BCO - The Brink's Company: The Cash Is Secure But Your Returns May Not Be

2023-04-19 00:13:43 ET

Summary

- The secular trend of the world going cashless is BCO’s biggest challenge.

- They have significant market share, but the size of the pie is slowly shrinking.

- The company is definitely valued on an intrinsic basis.

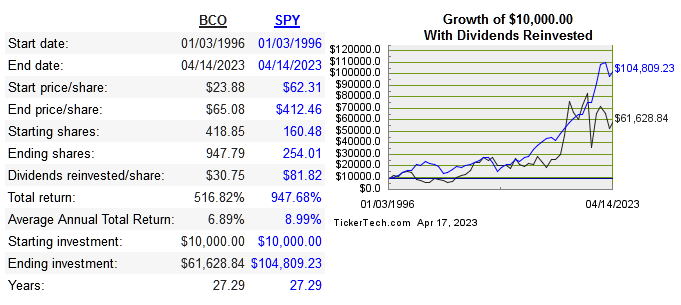

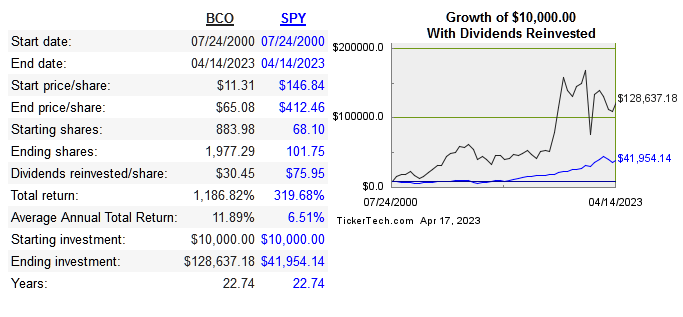

The Brink’s Company ( BCO ) is the largest cash management business in the world. Originally founded in 1859, they IPO’d in 1996. Below is BCO stock performance since IPO, followed by performance since lowest stock price.

{kind=link}

{kind=link}

Their operating segments break down into cash & valuables management, digital retail solutions, and ATM managed services:

Brink's investor presentation

Below we see some of the key metrics to the business:

| Company |

| Revenue 10-Year CAGR |

| Median 10-Year ROE |

| Median 10-Year ROIC |

| EPS 10-Year CAGR |

| FCF/Share 10-Year CAGR |

| BCO |

| 2.4% |

| 8.1% |

| 1.5% |

| 6.9% |

| 29% |

| [[LOIMF]] |

| 3.1% |

| 18.9% |

| 10.9% |

| 5.1% |

| 12.7% |

| [[PGUCY]] |

| -0.3% |

| 40.8% |

| 11.5% |

| -8/3% |

| n/a |

ROE has been incredibly high the past two years, but ROIC hasn’t had a corresponding increase. While earnings have been higher than usual, the increased debt load along with increased buybacks (both reduce equity) is mostly what drives up the ROE. If we omit the past two years ROE, then the average would be much lower as well.

Revenue peaked in 2004 at 4.7 billion, and hasn’t gotten close to this number again until more recently. This year and last they hit record highs in EBIT and FCF, which is good news, but the top line has essentially been flat for decades now.

Capital Allocation

Below we’ll look at BCO’s operating profit, FCF, and how they allocate it.

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| EBIT |

| 172 |

| -28 |

| 57 |

| 144 |

| 274 |

| 275 |

| 235 |

| 214 |

| 355 |

| 361 |

| FCF |

| 24 |

| 5 |

| 108 |

| 55 |

| 78 |

| 209 |

| 204 |

| 199 |

| 310 |

| 297 |

| Acquisitions |

| 18 |

| 5 |

| 15 |

| 1 |

| 224 |

| 513 |

| 173 |

| 442 |

| 313 |

| 174 |

| Debt Repayment |

| 27 |

| 81 |

| 676 |

| 645 |

| 1,187 |

| 715 |

| 1,196 |

| 1,122 |

| 2,978 |

| Dividends |

| 19 |

| 19 |

| 20 |

| 20 |

| 28 |

| 30 |

| 30 |

| 30 |

| 37 |

| 37 |

| Repurchases |

| 94 |

| 50 |

| 200 |

| 52 |

We can see that they regularly pay a dividend and make mostly smaller acquisitions. Share count has remained mostly unchanged over the years, but lately a bit more emphasis on repurchases had been employed.

Risk

The biggest risk by far is secular in regards to the world becoming more and more cashless.

eMarketer Bloomberg

BCO does have a bit of diversity with their other two segments. They finally sold the home security segment in 2020 to ADT. Nevertheless, the core business is destined to shrink over time, and these other portions of the business won’t be enough to replace what will be lost.

They’ve had strong FCF for the past few years, but the plain fact remains that cash transactions will continue to decline over time. I don’t have a clear forecast to provide a rate of decline to expect, but I do know that superior market share means little when the overall pie is shrinking. This is a major red flag as a potential long term investment.

I would prefer to see a company in Brink's situation dedicating a portion of FCF to buying common stock in the companies that benefit from digital transactions such as V, or MA. This would provide a hedge against the decline of the legacy business.

Long term debt is currently at $3.5 billion and the cash balance is $972 million. This does add extra risk for me, as I generally avoid companies that are so leveraged. As I mentioned earlier, the debt levels also drive up the ROE metric, which makes the quality look better than it really is.

Valuation

The secular risk mentioned above certainly ties into my valuation. It would be one thing if the legacy business was merely growing slowly, but its current decline is destined to continue. This will obviously play a part in my projections of EPS growth.

First we’ll look at the multiples comp, followed by historical price multiples.

| Company |

| EV/Sales |

| EV/EBITDA |

| EV/FCF |

| P/B |

| Div Yield |

| BCO |

| 1.2 |

| 8.3 |

| 17.6 |

| 5.3 |

| 1.2% |

| LOIMF |

| 1 |

| 5.1 |

| 12.4 |

| 1.9 |

| 3.4% |

| PGUCY |

| 0.8 |

| 4.3 |

| 8.3 |

| 7.6 |

| 2.7% |

Macrotrends Macrotrends Macrotrends

I do think it’s important to not look at this as a security you are analyzing, look at it as if you were a private buyer of this entire business. Assuming you are the owner, FCF is what the enterprise spits out each year, so you have to decide how much you would pay in exchange for the FCF. Paying 17 times FCF for BCO doesn’t look appealing since I expect a gradual decline in free cash as a result of the secular risk. Also, more of that capital will need to be devoted to paying down the increased debt levels.

This is why I like EV/FCF as far as multiples, but next I’ll provide my basic DCF model.

Moneychimp

On an intrinsic basis I think the company is clearly overvalued at around $66 dollars a share currently.

Conclusion

BCO is an example that shows us that having the largest slice of the pie in an industry doesn’t necessarily mean there is a moat. The obvious roadblock ahead for this company is the cashless trend worldwide.

At the end of the day, the service this business provides is a commodity that can be done by anyone with the capital to do so. Their brand power is worth something, and the longstanding relationships they have with clients are also worth something. This doesn’t mean they have a real economic moat though, and the easiest proof of this is that they have produced inconsistent returns on invested capital for many years now.

I think it's unfair to call BCO a low quality business, but it is average at best, and definitely not worth investing at the current price.

For further details see:

The Brink's Company: The Cash Is Secure But Your Returns May Not Be