LEVI - The Bottom Fishing Club: V.F. Corp

2023-03-20 09:44:10 ET

Summary

- An extremely low V.F. Corporation valuation has materialized on the multi-year drop from $100 to $21 a share.

- The stock is now one of the cheapest apparel makers available on Wall Street.

- Some share accumulation indications have popped up in recent weeks.

- V.F. Corporation may be an excellent buy-on-weakness idea into April for long-term thinkers.

I have not written a full-length article on V.F. Corporation ( VFC ) over my 10 years on Seeking Alpha. Risks in the apparel-making industry are many, and the valuation story has not stood out to me. That is, until the last few months.

The company markets apparel under brand names including Vans, The North Face, Timberland, Jansport, and numerous others.

{kind=link}

Today, I want to explain the tremendous valuation argument to own VFC stock. The nearly 80% drop in price from over $100 in late 2019 has occurred at the same time as operating results have not changed materially. The dividend has been cut as the company deals with a short-term cash flow crunch, but still stands at a well above-average rate vs. the industry and overall U.S. equity market of 5.6%. If earnings and cash flow hit current Wall Street estimates, VFC is essentially already trading at a valuation similar to past recessions, including its 1990-91, 2001, and 2009 lows.

A new wrinkle in the investment setup is some unusual buying has appeared in my technical trading momentum sorts, the kind of interest that occurs near bottoms historically.

So, if you are willing to take on the higher-than-typical risks of an apparel maker (because of quickly changing consumer tastes) going into a 2023 recession, investors may be rewarded handsomely by 2024 with both a strong cash yield upfront and significantly higher stock quote (eventually).

Undervaluation Story

The first noteworthy assessment is price to trailing fundamentals is near a decade low in March 2023, using basic ratio analysis. Cash flow generation has been the big problem over the past year as inventories swelled by $1.3 billion between December 2022 and the same month in 2021. Unsold clothing items are the issue facing VFC in 2023, and excuse for a struggling stock quote. Rising interest costs and a large goodwill impairment charge are other reasons.

YCharts - V.F. Corp, Price to Trailing Fundamentals, 10 Years

Price to forward projected sales is now one of the cheapest in the major apparel sector of Wall Street. A ratio of 0.717x revenues compares quite favorably against peers and competitors Ralph Lauren ( RL ), Levi Strauss ( LEVI ), Tapestry ( TPR ), Gildan Activewear ( GIL ), Lululemon ( LULU ), Under Armour ( UAA ), Nike ( NKE ), Columbia Sportswear ( COLM ), and Hanesbrands ( HBI ).

YCharts - Major Apparel Makers, Price to Forward Estimated Sales, 1 Year

Even better for shareholders, price to forward earnings estimates are just above 10x, which is effectively the lowest of the group.

YCharts - Major Apparel Makers, Price to Forward Estimated EPS, 1 Year

On a graph back to 1990, a P/E of 10x would be the lowest since the Great Recession ended in 2009, and on a par with the recession lows of 2001 and 1990-91.

YCharts - V.F. Corp, Price to Earnings, Since 1990

In terms of cash earnings (before charges and writeoffs), VFC's recovery from the COVID pandemic has been stronger than most peers and rivals.

YCharts - Major Apparel Makers, EPS Growth Since 2021, Wall Street Analyst Estimated to 2025

Plus, when we include debts and subtract cash holdings, the enterprise value calculation on EBITDA (earnings before interest, taxes, depreciation and amortization) or revenues is the lowest since 2012. The EV setup is close to its long-term average valuation since 1986, when the company was much smaller. Honestly, fewer than 10% of U.S. equities are trading near 40-year averages on EV ratios, as the general market remains closer to record overvaluations on underlying fundamentals.

YCharts - V.F. Corp, EV to EBITDA & Sales, Since 1986

Technical Trading Picture

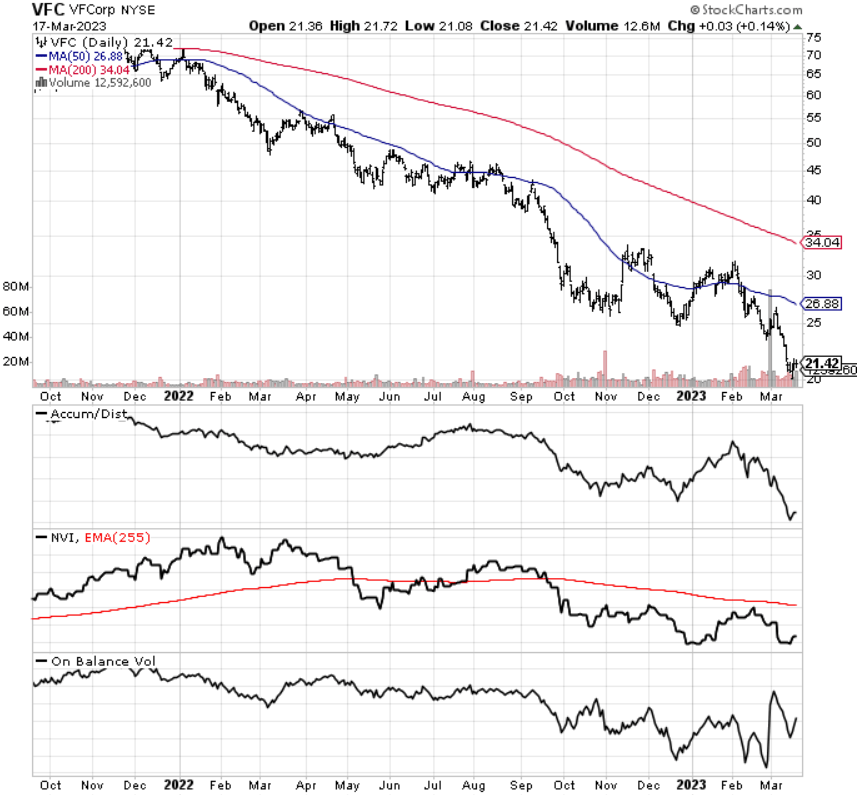

Another draw for me to VFC is its trading chart. The oversized price drop from $30 to almost $20 in 2023 has occurred in the face of quickly improving momentum indicators. I mentioned VFC as a buy candidate based purely on this divergence in technical activity a month ago. And, the buy proposition has only improved for long-term investors.

On the 18-month chart below, you can see how the Accumulation/ Distribution Line had a terrific January showing (which has faded into March), while the Negative Volume Index and On Balance Volume readings are trying to hold their December lows. What this means is considerable accumulation is taking place, although worries about a recession have hit the share quote through emotional purging by previous shareholders sitting on (taking) large losses.

The share price may act like a bobber when fishing. It could jump out of the water when your target fish quits fighting or you yank your line it out of the water. When this round of selling is finished (it could take days or weeks), price will likely recover nicely above $25 later in the year.

StockCharts.com - V.F. Corp, Daily Price & Volume Changes, 18 Months

{kind=link}

Final Thoughts

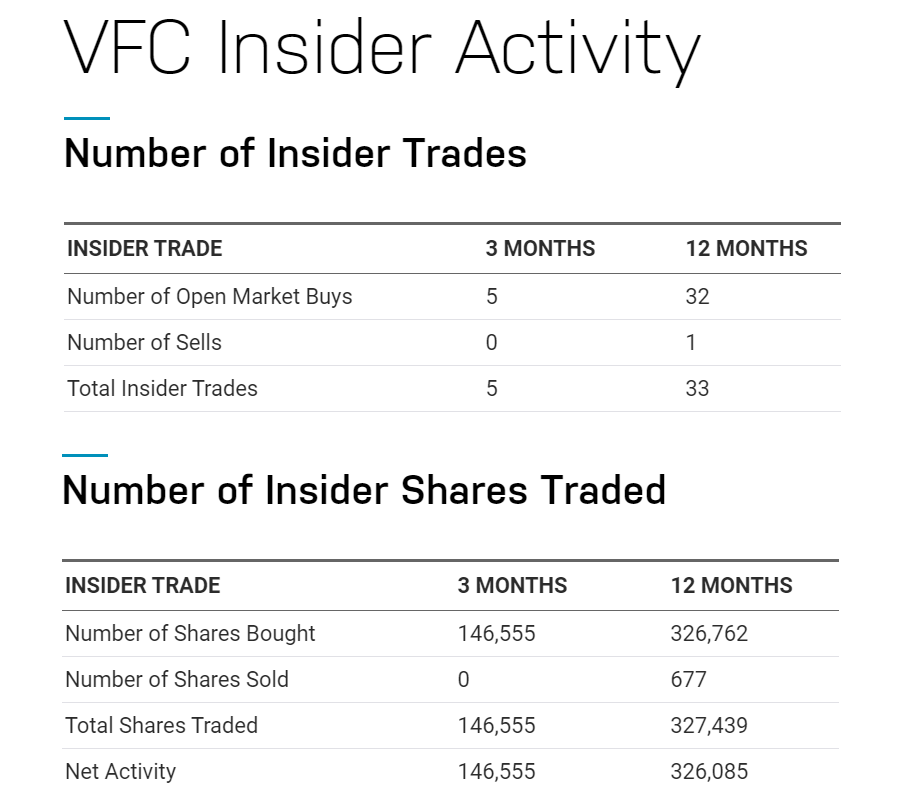

Insiders and management have increased their buying activity in V.F. Corporation stock under $30 a share since October. They believe something of a long-term bargain situation has opened. If serious long-term issues, hard to recover from, were the VFC future, I doubt insiders would be aggressively adding to their positions.

Nasdaq.com - V.F. Corp, Insider Trading Activity

{kind=link}

That said, VFC stock is not exactly a screaming buy as we enter a recession. But, the valuation is so low and technical clues becoming more bullish, I suggest taking a small position in V.F. Corporation close to $20 a share. My buy plan will be to add to my stake as prices decline (if they do) under $20 into April.

Can I guarantee an investment profit in 12-18 months? No, but the odds are becoming stacked in favor of a rise in price, sooner or later. Taking a measured cost-average approach can reduce your initial risk, if a deep recession sinks the VFC price to $15. And, if you can purchase a bigger stake at lower quotes, an eventual rebound should translate into nice investment gains. A return trip to $30+ by 2024 is probable, assuming a deep and prolonged recession is not next. That is the outlier risk (a monster recession does have a chance of occurring into 2024) for those jumping onboard VFC.

V.F. Corp. does carry significant debts and financial leverage, with rising interest expense. This is the main reason the stock price has been able to fall dramatically with stagnate business results. Total liabilities to assets are far greater than peers today.

YCharts, Major Apparel Makers, Total Liabilities to Assets, 3 Years

If management can focus on shrinking debt/leverage during 2023-24, the stock price and valuation will recognize/reward this progress with higher quotes and metrics on operating results.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

The Bottom Fishing Club: V.F. Corp