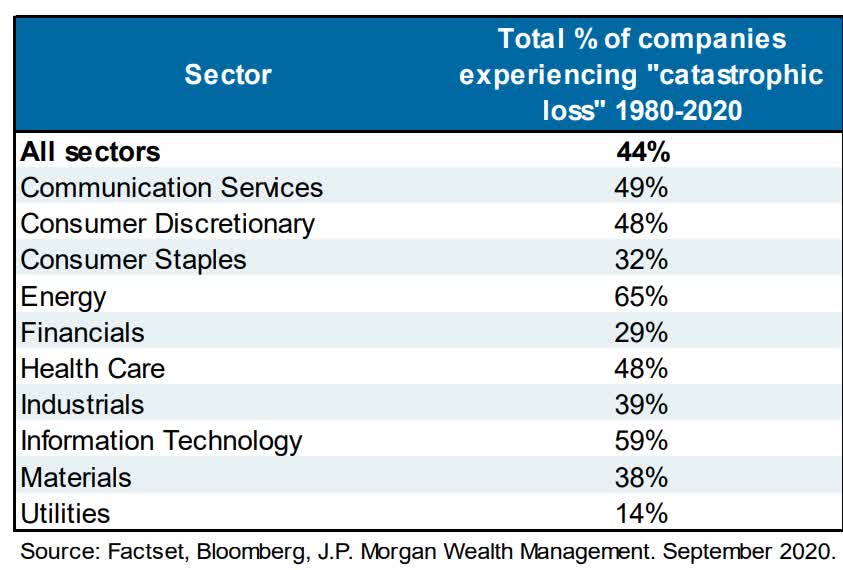

{kind=link}

44% of U.S. stocks fall 70+% or more and never recover. Ever.

If you don't like to track stocks? You need an exchange-traded fund, or ETF, to avoid the risk of permanent catastrophic declines.

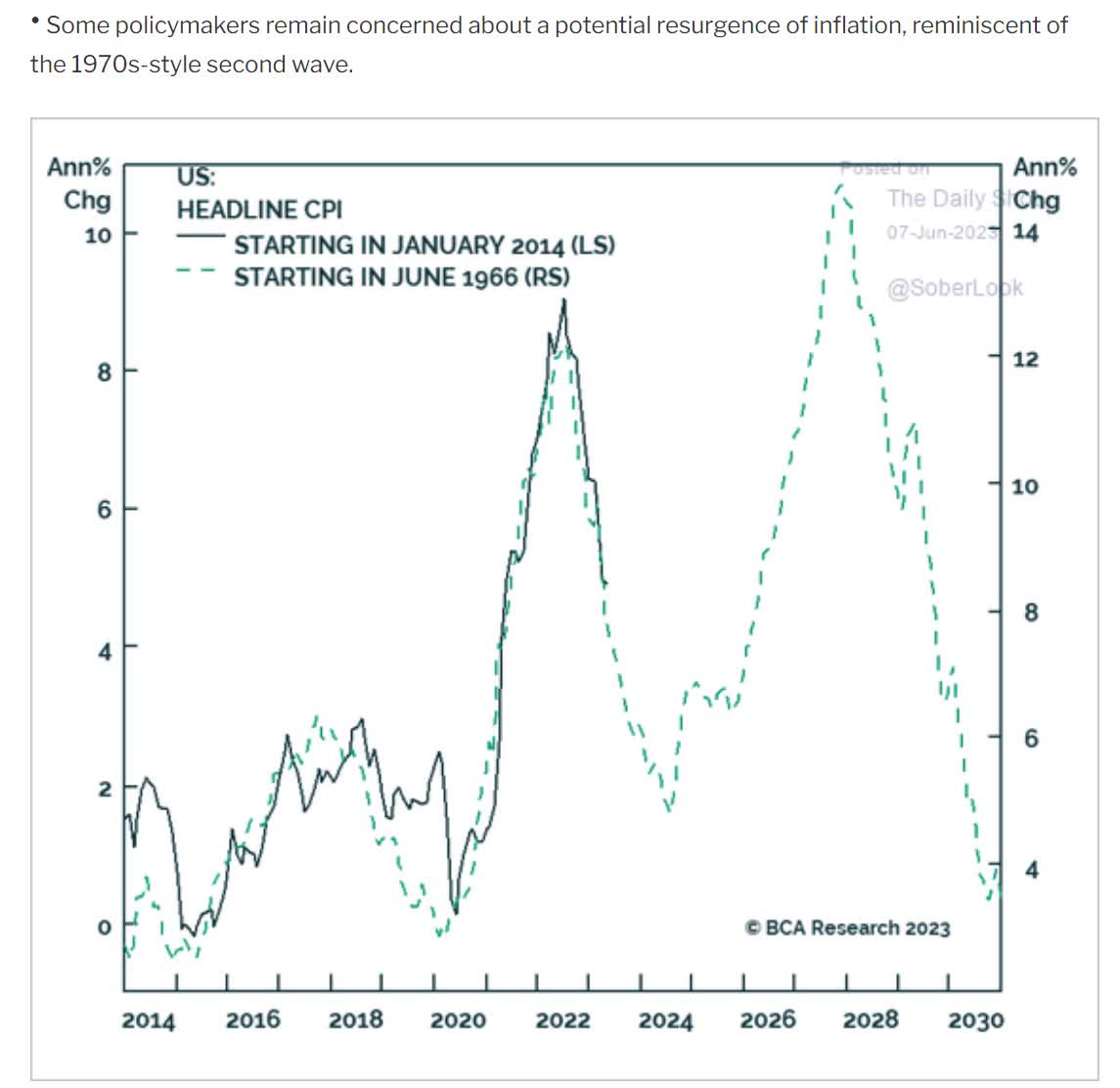

What about KMLM? Why not buy bonds and managed futures?

{kind=link}

If we get a 1970s style (and WWII) triple inflation spike scenario, then Jamie Dimon thinks the Fed is going to 7% and long-term interest rates could rise to 9% or even 10%.

- long bonds would fall 26% per 1% increase in 30-year yields

- 26% decline for 1% decline

- then another 26% for the 2nd 1%

- and so on

- 5% rise in rates from here = 78% decline from here

- if the 1970s were repeated? Then inflation of 11% leads to 13% to 14% 30-year yields

- 8% to 9% increase in yields from here

- 93% decline in value from here and 98% decline from record highs.

For myself and most investors with 30+ years? Bonds are risk-free even long bonds.

If you're using a short-term time horizon? Like 10 to 20 years? Then you have to plan for a worst-case stagflation hell scenario.

How Realistic Is That 12.3% Annual Return Forecast?

Let's tap into the power of Portfolio Visualizer's free Monte Carlo simulator to find out how realistic is that 12.3% consensus total return forecast.

After all, all of the investing is probabilistic. So, what does the range of potential outcomes look like?

75-Year Monte Carlo Simulation

- is applicable for anyone with a shorter time frame

- What is more likely? A 50% market crash in the next five years? Or sometime in the next 75?

- 75 years is the most extreme market scenario we're likely ever to see.

Portfolio Visualizer Premium Portfolio Visualizer Premium

{kind=link}

{kind=link}

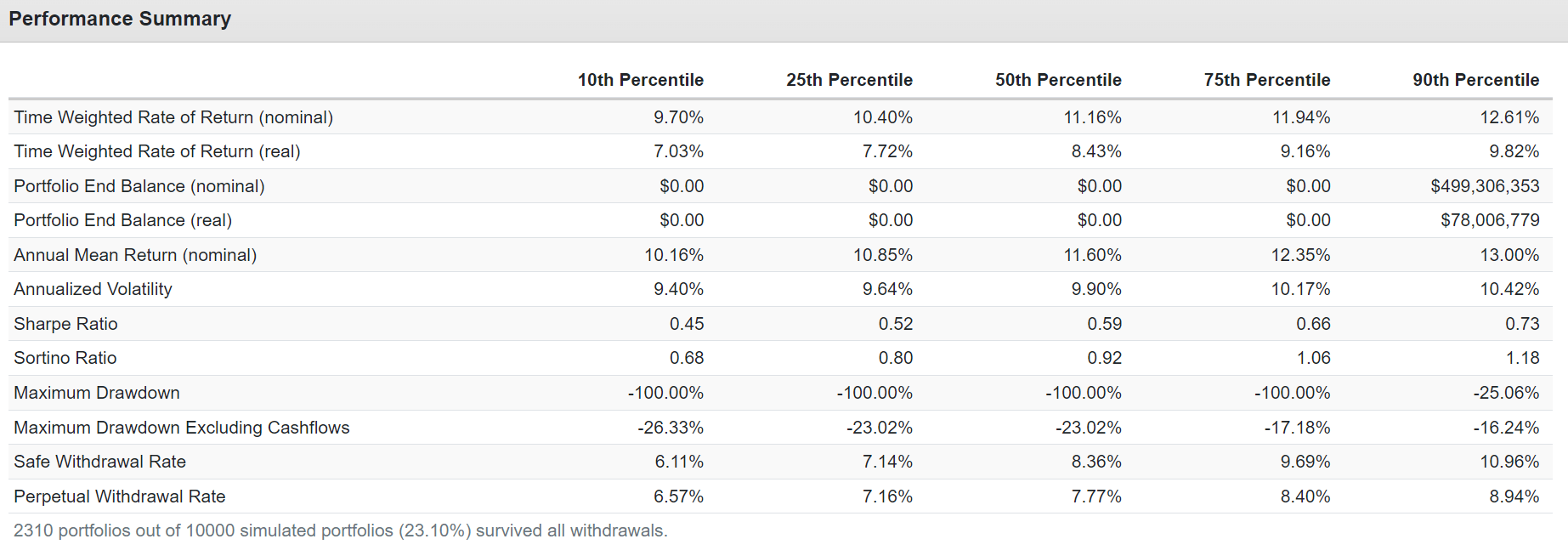

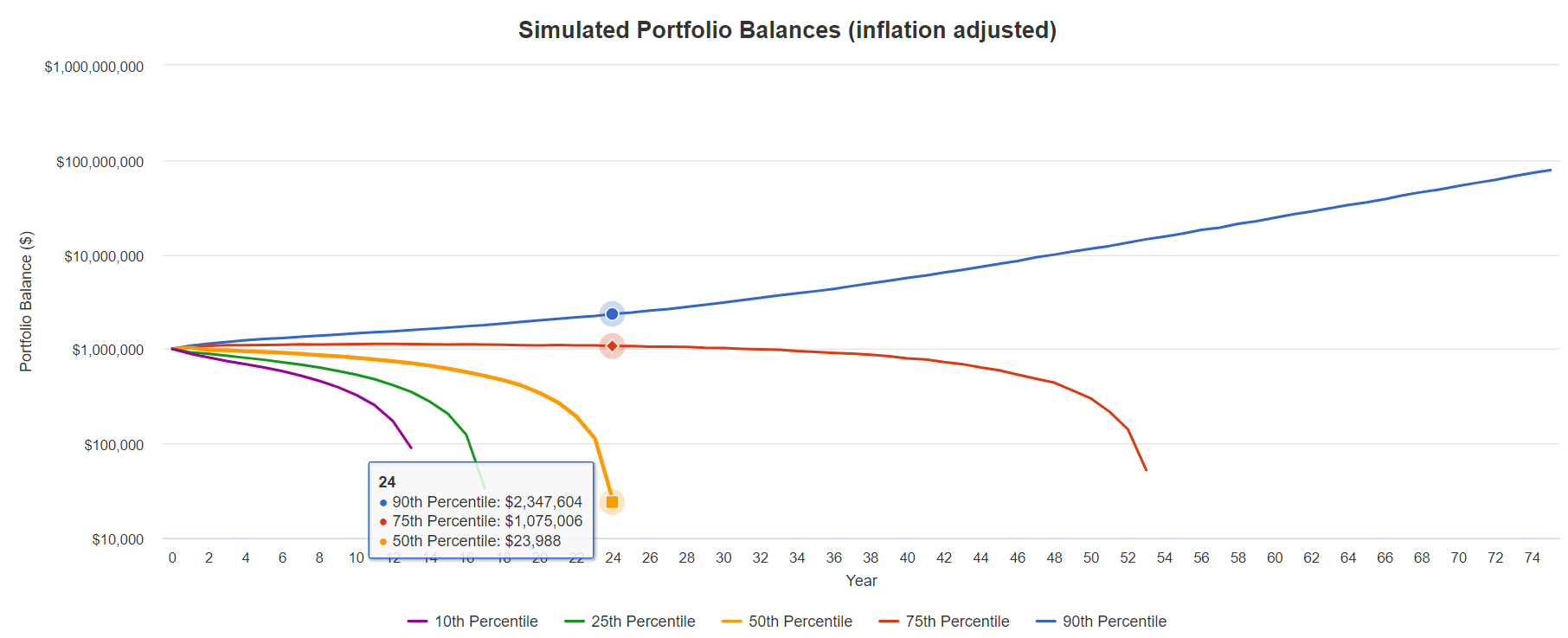

So, under the original 20-year withdrawal plan, this portfolio worked even with a 9.7% withdrawal rate.

{kind=link}

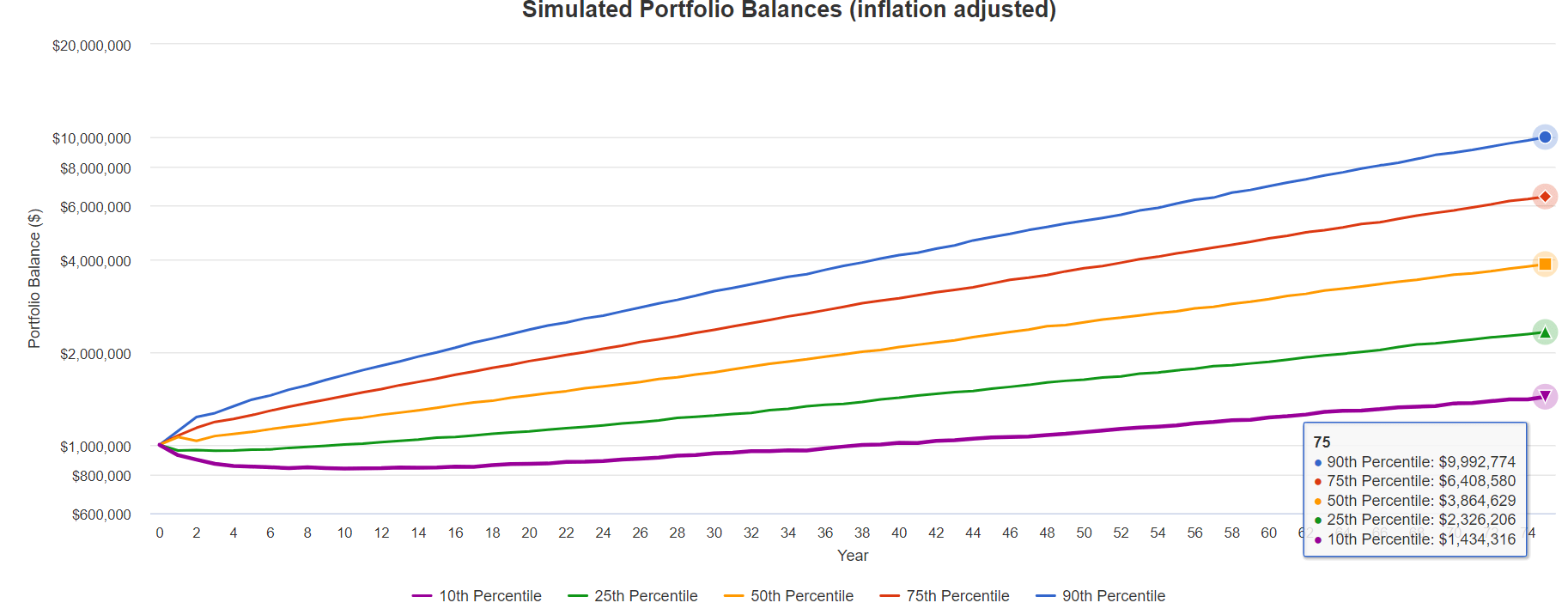

So, the 6.1% safe withdrawal rate survives the entire 75-year period, even in the worst-case scenario.

{kind=link}

The lowest this portfolio value falls to is $840,000 over the next 75 years.

{kind=link}

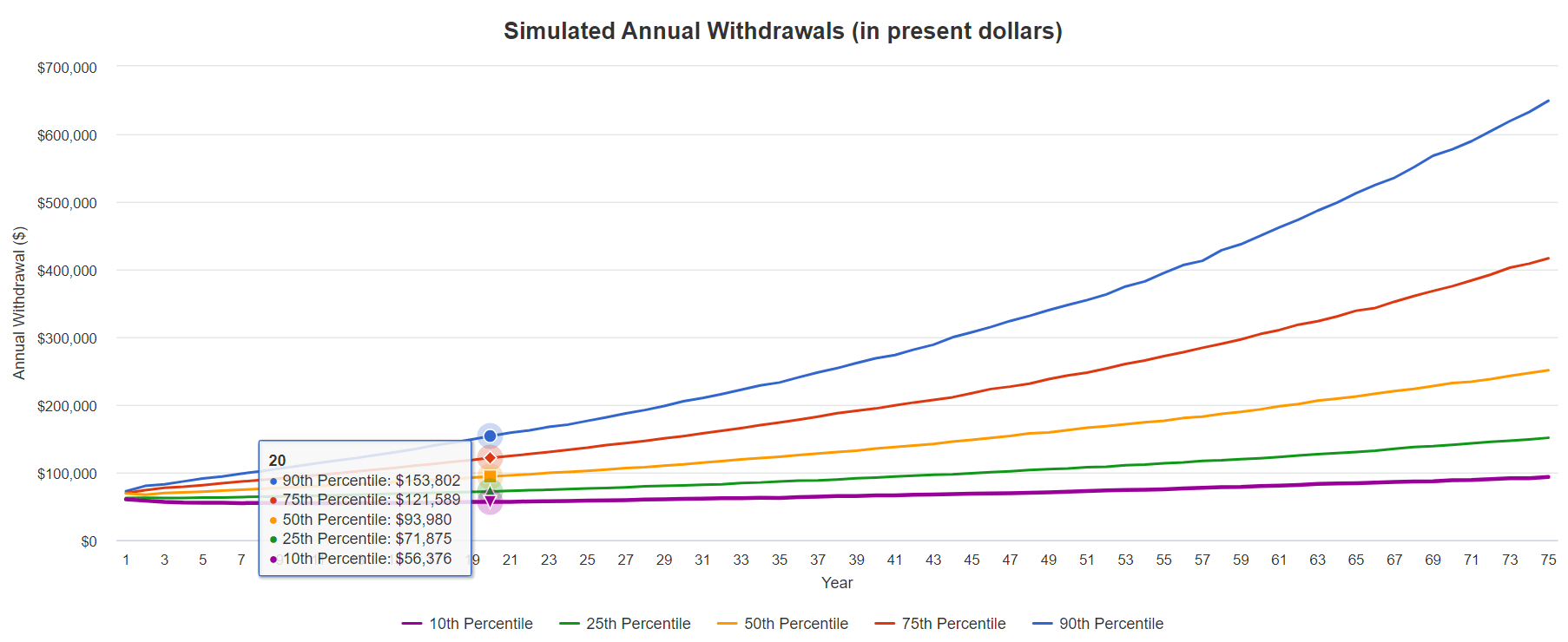

Starting with $60,000 per year in income and rising to around $94,000 by year 20 and $251,000 by year 75.

- These are adjusted for inflation.

{kind=link}

- 60/40 consensus: 7%

- S&P: 10.2%

- Nasdaq: 12.5%.

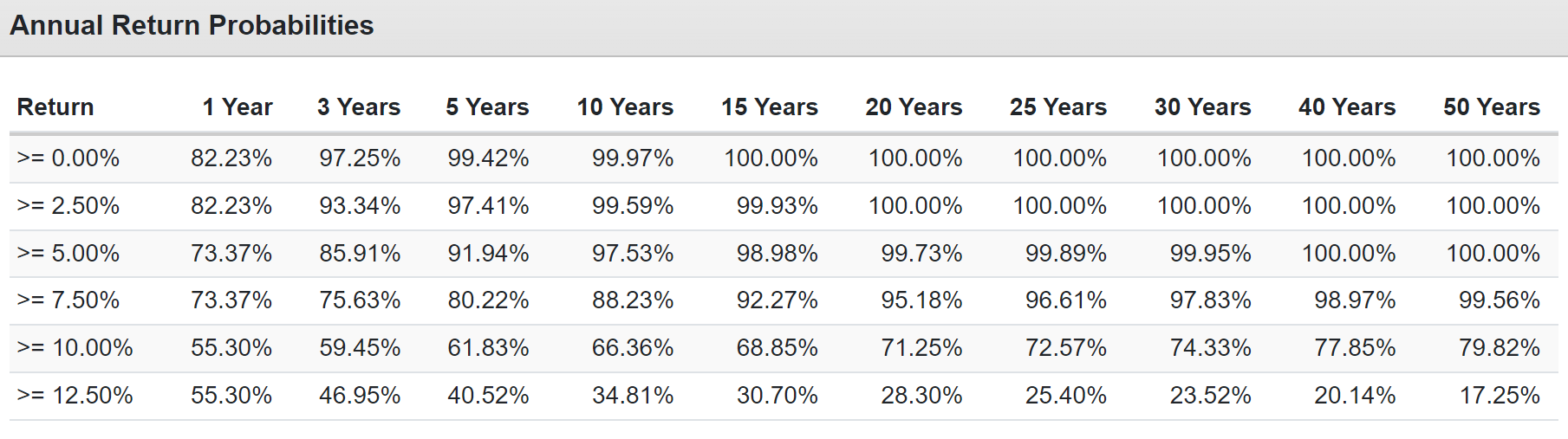

So ZEUS has a 99.56% chance of beating the 60/40 over the next 50 years, 80% chance of beating the S&P (SP500), and even a 17% chance of beating the Nasdaq (COMP.IND).

So what have we learned? That 50% of your expected total returns is a good rule of thumb for a safe withdrawal rate.

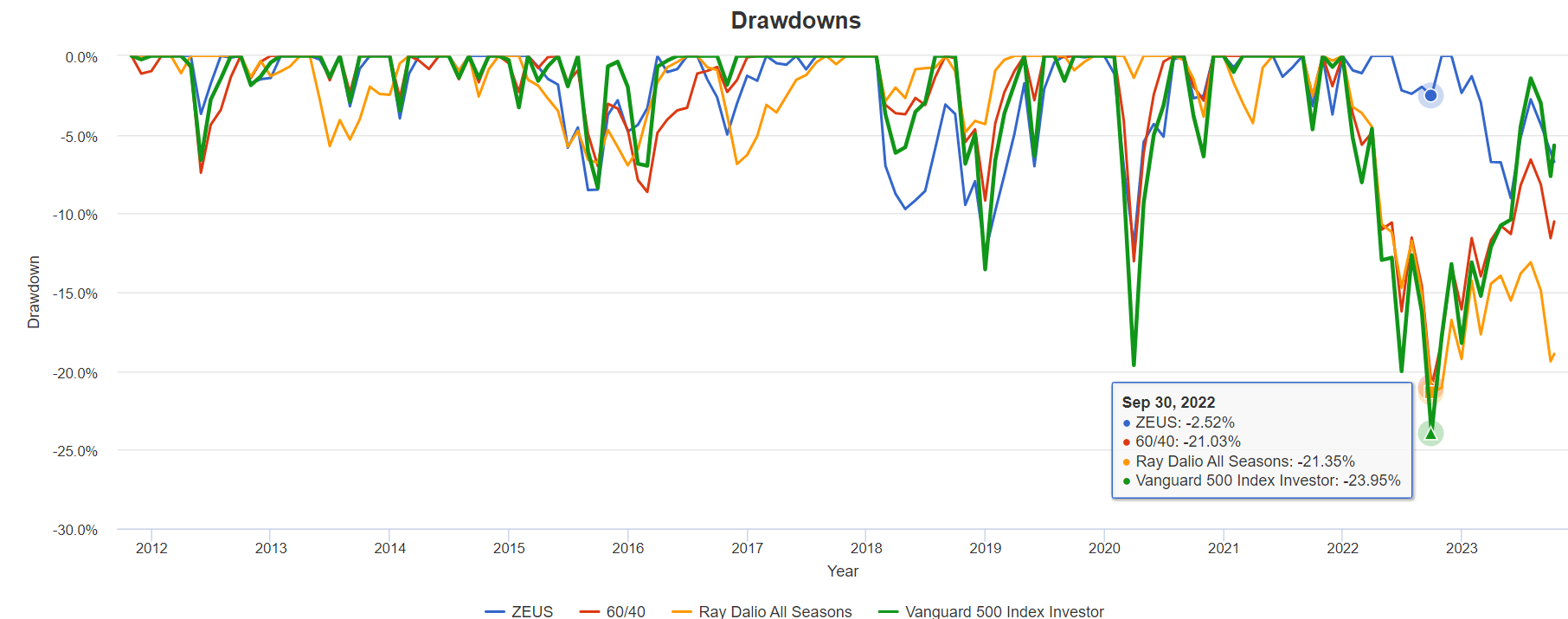

Historical Returns Since 2011

{kind=link}

Half the declines of the S&P 500 just as designed.

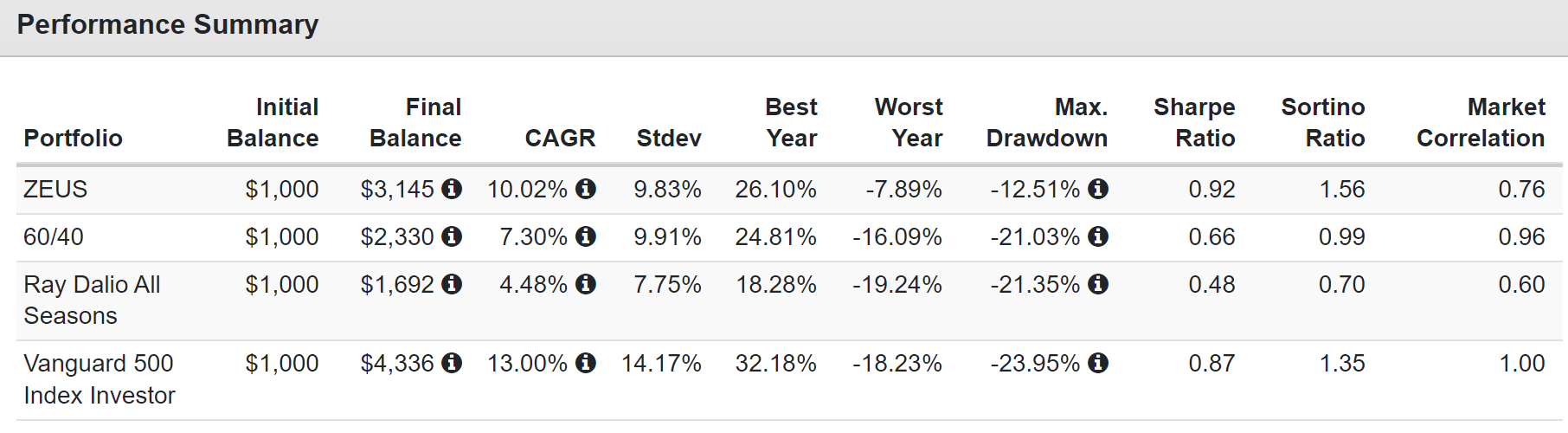

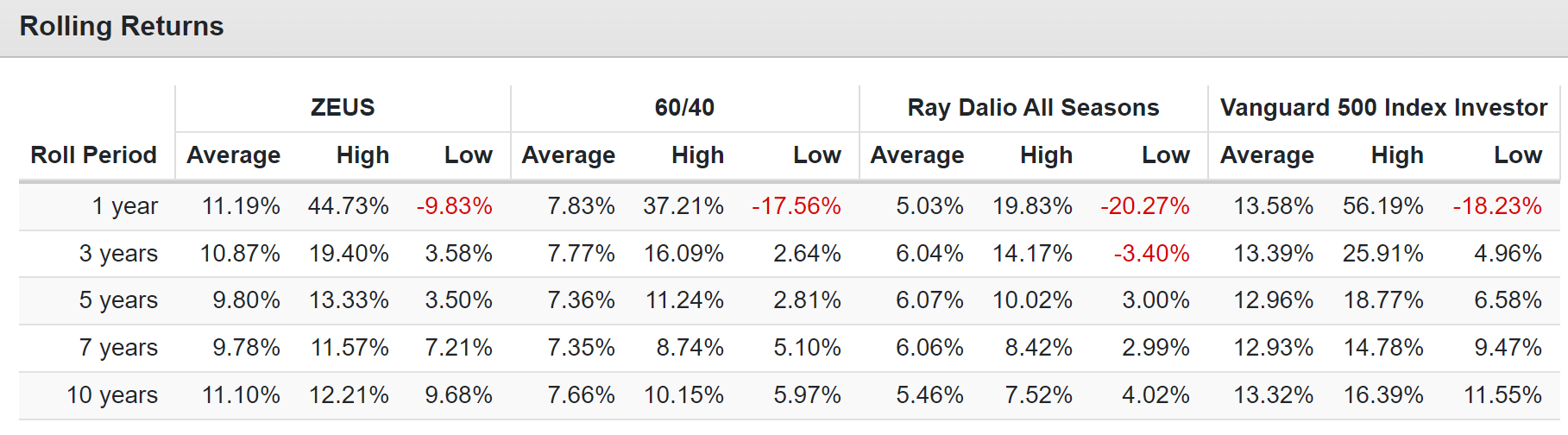

10% annual returns, 3% per year better than a 60/40, and Ray Dalio? The Hedge fund king? He did even worse (while charging an average of 5% per year).

{kind=link}

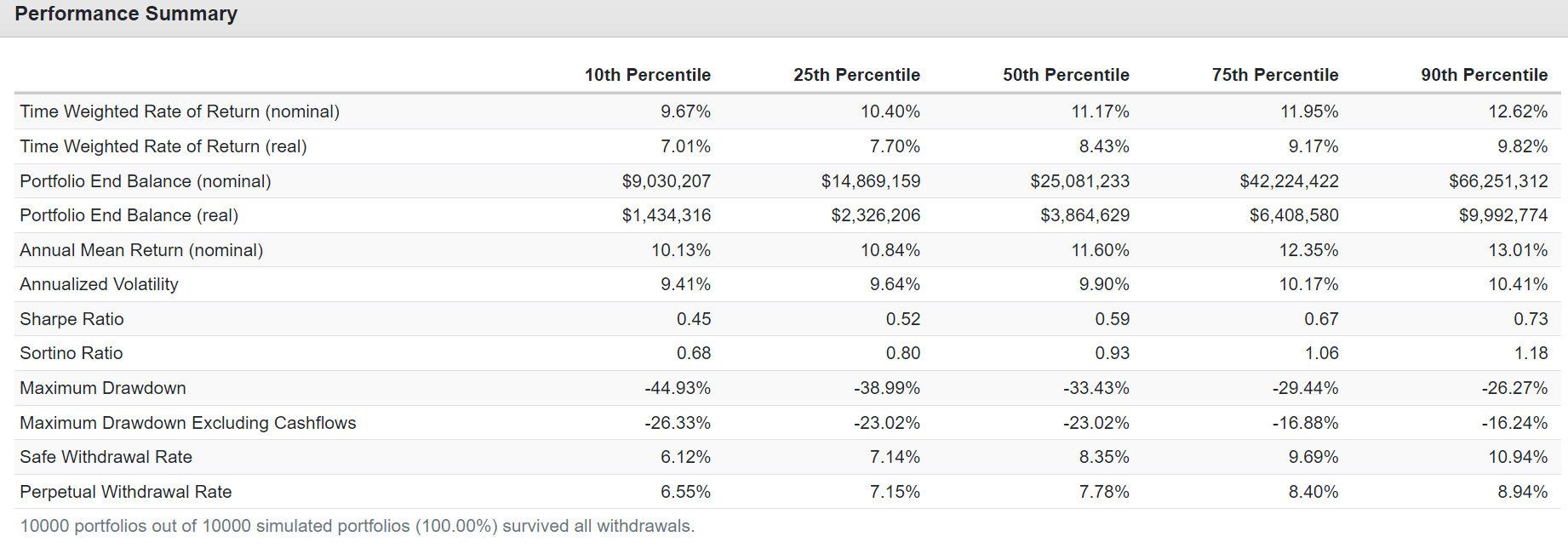

10% to 11% historical returns vs. 12% consensus forecast. That's pretty close, and the Monte Carlo simulation (10,000 of them) says a 90% chance of 10% to 13% annual returns.

Portfolio Visualizer Premium Portfolio Visualizer Premium

{kind=link}

{kind=link}

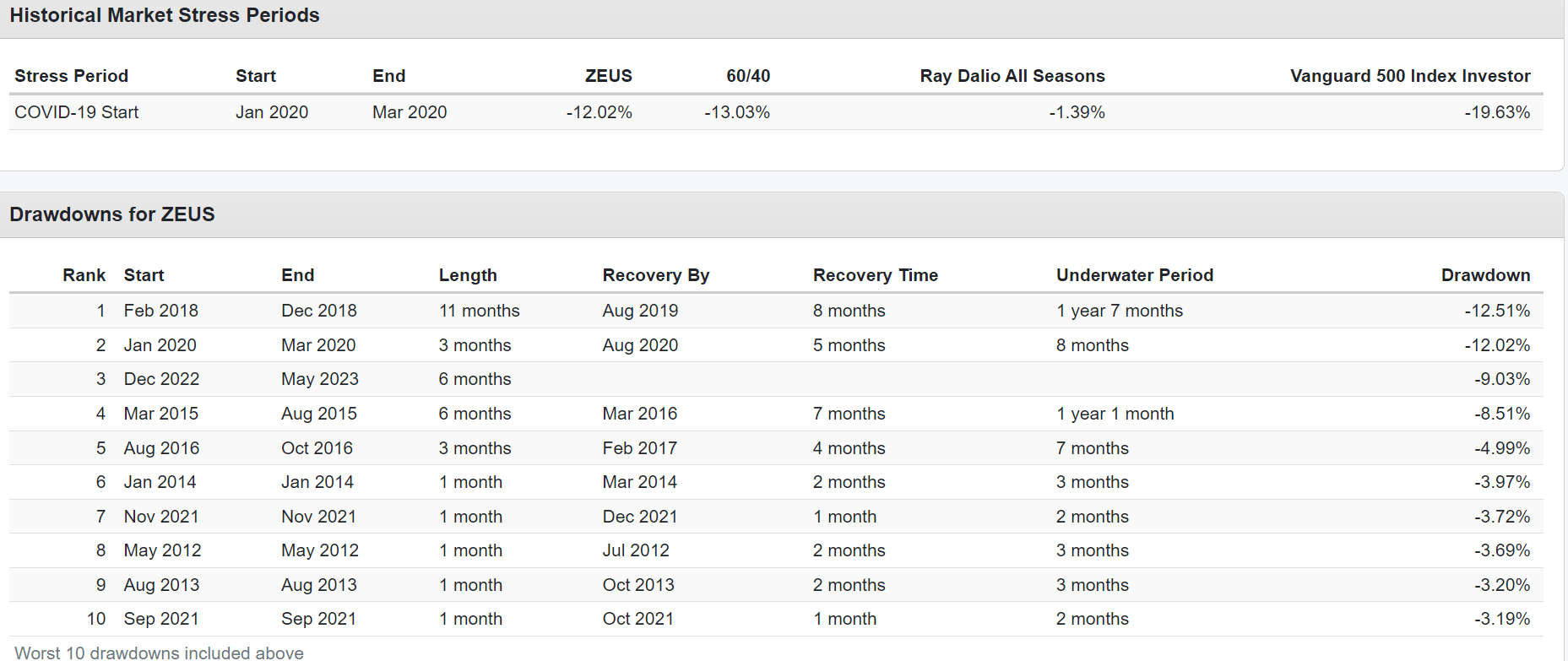

This ZEUS portfolio was down 3% during the October market bottom, 88% less than the S&P and even Ray Dalio's all-weather portfolio, which failed spectacularly in the 2022 bear market.

Bottom Line: Our View Is That SCHD + KMLM Is The Safest 5.3% Yielding Pure ETF Portfolio You Can Buy Right Now

Let me be clear: if you want personalized investment advice even deeper than what I showed you, you need a fiduciary CPA to walk you through your math.

Today I showed you a quick, basic analysis of how financial planning is done to create a framework for what your investing goals are, and how to go about building the asset allocation to achieve them.

SCHD and KMLM are the simplest 2-ticker retirement solution, requiring zero stock picking ever.

It's a 5.3% yielding portfolio that averages a 50% smaller decline than the market in bear markets, fell 88% less in the 2022 bear market, and is 80% likely to deliver double-digit returns, compared to 7% for a 60/40, for the next 50 years.

This portfolio is 99.56% likely to beat a 60/40 over the next 50 years.

And if you use a 6.1% withdrawal rate or less, there is a statistically zero chance of ever running out of money.

{kind=link}

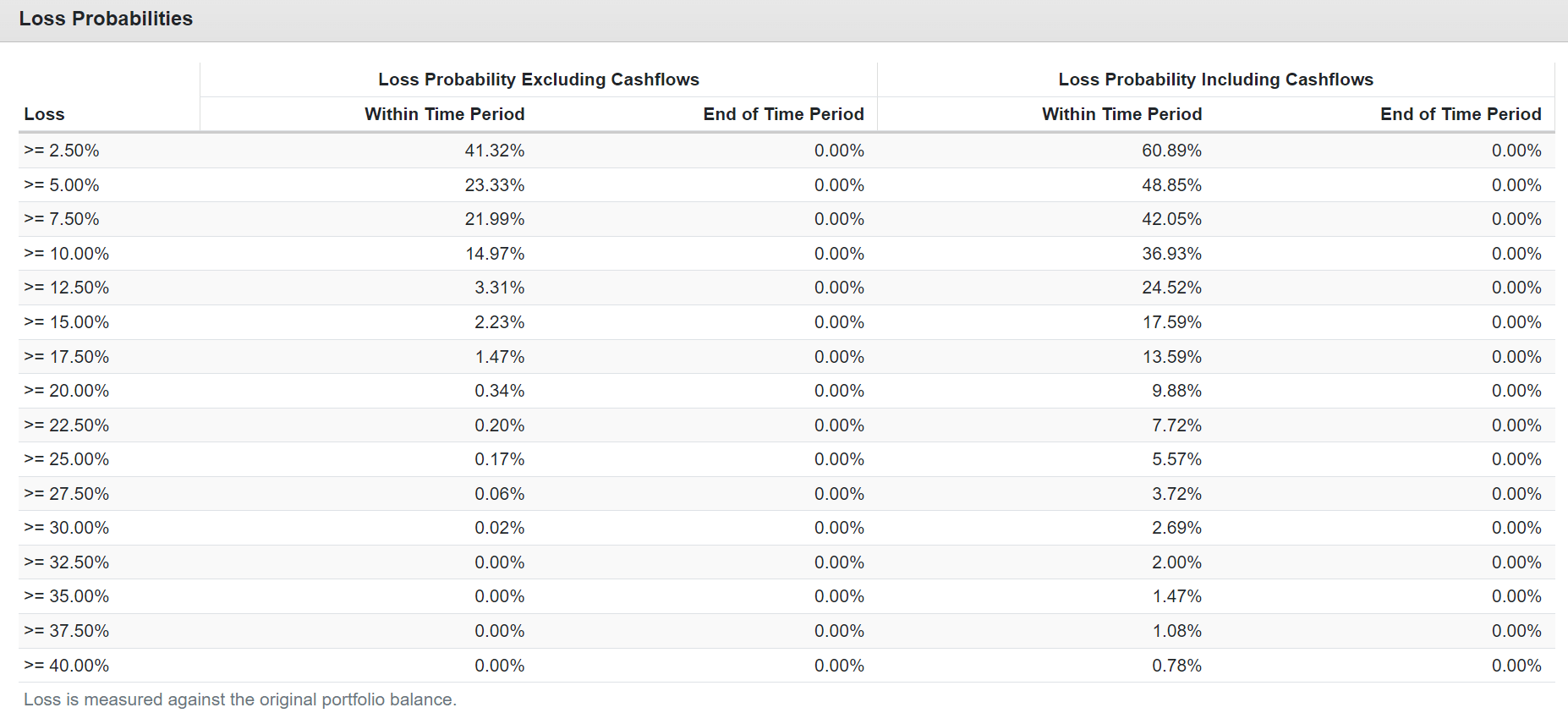

The probability of this ZEUS portfolio falling 20+% in the next 75 years is 0.34% or expected to happen once every 22,538 years.

A 30% decline probability is 0.02% or once every 375,000 years.

- The S&P averages a 30% decline every four years

- ZEUS is 93,750 less likely to fall 30% in any given year than the S&P 500

- while 80% likely to beat the S&P's total returns.

Can you see why I'm so passionate about safety and quality first, and prudent valuation and sound risk management always?

When you use disciplined, smart investing, you can build portfolios that are financial science-based magic and safe dividend-based sorcery;)

For further details see:

The Best Way To Invest $1 Million And Earn $53,000 In Annual Dividends