BCO - The Brink's Company: Multiple Contraction Overdone

2023-04-11 12:09:38 ET

Summary

- The Brink's Company offers cash and valuables management, commercial security, and payment services in the US and globally.

- Brink's reported an 8% increase in FY2022 sales with 12% organic growth, and a 17% YoY increase in reported EBIT.

- In FY2023, I expect the company to beat analysts' EPS expectations for a number of reasons.

- With a projected EPS of $6.65 [mid-range], BCO stock should trade at $79.8 by year-end, implying an upside potential of 22.4%.

The Company

According to Seeking Alpha, The Brink's Company (BCO) is a security company that operates in various regions globally, including North America, Latin America, and Europe.

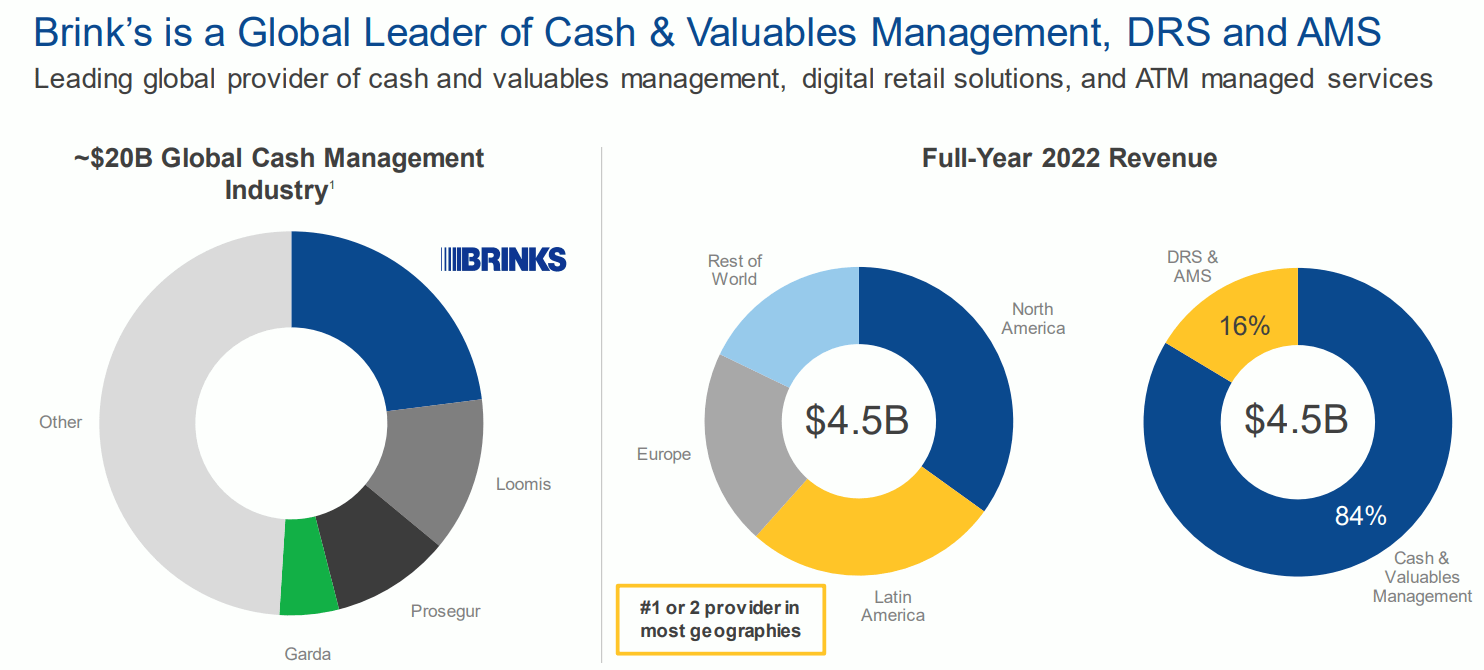

Under its "Cash and Valuables Management" services [84% of total revenues in 2022], BCO provides cash and valuables management services, including transportation, storage, counting, and sorting of cash and high-value commodities, as well as guarding, commercial security, and payment services. The company serves banks, financial institutions, retailers, government agencies, mints, jewelers, and other commercial businesses.

Also, The Brink's Company provides two other services - Digital Retail Solutions ((DRS)) and ATM Managed Services ((AMS)) - 16% of total sales in sum. DRS helps customers access cash deposits faster using technology-enabled devices and software platforms, while also providing customer analytics and visibility. AMS provides complete ATM management solutions, including cash forecasting, remote monitoring, and installation services.

Being founded in 1859 and headquartered in Richmond, Virginia, The Brink's Company has become one of the global leaders in its niche:

JPM's Conference, BCO's IR materials

{kind=link}

Due to the large number of services the company provides to its customers, its management reports 4 regions as business units: North America [34.7% of total sales], Latin America [26.2%], Europe [22.1%], and Rest of World [17%].

In North America, they operate in the US and Canada, including their Brink's Global Services [BGS] line of business. In Latin America, they have operations in countries where they have an ownership interest, including BGS services. In Europe, their operations primarily provide services outside of the BGS line of business. The Rest of World segment includes operations in the Middle East, Africa, and Asia, as well as BGS services in European countries and Latin American countries where they do not have an ownership interest.

BCO's Q4 2022 IR presentation, author's notes

{kind=link}

Latest Financials

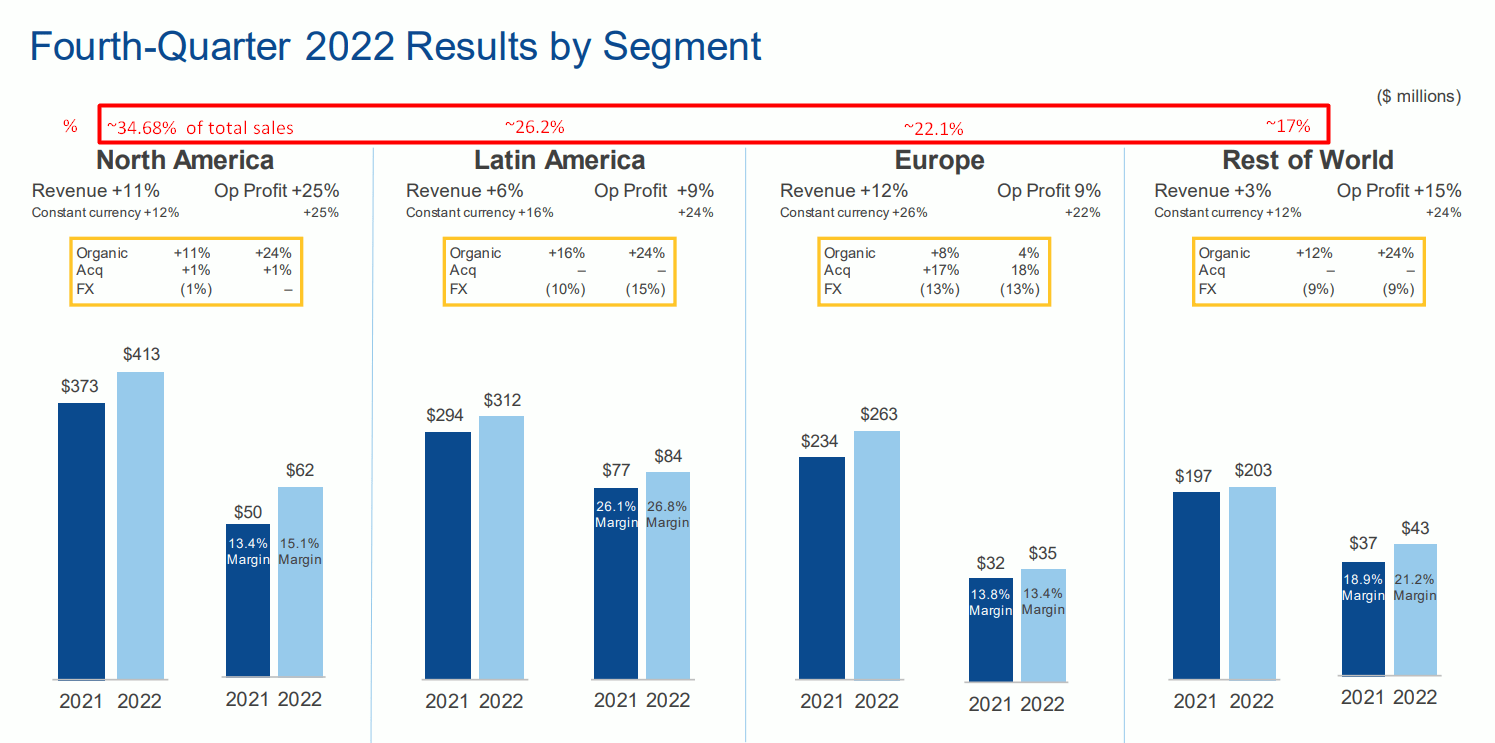

You have already seen from the chart above that the company's revenue in all 4 segments grew in 2022; while BCO's EBIT margins improved significantly across its business units. As it goes from the latest earnings call , the company was able to maintain strong pricing discipline and grow operating profit margins and EBITDA margins by 90 and 110 basis points for its DRS and AMS revenue streams, respectively. Their EPS for the year amounted to $5.99, an increase of $1.24 per share over FY2021. BCO generated $203 million in free cash flow [FCF] and prioritized share repurchases and the acquisition of NoteMachine. In Q4 FY2022, the company reported organic revenue growth of 12%, and North American operating profit margins were the highest in the segment's history. Adjusted EBITDA margins were above 20% for the first time in the company's history, benefiting from growth in high-margin businesses and aggressive cost-efficiency measures, according to the management.

For the full year 2022, The Brink's Company reported an 8% increase in sales, including the impact of foreign currency translation during the year [Argentinian peso was a headwind]. On a constant currency basis, sales increased 14%, with 12% organic growth and 2% from M&A activities. Reported EBIT increased 17% YoY, including negative currency effects of $45 million, while constant currency growth included organic growth of 23%. The company's $335 million revenue growth and $80 million operating profit growth added 24% to the margin and increased the overall operating margin to 12.1%.

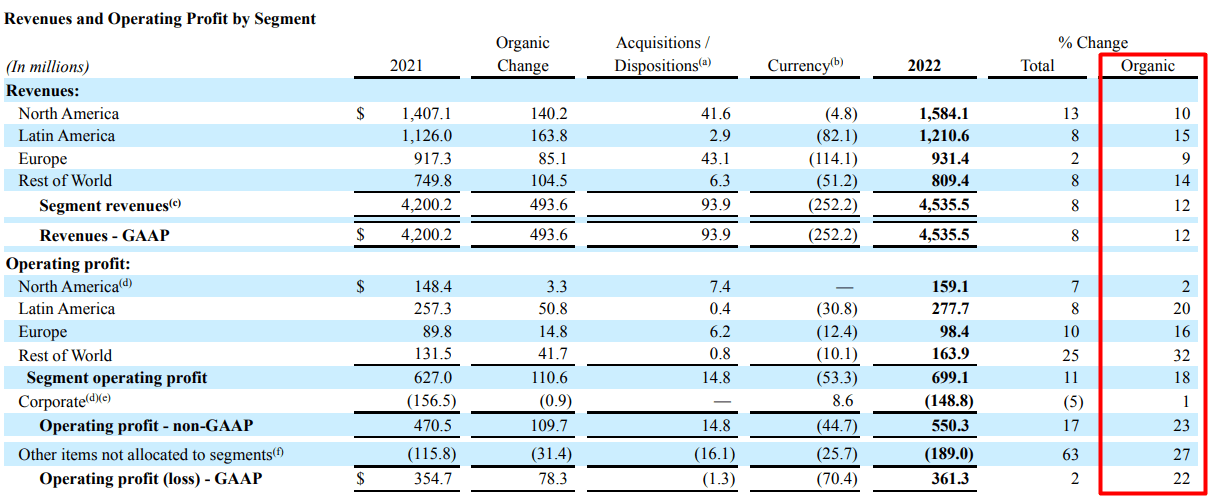

I think it's good that we can evaluate business growth using GAAP and non-GAAP measures [based on BCO's 10-K ]. This gives us a more accurate picture of the ongoing processes and the quality of the company's growth:

BCO's 10-K filing, author's notes

{kind=link}

As we can see, according to GAAP, the company showed EBIT growth of more than 20% with more than 2 times lower sales growth - a kind of operating leverage is created, thanks to which shareholders should theoretically get more value from a lower increase in production volume [in this case, a lower increase in the number of services provided].

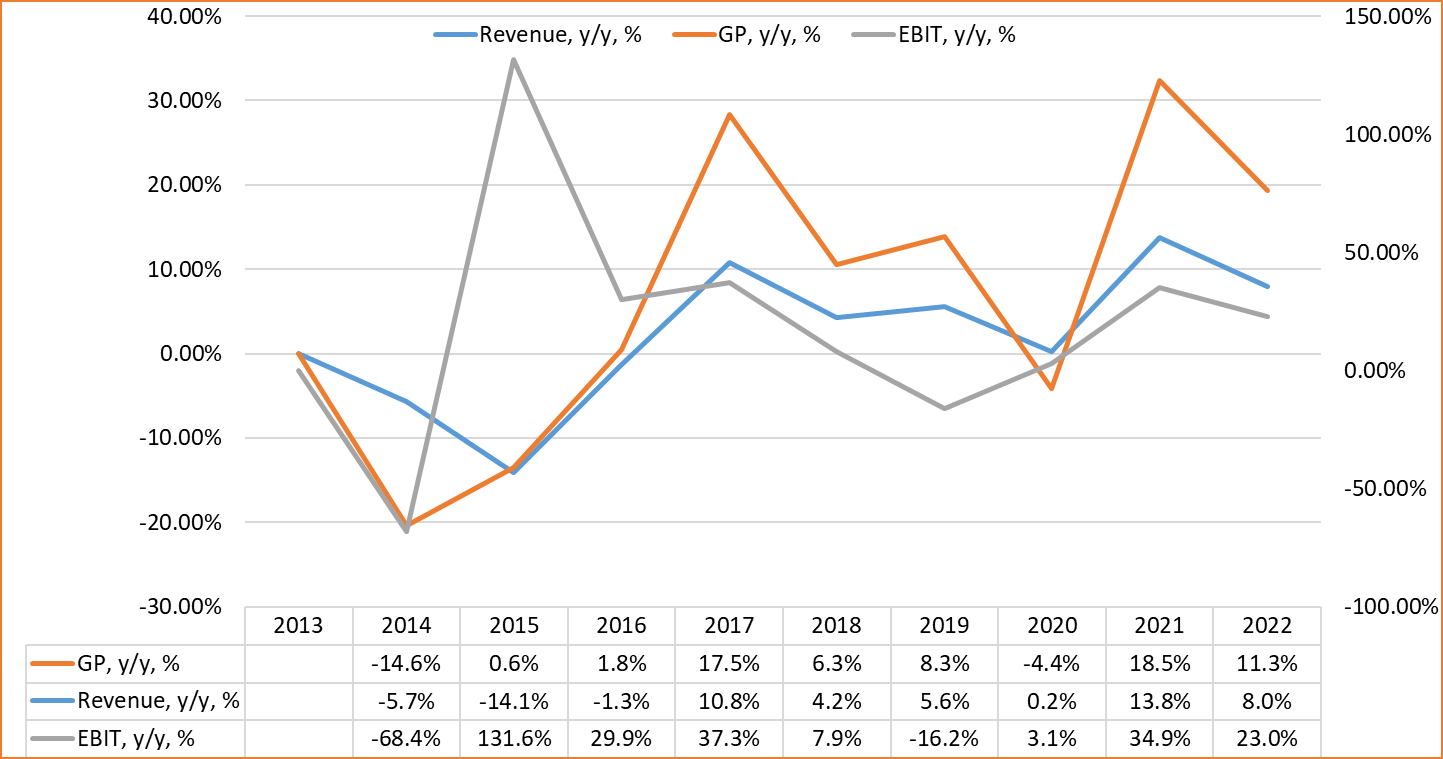

However, the operating lever also has a negative side - it can easily act in the opposite direction. This is exactly what happened in 2014:

Author's work, Seeking Alpha data

{kind=link}

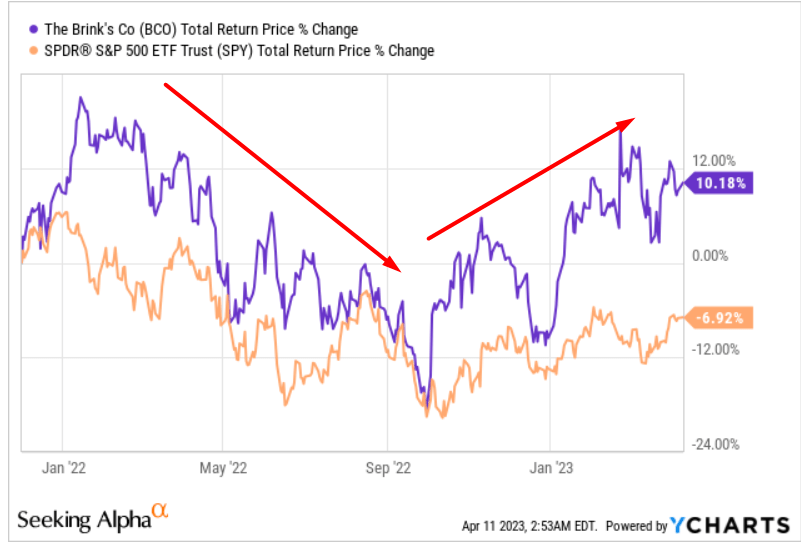

However, over the last 2 years, we have seen that leverage work in favor of BCO - if we take the company's first signs of a financial turnaround as the starting point from which an investor might decide to buy BCO stock, we can see a clear impact of that leverage on that same investor's overall profitability to date:

{kind=link}

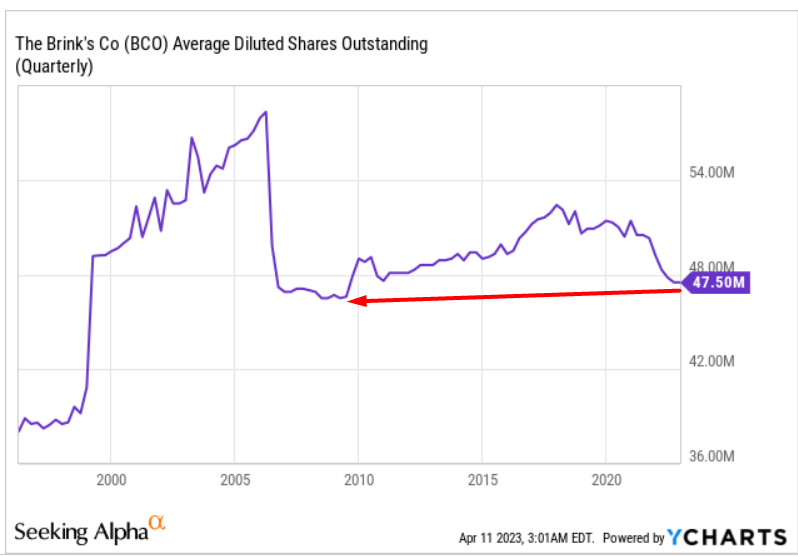

Now BCO costs about the same as it did before the GFC [2007-2008], while EPS, FCF, and revenue per share are higher by 40.7%, 116%, and 37.1%, respectively. You will say that there has been a dilution of share capital during this period - but that is not the case. BCO is at about the same share price level today as it was then.

{kind=link}

Over the past 3 years, BCO's management repurchased the company's common stock for $302 million and paid $105 million in dividends to shareholders.

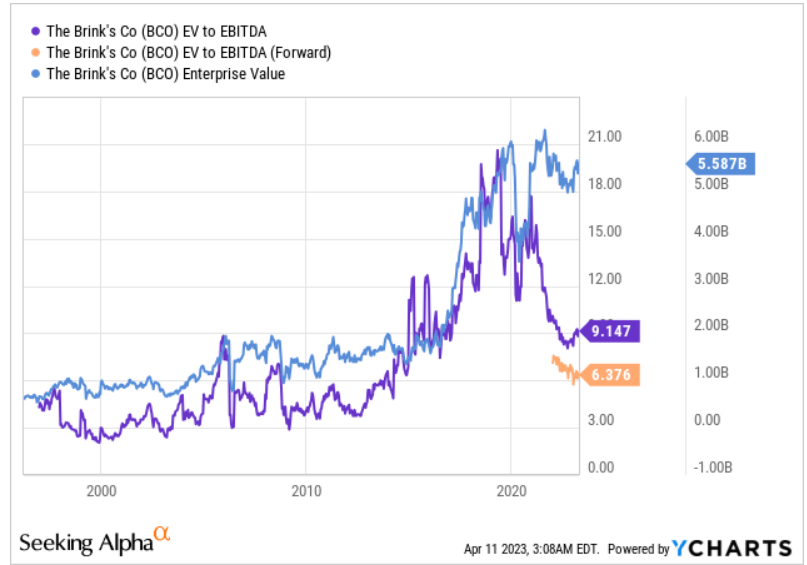

The problem lies in the discrepancy between the valuation of the company and the growth of its enterprise value:

{kind=link}

This may mean that Wall Street analysts are either afraid of high debt or do not believe in sufficient business growth in the foreseeable future - hence the valuation discount. Indeed, the debt on the company's balance sheet is now relatively high - especially compared to previous periods:

The management aims for a leverage ratio of 2-3x adjusted EBITDA. Currently, at 3.1x, they plan to reduce it to 2.6x by year-end using 2023 free cash flow. So I would caution those hoping for an expansion of the share buyback program - in Q4 2022 they already accounted for 12.2% of quarterly EBITDA.

However, I do not want to be too harsh on BCO's debt - operating income still more than covers interest payments, so I do not expect a big drop in net income, especially considering that its growth in FY2022 was mostly organic.

I suggest taking a closer look at the company's valuation and the market's expectations - perhaps BCO is currently mispriced?

Valuation & Expectations

Let's start with the management targets for FY2023:

Our 2023 guidance builds off a strong foundation developed in 2022. We're targeting organic growth between 7% and 11% , including continued strong growth in the DRS and AMS offerings. Operating profit is expected to improve by approximately 100 basis points through continued cost productivity and profitable growth in these higher margin lines of business.

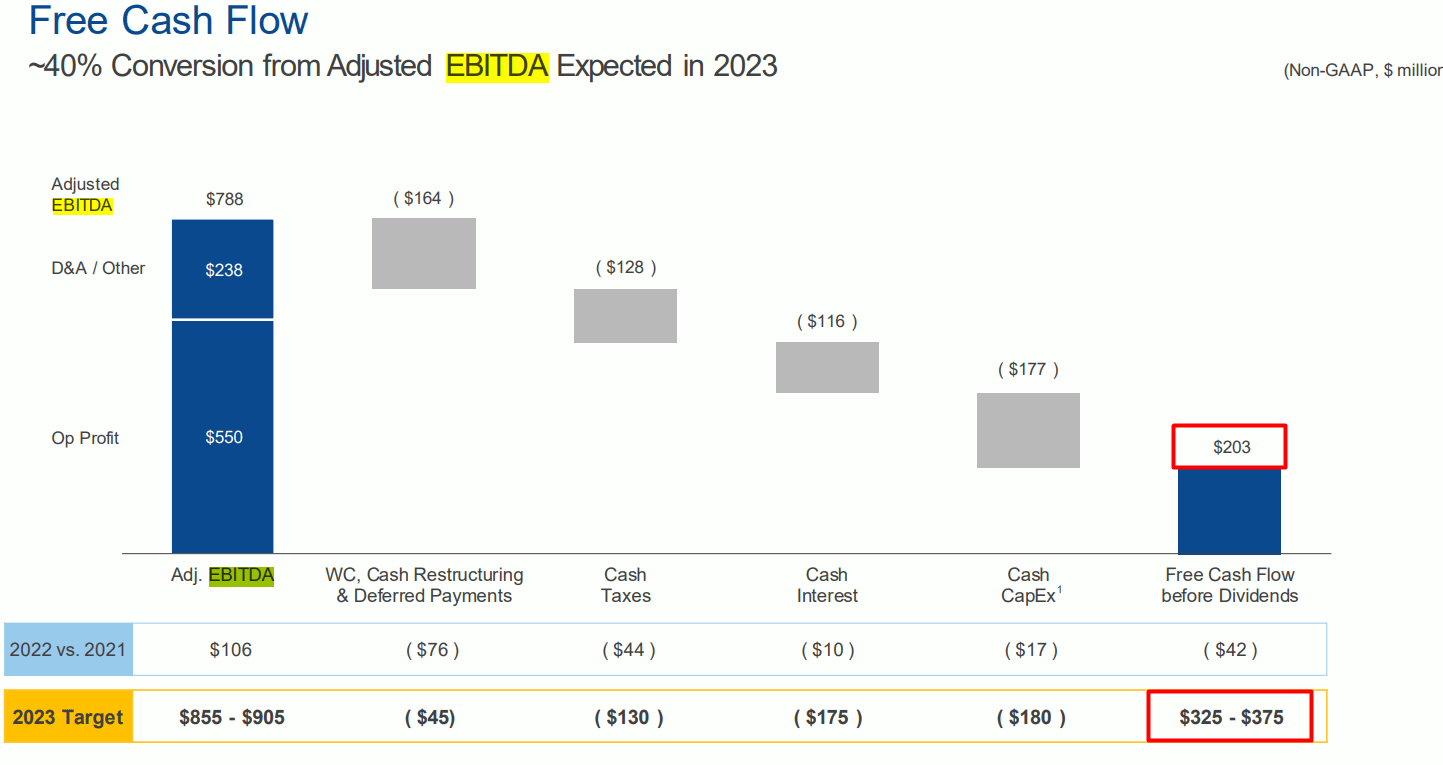

EBITDA is expected to be between $855 million and $905 million, with EPS between $6.30 and $7 per share . As always, we remain keenly focused on generating free cash flow. We expect significant improvement in free cash flow generation year-on-year to around 40% conversion of adjusted EBITDA , primarily through profitable growth and working capital improvements.

Source: Earnings Call, emphasis added by the author

If BCO revenue grows 9% in FY2023, EBIT is expected to be $439 million with a 100 basis point margin increase, up 22.8% from last year. At the same time, management indicates an adjusted EBITDA of $880 million [mid-range], up 11.8% year-over-year. Due to higher FCF conversion and lower restructuring costs, BCO's FCF in FY2023 is expected to grow 77% in the middle of the forecast range, based on my calculations.

BCO's Q4 2022 IR presentation, author's notes

{kind=link}

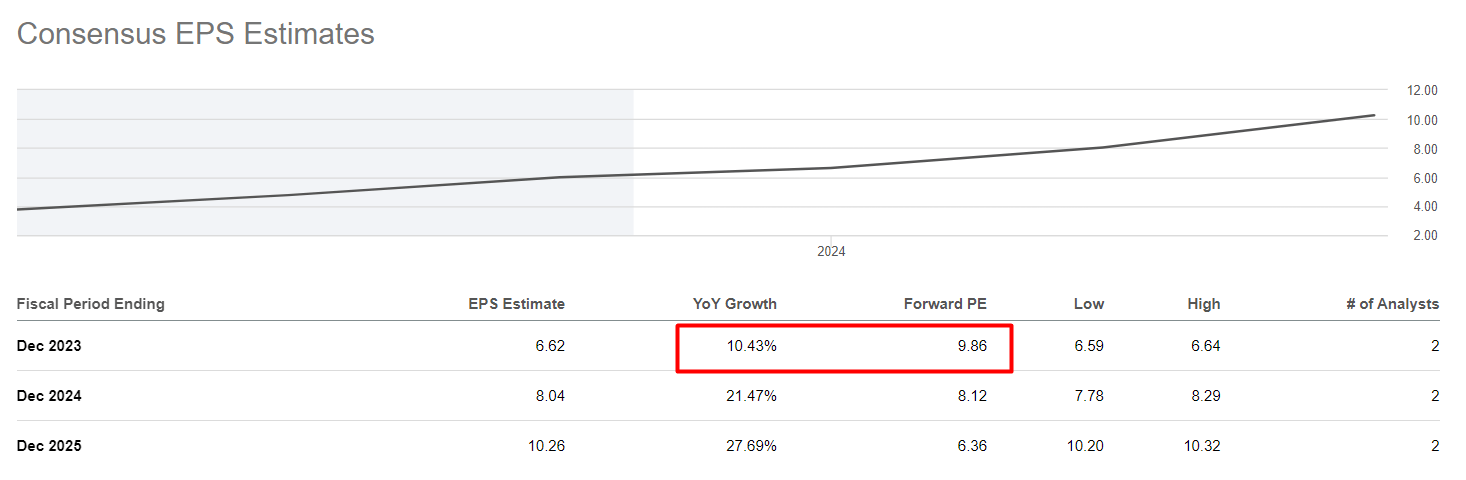

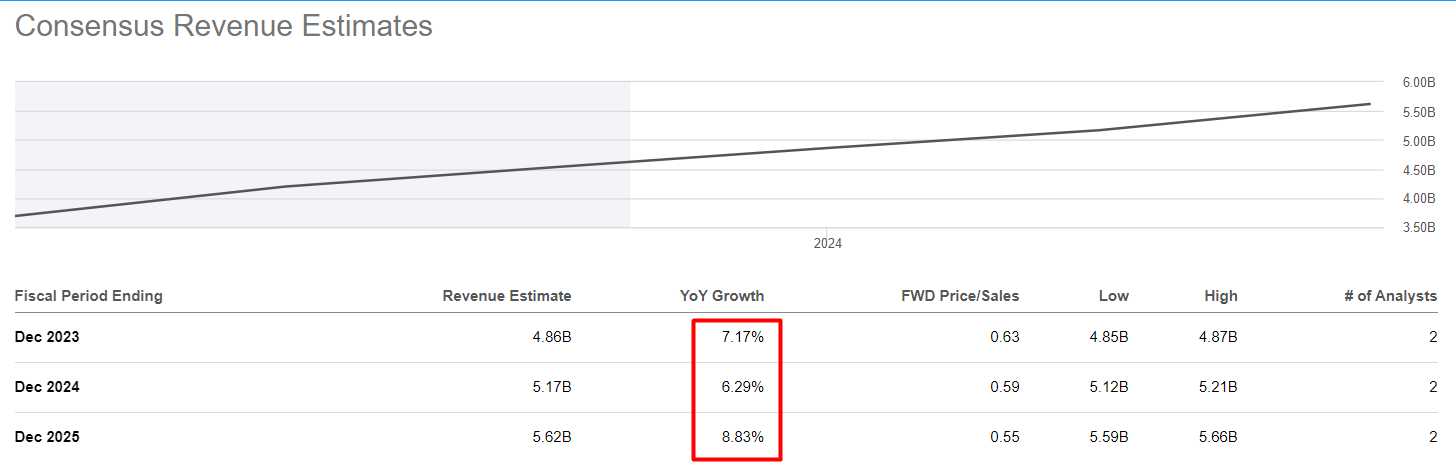

At the same time, analysts see very low earnings per share growth in FY2023 - just 10.43% year over year - combined with lower-than-expected revenue growth [compared to the management's guidance].

Seeking Alpha, author's notes Seeking Alpha, author's notes

{kind=link}

{kind=link}

The market expects EPS to be 0.45% below the mid-range indicated by management. At the same time, the predicted adjusted EBITDA should be two times higher than the forecast EBIT - I think BCO will be able to beat the consensus EPS forecast, and in some ways even exceed management's expectations, on the back of such a good FCF conversion and subsequent cost optimization, as mentioned earlier.

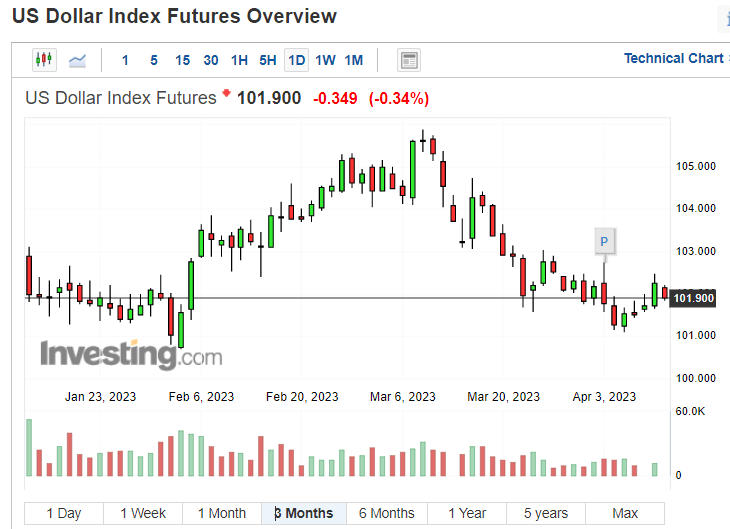

You also need to keep in mind that overall, more than 65% of all revenue generated by the company is not generated in North America - the U.S. dollar index ( DXY ) has come under severe pressure in recent months, which will give BCO additional tailwinds to beat its upcoming Q1 2023 earnings projections:

Seeking Alpha, author's notes Investing.com

{kind=link}

{kind=link}

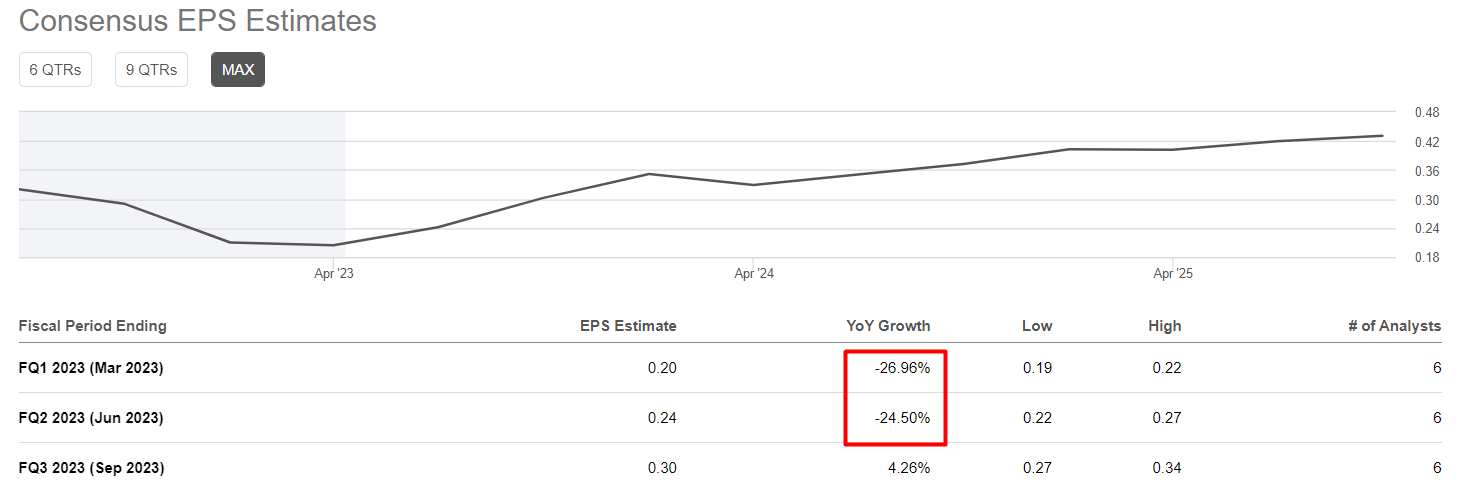

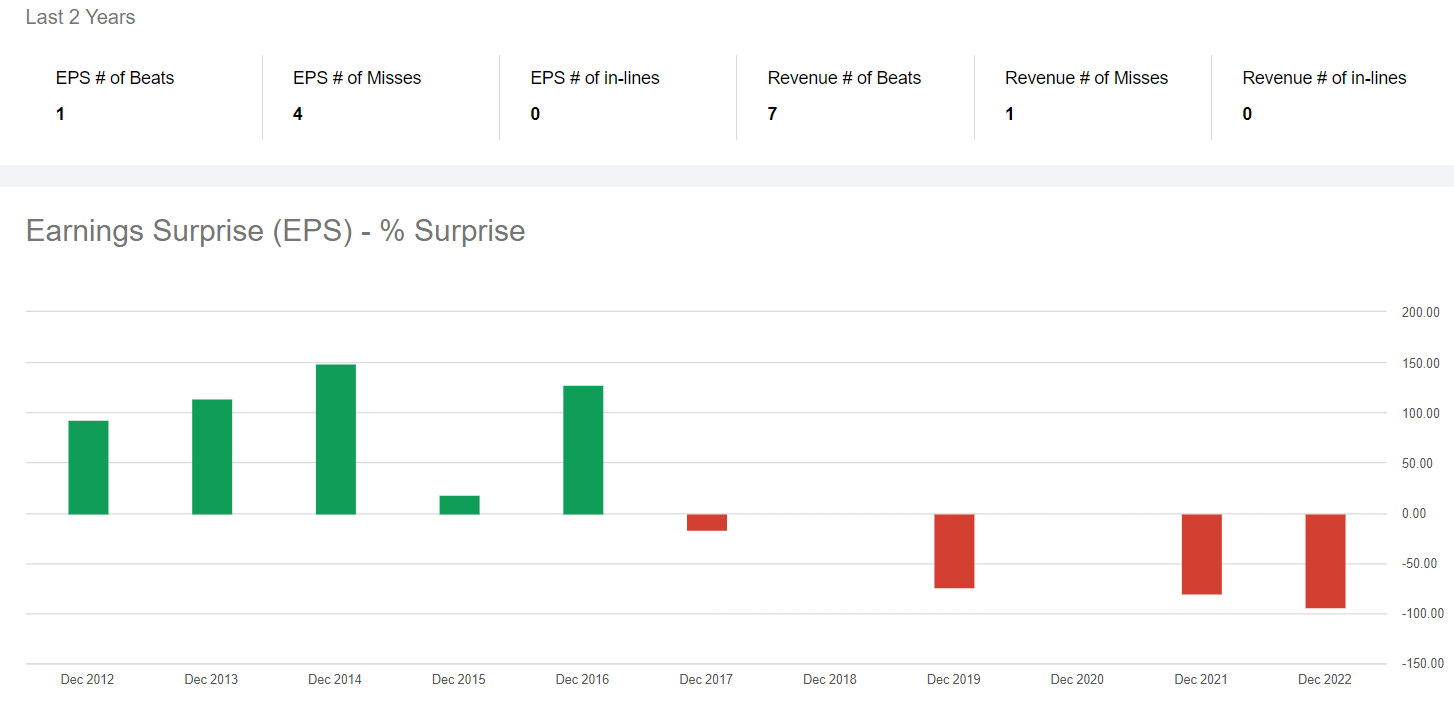

All this should break the series of earnings misses at the end of this year:

Seeking Alpha, BCO's Earnings Surprises

{kind=link}

Summary Thesis

Of course, there are certain risks associated with investing in The Brink's Company stock including economic conditions, competition, security & regulatory risks, currency exchange rate fluctuations, acquisitions and integrations, and dependence on key customers. These factors could negatively impact the company's financial performance and profitability in FY2024 and beyond. Remember, analysts believe FY2023 will be challenging for the company, but FY2024 and FY2025 will have above-average performance, which is far from certain right now.

While the company's increased debt also appears to be a risk factor weighing on valuation, I do not see major risks to BCO given the expected change in the company's FCF profile in FY2023. We saw a sharp decline in multiples in FY2022, such that forward multiples are now almost double TTM ones. I believe that BCO stock should not trade at 9x earnings, but at least 12x, given the slight discount in debt to the industry median, which is 16x according to Seeking Alpha data . With projected earnings per share of $6.65 [mid-range], BCO should trade at $79.8 per share by year-end, implying an upside potential of 22.4% from the previous trading day's close.

Thank you for reading!

For further details see:

The Brink's Company: Multiple Contraction Overdone