SAEF - The Brink's Company: Revisiting The Bullish Case

- Since the beginning of this bear market, BCO has been one of my few bullish recommendations.

- The firm is trading at less than 9x forward FCF, despite high-single digits growth and buybacks.

- BCO is now in a better position than at the beginning of the year to weather a credit event, especially since management extended debt maturities.

- I believe that BCO continues to provide an attractive risk-reward opportunity.

Investment Thesis

The Brink's Company ( BCO ) has been one of my few bullish recommendations since the start of this bear market. While the stock corrected in line with what we have broadly seen in equity markets so far this year, it failed to bounce in recent weeks despite strong earnings, leading me to believe that there continues to be a positive risk-reward opportunity at the current market price. The stock trades at less than 9x forward free cash flow ("FCF") while the business is growing at a high single-digit rate and management is doing buybacks. The high amount of leverage was one of my concerns, but the firm successfully extended its maturities and is now in a better position to enter this tightening cycle. In terms of valuation, I continue to believe that the stock is trading at a significant discount compared to its intrinsic value.

A Quick Update Following Q2 FY22 Results

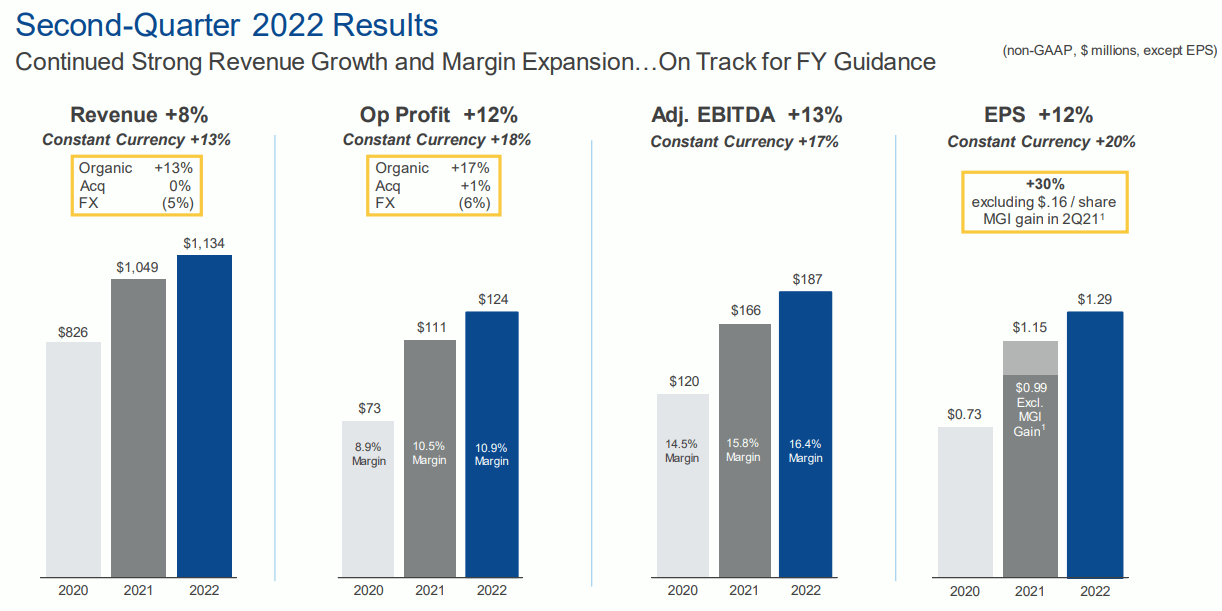

BCO published Q2 FY22 earnings on August 3rd, 2022. Sales increased by ~8.1% YoY to $1.13 billion in the most recent quarter, which is in line with the historical growth rate. The firm generated $266.4 million in gross profit, compared to $229.6 million in the same quarter last year, for a gross profit margin of ~23.5% and ~21.9% respectively.

{kind=link}

I was impressed to see that BCO managed to maintain high margins, despite FX headwinds. Both the LTM gross and operating margins remain near a record high of ~23% and ~8.5%, respectively. However, I believe it's important to keep a cool head and be open to the possibility of lower margins over the next quarters. After all, the business shows cyclicality over a long period of time, and given where we are in the business cycle, I believe the probability to have lower margins from here is higher.

{kind=link}

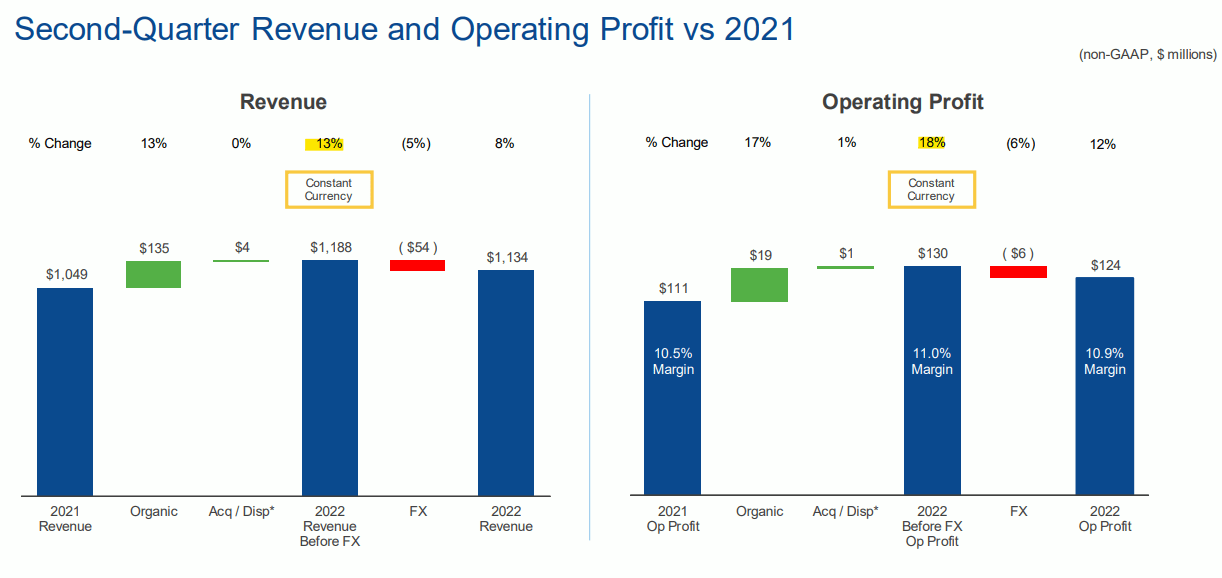

Talking about FX headwinds, revenue grew at ~13% in constant currency, which is higher than the historical average. It's encouraging to this positive evolution, which shows in my opinion that cash remains a valuable medium of exchange. On top of that, I expect revenue growth to remain elevated, especially once the dollar rolls over.

{kind=link}

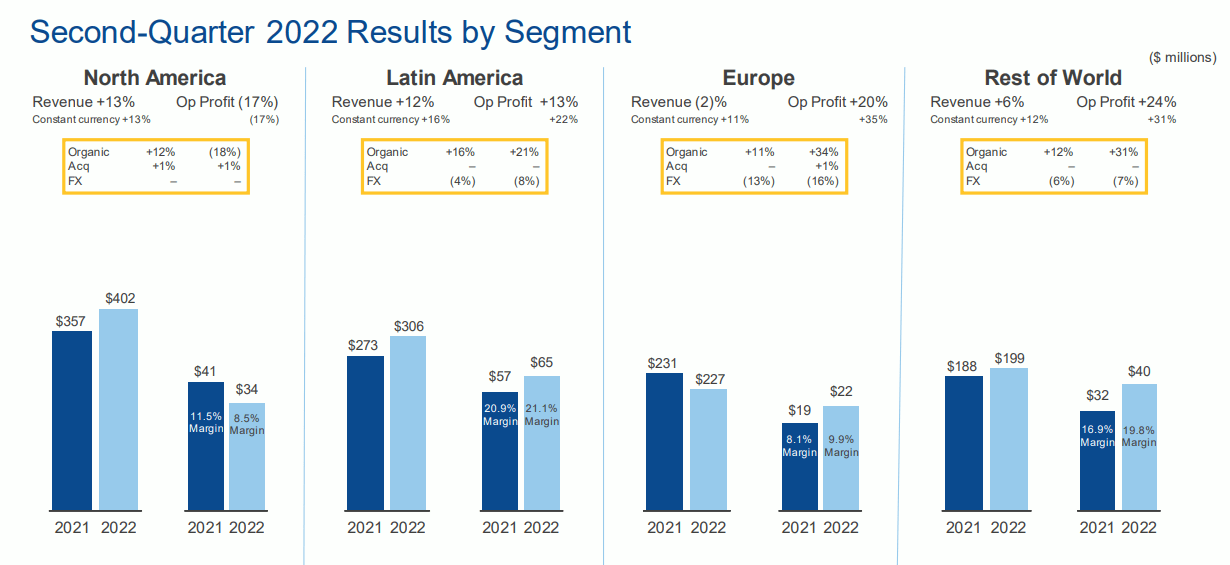

Every segment showed positive revenue growth in Q2 FY22, with the exception of Europe (because of FX). Operating profit per segment remains in line with previous quarters, which shows that business remains healthy.

{kind=link}

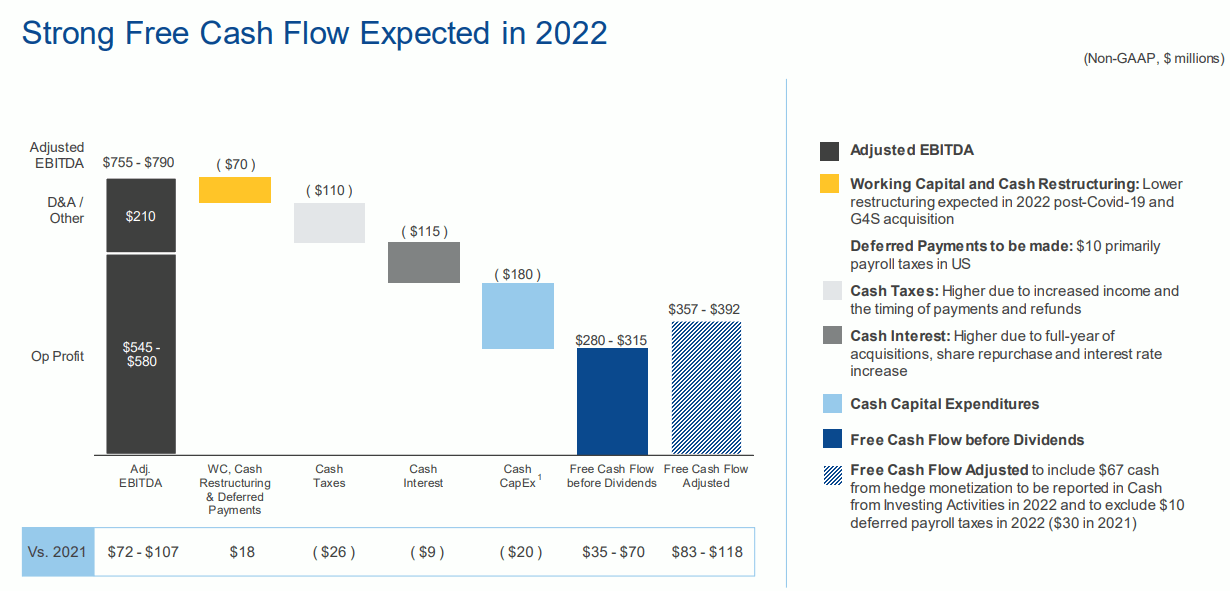

Management reaffirmed its FY22 free cash flow guidance of $280-315 and now sees adjusted (excluding deferred payroll taxes) FCF ~23% higher, which is another positive development in my opinion. Wall Street FY22 EPS estimates are now at $5.77 and are expected to reach $8.16 in FY24, growing at over 15% annually. Given BCO's forward P/E of ~10, I believe the stock is attractively valued, trading at a PEG ratio of less than 1.

{kind=link}

In my previous articles on BCO, I have raised the issue of leverage, especially in the event of a credit crunch when the firm needs refinancing. While this issue persists, management took the right step in rolling over part of their debt, resulting in an extended credit facility and maturities. Paying down debt doesn't seem to be an immediate priority for management as they continue to be focused on returning capital through dividends and share buybacks. Overall, I believe BCO had a good quarter, which is reflected in management's full-year expectations.

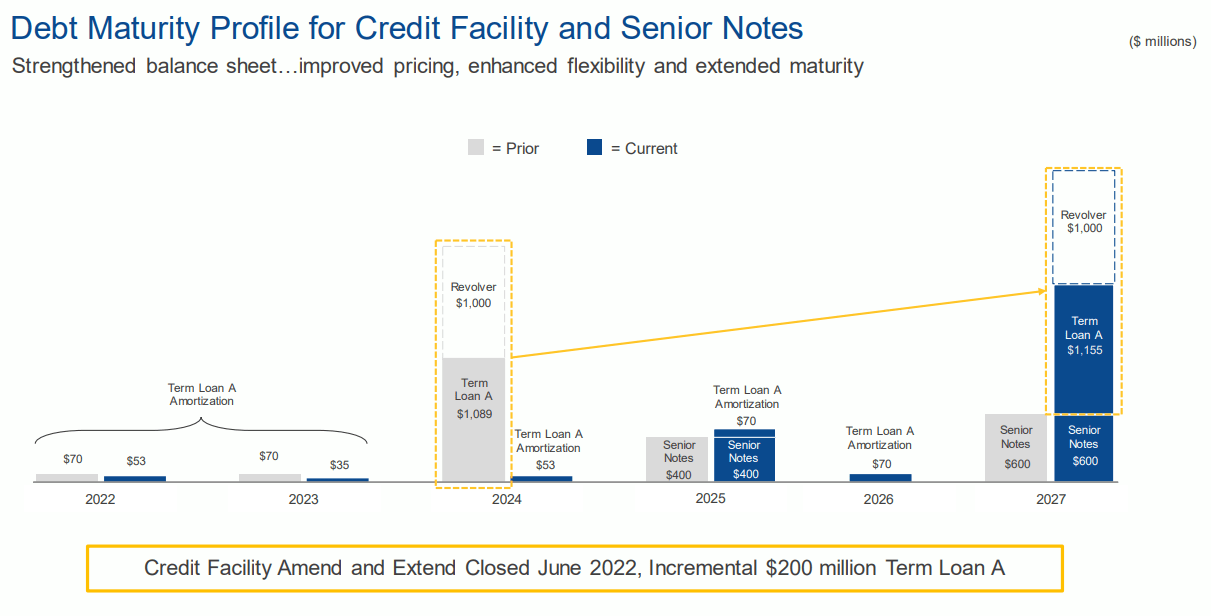

Moving to our debt maturity profile on slide nine. In the second quarter 2022, we amended and extended our credit facility. We retained $1 billion revolving credit facility and we expanded our term loan A by $200 million to $1.4 billion. The amended facility reduced our used pricing grid by 25 bps and is expected to provide significant interest expense savings going forward.

Maturity was extended out five years and meaningfully expanded our capacity to make restricted payments, including share repurchases. On this slide the light gray bars reflect our debt maturity before the amendment extend and the dark blue bars afterward. Our 5.5% senior notes mature in July 2025. And otherwise, we have no material debt retirement obligations until 2027.

Mark Eubanks - President & Chief Executive Officer - Q2 FY22 Earnings Call

{kind=link}

Company Valuation

In this part, I will update my discounted cash flow ("DCF") model to reflect some of my latest assumptions on BCO. Based on 47.8 million shares outstanding, and a price of $57.3 per share, the company now has a market cap of approximately $2.74 billion. In light of recent results, I have made the following adjustments to my model

- Estimated free cash flow for FY23 of $320 million - ~$20 million (~6.6%) higher than in May 2022.

- A growth rate of 7% until FY26 - unchanged.

- A 2% terminal growth rate - unchanged.

- A discount rate of 9% - unchanged.

{kind=link}

According to my model, the fair value of the stock is around $108 per share, ~14% higher than my previous estimate. While the spread between my intrinsic value estimate and the market price is relatively high, I believe that investors need to be cautious given where we are in the cycle and should factor in the possibility of lower-than-expected results stemming from weaker margins. On the other hand, there are other catalysts such as buybacks excluded from my valuation model that can enhance shareholders' returns. All in all, I see a positive risk-reward opportunity in BCO at the current market price.

Key Takeaways

Since the beginning of this bear market, BCO has been one of my few bullish recommendations. The firm is trading at less than 9x forward FCF, despite high single-digits growth and buybacks. BCO is now in a better position than at the beginning of the year to weather a credit event, especially since management extended debt maturities. In terms of valuation, the stock is priced at a considerable discount to its intrinsic value. As a result, I believe that BCO continues to provide an attractive risk-reward opportunity.

For further details see:

The Brink's Company: Revisiting The Bullish Case