BCO - The Brink's Company: Dividend Increases Innovation And M&A Imply Undervaluation

2023-09-05 03:10:21 ET

Summary

- The Brink's Company delivers beneficial guidance for 2023, including lower net leverage and growing FCF.

- Investments in infrastructure, innovations, and acquisitions could enhance FCF margins.

- Communication efforts on dividend distribution and stock repurchase programs may accelerate demand for BCO stock.

The Brink's Company ( BCO ) recently delivered beneficial guidance for 2023, including lower net leverage and growing FCF. I believe that further investments in infrastructure, innovations related to CompleteTM and CompuSafe services, and new acquisitions at beneficial valuations like that of NoteMachine could enhance the FCF margins. Additionally, more communication efforts to remark on the growing dividend distribution and more stock repurchase programs will most likely accelerate the demand for the stock. I do see risks from the total amount of debt, changing regulations, or failed international expansion, however the stock does really seem undervalued.

The Brink's Company

The Brink's company is a leading global provider of cash and value management, digital retail solutions, and ATM services. With a presence in more than 100 countries, it serves clients such as financial institutions, retailers, and government agencies. Founded in 1859 and headquartered in Richmond, Virginia, the company has undergone name changes over time. It employs approximately 72,200 people, and operates more than 1,300 facilities and 16,400 vehicles.

Source: 10-k

The Brink's company offers cash and valuables management services, including the secure transportation of cash between retailers and financial institutions as well as the transportation of valuables globally. In addition, it provides basic ATM management services, secure transportation solutions for high-value products through Brink's Global Services, and cash management services tailored to customer needs.

Its model also includes surveillance services, commercial security systems, and payment services. Brink's success has been built on safety, quality of service, risk management, and logistics expertise to serve customers around the world.

With the presentations being done about the business model, I believe that it is relevant to note about the guidance given by management in the most recent quarter. The company is expecting revenue growth close to 6%-9%, with Adjusted EBITDA close to $865-$915 million and FCF around $325-$375 million. In my view, if the numbers are as good as reported, or even a bit better, more market participants will most likely have a look at the stock.

Source: Investor Presentation

I studied a bit about the earnings releases previously reported by The Brink's Company. In 2023 and 2022, the company reported better than expected EPS figures. It means that management appears to be quite conservative with its estimates. In my opinion, further better than expected figures would most likely accelerate the demand for the stock.

Source: SA

Balance Sheet

As of June 30, 2023, the company reported cash and cash equivalents worth $890.1 million, with restricted cash of about $433.5 million, accounts receivable of $851 million, and total current assets close to $2.517 billion. Current assets/current liabilities ratio is larger than 1x, so I believe that liquidity does not seem an issue here.

Property and equipment stands at about $990.2 million, with goodwill worth $1.467 billion, other intangibles of about $516.2 million, and total assets of $6.411 billion. The asset/liability ratio is equal to close to 1x. Thus, the balance sheet does look quite stable, however investors may want to have a close look at the total amount of debt.

Source: 10-Q

With short-term borrowings worth $127.5 million, current maturities of long-term debt of $89.9 million, and accounts payable worth $231.5 million, total current liabilities stood at $1.619 billion. Long term liabilities include accrued pension costs of $134.1 million, retirement benefits other than pensions of $173.1 million, and total liabilities of $5.747 billion.

Source: 10-Q

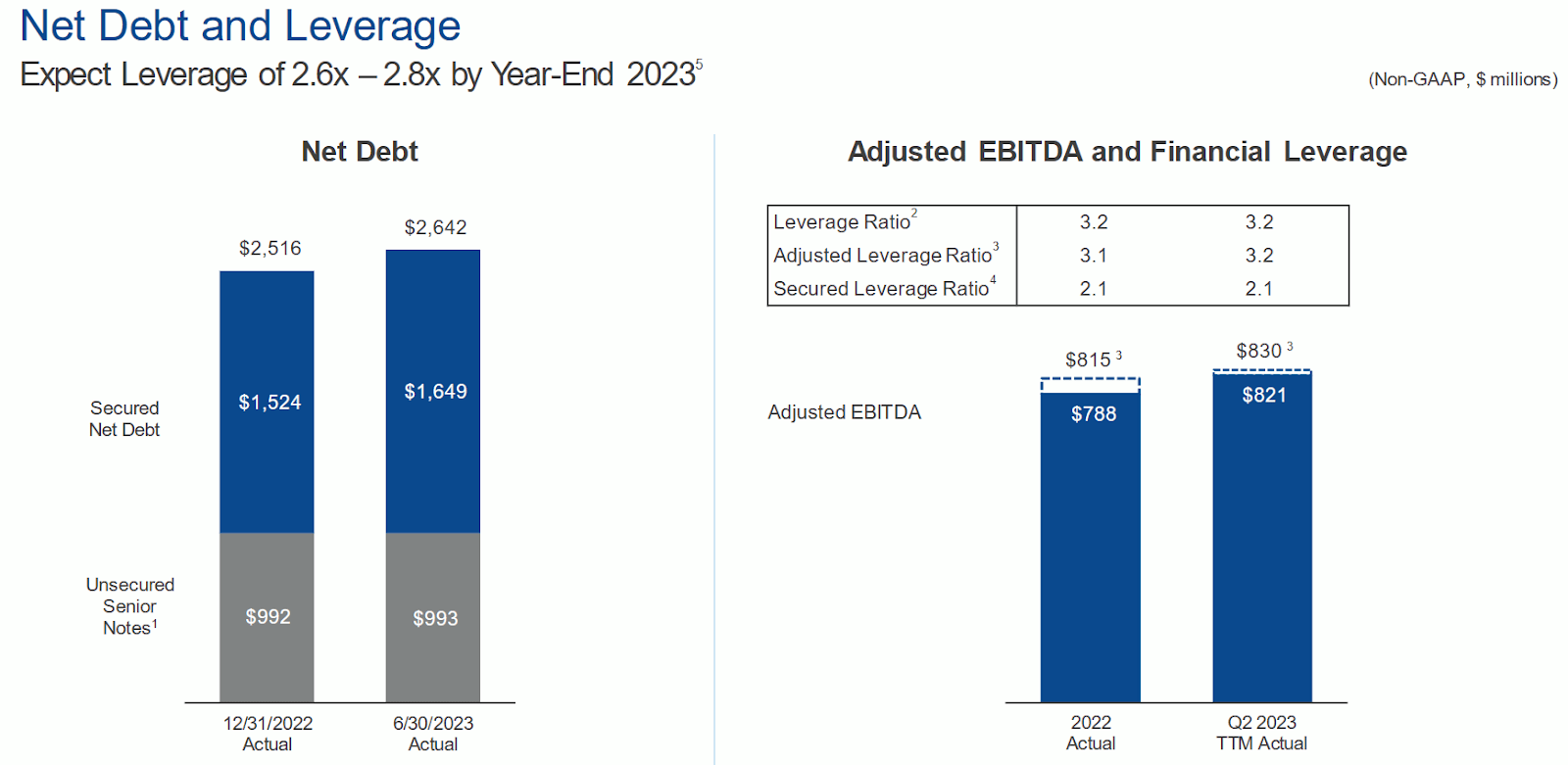

In the last presentation given to investors, The Brink's Company reported expectations of net leverage of close to 2.6x-2.8x. I am not concerned about the total amount of debt because The Brink's Company appears to run a business model that offers long term EBITDA and solid margins. With that, I would understand if conservative investors are a bit concerned about the total amount of leverage. I believe that lower leverage would most likely bring the attention of more market participants, and may lead to stock price enhancements.

{kind=link}

Contractual Obligation And Debt

In June 2022, The Brink's modified its senior secured facility. The credit facility consists of a $1 billion revolving credit facility and $1.4 billion term loans. Loans mature on June 23, 2027, with quarterly principal payments and a final lump sum at maturity. Interest rates are based on the secured overnight funding rate plus margin. The credit facility is secured by assets of the company and certain of its domestic subsidiaries, and the spread of the loans is adjusted based on the company's total net debt leverage ratio. As of December 31, 2022, $353 million was available on the revolving credit facility. The information about different loans and borrowings reported by the company is given below. The interest rate paid is close to 4%-5%. I used these figures to assess my DCF model and forecasting.

Source: 10-k

Share Repurchases And Constant Annual Dividend Increases Could Accelerate The Demand For The Stock

With regard to capital allocation, in my view, there is a lot to like. As soon as more market participants notice the repurchase of shares executed during the year 2023, in my view, stock demand could increase. In the first six months of 2023, the company acquired a significant amount of shares at a price close to $64 per share, and noted that $180 million remained available under the 2021 Repurchase Program.

During the first six months ended June 30, 2023, we repurchased a total of 272,467 shares of our common stock for an aggregate of $17.5 million and an average price of $64.38 per share. These shares were retired upon repurchase. At June 30, 2023, $180 million remained available under the 2021 Repurchase Program. Source: 10-Q

There is also the fact that The Brink's Company plans to increase its dividend distribution annually, which may also accelerate demand for the shares. According to SA, in the last 5 years, dividends increased by close to 6%, and in the last presentation, management confirmed that dividends would increase further.

Source: SA

Source: Investor Presentation

Net Sales Catalyst: Internationalization Could Bring Further Net Sales Growth And Geographic Diversification

The company currently serves customers in more than 100 countries, and reports 52 countries where it operates subsidiaries. With a business model proven in many jurisdictions, I believe that further internationalization could be easy. As a result, investors may be expecting net sales growth driven by a larger market opportunity. My rationale is that when The Brink's Company enters a new country, the potential number of customers multiplies. In this regard, it is worth noting that the company reported much quarterly revenue in Latin America and Europe.

Source: 10-Q

FCF Catalyst: Technological Solutions, Economies Of Scale, And Efficiency Will Most Likely Lead To FCF Growth

The Brink's Company seeks to simplify the management of cash and valuables with technological solutions and optimization. It uses technological improvements like Brink’s CompleteTM and CompuSafe services to introduce new value propositions, improve efficiency, and build infrastructure to increase scale and profitability. I assumed that these initiatives will most likely accelerate revenue growth, improving margins and cash flows in the changing payments ecosystem.

Acquisitions Would Most Likely Accelerate Scale, And Bring Further FCF Growth

Considering previous acquisitions, I am also expecting significant improvements in terms of FCF and net sales growth. In this regard, it is worth mentioning that the company acquired NoteMachine Limited, one of the leading ATM networks in the United Kingdom.

NoteMachine has one of the largest cash machine networks across the UK and is one of the leading ATM businesses in Europe. With over 11,000 cash machines in operation, we’re proud to say that every month, around 27 million people use at least one of our ATMs. Source: About – NoteMachine

The acquisition was done for approximately $179 million or 5.0 times adjusted EBITDA. The Brink's Company trades at close to 9.4x, so I believe that investors would most likely appreciate the deal. At the end of the day, you are buying a business at 5x EBITDA, and selling your own shares at more than 9x.

Source: Ycharts

I consulted the financials of NoteMachine, and I believe that The Brink's Company made an impressive acquisition at an attractive valuation. The acquisition is expected to be accretive to earnings in the first year, so I believe that we may see certain improvements in the financials of The Brink's Company in the near future.

Source: 10-Q

It is also worth noting that recent acceleration in goodwill indicates that The Brink's Company has extensive expertise in the M&A markets, and intends to grow more inorganically. In a recent presentation given to investors, The Brink's Company noted that it intends to acquire new targets offering strong synergy potential.

Source: Investor Presentation

Source: Ycharts

Valuation Model

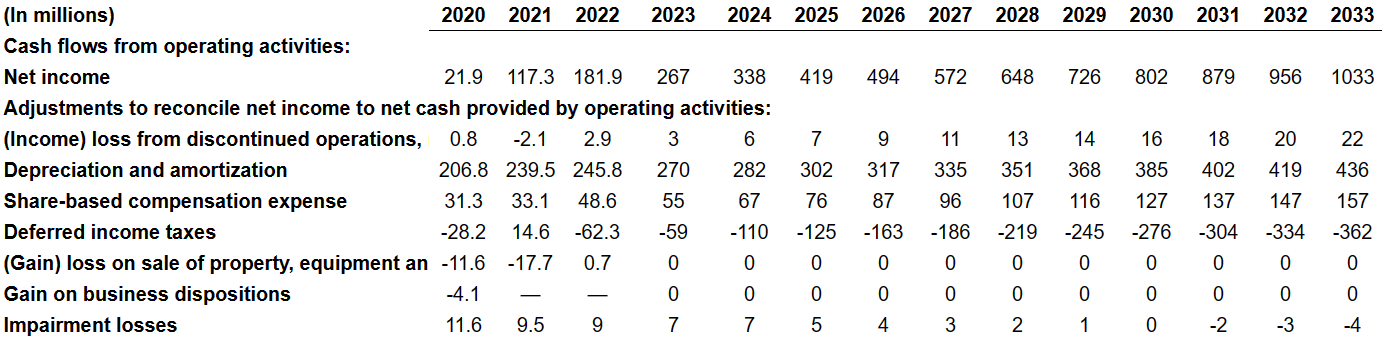

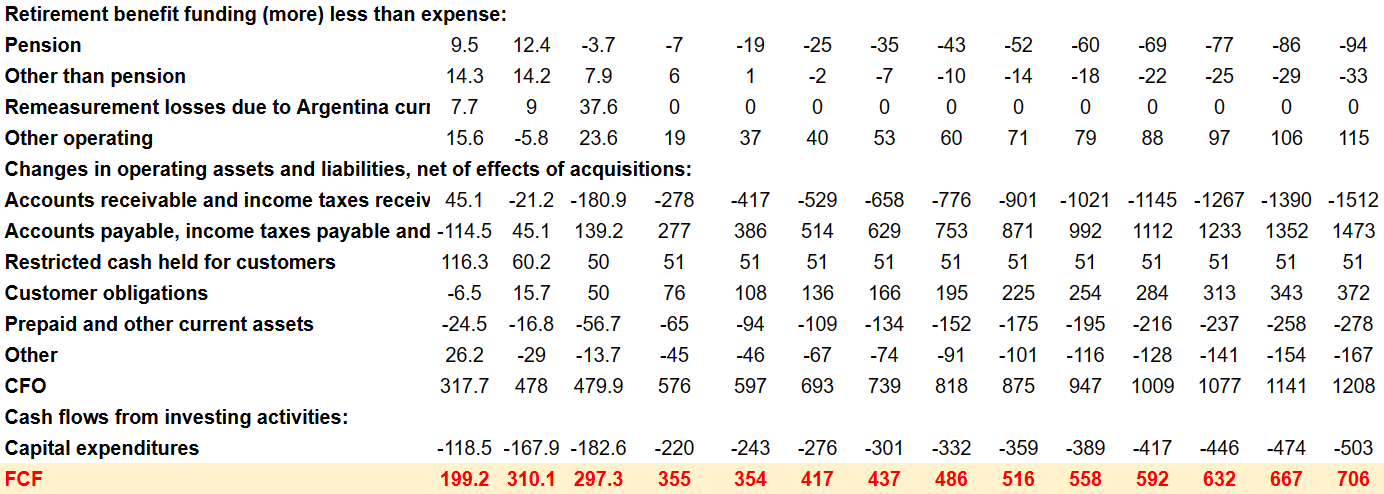

My forecasts included 2033 net income of $1.033 billion, with the following adjustments to reconcile net income to net cash provided by operating activities. Depreciation and amortization would stand at $435 million, with share-based compensation expense of $156 million and deferred income taxes worth -$363 million.

{kind=link}

Changes in operating assets and liabilities included changes in accounts receivable and income taxes receivable of about -$1512 million, accounts payable, income taxes payable, and accrued liabilities worth $1473 million, and restricted cash held for customers close to $51 million.

Besides, with customer obligations worth $372 million and prepaid and other current assets of about -$279 million, CFO would be close to $1.208 billion. Finally, cash flows from investing activities would include capital expenditures of -$503 million, so that the FCF would be $705 million.

{kind=link}

Using a terminal EV / 2033 FCF of 19x, which I consider quite adequate, the company currently trades at 17x, but it traded at more than 36x in the past.

Source: Ycharts

With my previous assumptions, my forecasts would include NPV of future FCFs worth close to $8.048 billion. Besides, if we also add cash and cash equivalents of $890 million and restricted cash worth $433 million, and subtract short-term borrowings worth $127 million, current maturities of long-term debt of $89 million, long-term debt worth $3251 million, accrued pension costs close to $134 million, and retirement benefits worth $173 million, the equity value would be $5596 million. Finally, the forecasted implied fair price would be close to $120 million, and the forecasted internal rate of return would be 5.86%.

Source: My DCF Model

Sensitivity Analysis

I ran a sensitivity analysis to understand how changes in the terminal EV/FCF and the cost of capital would affect the forecasts' implied price and the forecasted IRR. With changes in the cost of capital between 7.5% and 12.5% and EV/FCF of about 15x-21x, the implied forecasted price would be $73-$173. Besides, the forecasted IRR would be between -0.39% and 12%. With these figures in mind, I believe that there is an upside potential in the stock price.

Source: My DCF Model

Source: My DCF Model

Risks

Brink's faces risks related to its ability to make successful acquisitions and investments to support its growth strategy. Competition for suitable purchases can increase prices and reduce available options. The successful integration of the acquired businesses, operating performance, and profitability depend on various factors, and are subject to risks, such as business plan implementation issues, unforeseen changes in laws and regulations, labor issues, unfavorable customer feedback, and regulatory and environmental challenges. Raising funds to finance acquisitions also presents uncertainties, and may require additional financing through loans and securities issuances that could adversely affect shareholders.

Competitors

In my opinion, Brink's competes in the global cash and securities management market with large multinational companies such as Loomis AB ( OTCPK:LOIMF ), Prosegur ( OTCPK:PGUCY ), Compañía de Seguridad, SA, or Garda World Security Corporation. As compared to the peers offered by SA, The Brink's Company is not cheap, but not expensive either. With that, it is worth mentioning that the sector is trading at close to 5x-13x EBITDA, which is not that expensive.

Source: SA

Its main competitive advantages include strong brand recognition, an outstanding reputation for high level of service and safety, logistics and risk management expertise, an extensive global network and established customer base, proven operational excellence, coverage of high quality insurance, and financial strength. Although facing competitive pricing pressure, Brink's excels by focusing on providing a superior experience, value-added solutions, and a focus on quality of service to differentiate itself in the marketplace.

My Conclusion

Brink's appears to offer significant competitive advantages, such as brand recognition, reputation for a high level of service, and strong global infrastructure, which provide it a strong position against the competition. I also believe that further innovation, new technological advantages related to CompleteTM and CompuSafe services, and further investments in infrastructure will most likely bring FCF margin improvements. Additionally, new acquisitions at beneficial valuations like that of NoteMachine could also accelerate FCF growth. Finally, further acquisition of its own shares and dividend increases may also bring the attention of investors. There are risks associated with successful acquisitions, integrations, the uncertainties related to obtaining financing, or changes in the regulatory framework, however I believe that The Brink's Company is quite undervalued.

For further details see:

The Brink's Company: Dividend Increases, Innovation, And M&A Imply Undervaluation