PBF - The Bottom Fishing Club: PBF Energy

2023-11-04 02:40:41 ET

Summary

- PBF Energy has a stellar balance sheet and is trading below tangible book value.

- The company operates in the oil refining business, which is competitive and cyclical, meaning a downturn in energy demand is the main risk.

- Based on 11 years of trading as a public company, average enterprise valuation multiples support a double in price to $90 a share for a 12-month target.

Another stock that has popped up on my screens for stellar balance sheets, with price trading well underneath tangible book value is PBF Energy (PBF). It has similar investment risk/reward characteristics to recently suggested Fresh Del Monte Produce (FDP) here , Danaos (DAC) here , and Seaboard (SEB) here . Each runs relatively capital-spending heavy businesses, without the use of much debt, which is quite rare.

YCharts - Undervalued Favorites, Price to Tangible Book Value, Since July 2021

My primary common-denominator search goals are equity market capitalizations and net enterprise values selling for less than GAAP accounting book worth on tangible assets. All are earning nice profits, cash flows are rich, while analysts are projected good times for 2024. Of course, you can find businesses selling for less than tangible book value on Wall Street today. But, the vast majority are operating money losers that conservative investors should avoid. Locating names with growing balance sheets and serious income/cash flow compounding your wealth is key.

PBF Energy is a large crude oil refiner based on the U.S. east coast. It produces gasoline, ultra-low-sulfur diesel, heating oil, diesel fuel, jet fuel, lubricants, petrochemicals, and asphalt, as well as unbranded transportation fuels, petrochemical feedstocks, blending components, and is moving into the more environmentally friendly hydrogen supply market.

PBF Energy Website - November 3rd, 2023

{kind=link}

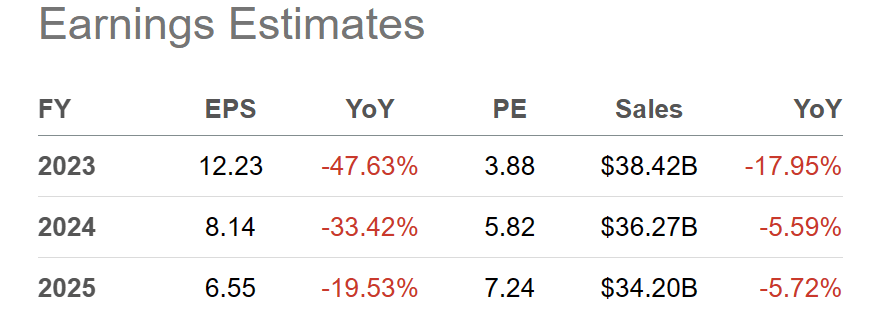

For sure, the oil refining business is quite competitive and cyclical. For example, during recessions, this part of the energy industry will lose money on imploding demand volumes and profit margins. At this stage, Wall Street is anticipating both a slowing economy and lower crude oil product pricing during 2024. You can see this forecast in current analyst projections for results from the company during 2023-25.

Seeking Alpha Table - PBF Energy, Analyst Estimates for 2023-25, Made November 3rd, 2023

{kind=link}

Even with a forecast of recession in 2024, the valuation and balance sheet have become so conservative and prepared for a downturn, I do not anticipate much of a share price decline from $45 on Friday (November 3rd, 2023). Why?

Cheapest Valuation Ever

The price to earnings ratio of 2x trailing results, 4x immediate future numbers, and 6x estimates for 2024 are some of the lowest you can find on Wall Street in November 2023. And, PBF has never been valued like this before, over the years since public trading began in late 2012. One explanation for the low valuation is the share price has rerated itself for the end of record-high crack refining spreads during 2022-23.

YCharts - PBF Energy, Trailing P/E Ratio, 10 Years

In terms of the most reliable predictor/support for company price, the quote valuation on tangible book value did trade closer to 0.4x right after the economic closures of the early days of the 2020 pandemic. Otherwise, price has rather consistently traded above net hard assets (cash, inventory, receivables, land, refineries, pipelines, storage tanks, trucks, etc. minus all liabilities).

YCharts - PBF Energy, Price to Tangible Book Value, 10 Years

Yet, these basic valuation tools only tell part of the bullish story. When we look at enterprise valuations, which includes changing debt and cash levels, the picture morphs drastically for the better. It's the consequence of management hoarding cash and feverishly paying off debt with the pandemic windfalls in cash flow and income. At the end of September, cash sat at $1.89 billion vs. $1.24 billion in financial debt (bearing interest) and $678 million in long-term lease obligations. Effectively, the organization is now "net" debt free.

So, when we look at the net real-world takeover or take private value of $5.92 billion in equity (at $45 a share), after all debts are extinguished and cash on hand is paid back to a single owner, this EV number is also sitting at a discount to net tangible assets for the first time in trading history during 2023. In contrast, even the 2020 bust-low EV to BV reading was a "premium" to cost-accounting and depreciated asset totals. My argument is PBF has reached a bottom of the barrel point to buy shares this year.

YCharts - PBF Energy, Enterprise Value to Tangible Book Value, 10 Years

Other impressive all-time low or nearly so stats are part of the enterprise valuation setup. EV to EBITDA (1.2x) and revenue (0.14x) multiples are difficult zones to seriously consider selling PBF.

YCharts - PBF Energy, Enterprise Value to EBITDA, 10 Years YCharts - PBF Energy, Enterprise Value to Revenue, 10 Years

Where else can you find a legitimate energy business with a total company value almost equal to ANNUAL earnings before interest, taxes, depreciation and amortization? Compared to a list of major U.S. oil refiners, none of them are priced as inexpensively as PBF Energy.

YCharts - Major U.S. Oil Refiners, Enterprise Value to EBITDA, 2022-23

Again, looking at EV to free cash flow generation, PBF is hands down the bargain pick of the group. Alongside the strongest balance sheet, investors are getting twice the free cash flow return on EV (theoretical total company worth) as the industry average (37% vs. 19%).

YCharts - Major U.S. Oil Refiners, EV to Free Cash Flow, 12 Months

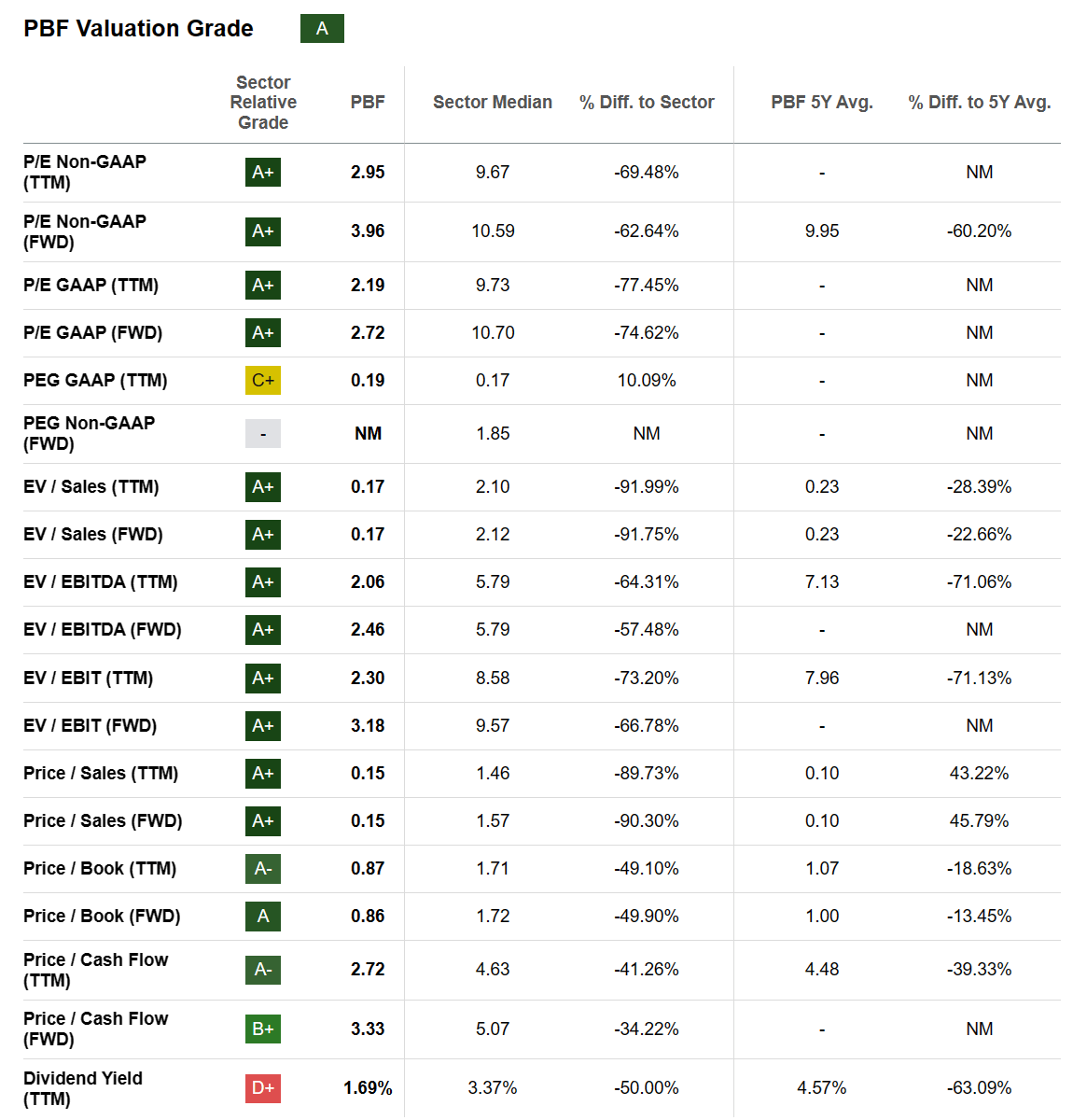

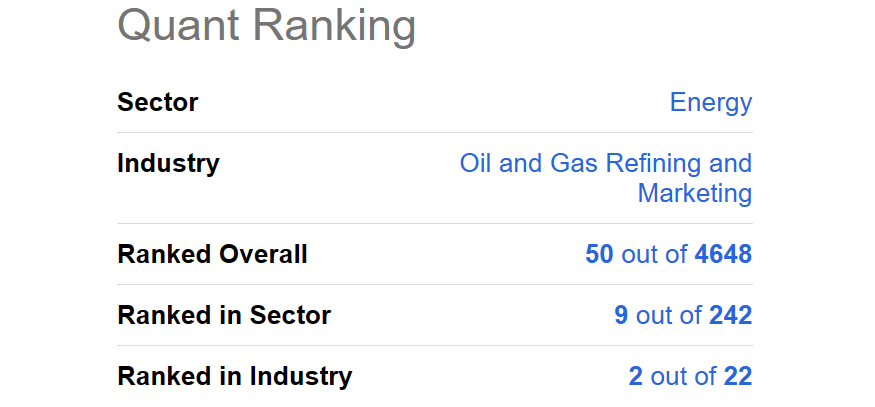

Seeking Alpha's computer ranking system puts a Valuation Grade of "A" on PBF Energy presently. And, the Quant sort formula reviewing trading momentum and operating results has the stock listed as a Top 1% buy proposition today.

Seeking Alpha Table - PBF Energy, Valuation Grade, November 3rd, 2023 Seeking Alpha Table - PBF Energy, Quant Rank, November 3rd, 2023

{kind=link}

{kind=link}

Final Thoughts

Not only does the elimination of debt help when interest rates (expense) are rising, but it gives financial flexibility to prepare for a potential recession. PBF might even be able to pick off some assets at a steal price during any economic downturn as cash coffers are still building every day.

I definitely recommend reading the short article posted this week on the company here by fellow analyst Seeking Profits . Refining capacity has not grown in America since the end of the Great Recession in 2009, largely because of environmental regulations. Plus, total capacity today is not much different than 10 years ago. What this means is any hiccup in plant operations around the country (weather, maintenance, fire) could easily support future spikes in profit margins for PBF Energy.

Crack refining spreads are nearing 2-year lows presently, an indication of a stabilizing supply/demand situation after the pandemic. The remaining good news is pricing and profit spreads are still considerably above the lows of 2020 during the oil/gas bust.

EnergyStockChannel.com - Crack Spreads per Barrel, 5 Years

My overall view is any unexpected, outsized gain in crude oil during 2024, and/or a U.S. economy that skirts deep recession, should allow for nice share price gains in PBF Energy. Just remember, a serious or prolonged economic downturn could lead to price again selling at a 30% to 40% discount to tangible book value, as the market tries to price in meaningful operating losses. Such could translate into a $30 PBF quote from $45 today, as the risk side of the investment equation (in my research, accounting for the much-improved balance sheet since 2020).

An outlier risk has to do with government interference and potential fines/lawsuits eating into cash holdings. Either price gouging claims or environmental pollution are the excuses. California is a state leading the attack on oil/gas industry businesses.

Nevertheless, if energy demand remains strong next year, crude oil prices rise, and crack margins are stable, EPS in the $7 to $10 range is possible over the next 12 months. Given this rosy scenario and better investor interest pushing the P/E toward 10x, an upside projection of $70-100 for share pricing seems reasonable. Further, factoring in the dirt-cheap enterprise valuation, a normalized EV number of 2x tangible book value would bring at least $90 for a target price by the end of 2024.

I rate PBF Energy a Buy and own a position. To me, the growth potential of +100% for a total return (including a 2.2% forward-indicated dividend yield) is far juicier than the downside risk in a deep recession of -30%.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

The Bottom Fishing Club: PBF Energy